PACWP - PacWest Preferred Shares: Size Matters

2023-03-22 06:53:44 ET

Summary

- PacWest is a bank holding company with over $41 billion in assets headquartered in Los Angeles, California.

- PACWP is the Series A preferred shares from PacWest.

- The preferred shares are currently priced at $13/share versus a $25/share liquidation price.

- PACW has a very transparent, straightforward balance sheet with no outside risks such as crypto.

- The potential liquidity backstop needed here is small from a dollar figure perspective, and the bank has already raised $10 billion in cash.

Thesis

PacWest ( PACW ) is a California banking institution with over $41 billion in assets, headquartered in Los Angeles. The bank has been caught up in the recent regional banks crisis, being down over -54% in the past three months. The banks has a Series A 7.75% fixed rate non-cumulative perpetual preferred shares series ( PACWP ) outstanding:

{kind=link}

In this article we are going to have a more detailed look at PACW's balance sheet and assess if the bank is in a good position to survive the current crisis, as well as assess the viability of investing via the preferred shares.

We are of the opinion that many of the regionals which have come under the gun, even if they do survive, will be much less profitable institutions going forward. Regional banks will be forced to do two things: 1) increase the rate they pay on existing deposits to keep clients, 2) come up with backstop liquidity sources, which will cost money. Both actions will incur a negative drag on net interest margins. Therefore, in our minds the common equity play is not necessarily a smart move by retail investors at the moment.

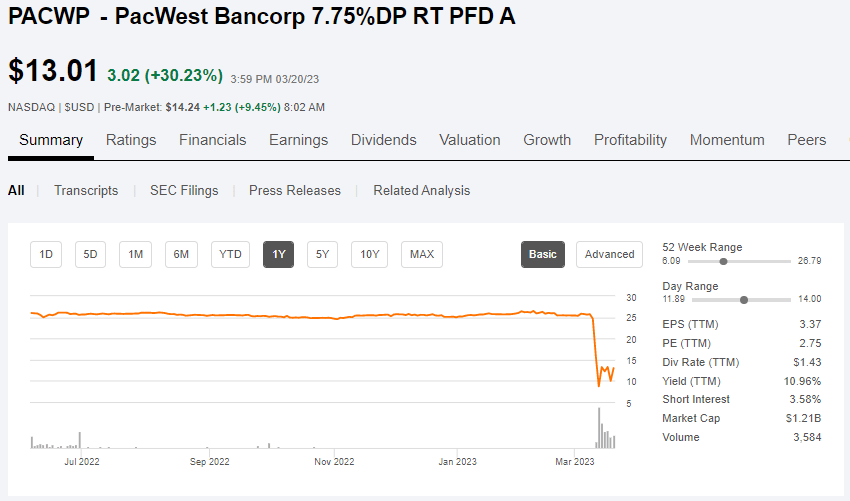

The fixed rated Series A preferred shares for PACW, on the other hand, offer almost 100% upside if the bank survives:

{kind=link}

The preferred shares are currently priced at $13/share versus a $25/share liquidation price. Generally preferred equity is a rates play, acting more like a fixed income security, but in cases of distressed companies they tend to trade like the equity (i.e. implying that a bank run can wipe them out).

How does the Pacific Western Bank balance sheet look like?

Let us better understand this entity by looking at the bank's balance sheet:

{kind=link}

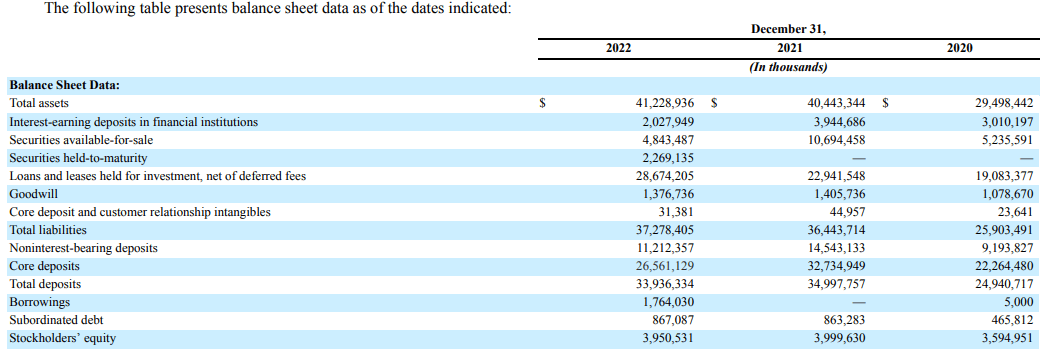

This is a small bank by any means - only $41 billion in assets. Also when parsing out the asset side of the balance sheet we can see the entity is overweight pure commercial loans which stand at $28 billion, versus an investment portfolio of $7 billion. The investment portfolio is split between $5 billion in available for sale and $2.2 billion in held to maturity. To note the bank reclassified the securities now held in HTM from AFS last year. Presumably as the value went down they wanted to limit the OCI impact.

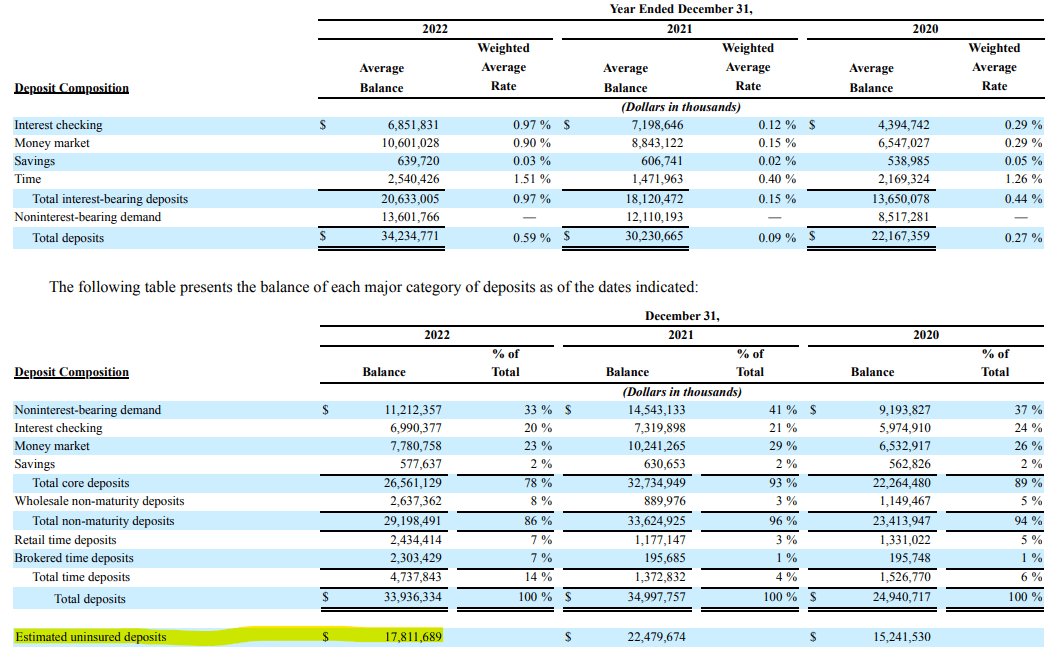

On the deposit side the bank has around $17 billion in uninsured deposits:

{kind=link}

It is interesting to note that figure went down from 2021. Currently the uninsured portion is around 50% of all deposits, but more importantly it is fairly small on its own. $17 billion is 'small' just because it represents a sum that many players in financial markets can inject in an entity in order to take it over. It is very small especially when compared to the $30 billion that a number of major banks injected into First Republic Bank ( FRC ) last week as deposits in order to stem the crisis.

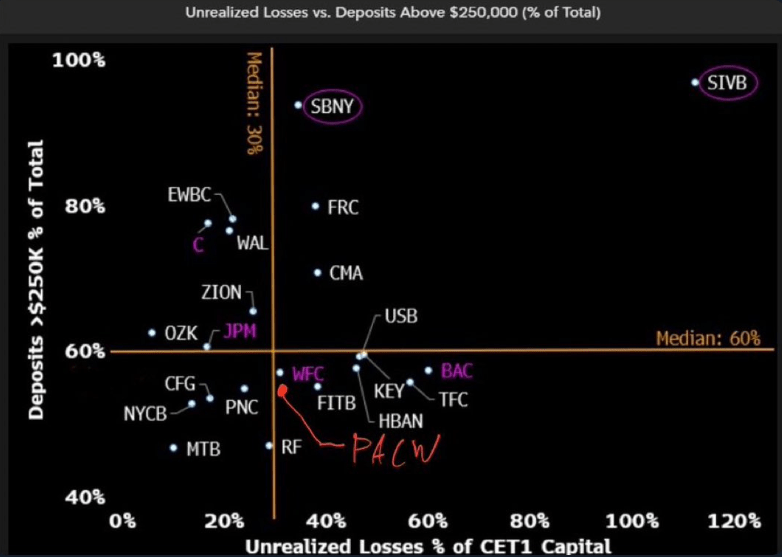

How does PACW compare to the other banks?

We have a nice comparison graph here, courtesy of Mr. Burry :

{kind=link}

The PACW name is scribbled there by him, not us.

We are not going to mince our words - we like PACW. We think it has a nice, classic commercial and residential loan portfolio (two thirds of assets) and a small investment portfolio (20% of assets) which does not have unbearable unrealized losses. Most importantly the bank is small as a total dollar figure, and the uninsured deposit amount is also fairly small (in dollars).

We like clean, understandable balance sheet with no 'noise'. In Signature's case the 'noise' was its crypto business (the bank faced a criminal probe before its collapse), while SVB acted more like a hedge fund via its tech investments and massive bets on the treasury curve. None of that here.

PACW got swept in the crisis via its large uninsured depositor percentage, but it is doing something about it:

Company Release - 03/17/2023

LOS ANGELES, March 17, 2023 (GLOBE NEWSWIRE) -- Pacific Western Bank, the primary subsidiary of PacWest Bancorp (NASDAQ: PACW), today issued the following statement reaffirming its financial strength.

Pacific Western Bank continues to have solid liquidity, with over $10.8 billion in available cash as of March 17, 2023. Available cash exceeds total uninsured deposits. Following the announcement of the Silicon Valley Bank and Signature Bank closures, the bank experienced elevated net deposit outflows, concentrated primarily in our Venture Banking business line. Since Monday, March 13, 2023, net outflows have fallen sharply, with deposit balance fluctuations substantially stabilizing.

As of March 16, 2023, insured deposits exceed 62% of total deposits, including accounts eligible for pass-through insurance. Additionally, as of March 16, 2023, insured venture-specific deposits account for more than 77% of total venture deposits, including accounts eligible for pass-through insurance. The bank continues to have a diversified deposit base that includes commercial, community banking, homeowners associations, retail, and venture deposits, with venture deposits representing approximately 25% of total deposits as of March 16, 2023.

As previously disclosed, our risk-based capital ratios, including CET1, have been increasing for the past three quarters, including a tier 1 risk-based capital ratio of 10.61%, which is well in excess of regulatory requirements, as of December 31, 2022. Additionally, asset quality remains excellent, and the bank has experienced no significant asset quality changes since year-end, including classified assets, non-performing assets, and charge-offs.

Versus its Q4 2022 results, it looks like the bank has already experienced outflows, but the situation is stabilizing. With over 25% of the asset base now in pure cash, the balance sheet is starting to look like a fort. Furthermore, the bank is in talks for liquidity backstops . I think the bank is going to get them. It is not going to be cheap, but the dollar figures are small enough for people to inject them as needed. What is going to suffer? Profitability.

Conclusion

Pacific Western Bank is a California banking institution with over $41 billion in assets. The bank is small by any standards, and got swept into the current regional banks crisis via its high uninsured deposit percentage, which stood at 50% as of Q4 2022. The bank is a classic one, with a commercial and residential loan portfolio accounting for two thirds of assets, and a small investment portfolio accounting for 20% of assets. There are no tech company investments here, or associations with the crypto world. The bank has a clear-cut, transparent balance sheet with no outside risks. The institution has taken steps to address investors' concerns, raising its cash balance to $10 billion now, as well as working to arrange further liquidity backstops.

On a spectrum where we benchmark PACW with other banks based on uninsured deposits and unrealized losses, PACW fares well. We like what we see here - the bank has a transparent and straight forward balance sheet with no outside risks like crypto. Given its rather small size, the dollar figure associated with any liquidity injection is small, meaning the potential suitor pool is very large. We feel this is going to ensure the survival of the bank, albeit at a cost. The cost will be profitability. For a retail investor looking to double their money via a high risk play, the preferred shares ( PACWP ) offer almost 100% upside right now if the bank survives. We feel Pacific Western is going to make it through given the steps it has taken, and its small size.

For further details see:

PacWest Preferred Shares: Size Matters