PACW - PacWest: Speculative Buy Heading Into Q2 (Rating Upgrade)

2023-07-23 07:48:06 ET

Summary

- PacWest Bancorp could deliver a strong Q2 report on July 25, 2023 due to recovering deposit flows.

- The bank has seen a return of deposits after losing 17% in Q1, with $700M in deposit inflows reported after the end of the first quarter.

- PacWest Bancorp also sold assets in Q2 which provided additional liquidity and reduced lending risks.

- Despite being one of the riskier regional banks, I consider PacWest Bancorp a speculative buy ahead of its Q2 earnings release.

- The near-50% discount to BV seems exaggerated.

PacWest Bancorp ( PACW ) will report earnings for its second-quarter on Tuesday, July 25, 2023, and I believe the regional bank could be set for an outsized share price move to the upside due to recovering deposit flows and subsiding fears about the bank’s balance sheet. PacWest Bancorp was, and still is, one of the most heavily punished regional banks after Silicon Valley Bank failed in the first-quarter, and it still trades at an excessive discount to book value of nearly 50%. Since other regional banks, including Western Alliance Bancorporation ( WAL ) have made progress in restoring their deposit bases in the second-quarter, I believe PacWest Bancorp has considerable surprise potential on Tuesday.

Previous rating

I rated PacWest Bancorp a hold on May 25, 2023 and am more bullish now for the reasons explained in this article. Since my last coverage, shares of PACW have appreciated 38.32%, and I am now upgrading my recommendation to (speculative) buy.

Deposit flows

The key reason why I am bullish heading into PacWest Bancorp's earnings release is that recent reports from regional banks were quite good and investors seem to regaining their confidence in the banking sector. Although most banks that I covered reported quarter-over-quarter declines in their net interest margins due to the Fed raising interest rates, the regional banking sector as a whole saw stabilizing deposit outflows.

Interestingly, one of the regional banks that saw very large deposit outflows in Q1’23, Western Alliance Bancorporation, reported $3.5B in new deposits in the second-quarter, allowing the bank to recapture more than half of deposits lost in the previous quarter. In Q1’23, Western Alliance lost $6.1B of its deposits (a total of 11%) and I believe Western Alliance could fully restore its deposit by the end of the year.

Deposit flows at PacWest Bancorp will therefore be of intense interest when the bank reports earnings on Tuesday. Overall, the deposit situation at regional banks has stabilized , which is a reflection of the Fed taking decisive action and providing emergency liquidity to the U.S. depository institutions at the peak of the crisis in Q1. This emergency liquidity window, called the Bank Term Loan Program, has prevented the financial crisis spiraling out of control in the first-quarter.

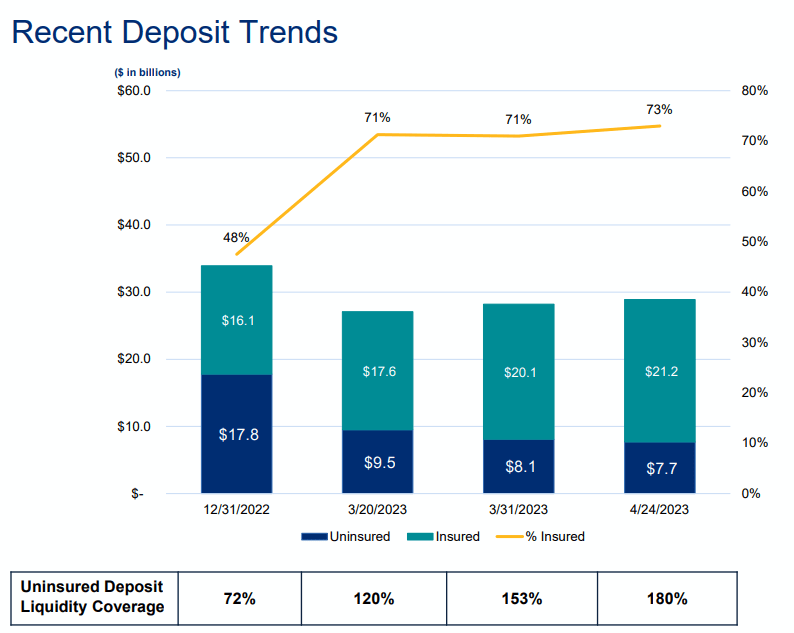

PacWest Bancorp lost $5.7B of its deposits (17% of its total) in the first-quarter, but the situation at the regional bank already stabilized as well and the bank saw $700M in deposit inflows after the end of the first-quarter. Assuming that depositors and savers have also regained their confidence in PacWest Bancorp during the second-quarter, the bank could have seen a massive inflow of new deposits as well, especially after the sale of a $2.6B construction loan portfolio resulted in recovering investor sentiment. Subsequently, PacWest Bancorp also sold a $3.5B asset-backed loan portfolio to investment company Ares Management to raise liquidity, strengthen its balance sheet and reduce lending risks.

{kind=link}

CRE portfolio

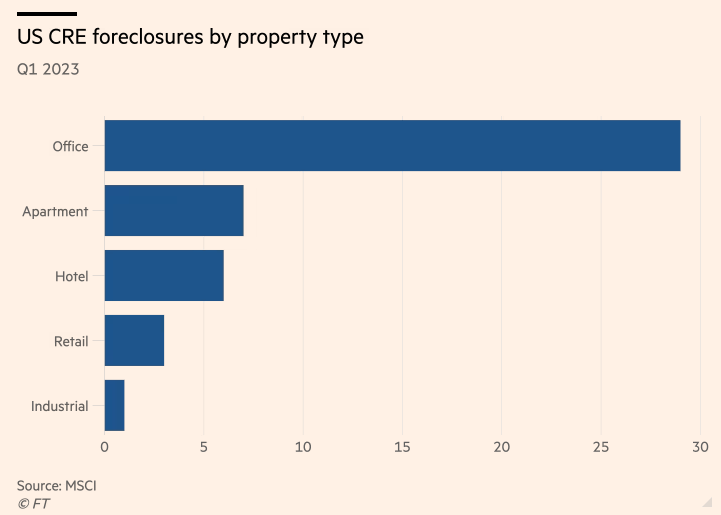

One reason why investors have been concerned with regional banks is that they have exposure to offices which are experiencing headwinds. Foreclosures in the office market are on the rise ( Source ), which raises concerns on the part of investors about the CRE exposure of smaller regional banks like PacWest that don’t have as large of a capital buffer as top tier banks.

{kind=link}

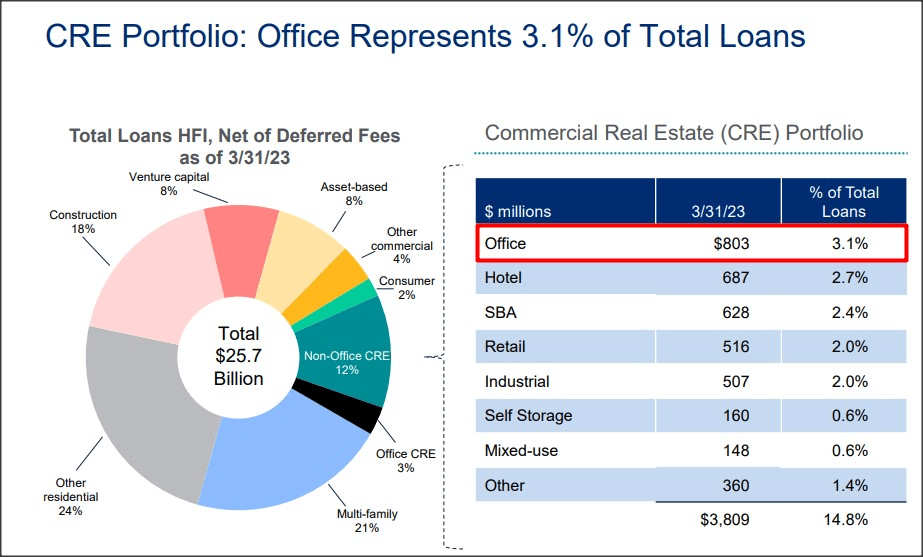

However, PacWest Bancorp has only very little exposure to the office market: at the end of the first-quarter, only 3.1% of the bank’s total loans were related to the office market. In other words, investors don’t have to be fearful of an outsized influence of defaults and rising foreclosures in the office market.

{kind=link}

Largest discount to book value in the sector

PacWest Bancorp continues to trade at the largest discount to book value in the regional banking market. Previously, First Republic Bank sold at the highest discount to book value, but the bank was ultimately seized by the Federal Deposit Insurance Corporation and then sold to JPMorgan Chase (JPM).

PacWest Bancorp is trading at about half of its book value (50% discount to book value), which gives PACW, in my opinion, the highest revaluation potential... if the company puts a strong Q2 earnings report on the table next Tuesday. Western Alliance, as an example, is now almost trading back at book value while selling at a near-40% discount to BV in April.

Risks with PacWest Bancorp

PacWest Bancorp is one of the riskier regional banks in the market, and the bank still needs to prove that it can attract more deposits. If the bank saw strong deposit outflows in the context of the First Republic Bank failure at the beginning of May, then PacWest may head for a disappointing earnings release. The bank naturally also faces headwinds for its net interest margin, as deposit costs will have risen sharply in Q2. PacWest Bancorp is a high risk, but also high potential bet and investors should manage their exposure very carefully (taking small position sizes and using stop loss limits).

Closing thoughts

Despite the risks with PacWest Bancorp, I believe the regional bank is a speculative buy ahead of the second-quarter earnings release next Tuesday, July 25, 2023. The reason is that the regional banking market as a whole has benefited not only from a stabilization, but from a recovery of deposit flows... which could especially benefit those banks that were hit the hardest in Q1. Since PacWest Bancorp also pulled off successful sales of its construction and specialty finance loan portfolios in Q2, I believe PacWest Bancorp has a lot of surprise potential next week!

For further details see:

PacWest: Speculative Buy Heading Into Q2 (Rating Upgrade)