SOFI - Pagaya Technologies: Facing A Promising 2024

2023-12-04 02:06:28 ET

Summary

- Israeli company Pagaya uses AI to provide loans to applicants rejected by traditional banks, increasing loan volume and profits.

- Pagaya securitizes loans into asset-backed securities, reducing credit risk for affiliated banks and providing investors with high-quality ABS.

- Recent partnerships with large banks and automobile finance companies will lead to substantial revenue growth in the coming quarters.

- By next year 2024, it is very likely that total revenue will be close to $1 billion, and it would not be strange to see the share price in a range of $3/$4.

The Israeli company Pagaya (PGY) has cleverly used artificial intelligence to provide loans to applicants who would have been rejected by traditional bank underwriting systems. Therefore, Pagaya's proprietary AI algorithm, which uses millions of data in less than a second, can assess an applicant's credit quality more effectively than traditional scoring systems. So Pagaya implements this AI algorithm in the systems of its affiliated banks in exchange for a fee. In this way, its partnerships benefit from credit operations that would be wasted if it were not for Pagaya, increasing the volume of loans granted and, therefore, their profits.

In addition, Pagaya connects investors who invest in credit assets on the same platform. Thus, Pagaya securitizes the loans it grants through its platform into asset-backed securities ((ABS)) to sell them to investors, eliminating most of the credit risk from the balance sheet of its affiliated banks.

In this way, Pagaya benefits from both sides of the credit process, all through the same platform.

It provides partnerships with additional credit volume without increasing risk on their balance sheets and provides investors with ABS of very good credit quality. In fact, the percentage of loan defaults captured by the Pagaya AI algorithm is significantly lower than the banking industry average. And finally, loan applicants who are excluded from traditional underwriting systems have a good chance of obtaining the financing they demand. It is a process where everyone wins (win-win-win).

This ingenious business model has worked very well in the short time life of Pagaya. In fact, in recent quarters and with a complicated economic-financial environment, with an aggressive monetary policy by the Fed of continuous increase in interest rates, the volume of loans obtained has not stopped increasing, income has increased slightly and the company has reduced its operations costs due to the improvement from economies of scale.

The company recently reported its third-quarter earnings. Results have exceeded expectations in many parameters:

…Exceeded third quarter guidance on all metrics:

- Record Network Volume of $2.1 billion

- Record Total Revenue and Other Income of $211.8 million

- Record Adjusted EBITDA of $28.3 million

- Announced new partner integrations, including a top 5 bank in the U.S. by total assets and a top 4 OEM auto captive by U.S. vehicle sales…”

These good results confirm the good progress of the business in a difficult environment (Fed, Israel war, etc.).

Despite these difficulties, Pagaya has managed to maintain and even slightly increase the level of its operating income in recent quarters, slightly reducing its operating costs until practically on the verge of a positive net result (-0.03 $ of EPS in the last quarter).

Pagaya is currently at an important turning point for several reasons:

- The latest partnerships with large banks and automobile finance companies will imply a substantial increase in revenue in the coming quarters. This significant increase in revenue will help Pagaya to record positive net profits starting next year 2024. They are also in talks with 80% of the top 25 US banks, so new partnerships will likely be reported.

- Inflation seems to be showing signs of exhaustion. The last CPI data for October falls to 3.2%, with the data for the previous month (September) being 3.8%. This could be the first signal for the Fed to stop the process of rising interest rates next year, which would result in an increase in demand for loans, from which Pagaya would directly benefit.

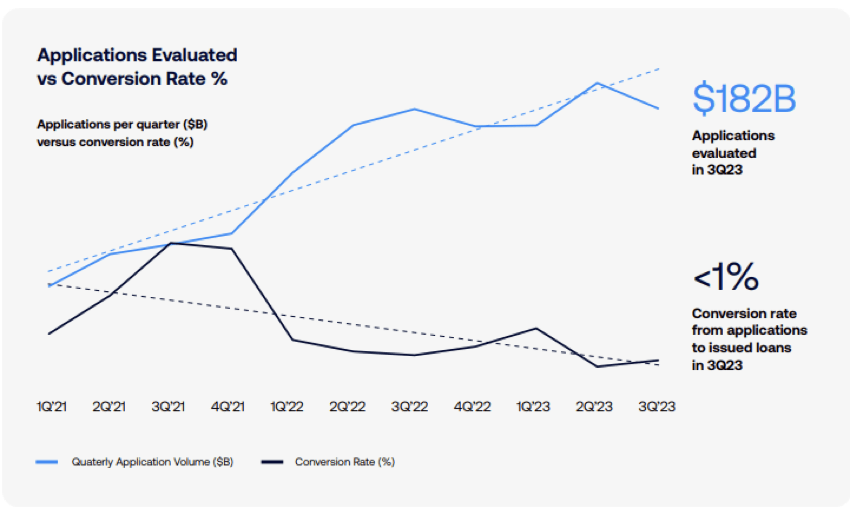

- The conversion rate is less than 1%. It is the smallest figure in the entire life of Pagaya. According to the company, this ratio is expected to increase due to the improvement of the IA algorithm. An increase in the % of conversion rate would imply a directly proportional increase in revenue. This route is the fastest and easiest to achieve an increase in income. It would not be unreasonable to see this ratio between 1.3% and 1.5% over the next year in a stable/lower interest rate environment.

For all these reasons, I believe that next year 2024 will be a great year for Pagaya, where we will see more important strategic alliances, a substantial increase in operating income and finally, a positive net profit.

During the last few months, the share price has suffered excessive punishment. This bad behavior has not only affected Pagaya, but the entire fintech sector. An aggressive monetary policy by the Fed, future economic uncertainties, etc. seem to be some of the factors. When these dark clouds clear, Pagaya will be in an advantageous position for the start of a strong recovery.

With a market capitalization of $850 million and revenue set to be close to $1billion next year 2024, the company is currently highly undervalued. I consider Pagaya as a very good medium and long-term investment opportunity with x3 or x4 revaluation potential, that’s why I rate Pagaya stock as Strong Buy .

Pagaya: A Profitable Company for next year 2024

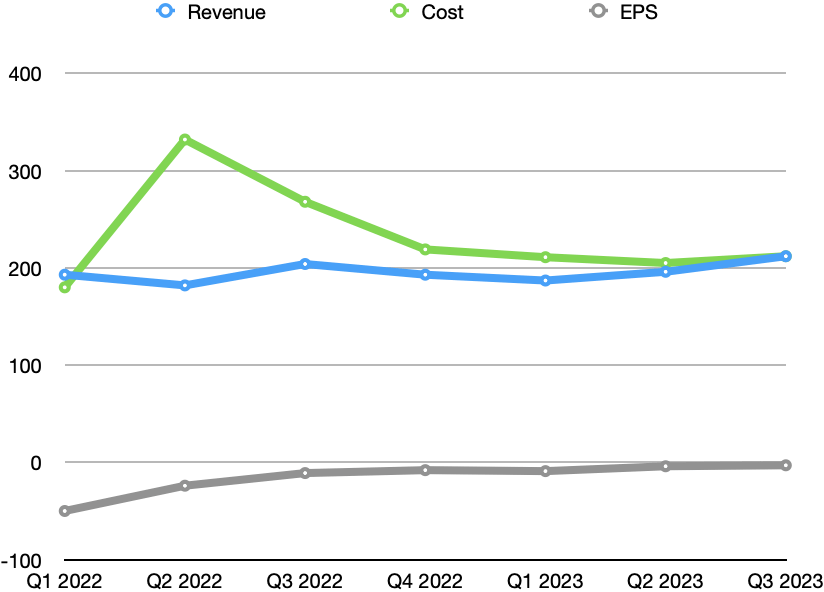

As we have previously commented, the company's net profit ((EPS)) has continued to improve in recent quarters as a result of a slight increase in operating income and cost containment. In fact, net EPS has increased over the last year from -0.11 in Q3 2022 to -0.03 in Q3 2023:

{kind=link}

As can be seen in the previous graph, the evolution of EPS in recent quarters is clearly positive, reaching -0.03 dollars in the last quarter (the best EPS in Pagaya´s life). This good evolution of EPS has been the result of a slight increase in operating income (in quarters with a difficult environment) and a reduction in operating costs. With this good evolution, and above all, thanks to the latest partnerships with two large credit institutions (a Top 5 Bank in the US and a Top 4 auto-financial) together with the increase in the conversion rate ratio, it is more than likely that the revenue will experience strong growth in the coming quarters. With this outlook, it is very likely that Pagaya will post a positive net EPS by next year 2024 (possibly by the first or second quarter).

Furthermore, according to the company, they are in talks with 80% of the top 20 US banks, of which at least 8 are at a very advanced level. All of this makes me think of a 2-digit net positive EPS in a few quarters.

{kind=link}

In the previous graph, you can see the negative evolution of the conversion ratio in recent quarters, currently standing at the lowest levels of the last two years due to the high-risk aversion from the partnerships credit institutions and interest rates environment. Now the company is implementing improvements to the AI ??algorithm to increase this ratio, taking advantage of the enormous amount of data it could be plausible to approve a higher percentage of loan applications without harming credit quality. Therefore, it is very likely that we will see a growth in the conversion ratio in the coming months. This will cause an automatic increase in income. The increase in the conversion rate will cause a proportional increase in income since:

Total revenue (Loan side) = (Total loans requests evaluated) X (conversation rate) X % fee.

Regarding the last two partnerships with two large credit entities, my opinion is that they are: US BANK and Chevrolet (GM financial company).

US Bank is ranked 5th in the ranking of Banks by assets, and among its strategic guidelines is partnering with Fintech to take advantage of new technologies such as artificial intelligence:

We embrace new technologies, partner with FinTech and seek feedback directly from our customers.

Chevrolet meets the characteristics that Pagaya specifies in the recent letter to shareholders:

This OEM had over 1.5 million in annual US vehicle sales in 2022, with over 10% market share in new vehicle sales among the largest in the US.”

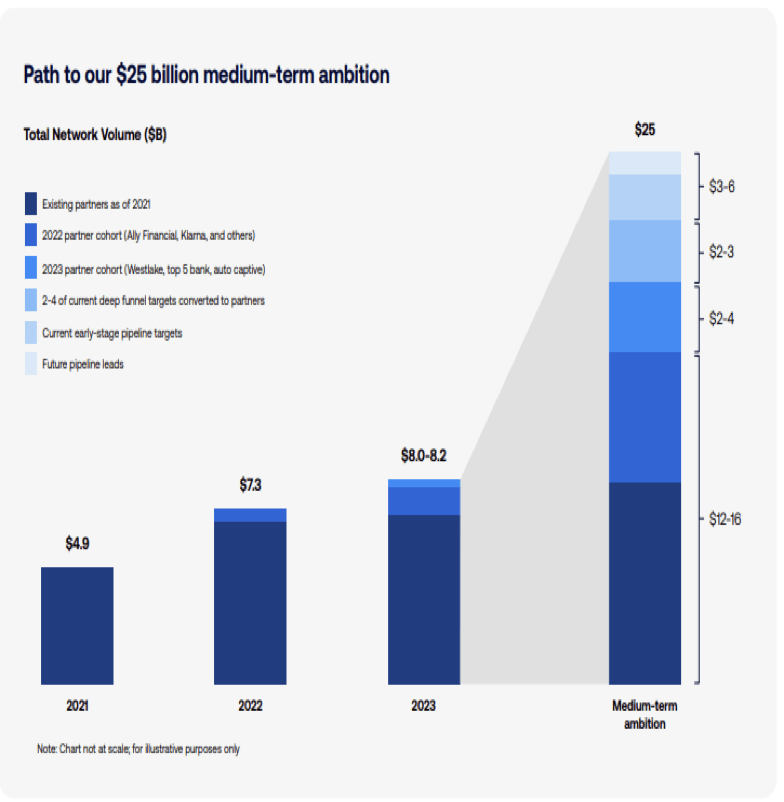

Total network volume target of $25 billion in the medium term. Some considerations about the Balance.

Pagaya's medium-term goal is to reach an operating volume of at least $25 billion annually (now it is approximately $8 billion). This objective can only be achieved by increasing the volume of operations captured by current partners and with new alliances with large banks and automobile finance companies. Thus, as the company explains in the letter to investors in the last third quarter:

Looking at all of our existing partners as of year-end 2022, they generated an estimated $65-$75 billion in annual originations. If we apply Pagaya’s average contribution to total volumes of its most mature partners of approximately 20%, the long-term network volume potential of these partnerships could range from $12-$16 billion.

{kind=link}

If we take into account that they have already signed two alliances with two large credit institutions and that they are in talks with 80% of the top 20 US banks, it seems reasonable to think that they could easily reach 25 billion dollars in Network volume in the mid-term.

Of these possible new alliances, Pagaya estimates that those that are in more advanced conversations could incorporate between $2B and $3B more in Network volume:

Our latest-stage opportunities in our deep funnel (those we expect can be onboarded within the next 12-24 months) represent an opportunity of approximately $2-$3 billion in incremental annual network volume once fully ramped.

In the previous article published in SA: “ Pagaya Q3: An early Christmas gift from Mr. Market", the author claims that to reach that $25 billion target, Pagaya would have to take on a balance sheet risk of at least $1.5 billion to meet the 5% liquidity requirement of Dodd-Frank regulation. The author states that assuming an operating cash flow of 2%-3%, Pagaya would need to carry out a capital increase of between 2% and 3% of that $25 billion ($500-$750 million) to be able to meet the regulatory requirements:

I believe Pagaya would need to find 2-3% of network volume in additional capital

This assumption is not exactly correct:

It should be noted here that this legal restriction applies only to securitized assets that Pagaya issues on the market (ABS-Assets Backed Securities) through the platform connected to investors.

In fact, the Frank-Todd regulation requires that 5% of the total securitized assets issued in the market be held on the issuer's balance sheet. Therefore, the target of $25 billion in raised loan volume in the medium term does not necessarily require Pagaya to take on 5% ($1.25 billion) on its balance sheet. Of that $25 billion, Pagaya will issue ABS for a slightly smaller amount. If we look at the latest quarterly and annual ABS issues, the amount is always lower than the total volume of loans granted.

Thus, during the first 9 months of this year 2023, it has issued a total of $4.9 billion in 11 ABS and has raised $5,91B ($2.1 billion+$1.96 billion+$1.85 billion=$5.91billion).

This means that Pagaya has had to retain 5% of $5.91B = $295M on its balance sheet during these first 3 quarters.

The balance sheet as of 9/30/23 showed $665 million in investments in loans and securities. At the end of last year 2022 that figure was 463 million dollars. Therefore, there has been a net increase in credit assets on the balance sheet of $202 million. Why not equal the difference of 295 million dollars? Most likely it is due to the amortization of the loans during those 9 months. Personal loans usually have an average life of between 3 and 5 years. This implies an annual amortization % of between 20% and 33%.

The question here is whether in a few years Pagaya, to reach the target of $25 billion in Network volume and taking into account current cash status ($284M), will need to carry out a capital increase to obtain funds that will allow it to retain assets on its balance sheet to comply with regulatory requirements.

Observing the behavior of the cash status of these first 9 months of the year: the cash at the end of the last year 2022 was $337M. At the end of the last quarter (Q3), it was $284M, so in these 9 months of the year, the cash has been reduced by $53M. As we have seen previously, with the ABS issuances ($5.91B) this year 2023, they have needed to invest in credit assets for an amount of $295M. That is, to maintain assets on the balance sheet worth $5.91 billion in these 9 months, cash has only been reduced by $53 million.

This is explained because Pagaya obtains cash flows from the fees of its credit operations, as well as from the sales of other assets.

Doing a simple extrapolation and considering all other parameters constant, to reach a volume of $25 billion, assuming an annual issuance of about $20 billion in ABS, cash would be reduced by about $200 million in the coming years. Cash as of 09/30/23 was $284 million, so the medium/long-term cash situation, in principle, would be very tight but not extreme.

In any case, the company stated in the previous Q2 CC that in the future they will diversify financing products ((ABS)) to look for those that do not require risk retention requirements on the balance sheet:

So that gives us actually a long runway to be able to continue to grow the business. Obviously, long term will diversify and actually supplement the ABS distribution mechanism with other funding products that don't have the same balance sheet requirements...

Therefore, my opinion is that, although the current funds raised from investors through ABS require a 5% withholding on the Balance Sheet and that the medium-term objective is to achieve a network volume of 25 billion dollars annually, I believe that this necessarily NOT implies that Pagaya will have to undertake large capital increases to obtain the necessary funds. An increase of $100 or $200 million would be plausible in the medium term, but I wouldn't be surprised if they didn't even have to resort to it.”

A Network volume of 25 billion dollars would mean multiplying the current annual volume by approximately three. This would increase annual revenue to almost $3 billion, keeping the current conversion rate below 1%, which is highly unlikely as this ratio will surely increase. Therefore, we could be talking about estimated medium-term revenues that easily exceed $3 billion.

Intrinsic value of Pagaya (Price to Revenue multiple)

We are going to carry out a valuation of the company using the P/S ratio. To do this, we will estimate the income for the next 5 years.

The expected annual revenue for this year 2023 is estimated between $800M and $825M. This represents an income growth for this year 2023 of 10% compared to the previous year 2022.

We estimate the average % annual growth for the coming years at a prudent 10%. I consider this data prudent because thanks to the latest strategic partnerships with large credit institutions, strong income growth is expected for the coming quarters.

We will take a discount rate of 5%. This is a reasonable long-term discount rate considering current market conditions.

Shares outstanding = 900 million (diluted shares outstanding as of 09/30/23 are = 796 million. I believe this figure will increase in the coming years due to management incentive plans, that’s why I take 900 million).

I am going to use a price/sales ratio of 2. This data is very conservative since the current ratio for other companies in the same sector is higher: P/S SoFi=3.53, P/S Upstart=4.02.

| Year |

| 2024 |

| 2025 |

| 2026 |

| 2027 |

| 2028 |

| Revenue (x$1000) |

| 907 |

| 998 |

| 1098 |

| 1207 |

| 1328 |

| Discounted revenue (x$1000) |

| 863 |

| 905 |

| 948 |

| 993 |

| 1040 |

| Full discounted revenue |

| 4,7B |

| P/S=2 |

| 9,5B |

| Intrinsic value per share |

| 10,55$ |

Source : Author

Therefore, according to my valuation model, the current intrinsic value of Pagaya is $10.55 , assuming the parameters described above. This implies a potential % revaluation in the mid/long term of 642% (share price today: $1.43).

If the variables studied above behave in the coming months/years as we have described here, the share price should trend towards the intrinsic value calculated here.

You can clearly see how incredibly undervalued the share price is currently, but we have to keep in mind that the share price was around $30 one and a half years ago.

Peers Comparison in Fintech Sector

| Company |

| Pagaya |

| Upstart |

| SoFi |

| Opera |

| P/S ratio |

| 1,2 |

| 4.02 |

| 3.53 |

| 2.80 |

Source : Author

Comparing the valuation according to the P/S ratio of Pagaya with other companies in the Fintech sector: SoFi (SOFI) and Upstart (UPST) we can clearly see that Pagaya is the cheapest. Since they are all “growing companies”, the most used valuation ratio is the P/S since the “revenue” variable here is the most important factor.

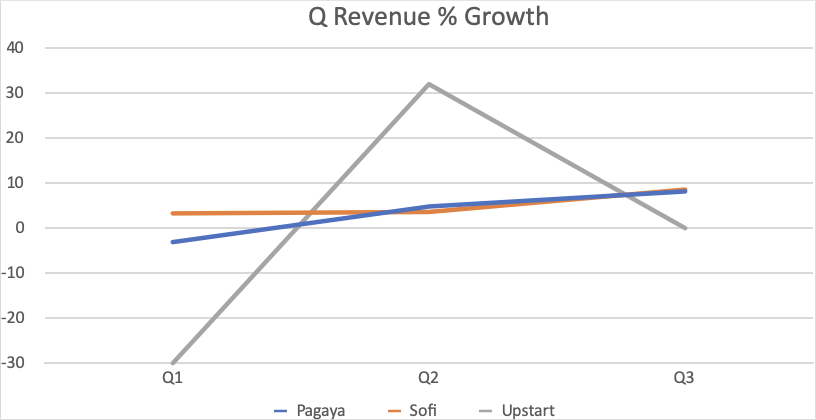

Revenue Growth in the previous quarters (Peers comparison)

| Q1 2023 |

| Q2 2023 |

| Q3 2023 |

| Pagaya |

| 187 (-3.10%) |

| 196 (4.81%) |

| 212 (8.16%) |

| SoFi |

| 472 (3.28%) |

| 489 (3.60%) |

| 531 (8.58%) |

| Upstart |

| 103 (-30%) |

| 136 (32%) |

| 135 (0%) |

Source : Author

{kind=link}

As can be seen in the graph above, the evolution of quarterly revenue growth shows a clear increasing trend for Pagaya and SoFi. However, for Upstart the evolution is more erratic.

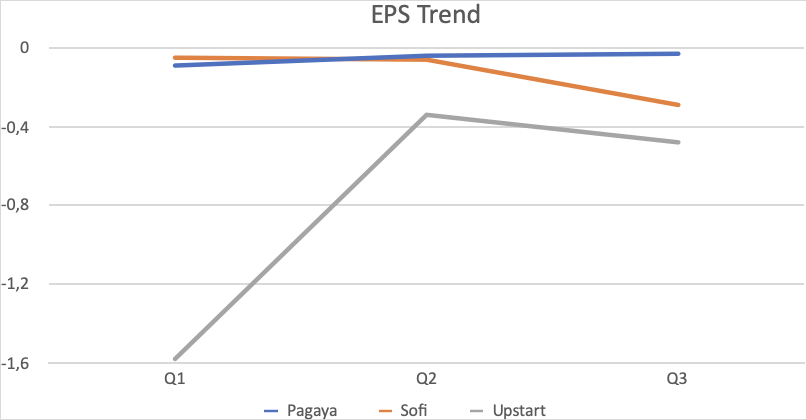

EPS Growth in the previous quarters (Peers Comparison)

{kind=link}

Regarding the evolution of net EPS, Pagaya is the one that has clearly presented the best performance in the last 3 quarters. In fact, it is very close to presenting positive net profits.

Institutional Holders transactions

Pagaya emerged a few years ago as a SPAC. SPAC is a good vehicle to channel financing to growth companies in their early stages.

The problem here arises from the fact that many of these initial investors unwind their positions in the short/medium term, exerting strong selling pressure in the market and, consequently, damaging the share price.

In various stock forums, the latest transactions carried out by insiders and their possible influence on the share price have been discussed. If we look at the last institutional holder´s transactions, we see that there have indeed been several movements within the group of the company's most important institutional holders. Thus, for example, Clal Seguros (second institutional holder in the ranking) in the last quarter has reduced its participation by 34.23% with the sale of 14.6 million shares. They still have a little more than 28M left. In this case, being an Israeli insurance company, it is very likely that with the current Israel war, it will need liquidity to cover the compensation of its clients. We see that of its 145 current positions in 72 it has reduced its participation and in 26 it has completely liquidated them. Therefore, in this case, the sale of Pagaya shares is fully justified. The question here is whether they will continue to liquidate more Pagaya positions since they still have 28 million shares. On the other hand, we have Tiger Global Management LLC, 5th in the ranking of institutional holders at the end of the previous quarter. Tiguer disposed of almost all of his positions in Pagaya last quarter (selling just over 29 million shares), reducing his stake to just 3.5 million shares. Most likely, Tiguer should have already completely sold their position. In the case of Tiger we do not observe that there has been intense sales activity of its other positions in its portfolio, so we really do not know the reason for the liquidation of Pagaya´s position.

As an anecdotal fact, the famous fund managed by Cathie Wood Ark Invest entered for the first time in the previous quarter with just over 938 thousand shares (15th in the ranking).

The positive here is that, except for Clial Insurance, it no longer seems that there are any more institutional holders who are going to sell their shares in the short term.

Top Institutional Holders as of 09/30/23:

| Holder |

| Shares |

| Date Reported |

| % Out |

| Value |

| Viola Ventures V.c. Management 4 Ltd. |

| 98,109,329 |

| Sep 29, 2023 |

| 18.37% |

| 136,371,965 |

| Clal Insurance Enterprises Holdings Ltd |

| 28,094,134 |

| Sep 29, 2023 |

| 5.26% |

| 39,050,845 |

| Ejf Capital Llc |

| 13,681,142 |

| Sep 29, 2023 |

| 2.56% |

| 19,016,787 |

| Millennium Management Llc |

| 5,976,812 |

| Sep 29, 2023 |

| 1.12% |

| 8,307,768 |

| Tiger Global Management, LLC |

| 3,565,657 |

| Sep 29, 2023 |

| 0.67% |

| 4,956,263 |

| JTC Employer Solutions Trusteee Ltd |

| 2,761,840 |

| Sep 29, 2023 |

| 0.52% |

| 3,838,957 |

| VK Services, LLC |

| 2,365,121 |

| Sep 29, 2023 |

| 0.44% |

| 3,287,518 |

| Morgan Stanley |

| 1,924,193 |

| Sep 29, 2023 |

| 0.36% |

| 2,674,628 |

| Alyeska Investment Group, L.p. |

| 1,620,232 |

| Sep 29, 2023 |

| 0.30% |

| 2,252,122 |

| AFLAC Inc. |

| 1,563,895 |

| Sep 29, 2023 |

| 0.29% |

| 2,173,814 |

Source : Seeking Alpha

Last Insiders transacctions

In recent days there have been 3 insider movements:

1) On 11/27/23, the sale of 1,500,000 shares by Yahav Haim Yulzari (co-founder and chief revenue officer).

2) On 11/24/23 sale of 1,500,000 shares by Avital Pardo (Co-Fouder and Chief Technology Officer).

3) On 11/13/23 sale of 195,734 shares by Tami Rosen (director of personnel)

In total, more than 3 million shares have been sold on the open market in recent days.

At first, this coincidence in the sale of shares by 3 insiders in a few days may seem somewhat suspicious. However, we observe that they have been the only insider sales in the entire current year 2023, and furthermore, a tiny percentage of the total positions they currently hold.

Thus, for example, Avital in its last 13D/A SEC filing last September claimed to have just over 154M shares, so the sale has been just under 1% of its total holdings.

I have not been able to obtain information about the current portfolio from the other two insiders, but since one of them is also a co-founder, it is assumed that the sale was a small percentage of their current portfolio.

Therefore, I do not consider these sales to be red flags.

$500M mixed securities shelf

Pagaya filed for a $500 million mixed securities shelf on October 4. The company has not specified the purpose of this presentation. One possibility was to obtain funds to buy GreenSky to Goldman Sachs, given that Pagaya had made an offer for said company last August of between 600 and 800 million dollars, an offer that was finally rejected (Goldman Sachs ultimately chose Sixth Streets' bid for $500 million, a decision that surprised many because it rejected Pagaya's largest amount ($700 million. I don't think this decision hides any negative aspects as some may think).In my opinion, this shelf offering was simply a strategic decision, possibly to raise cash for the Sixth Street bid or even to keep cash flow under control for the next 3 years. If they need to obtain funds in the coming years, they are guaranteed the issuance of up to $500 million. As I said previously, I don't think the company will carry out a capital increase in the short term. And I wouldn't be surprised if they never had to make any offers in the end.

Risks

The main risks I see here are summarized in:

1- Inflation picks up in the last quarter of the year, which would force the Fed to have to raise interest rates again in the first quarter of next year.

2- A possible economic recession for next year 2024 that causes a reduction in demand for loans.

3- The new alliances do not generate the estimated volume of operations.

4- Pagaya finally uses the $500M shelf offering.

Conclusion

Pagaya is currently at an inflection point and faces a promising 2024 year due to several factors:

1-Inflation shows the first signs of exhaustion. The latest CPI data have shown a figure of 3.2% compared to 3.7% the previous month (October). This may be the end of the restrictive monetary policy that the Fed has been applying for the last two years. Rates could stop rising, and could even begin a slow decline in the middle of next year 2024. All of this will favor Pagaya's activity as it will help increase demand for loans.

2- The increase in revenue in recent quarters and cost containment have contributed to generating increasingly better net EPS. The last reported EPS (3rd quarter) was -0.03, the best in Pagaya's history. It looks like the good performance is going to continue, so it is very likely that a positive net EPS will be achieved in the first or second quarter of 2024, which would make Pagaya generate positive net profits for the first time.

3- It has recently signed, strategic alliances with large credit institutions (Top 5 banks and top 4 auto financial), which will open the doors to more alliances with large banks in the future. This will result in a huge increase in Network volume and revenue.

4- The conversion ratio, currently at minimum levels, will begin to rise in the coming months as a result of the improvement implemented in the AI ??algorithm. This will directly translate into higher income.

For all these reasons, I believe that we are facing a very important moment in the life of Pagaya, the wind is blowing in favor on many fronts, and I expect that all this will be reflected in a significant revaluation of the share prices in the coming months. By next year 2024, it is very likely that total revenue will be close to $1 billion, and it would not be strange to see the share price in a range of $3/$4.

Editor's Note: This article was submitted as part of Seeking Alpha's Top 2024 Long/Short competition, which runs through December 31 . With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Pagaya Technologies: Facing A Promising 2024