PAI - PAI: Yield Is Too Low Just Buy Treasuries

2023-10-02 16:48:00 ET

Summary

- The Western Asset Inv Grade Income Fund Inc has a current yield of 4.96%, lower than most money market funds.

- The PAI closed-end fund has outperformed bond indices over the past year, but its low yield and limited potential for capital gains make it unattractive.

- The fund's use of leverage is relatively low, but it also limits its ability to provide a higher yield.

- An investor could earn higher income with lower risk by buying U.S. Treasuries.

- The fund itself would be fantastic if its distribution yield was 100 basis points higher, but its expenses prevent that.

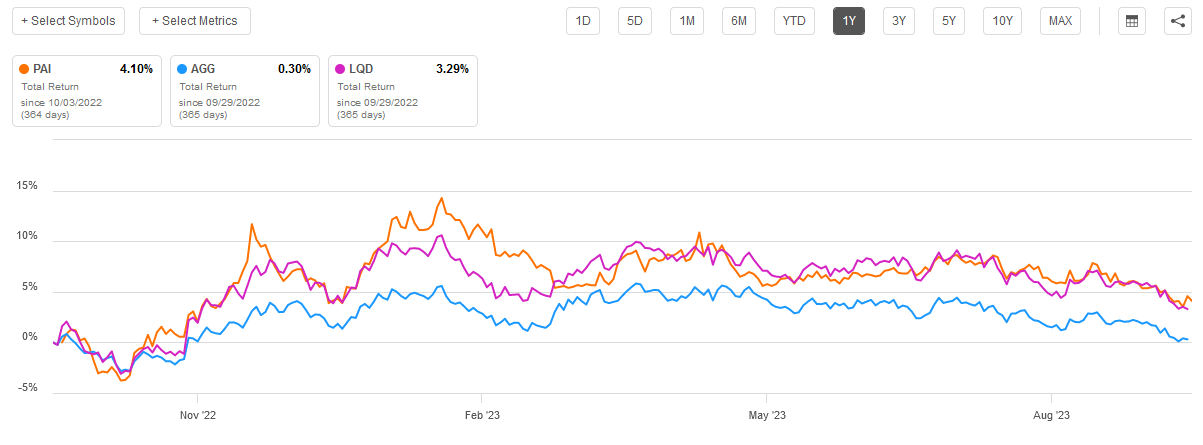

The Western Asset Inv Grade Income Fund Inc ( PAI ) is a closed-end fund aka CEF that investors can employ for the purpose of generating a high level of income from their portfolios. Unfortunately, this fund does not do nearly as well as most other income-focused closed-end funds as its 4.96% current yield is actually lower than most money market funds right now. While the fund did increase its distribution going forward, with a tenth-of-a-cent increase starting in November, it still seems unlikely that it will attract much attention from yield-seekers right now. This is unfortunate, as this fund has managed to do better than both the Bloomberg U.S. Aggregate Bond Index ( AGG ) and the Markit iBoxx USD Liquid Investment Grade Index ( LQD ) over the past year:

{kind=link}

With that said though, it is still very difficult to make a case for any bond fund yielding under 5% considering where interest rates are. After all, right now an investor could simply buy a five-year or a ten-year Treasury and obtain a very similar yield and a guaranteed return of principal in a few years. That is better than any bond fund can deliver, especially considering that interest rates are unlikely to come down dramatically in the near future. This means that potential capital gains are likely to be limited, although the truth is that Federal Reserve policy can be unpredictable, and right now the Federal Reserve is basically between a rock and a hard place.

About The Fund

According to the fund's webpage , the Western Asset Investment Grade Income Fund has the stated objective of providing a very high level of current income for its investors. This is a very common objective for a bond fund, and the name suggests that this one is a bond fund. This is reinforced by the fact that the fund's portfolio consists of 96.12% bonds along with a small amount of cash, preferred stock, and convertible securities:

CEF Connect

This is in line with the fund's description on its webpage, which states:

[The Fund] provides a portfolio of primarily investment-grade debt, including government securities, bank debt, commercial paper, and cash/cash equivalents.

As I have mentioned in various previous articles, bonds deliver the overwhelming majority of their investment returns in the form of direct payments made to the investors. There are no net capital gains since bonds are both issued and redeemed at face value. Thus, a focus on current income generally makes sense for a bond fund.

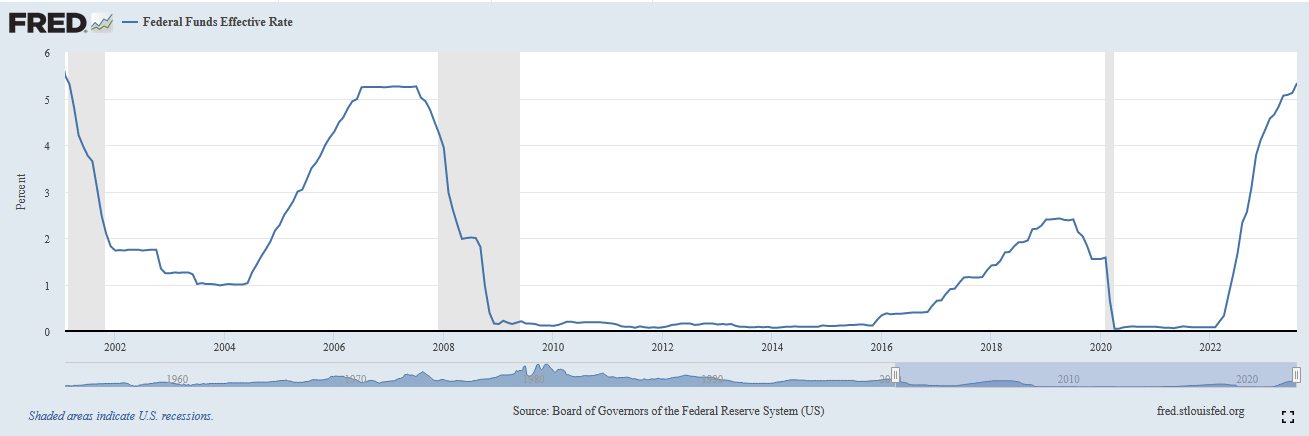

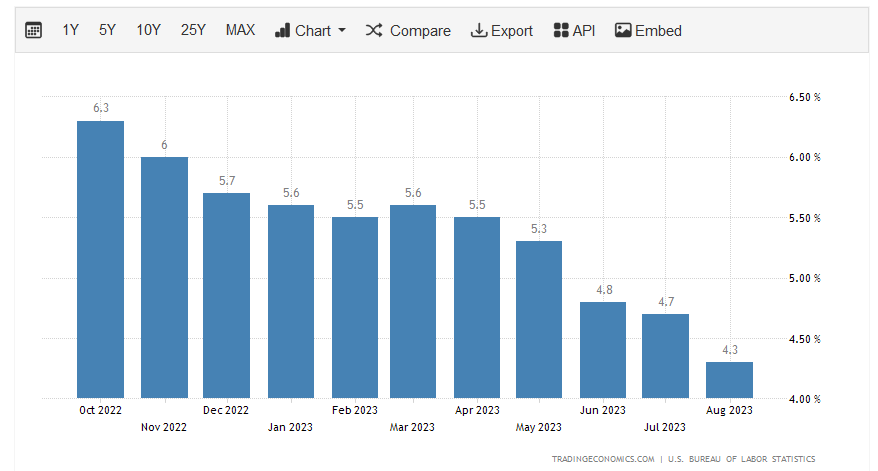

With that said bond prices do fluctuate inversely with interest rates. This is because newly issued bonds will have a coupon rate that corresponds with the market rate at the time of issuance. Thus, when rates go up, older bonds will have a yield that is lower than the current market rate. As bonds have no net capital gains, it makes no sense to pay face value for an older bond that has identical characteristics but a lower coupon rate than a brand-new bond. Thus, the price of the existing bond has to decline in order to induce anyone to purchase it. This has proven to be a problem for bonds since the start of 2022 as the Federal Reserve has been aggressively raising interest rates in order to combat the incredibly high inflation rate that has been plaguing the economy. As of the time of writing, the effective federal funds rate is 5.33%, which is the highest level that has been seen in more than twenty years. In fact, the last time the effective federal funds rate was this high was in February 2001:

{kind=link}

The thing that should immediately leap out at anyone reading this chart is how quickly the effective federal funds rate went from basically zero to its current level. In fact, in February 2022, the effective federal funds rate was 0.08%. Thus, the benchmark interest rate for the domestic economy increased by 525 basis points in about eighteen months. This is one of the fastest rate increases in history, perhaps only comparable to the rapid increases and decreases that occurred during the late 1970s and early 1980s when the economy was suffering from a comparable bout of inflation.

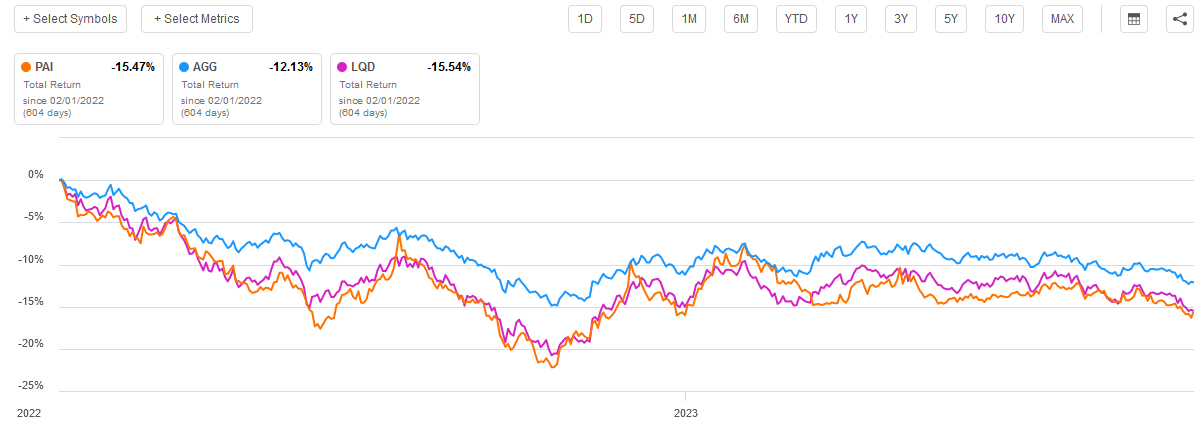

This is one of the biggest reasons why bond investors have experienced massive losses since the start of 2022. We can see that reflected in this fund. This chart shows the performance of the Western Asset Investment Grade Income Fund against the two broad-market bond indices mentioned in the introduction since February 1, 2022:

{kind=link}

Please note that this chart takes the distributions paid by the assets into account. Overall, investors in the Western Asset Investment Grade Income Fund have seen their wealth decline by a whopping 15.47% over the period. The aggregate bond index did better, but not by very much. The Western Asset Fund did actually outperform investment-grade corporates, which is nice to see.

One thing that is very important to note is that bond investors who hold their bonds for the entire life of the bond do not lose money. This is because bonds are issued at face value, and they pay their face value back when they mature. Thus, an investor in a bond will not lose money in a bond unless the issuer defaults. This is very important right now because U.S. Treasuries are actually offering comparable yields to the fund:

| Security |

| Current Yield |

| 2Yr. U.S. Treasury |

| 5.117% |

| 5Yr. U.S. Treasury |

| 4.721% |

| 10Yr. U.S. Treasury |

| 4.697% |

The yield of the Western Asset Investment Grade Income Fund is 4.96% at the current price. Thus, realistically, unless you are expecting the fund's share price to go up significantly within the next two years or so, there is absolutely no reason to buy this fund. It would make far more sense to just buy a two-year U.S. Treasury (US2Y), collect a higher yield, and get your money back in 2025. While there is always a higher risk of losing money to defaults when buying an individual bond than buying a fund, if the U.S. Treasury actually defaults then pretty much any bond fund is going to be utterly annihilated. In addition, any event that causes the fund's share price to go up (namely a decline in interest rates) would also benefit Treasuries. Thus, it appears as if it would make more sense to just buy and hold U.S. Treasury securities as the yield of this fund is not sufficient to justify the added risk.

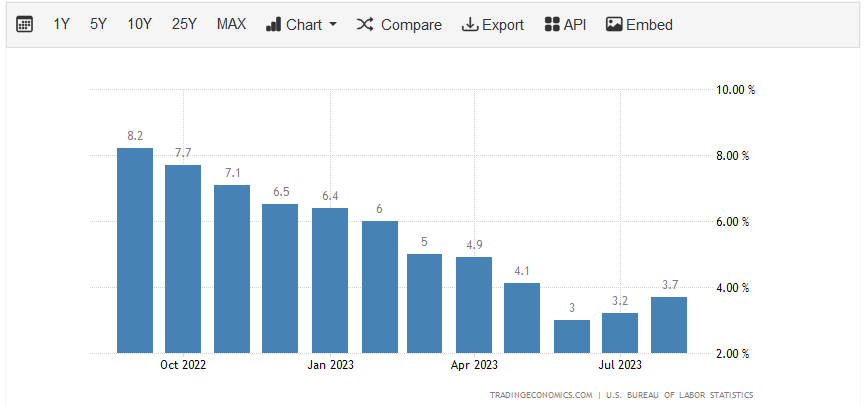

There is, however, little reason to expect interest rates will fall significantly in the near term. Thus, the fund's probability of delivering capital gains or share price appreciation is also going to be very low. As mentioned earlier, the primary reason why the Federal Reserve raised interest rates in the first place was to combat the incredibly high inflation rate that has been permeating the economy. For a while, this appeared to be working as the headline inflation rate was dropping over much of the first half of this year. However, for the past few months, it has actually been trending up once again:

{kind=link}

The biggest reason for this is that inflation was not really coming down much at all. As I pointed out in a blog post earlier this year, the majority of the improvement that we saw in the inflation rate through the middle of this year was due to the Federal Government dumping crude oil from the Strategic Petroleum Reserve onto the market. This was pushing down crude oil prices, which are a major component of the headline inflation number. We can see this by looking at the core consumer price index, which excludes food and energy prices, as those can be somewhat volatile:

{kind=link}

We can see that there was not much improvement here, although the core consumer price index growth rate did decline quite a bit over the same. However, at 4.3% year-over-year, it is still substantially above the Federal Reserve's 2% target level. Jerome Powell has implied that the Federal Reserve will not pivot or reduce rates until inflation is consistently down below the 2% target rate. When we consider that it has yet to reach that level and that rising energy prices are applying upward pressure on the prices of everything that we produce or consume, the only logical conclusion is that the economy is still a long way off from rate cuts being a realistic possibility.

In fact, now that crude oil prices have started to rise, and appear likely to continue to do so because of the crude oil shortage, it is possible that the core inflation rate will start to tick upward. After all, energy is a cost of every business, so rising prices of energy will cause the price of everything else to rise. That could induce the central bank to raise interest rates further, which would have a devastating effect on bond prices. As bond prices affect the net asset value of the Western Asset Investment Grade Income Fund, there is little reason to believe that its net asset value will increase in the near future. This essentially precludes the possibility of much price appreciation in the fund's shares.

At least, it precludes the possibility of much near-term price appreciation unless the high rates cause the entire economy to collapse. There is, after all, substantially more debt in the economy than there was the last time that interest rates were at the current level. There is even a lot more debt in the economy than there was in 2007 when the nation experienced a financial catastrophe. While we do not have nearly the risk of people defaulting following a reset on an adjustable-rate mortgage, businesses and governments that borrowed money over the past ten years will need to roll over their bonds eventually. That could cause bankruptcy rates to start going up as many companies will not be able to afford to carry their debt at today's rates. It is, unfortunately, very difficult to predict what this would do to a bond fund as the Federal Reserve would probably slash interest rates but there would still be losses from the defaults.

In short, it is incredibly hard to justify buying any bond fund with a yield below 5% like this one when someone could just buy a U.S. Treasury ladder instead. The risks here are too great, especially given that the yield is less than that of a two-year U.S. Treasury bill.

Leverage

One of the strategies that closed-end funds usually use to boost the effective yield of their portfolios is the use of leverage. I explained how this works in numerous previous articles, such as this one :

Basically, the fund borrows money and then uses that borrowed money to purchase bonds and similar income-producing assets. As long as the purchased assets have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. This fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates. As such, this will normally be the case. With that said, this strategy is much less effective today than it was two years ago when borrowing rates were at 0%. This is because the difference between the yield on the purchased assets and the interest rate that the fund has to pay on the borrowed money is much less than it once was.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much debt since that would expose us to an excessive amount of risk. I generally do not like a fund's leverage to exceed a third as a percentage of its assets for this reason.

As of the time of writing, the Western Asset Investment Grade Income Fund has levered assets comprising 8.93% of its portfolio. This is certainly well below the specified one-third maximum level that we would like to see, as well as being considerably below the leverage possessed by most other bond funds. This is somewhat nice right now since the low leverage will result in lower losses than we would otherwise experience should bonds continue to decline. However, it also explains why the yield is less than that of a money market fund. In some ways, the fund is stuck in a tight spot as it needs to increase its leverage in order to provide an attractive yield, but doing so would increase losses in a rising rate environment.

Distribution Analysis

As mentioned earlier in this article, bonds deliver the overwhelming majority of their returns through direct payments made to their investors. After all, bonds have no net capital gains over their lifetimes, so the coupon payment is all they have. As such, most bonds will deliver a yield that is higher than the dividend yields of common stocks. The fund's basic business model is to collect the coupon payments from the bonds in its portfolio and pay them out to its investors, net of expenses. The fund also has the potential to earn some profits by exploiting changes in bond prices and trading them prior to maturity.

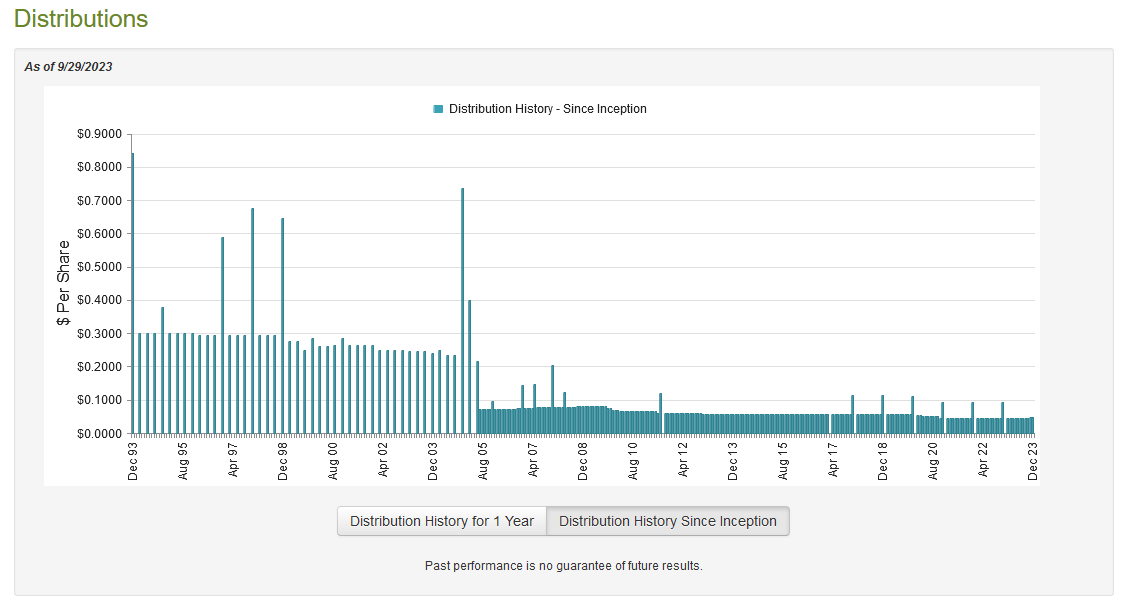

The unfortunate reality though is that this fund does not have much to offer in the way of yield due to its lack of leverage. It currently pays a monthly distribution of $0.0465 per share ($0.558 per share annually), which is a 4.96% yield at the current price. The fund did increase this to $0.0475 per share ($0.57 per share annually) starting in November, but even that is only a 5.07% yield at the current price. This is roughly in line with a money market fund and quite a bit below the yield of a two-year U.S. Treasury. To its credit though, the Western Asset Investment Grade Income Fund has been more consistent with respect to its distribution than most fixed-income closed-end funds, as it has only changed its payout a few times over its history:

{kind=link}

This solid distribution history might appeal to someone who is seeking to generate a consistent amount of income from their portfolios. The fund's long-term history is certainly conducive to that goal, even though its current yield is very low. However, we can see that it is hardly perfect as the fund's distribution was higher prior to the COVID-19 pandemic than it is today, even though it should be receiving a much higher yield on any bond that it purchases today.

With that said, let us have a look at the fund's finances and see how well it can sustain its distribution. After all, that is the most important thing for any income-focused investor who is purchasing the fund today.

Fortunately, we do have a relatively recent report that we can consult for the purpose of our analysis. As of the time of writing, the fund's most recent financial report corresponds to the six-month period that ended on June 30, 2023. This period of time represented a period of great optimism for the bond market as the market was generally anticipating that the Federal Reserve would pivot by the end of 2023 and was pricing bonds accordingly. While it certainly appears that the market was wrong, the fund still had the opportunity to potentially earn some profits by selling bonds into the optimistic market that was actually bidding up bond prices.

During the six-month period, the Western Asset Investment Grade Income Fund received $3,319,696 in interest and $23,618 in dividends from the assets in its portfolio. Once we net out foreign withholding taxes, we get a total investment income of $3,339,229 for the fund during the period. It paid its expenses out of this amount, which left it with $2,789,981 available for shareholders. That actually was sufficient to cover the $2,653,558 that the fund paid out in distributions over the period.

Thus, it appears that this fund is simply paying its distribution out of the net investment income. This is the same thing that it did over the full-year 2022 period, which actually makes this one of the only fixed-income funds that can claim that it fully covered its distributions last year. This is pretty nice for someone who is looking for safety as we know that the fund is not overdistributing.

Valuation

As of September 29, 2023 (the most recent date for which data is available as of the time of writing), the Western Asset Investment Grade Income Fund has a net asset value of $12.15 but the shares only trade for $11.11 per share. This gives the fund's shares an 8.56% discount on net asset value at the current price. This is quite a bit better than the 7.26% discount that the shares have had on average over the past month, so the price certainly seems reasonable today.

Conclusion

In conclusion, the Western Asset Investment Grade Income Fund is probably one of the safest fixed-income closed-end funds on the market. It has very limited leverage right now, which helps keep volatility risk down, and the fund is entirely invested in investment-grade securities. The fact that it can fully cover its distribution out of net investment income is a bonus. The big problem with this fund is that the yield is not competitive with other options that have lower risk. A U.S. Treasury ladder would offer a similar level of income and even lower risk because you are invested in U.S. Treasuries as opposed to corporate bonds. If the yield on this fund was 100 basis points higher, it would be quite attractive but as it stands now, there is no reason to invest in it.

For further details see:

PAI: Yield Is Too Low, Just Buy Treasuries