VRE - Pain In The Housing Market Is Setting The Stage For Significant Value Creation

2023-05-16 09:50:15 ET

Summary

- The homebuilding market is crashing even as we are dealing with a massive housing shortage.

- This should create a nice catalyst for homebuilding companies down the road, but perhaps the more interesting catalyst involves REITs that lease properties out.

- Fewer homes built should translate to even greater pricing power for these REITs, with the greatest upside involving multi-family operators.

If you are a value investor like I am, odds are that you believe that, at least in the short run, the market can be very inefficient. Ultimately, the market will find fair value or something approximating it for every security. But that can take days, weeks, months, or sometimes years. In the meantime, investors have the opportunity to buy into these stocks and capture the upside that they deserve once the market comes to realize what they are ultimately worth.

One area that I believe is not being priced appropriately, solely because of short-term thinking, is the rental market for both single family and multifamily properties. Short term issues have caused investors to ignore some rather attractive catalysts that should start paying off in the next year or so. And when that does come to pass, I believe that the upside for some of these companies can be quite appealing.

Pain in the market

The past several years have been very interesting for the housing market. Leading up to the last financial crisis back in 2008 and 2009, the number of homes being built skyrocketed. To put this in perspective, in 1991, there were just under 1.1 million housing completions. That number increased almost every year after, eventually peaking at 1.98 million in 2006. Rampant speculation in the housing market, poor underwriting standards, fraud, bad government policy, low interest rates, and other factors all caused this. If you're reading this now, you were almost certainly around back then. The pain that followed was significant.

{kind=link}

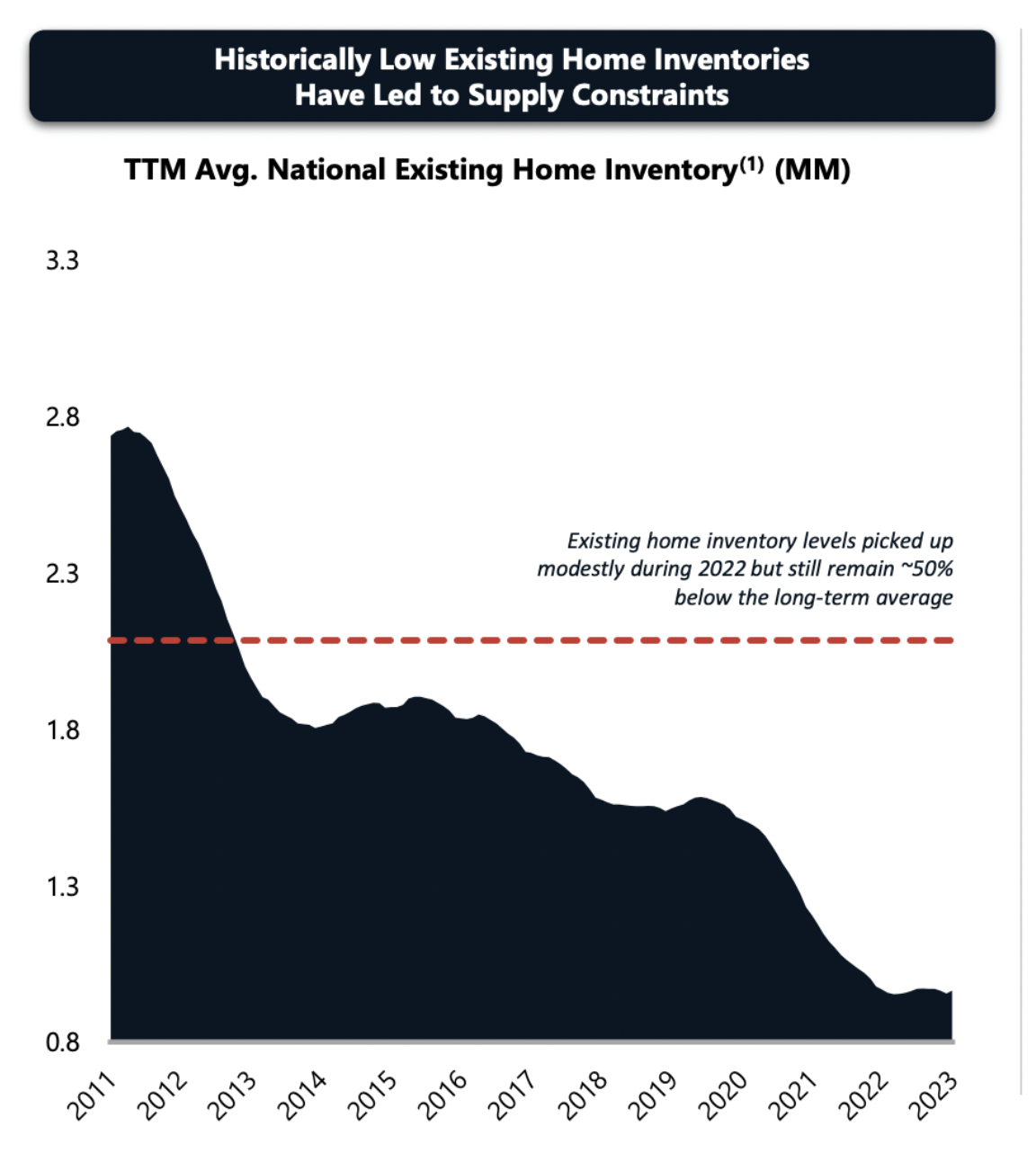

After peaking in 2006, housing completions plunged, bottoming out at around 584,900 in 2011. And despite interest rates remaining low for much of the time since, the market was very slow to recover. As I detailed in another article not too long ago, an article that the image above has been taken from, housing inventories remain low. This is in spite of the data in the chart below, which shows that housing completions have increased materially in recent years. In 2022, for instance, they totaled 1.39 million. These go hand in hand.

Years of under-building, a slow start to increasing the number of new units out there because of the memory of the pain of the crisis, and a continuous growth in the population, ultimately culminated in the shortage that we are experiencing today. This shortage, combined with a mixture of price gouging by homebuilders and inflationary pressures that came from supply chain issues, caused housing prices to skyrocket. At the same time, rental prices also rose rather materially.

You might think that all of these factors combined would prove promising for both homebuilders and real estate investment trusts, or REITs, that are dedicated to owning and leasing out properties. In the long run, this is probably the right way to think about it. But in the short run, we are seeing some issues in the homebuilding space that should take away from their opportunity and should add significantly to the opportunities that the aforementioned REITs should enjoy.

For the purpose of this article, I decided to look at updated data associated with nine significant homebuilding companies. The largest of these, from a backlog perspective, is D.R. Horton with 19,237 units that it is currently contracted to build. The smallest player is Beazer Homes USA, with 1,858 your units in its backlog.

| Company |

| Current Backlog |

| Backlog 1 Year Ago |

| Annual Change |

| KB Home ( KBH ) |

| 7,016 |

| 11,886 |

| -41.0% |

| Taylor Morrison Home Corporation ( TMHC ) |

| 6,267 |

| 9,400 |

| -33.3% |

| Meritage Homes Corporation ( MTH ) |

| 3,922 |

| 6,695 |

| -41.4% |

| Century Communities ( CCS ) |

| 1,920 |

| 5,247 |

| -63.4% |

| Beazer Homes USA ( BZH ) |

| 1,858 |

| 3,121 |

| -40.5% |

| PulteGroup ( PHM ) |

| 13,129 |

| 19,935 |

| -34.1% |

| Toll Brothers ( TOL ) |

| 7,733 |

| 11,302 |

| -31.6% |

| NVR Inc. ( NVR ) |

| 10,411 |

| 13,443 |

| -22.6% |

| D.R. Horton ( DHI ) |

| 19,237 |

| 33,859 |

| -43.2% |

Without exception, these nine homebuilders have seen a plunge in their backlog figures over the past year. Using data from the most recent quarter available, you can see the end result in the table above. All combined, they have a backlog of around 71,493 homes. That's down from 114,888 reported one year earlier. That's a decline of 37.8% year over year. The largest decline was the 63.4% drop experienced by Century Communities. But not even D.R. Horton was immune from this drop. Its backlog is down 43.2% compared to what it was one year earlier.

As you can see in the table below, orders that came in during the most recent quarter are also lower year-over-year. This is, once again, without exception. Though it is interesting to note that the severity of the decline in orders does vary rather materially from firm to firm. For instance, D.R. Horton's orders are down only 4.9%, while the drop for Toll Brothers has been a rather monumental 50.1%.

| Company |

| Current Orders |

| Orders 1 Year Ago |

| Annual Change |

| KB Home |

| 2,142 |

| 4,210 |

| -49.1% |

| Taylor Morrison Home Corporation |

| 2,854 |

| 3,054 |

| -6.5% |

| Meritage Homes Corporation |

| 3,487 |

| 3,874 |

| -10.0% |

| Century Communities |

| 2,022 |

| 2,944 |

| -31.3% |

| Beazer Homes USA |

| 1,181 |

| 1,291 |

| -8.5% |

| PulteGroup |

| 7,354 |

| 7,971 |

| -7.7% |

| Toll Brothers |

| 1,461 |

| 2,929 |

| -50.1% |

| NVR Inc. |

| 5,888 |

| 5,927 |

| -0.7% |

| D.R. Horton |

| 23,142 |

| 24,340 |

| -4.9% |

{kind=link}

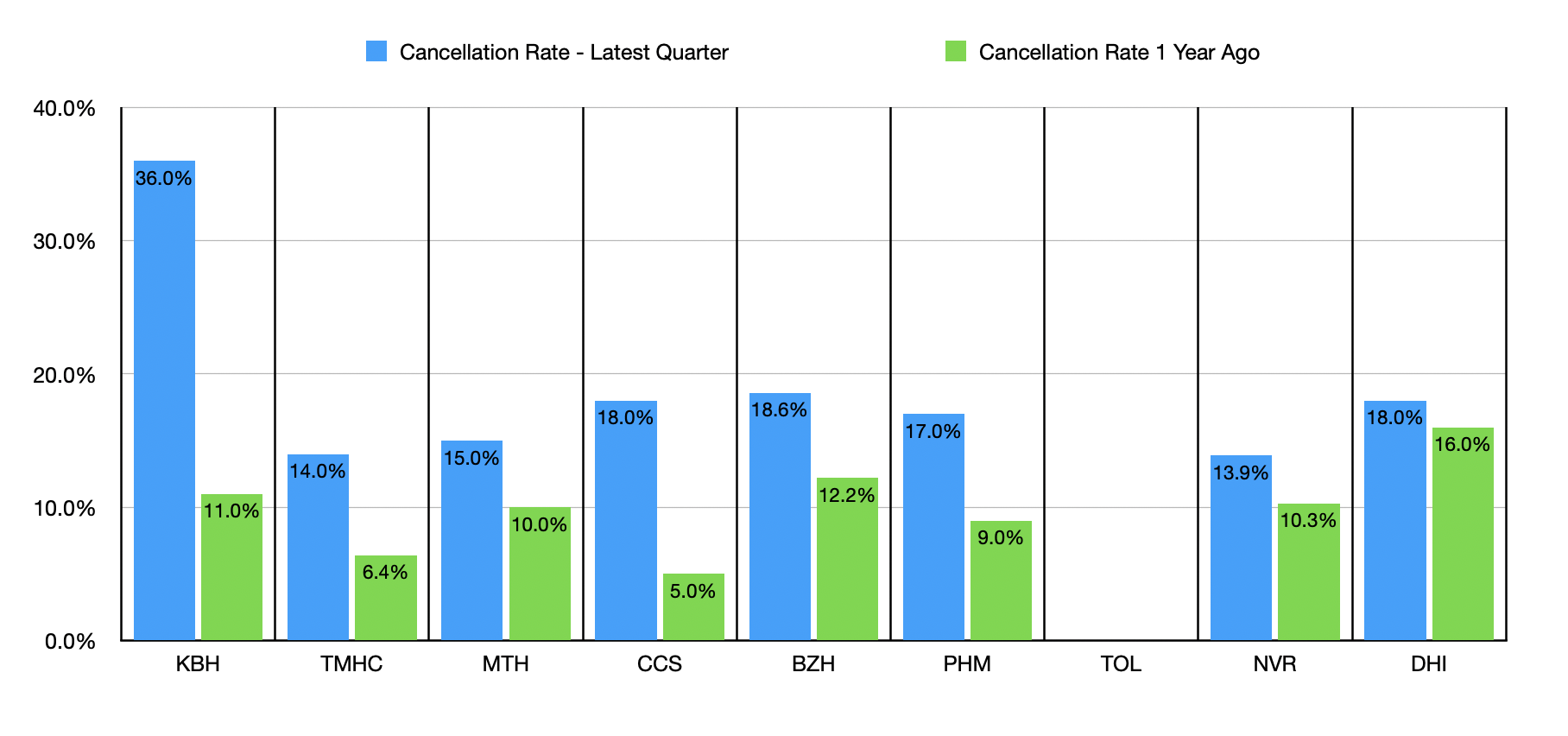

As you can see in the chart above, it's not just that orders are coming in weak. It's also that cancellation rates have risen materially over the past year. It is worth noting that the only company that I don't have cancellation rate data for is Toll Brothers, so it is missing from the chart. But odds are, its data also looks bad.

All of this is the product of a couple of different factors. What started it all was the increase in interest rates aimed at combating inflation. Given the high cost of homes, combined with the fact that they are overwhelmingly reliant on long-term financing, the housing market would be one of the first impacted and would face some of the most severe consequences of policy changes. There are other markets that are being impacted as well, such as the RV market. But it shares the same characteristics as the home building space does. The price hikes on homes certainly didn't help.

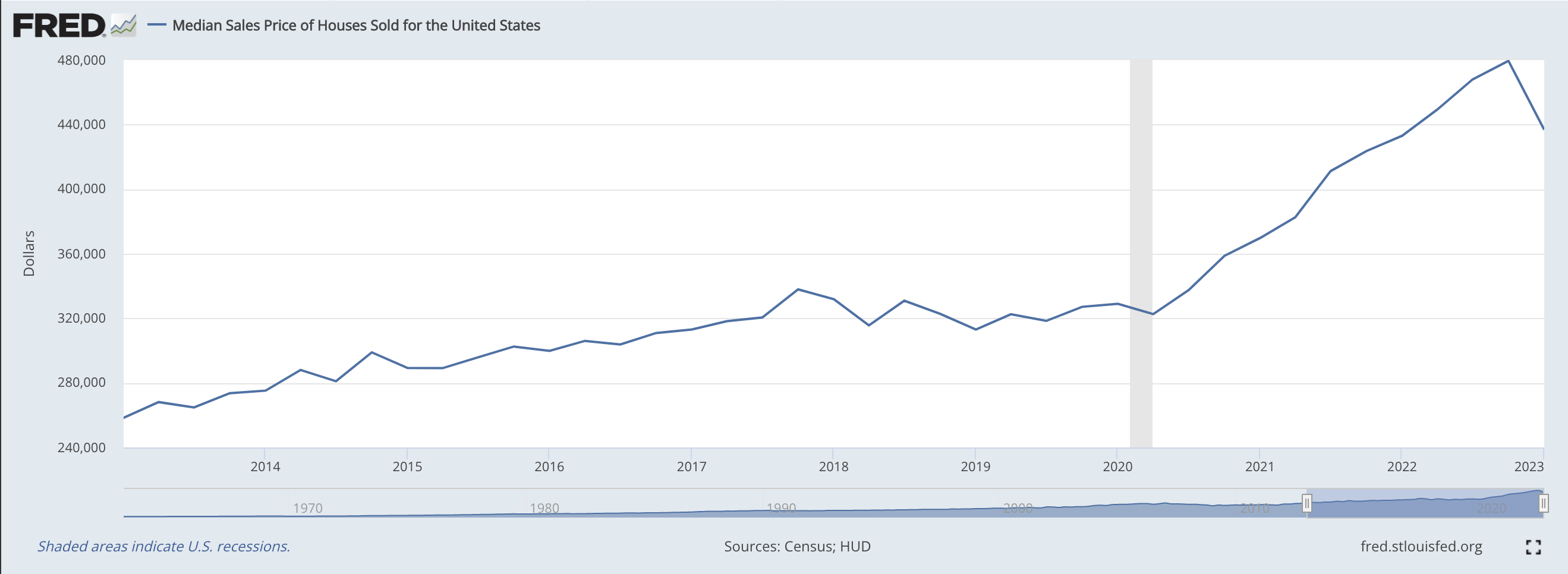

In the final quarter of 2019, right before the COVID-19 pandemic hit, the median sales price for a home in the U.S. was $327,100. By the first quarter of this year, that number had spiked to $436,800. Some of this was in response to inflationary pressures and other market forces. Other parts, I believe, involved price gouging.

{kind=link}

In the short term, this will all prove very painful for homebuilders. Though when combined with the shortage in housing that currently exists, the long-term picture for the companies that come out of this in solid shape should be quite appealing. This is most certainly an area that investors could consider buying into. But one that I think might be a bit more stable while also benefiting from this attractive catalyst would be REITs that own and lease out single family and multifamily properties.

{kind=link}

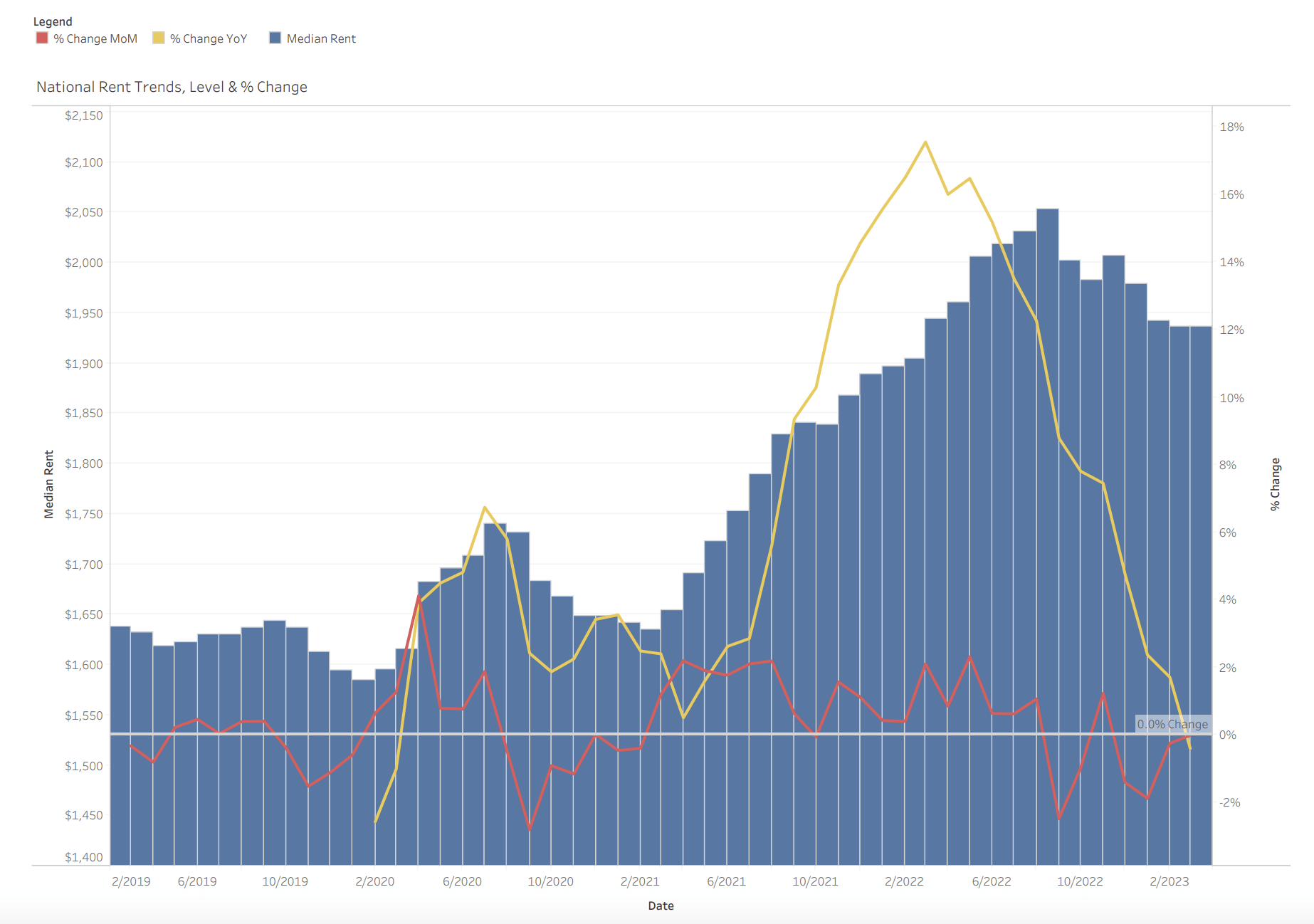

Over the past couple of years, we have seen a surge in the median rent across the U.S. Rent peaked in August of 2022 when it averaged $2,053 per month. This was up 12.2% compared to the $1,829 per month reported for just one year earlier. Even though the number of homes being built was on the rise, the increase in their cost and the continued shortage ultimately empowered those who owned properties that they were renting out to increase how much they charge. Of course, this is a very regional phenomenon. Where I live in Ohio, for instance, you can get a perfectly good place for around $1,000 per month. But elsewhere, the picture is far worse.

{kind=link}

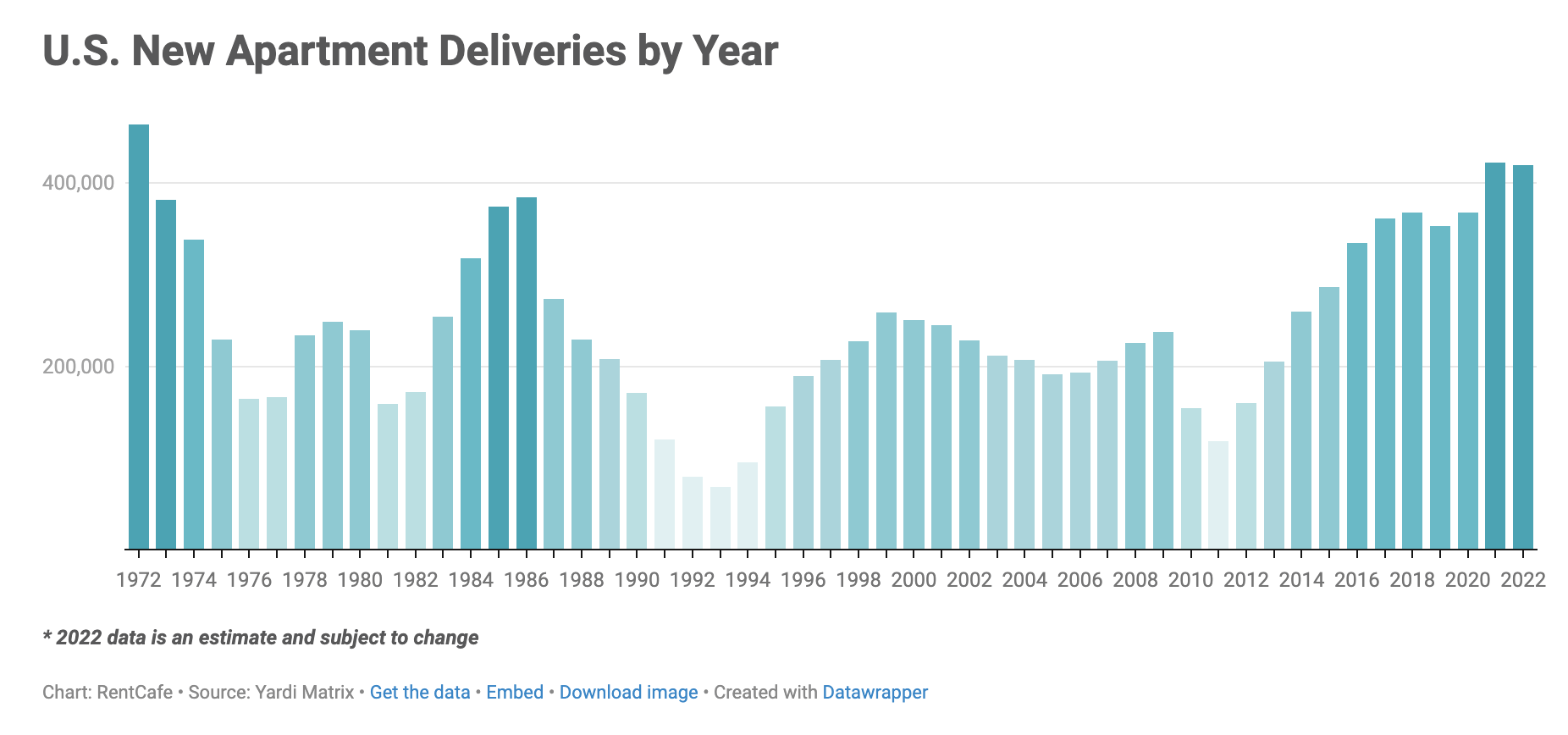

The reason for the recent decline in rental prices, with a median cost per month of $1,937 in March of this year, can largely be chalked up to the fact that new apartment deliveries have skyrocketed over the past few years. Around a decade ago, about 200,000 new apartments were being delivered each year. Over the past two years, that number has been more than double that. But if overall activity in the homebuilding space is being curtailed, you can bet that the same will apply with investment properties.

With the housing shortage likely to only worsen because of the decline in newbuilds, I would wager that REITs that own single family and multifamily properties will be able to increase how much they charge faster than home builders will be able to respond with increasing the number of properties they put out each year. This wager is backed by one of the earlier charts that showed how many years it took just for the last plunge in units to recover. Whether it's one year from now or two, this should result in more attractive pricing power for the aforementioned REITs. But even so, the market has not done anything other than punish them for the recent weakness in the rental market.

{kind=link}

{kind=link}

{kind=link}

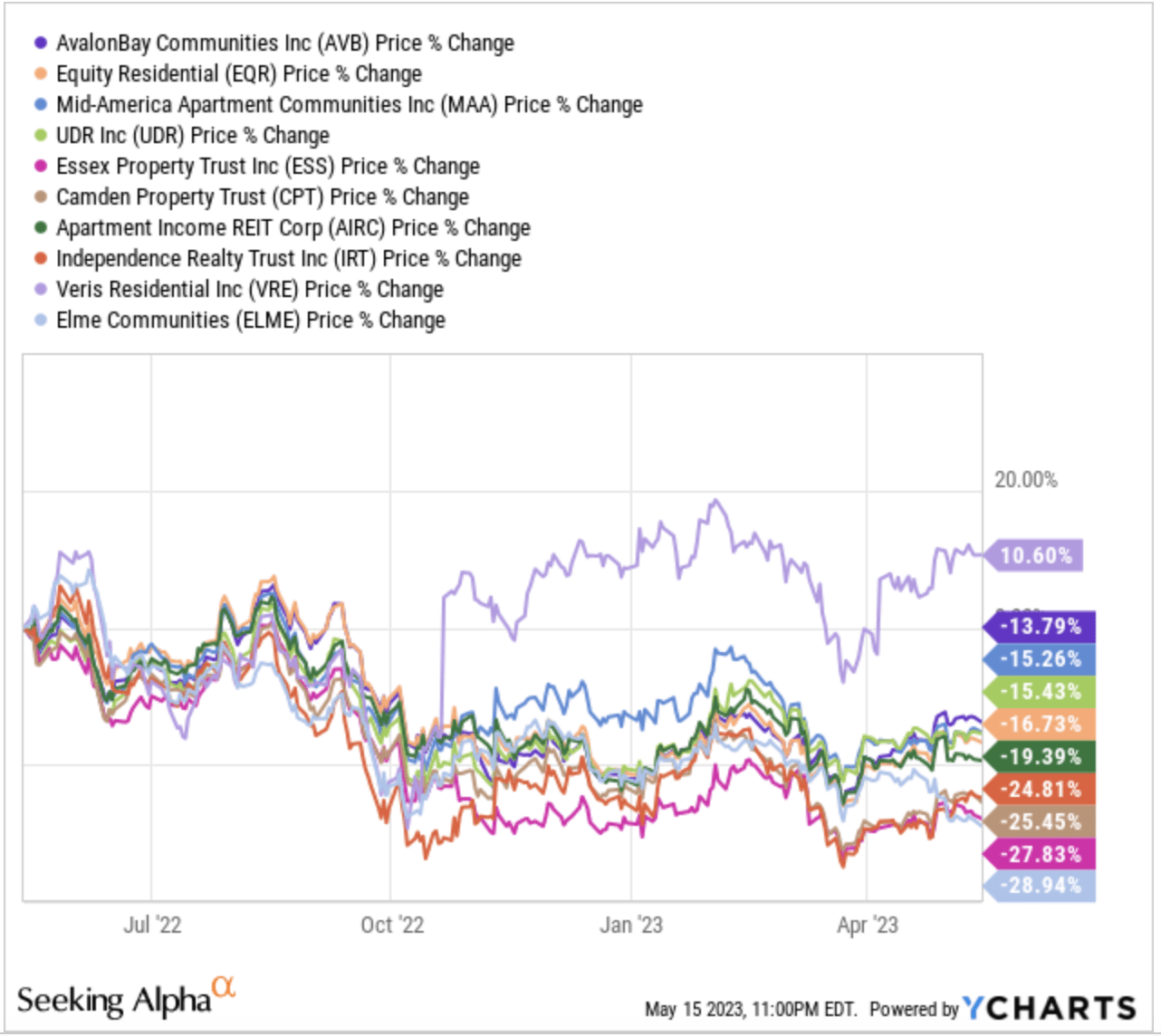

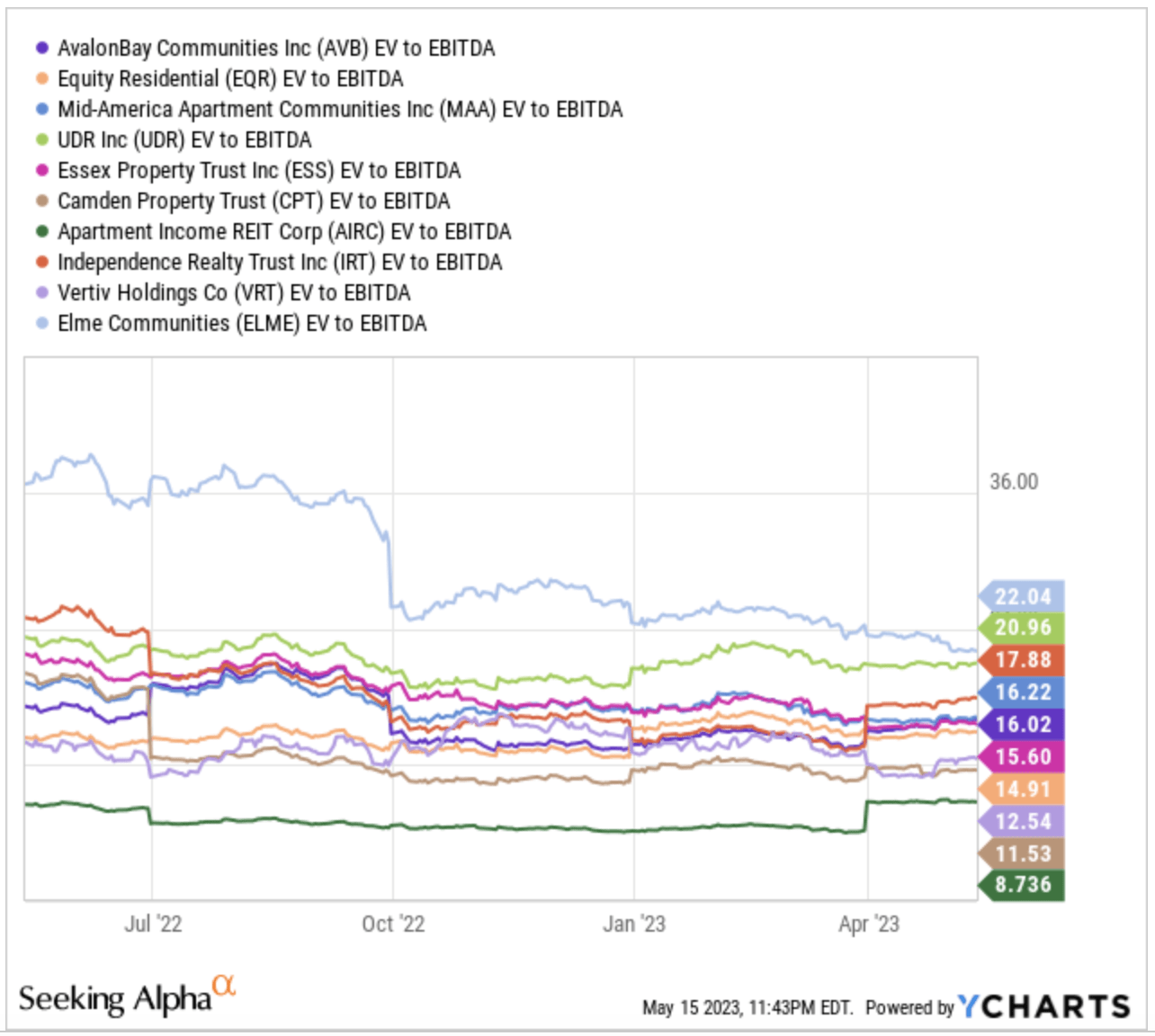

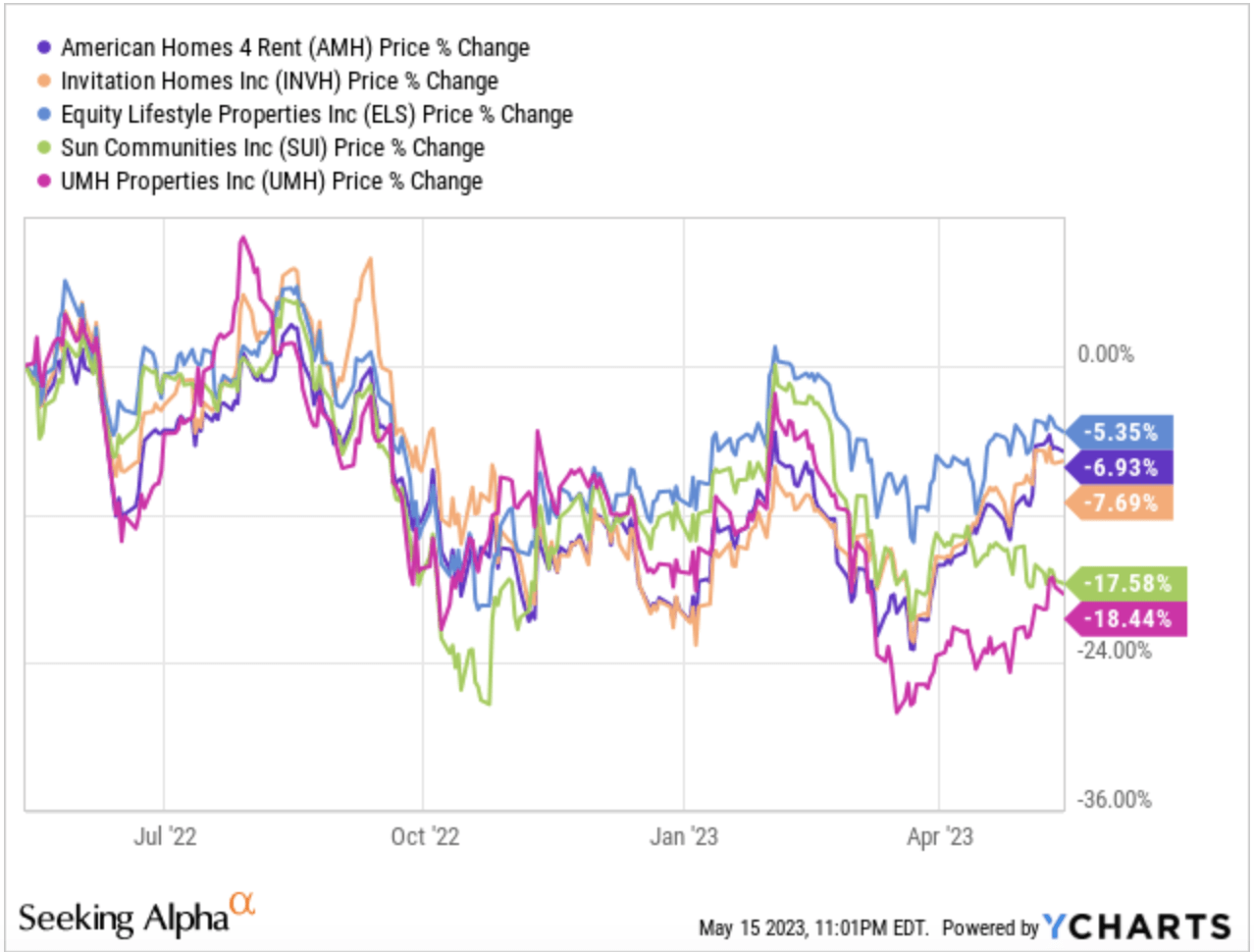

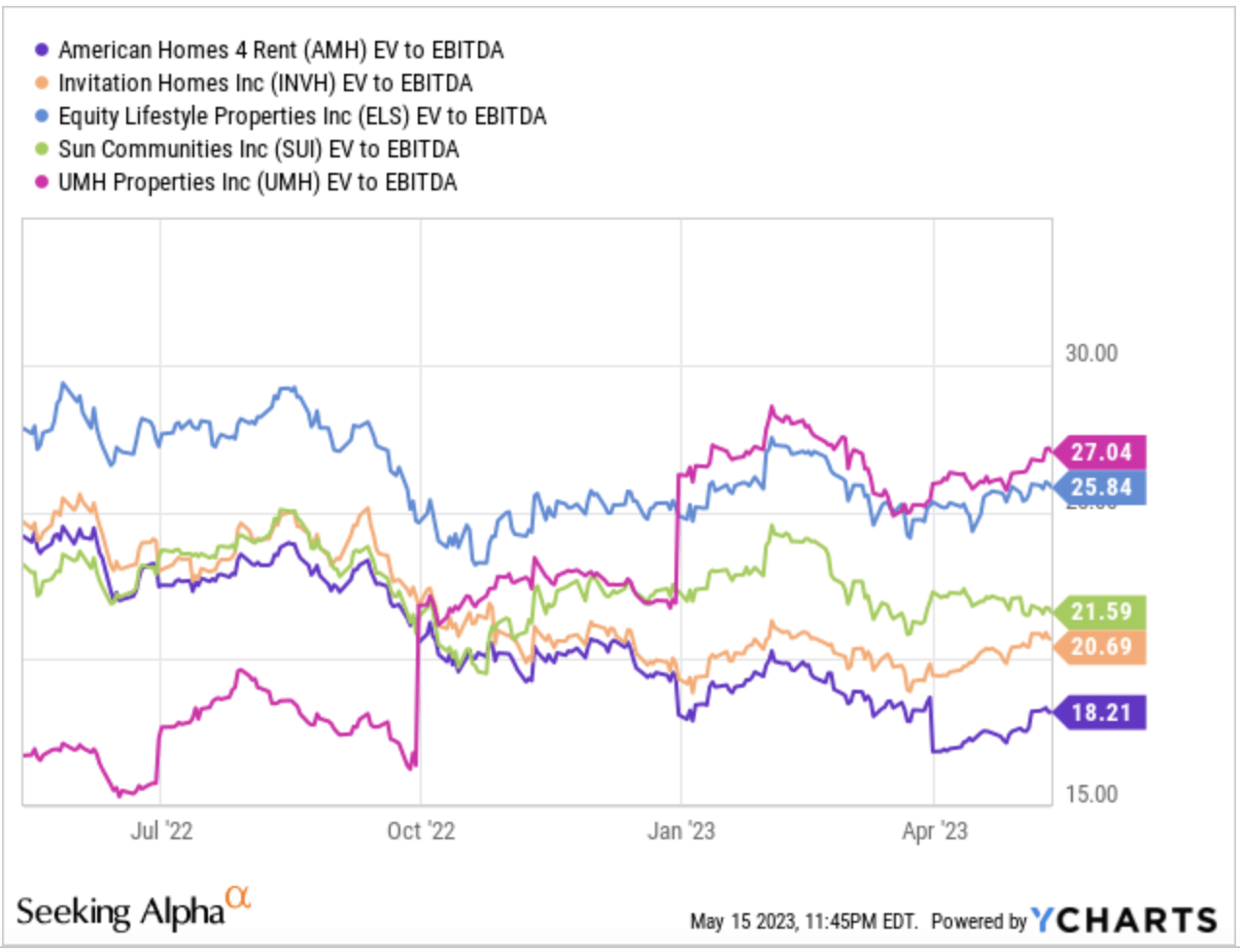

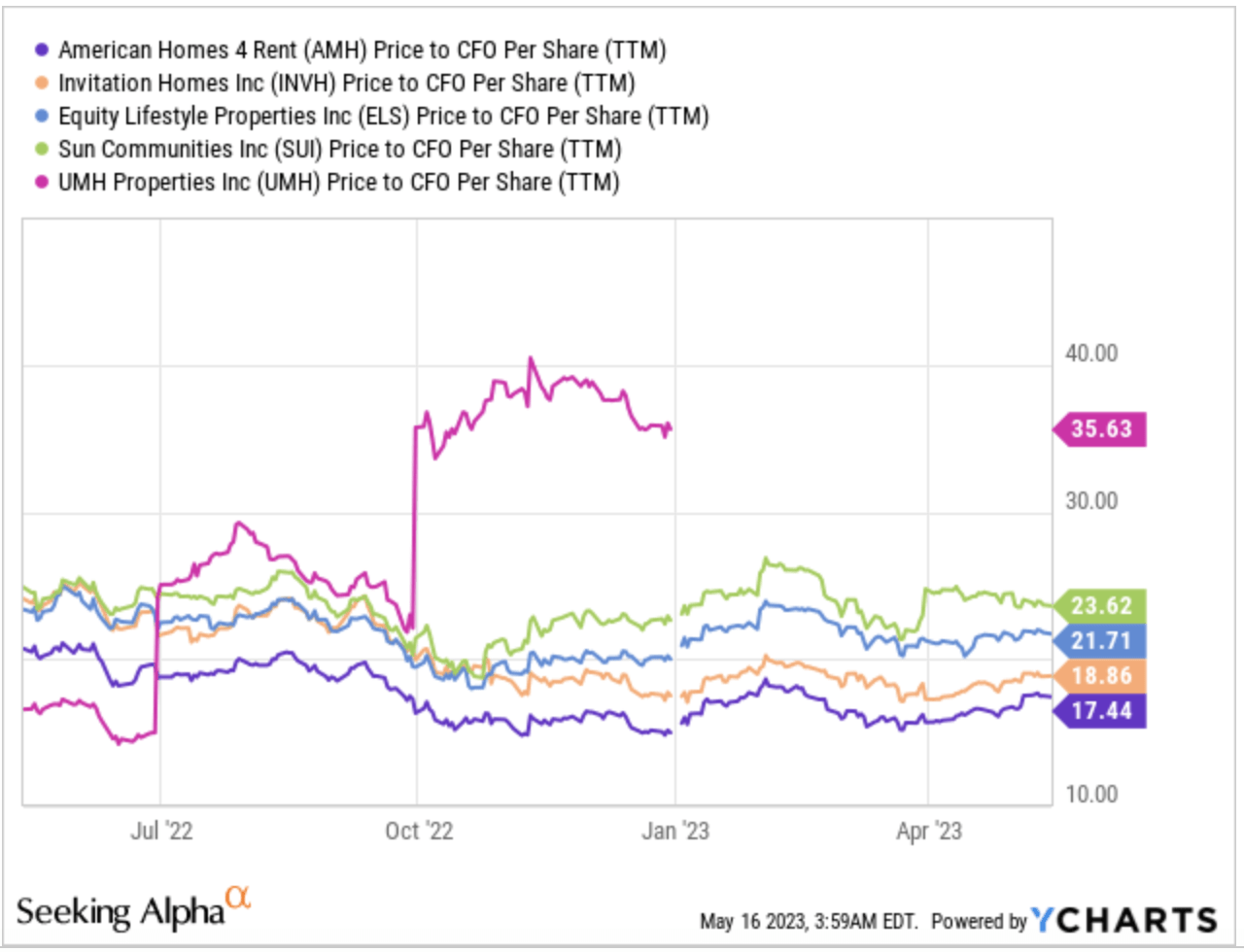

As you can see in the chart above, I looked at pricing actions regarding 10 different multifamily REITs. With one exception, they all saw their share prices plunge over the past year. The decline for the nine that did drop ranged between 13.8% and 28.9%. And for the five single family REITs I looked at in the chart below, the decline ranged between 5.4% and 18.4%. With one exception, the multifamily REITs are trading at price to operating cash flow multiples that don't seem out of place. When it comes to the EV to EBITDA multiple, however, a few of them do seem rather pricey. But there are definitely some in that basket that are trading at pretty attractive levels. As the charts below illustrate, the multiples of the single-family REITs are definitely a bit loftier. In fact, I would make the case that those firms are probably much closer to being fairly valued.

{kind=link}

{kind=link}

{kind=link}

Takeaway

Based on all the data I'm looking at, I do believe that the market is making a mistake. In the long run, I believe that both home builders and residential REITs will fare well from an operational perspective. There definitely is going to be more pain in the home building space. But that could be where some of the greatest upside is.

However, for investors who want an opportunity that seems to be mispriced and that is unlikely to see the same kind of volatility that the home building market is experiencing, a better alternative might be the residential REIT arena. The single-family firms don't look all that appealing to me at the moment. Though a case could be argued that, as the housing shortage worsens during the plunge in properties that are being built, the ability to sell those single-family units might bring in a great deal of capital. But for those focused more on the ownership and leasing out of residential real estate, the multifamily REITs might make the most sense to focus on.

For further details see:

Pain In The Housing Market Is Setting The Stage For Significant Value Creation