VNO - Pain In The Office Property Market Isn't Over Yet

Summary

- Office REITs generated the lowest returns of any property sector tracked by the Nareit since Covid hit, but returns are set to disappoint further.

- Despite optimists' hopes for a broad office recovery, remote work patterns are now too ingrained to reverse a permanent cut in office usage.

- NOI declines have been moderated by long leases and built-in rent escalations, but will accelerate as leases expire, pressuring occupancy and rents.

- Distressed building sales and foreclosures will accelerate as property loans mature and NOI drops with lease expirations.

- A tenant and investor "flight to quality" will hit the holdings of many REITs and institutional owners especially hard.

The year-end 2022 office market figures are coming in now, and they confirm what any objective observer of the office sector should have known was in the offing: Owners are taking a whupping. Despite record office employment – usually the single most important driver of office leasing – vacancy rates are reaching historic levels and will be going higher still as job growth slows in 2023 and tenants surrender their spaces when their leases expire.

The reason is obvious: Many more of us “office workers” are working at home more often. Some firms have given up their office space entirely. Many more have relaxed worker requirements to commute to an office, allowing them to reduce their space commitments and save money. Not every firm, of course, and not every worker. But enough firms and workers to make a meaningful dent in office space demand.

Plus, tenants are becoming more selective, leaving owners of obsolete buildings enduring mounting losses and facing difficult choices. Investment returns on office buildings are already weak in both the private and public markets compared to other property sectors. Those returns will only decline further as market conditions weaken and waning investor demand lowers values.

Less Office Space Demand

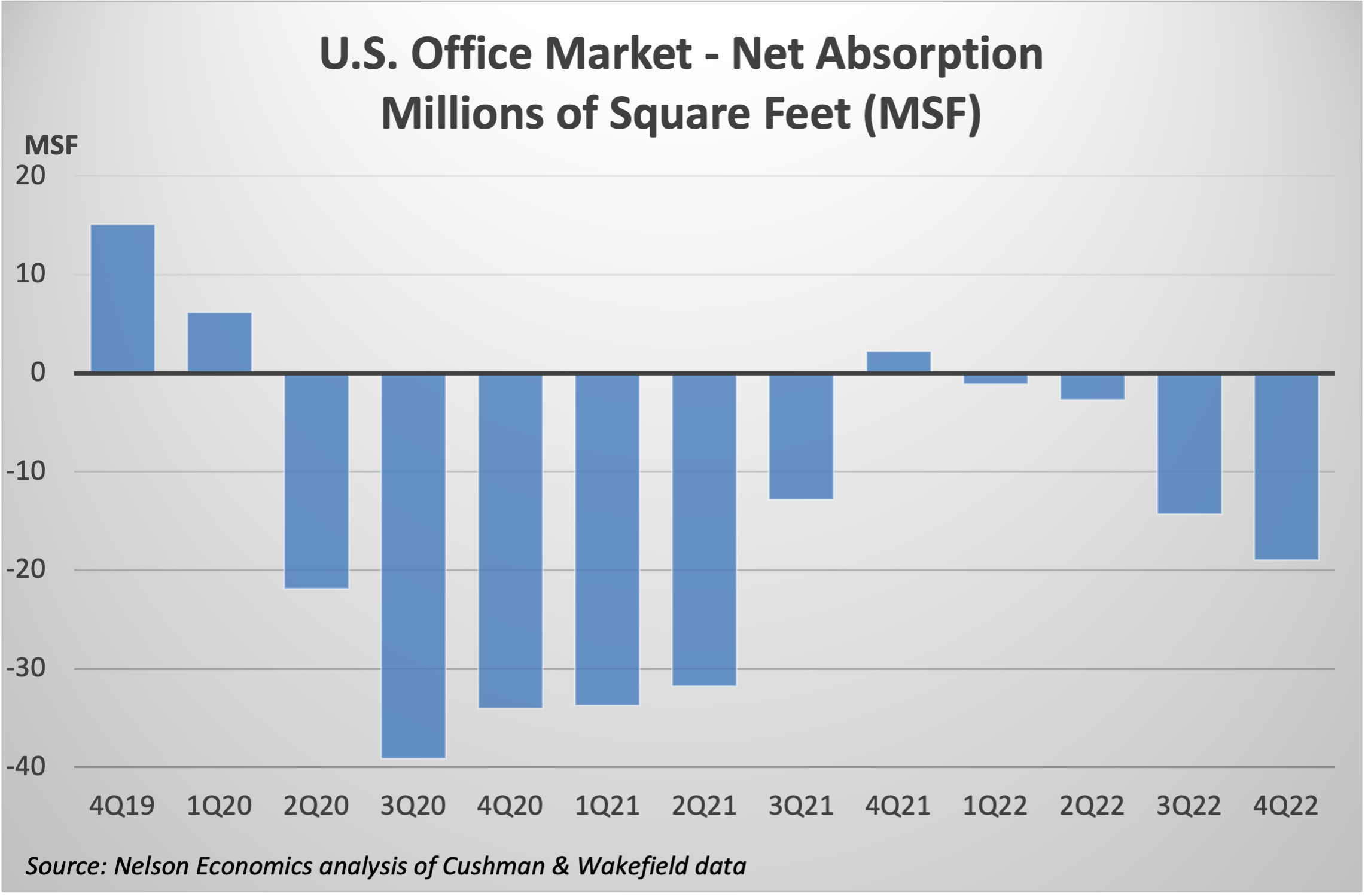

Net absorption of office space – new leasing minus lease expirations – has been negative in ten out of the last eleven quarters. That is, firms have given back more space than they have leased. And absorption has been successively more negative in each of the previous four quarters (Exhibit 1)

Nelson Economics analysis of Cushman & Wakefield data

{kind=link}

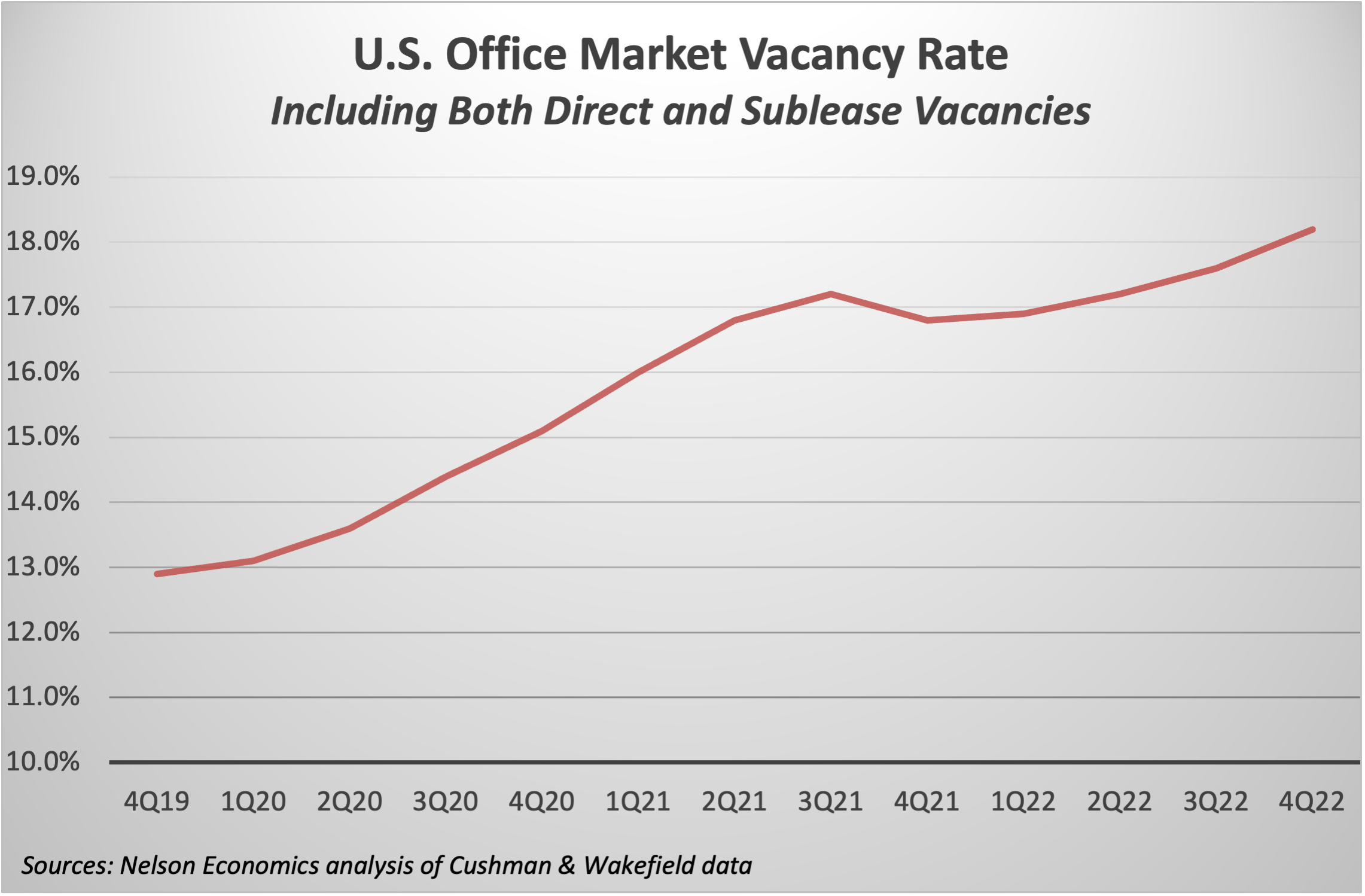

All told, leased space fell by more than 200 million square feet nationwide over the past three years, according to Cushman & Wakefield, a leading real estate brokerage firm. On top of that, C&W tallies new space deliveries exceeding 150 million square feet over this period. After deducting demolished buildings, that translates into almost a 50% jump in vacant space since the end of 2019, as the vacancy rate climbed from less than 13% to over 18% (Exhibit 2) . No other property sector has experienced a comparable decline in occupancy.

Nelson Economics analysis of Cushman & Wakefield data

{kind=link}

A year ago, it seemed that the office market might turn the corner to recovery. Leasing activity accelerated as Covid was finally receding and more firms began to renew leases, though few tenants were actually expanding their space. But those encouraging signs in late 2021 were brief, and now the office downturn is accelerating – despite record employment in the normally office-based sectors and positions.

The Damage to Owners and Investors

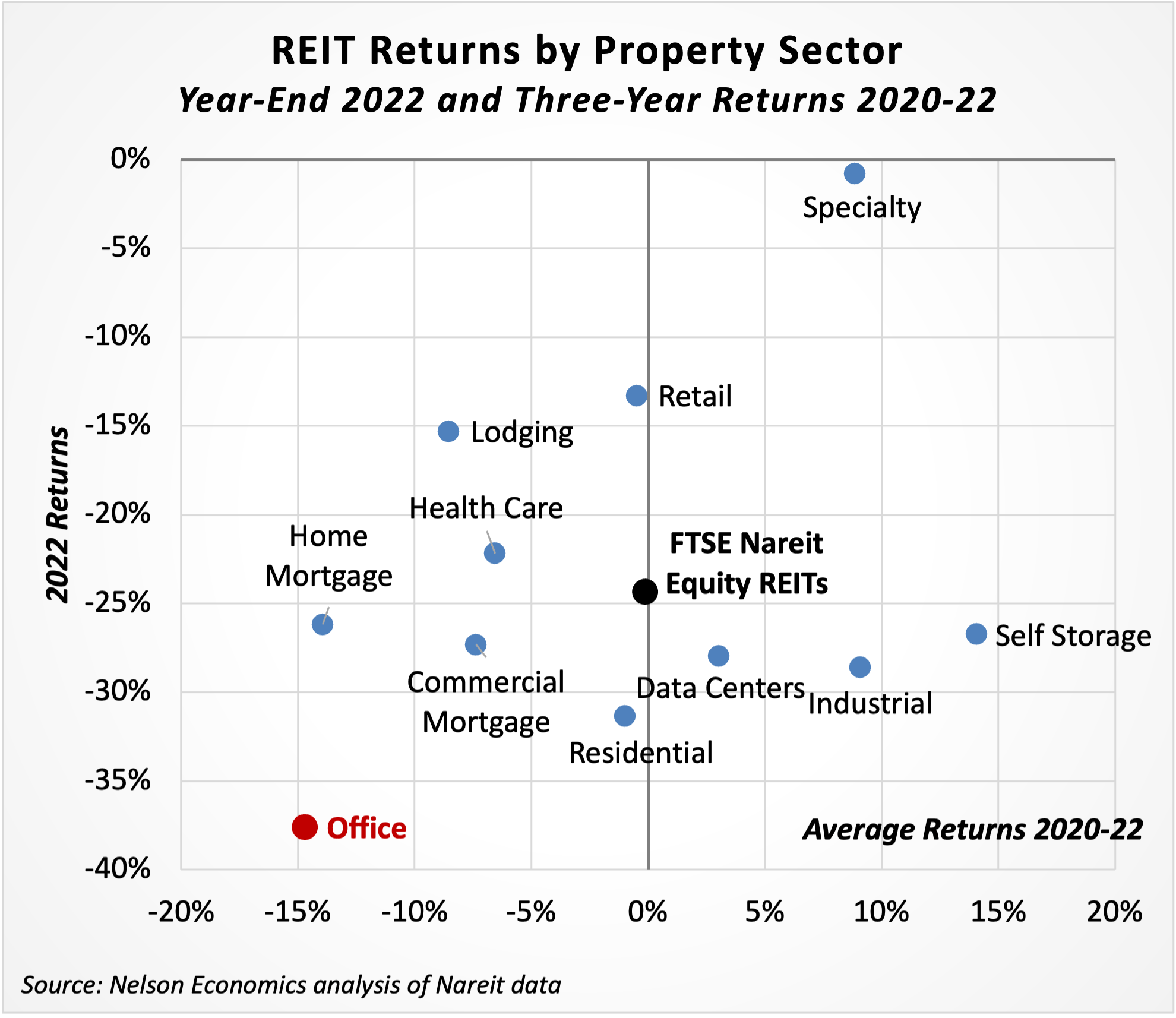

The challenging operating environment for office buildings has driven down investment returns in the private and especially the public markets, which tend to lead the private markets and can be a valuable, if unreliable, gauge of future underlying asset values. (REITs often overshoot the eventual trends in private markets.) Office REITs generated the lowest returns of any property sector tracked by the National Association of Real Estate Investment Trusts (Nareit) both in 2022 and for the three pandemic years (Exhibit 3) . With a return of -37.2% last year, office returns badly lagged overall REIT returns as measured by the FTSE Nareit Equity REITs Index (FNER), underperforming by almost 13 percentage points; ((PP)); the three-year average return of -14.7% lagged the FNER by almost 15pps.

Nelson Economics analysis of Nareit data

{kind=link}

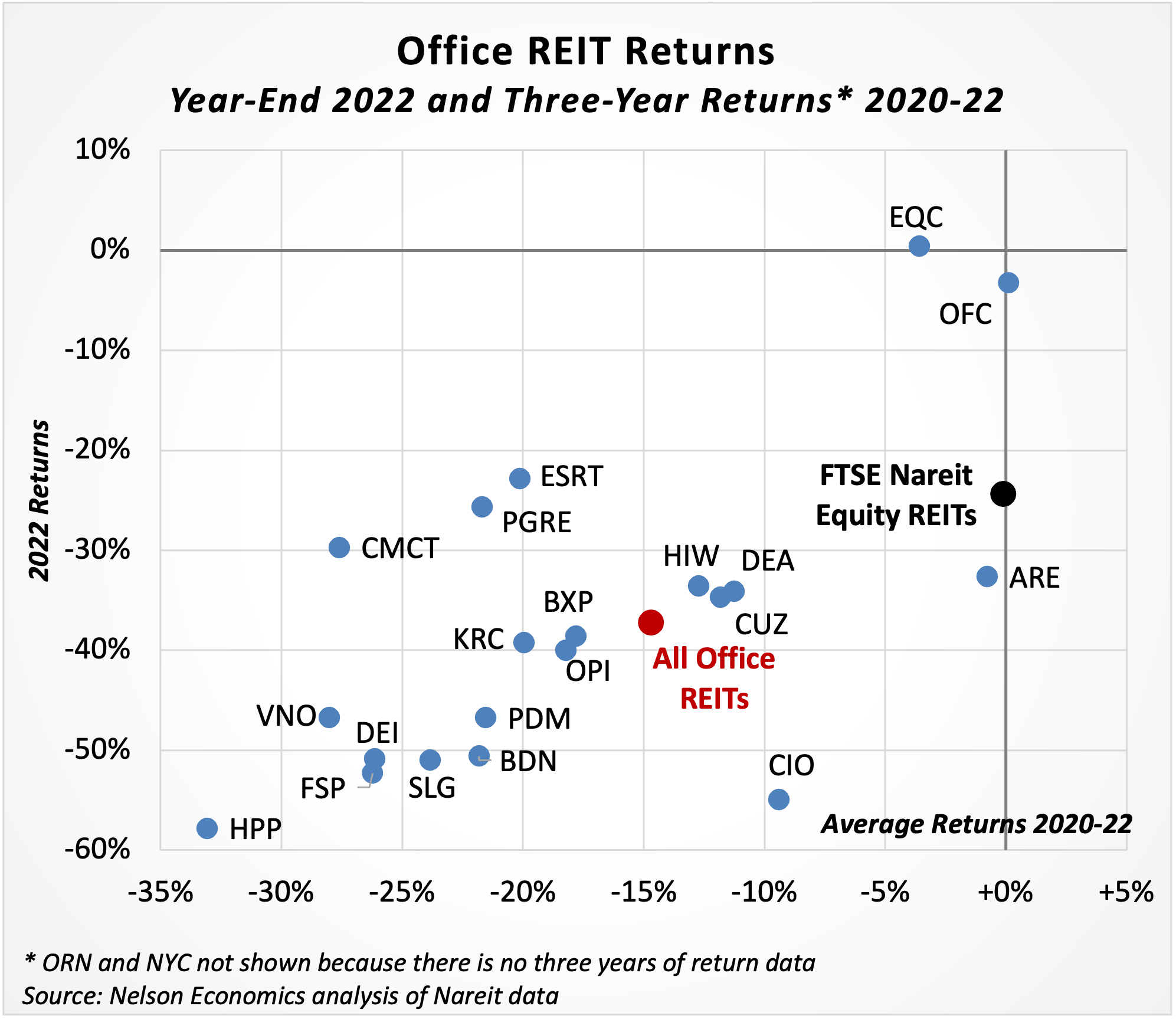

Underperformance among office REITs is nearly universal. Only two of 22 office REITs in the index bested the all-sector FNER index in 2022: Equity Commonwealth ( EQC ) and Corporate Office Properties ( OFC ), which together account for just 8% of the equity value of all office REITs (Exhibit 4) . And only OFC beat the REIT index over the past three years. Importantly, neither of these relatively small funds is a typical office REIT. EQR owns just four assets in three markets while OFC primarily serves the “United States Government and its contractors, most of whom are engaged in national security, defense, and information technology related activities.”

Nelson Economics analysis of Nareit data

{kind=link}

Average returns in the sector would be even weaker were it not for the inclusion of Alexandria Real Estate Equities ( ARE ), which arguably is not even an office REIT in that it owns only life science buildings. Life science is a highly specialized asset type generally viewed as a niche real estate sector with different drivers and market dynamics than traditional office. ARE has been among the top-performing office REITs in recent years, partly reflecting the overall strength of life sciences, and accounts for over a third of the equity value in the office REIT index. Excluding ARE from the index would push average returns in the sector further below those in other property sectors.

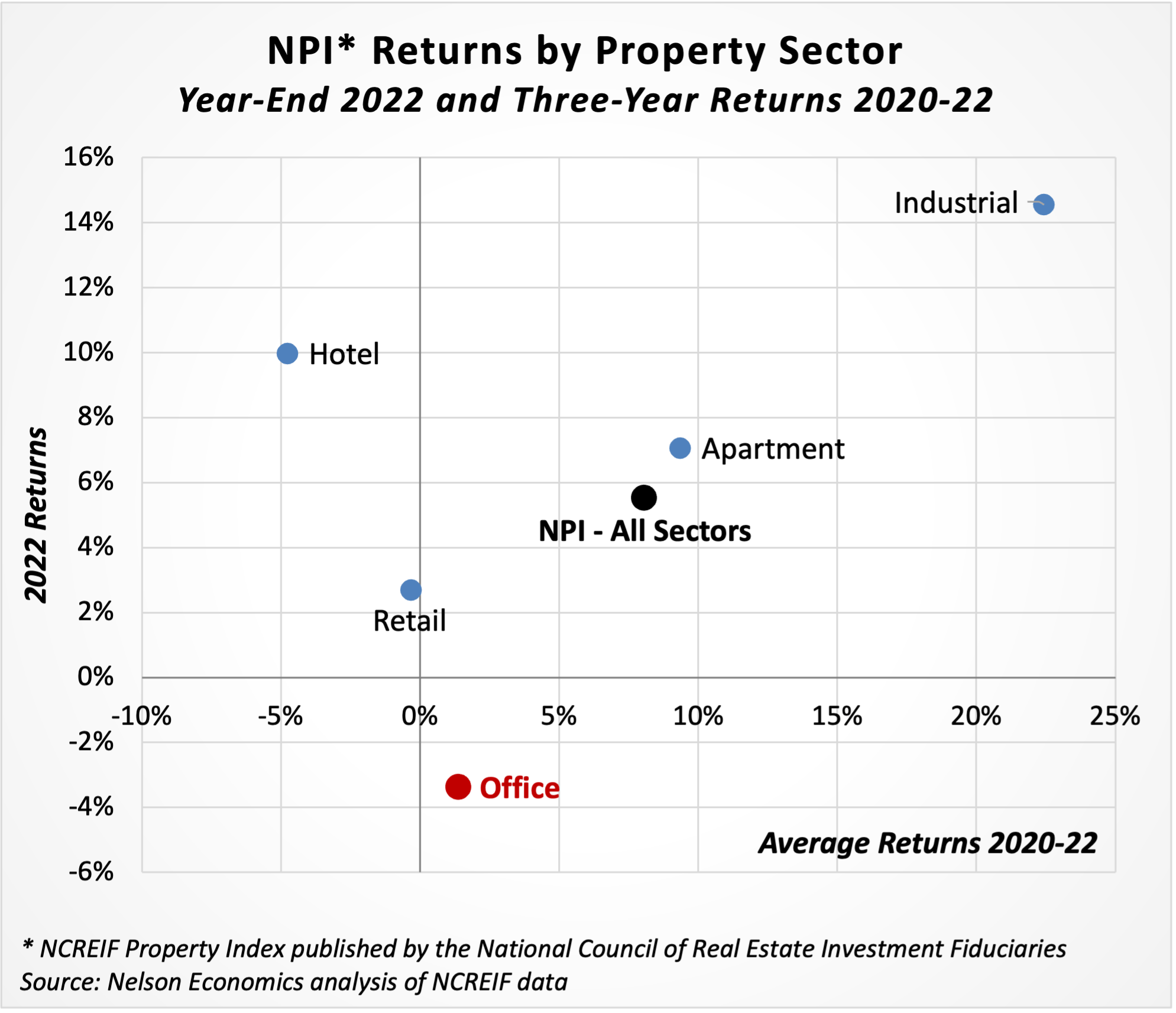

The story is similar in the private real estate market, if less extreme, as market dynamics are less dynamic, primarily due to “appraisal lag.” (Whereas assets are effectively repriced every trading day in the public markets, privately-held assets are revalued only when sold or when scheduled for appraisal, which can be quarterly or even annually.) Returns in the office sector were the lowest of any property sector over the past year, according to the National Council of Real Estate Investment Fiduciaries (NCREIF), which tracks investment returns by institutional investors like pension funds and other large private investors. Offices were the only major sector with negative returns in 2022 (Exhibit 5) . Over the three years since the pandemic started, office returns have been less than a fifth of the average for all major real estate sectors as measured by the NCREIF Property Index (NPI).

Nelson Economics analysis of NCREIF data

{kind=link}

Stable Income but Falling Values

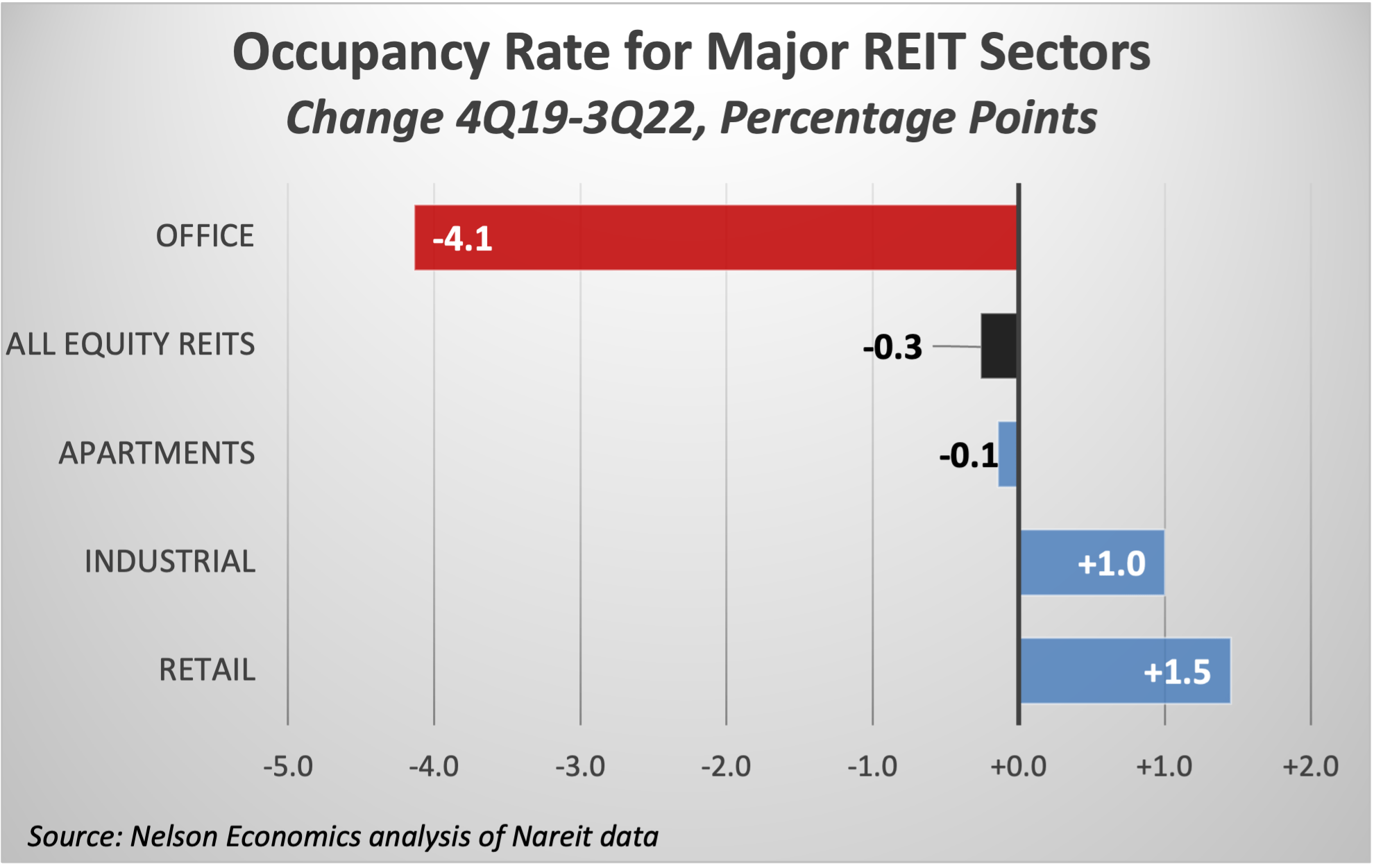

What’s driving the office sector's underperformance? Perhaps surprisingly, not the rise in vacant space. Occupancy across all office REITs has declined from 93.5% at the end of 2019 to 89.4% in the third quarter of 2022 (latest data available) – by far the greatest drop of any major sector (Exhibit 6) .

Nelson Economics analysis of Nareit data

{kind=link}

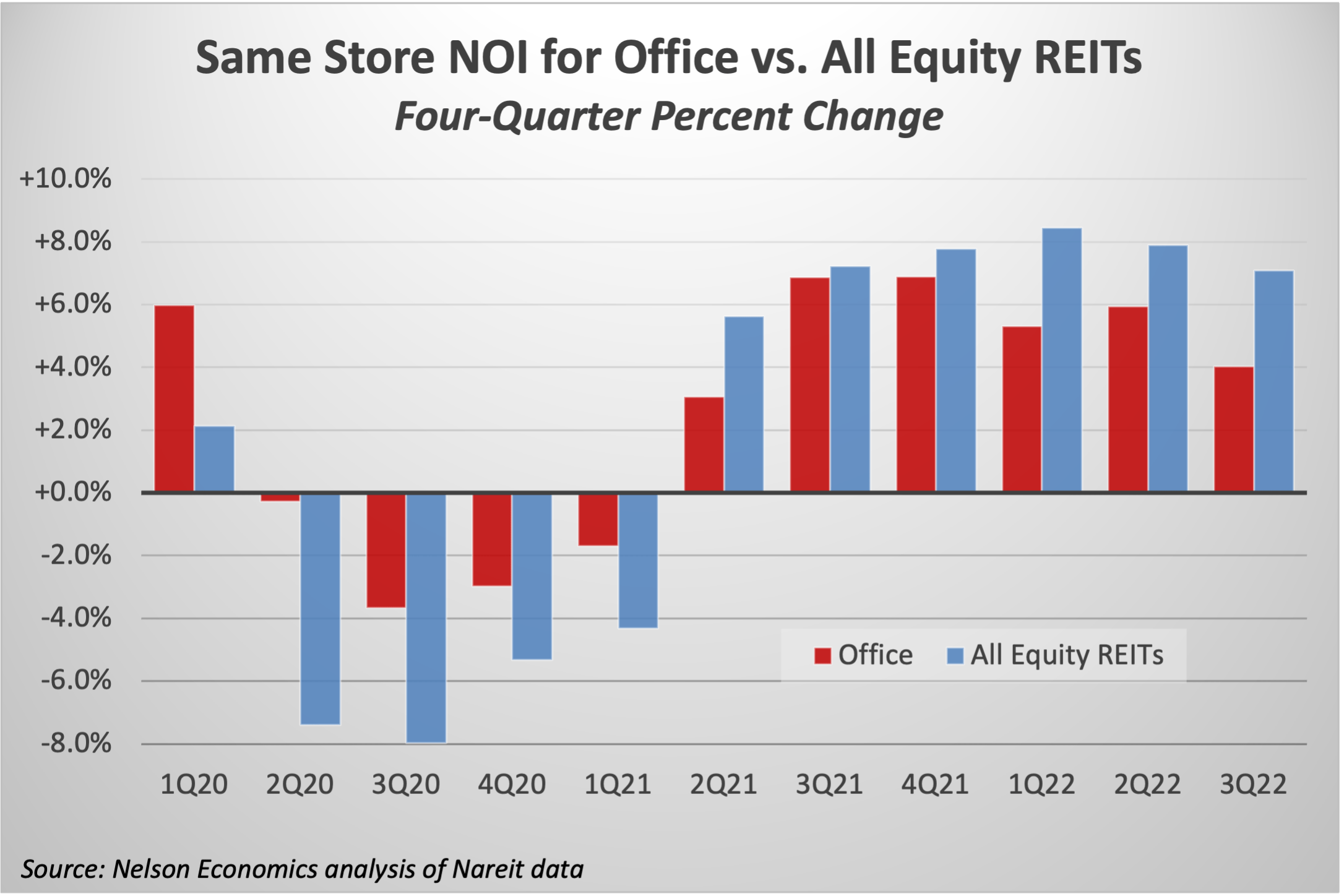

Nonetheless, revenue has been remarkably resilient. Office leases typically have built-in rent and expense escalations, often tied to inflation rates, so net operating income (NOI) can rise even as occupancy falls, particularly in an inflationary environment. Thus, the four-quarter percent change in office REIT same-store NOI – roughly equivalent to annualized growth – has been positive for the last six quarters (Exhibit 7) . Office NOI growth even beat the average for all REITs in the first year of the pandemic – or, more accurately, fell by less – due to the stabilizing impact of long-duration office leases.

Nelson Economics analysis of Nareit data

{kind=link}

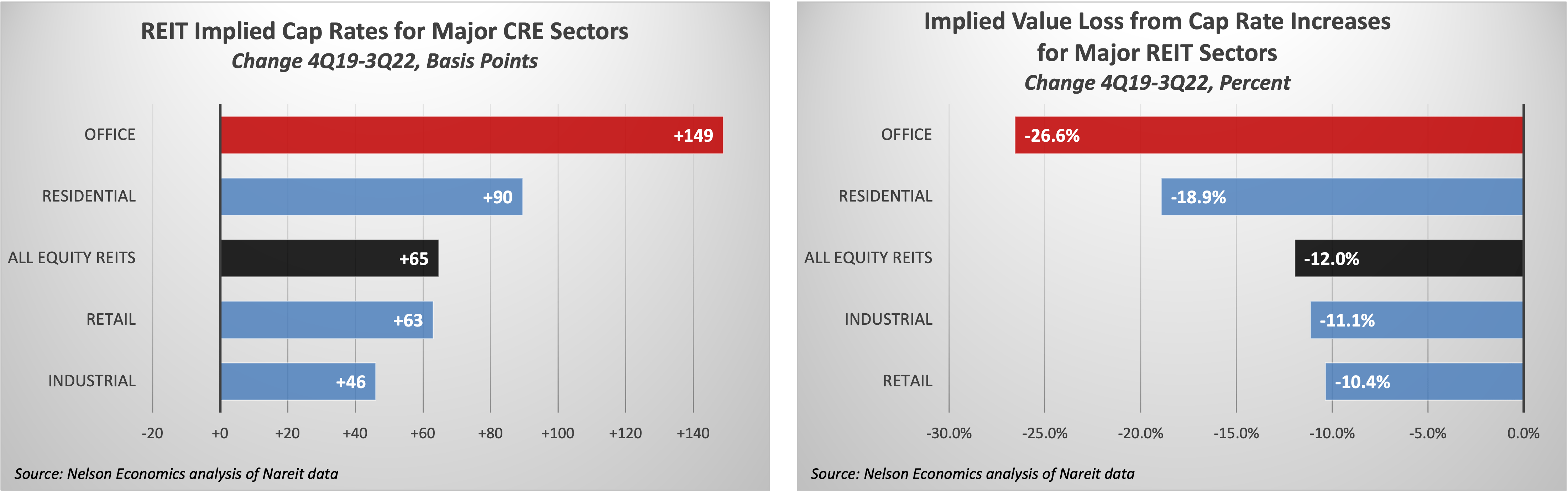

What then accounts for the plunge in office REIT values and returns if NOI has generally been rising? Investors' expectations about the durability of future income streams. Office capitalization rates have been rising, increasing the most of any primary REIT sector both absolutely and relative to its starting cap rate. (Like interest rates, cap rates move in the opposite direction from values.) Office cap rates have increased 149 basis points since the end of 2019, equivalent to a nearly 27% decrease in value (Exhibit 8a) – again, the most of any major property sector and more than twice the implied 12% value decline in the all-sector REIT index (Exhibit 8b) .

Nelson Economics analysis of Nareit data

{kind=link}

Cyclical and Structural Cuts to Office Demand

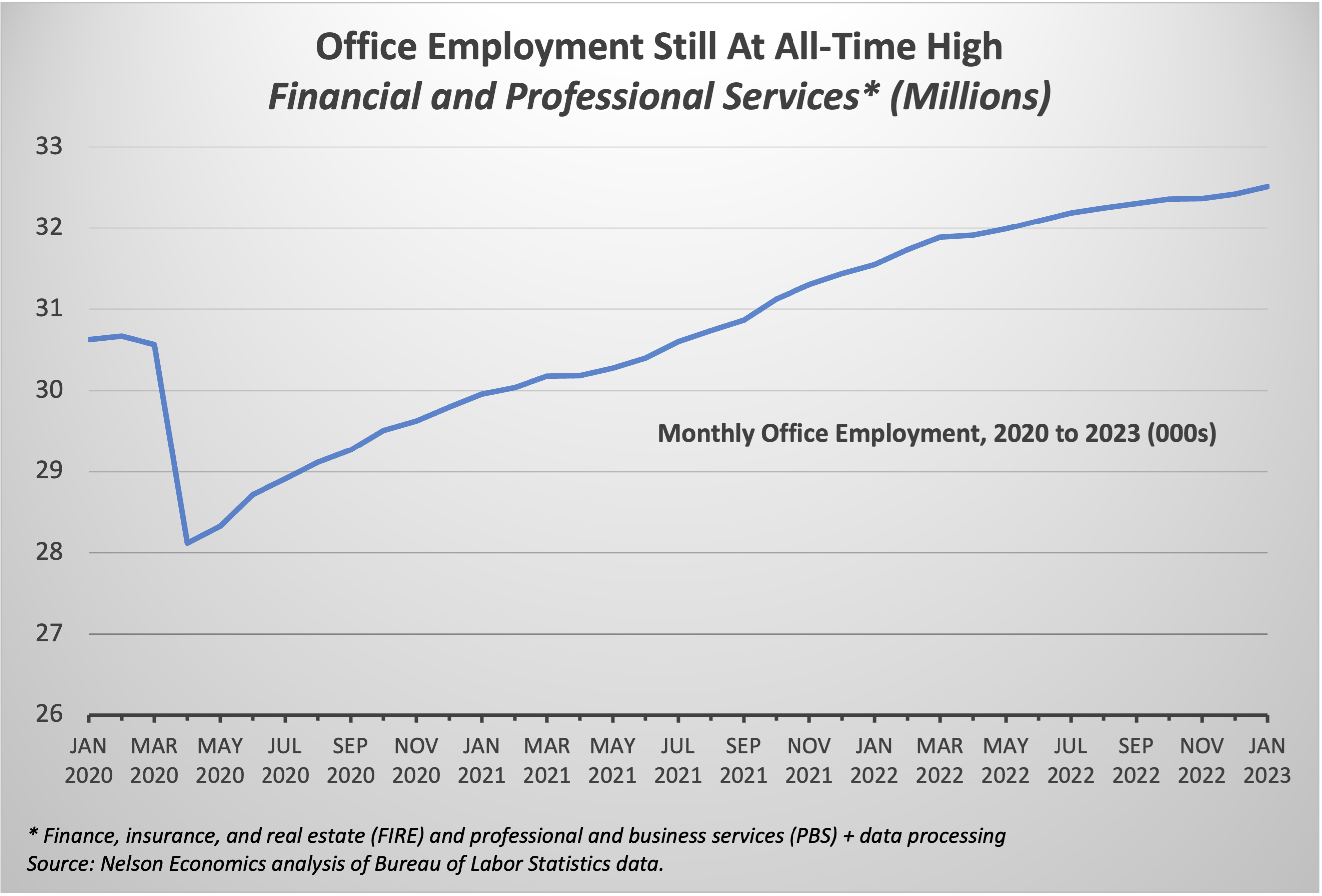

Investment returns and office valuations are now set to weaken further due to both cyclical and structural reasons. The cyclical is the more immediate. The precipitous decline in office leasing over the last year is occurring despite record “office” employment – the knowledge jobs in finance, tech, and professional services that typically are office-based (Exhibit 9).

Nelson Economics analysis of Bureau of Labor Statistics data.

{kind=link}

Of course, even before Covid, not all these professionals worked in office buildings, and many workers in other sectors, like government and education, also frequently work in offices. But finance, tech, and professional services are the primary drivers of office space demand. Despite the blockbuster January jobs report, growth undoubtedly will slow and perhaps reverse in 2023 as the Fed clamps down on inflation and slows the economy, further paring office space demand and occupancy.

But cyclical swings are, by definition, transitory, and that demand should eventually return as the economy again expands in 2024 and beyond. More problematic for owners are the structural changes permanently undercutting office space demand. Simply, firms are slowly coming to accept that most of us will not be returning to the office as frequently as in the “before times.”

Widely-cited estimates compiled by Kastle Systems based on keycard swipes in office buildings show that three years after Covid paralyzed the nation, only about half of office workers are back at their company desks on an average day, and attendance on even the highest occupancy days don’t exceed 60% in most cities. It’s simply too convenient for workers while providing tangible benefits for their employers.

Most importantly, occupancy costs are too material for firms to ignore potential savings. Space reductions won’t be commensurate with the share of days worked remotely. More workers tend to show up midweek to collaborate with colleagues, so firms must provide the space needed for the maximum usage days. The amount any individual firm will be able to reduce their space depends upon their particular workflow and location strategy, but the emerging consensus is that demand will decline by some 15% relative to pre-Covid trends.

Some industry optimists argue that an economic slowdown will tilt labor force dynamics back to employers, who could then insist that their workers return to the office. Don’t count on it. After three years of working from home, hybrid work is too ingrained to give up, particularly for the most-valued knowledge workers who used to fill Class A office buildings.

The Slow-Motion Train Wreck

Why hasn’t the drop in leased space matched the decline in the amount of space firms are actually using? First, most firms initially believed remote working would be relatively short-lived, so they didn’t want to give up their valuable office space if they would soon be back in the workplace. More importantly, most office leases run for at least five years – and often much longer – and cannot be easily forsaken except via bankruptcy. That’s how many firms break their commitments in recessions, when bankruptcies normally surge. The brief Covid recession in 2020 was different, however. Generous government relief benefits kept firms afloat, so tenants couldn’t quit their leases even if they wanted to. They had to wait for their leases to expire.

Now three years later, vacancies are still rising, with no end in sight, as leases finally roll and firms either do not renew or opt for less space. One clear sign of what’s ahead is the amount of unused space available on the sublease market. Real estate firm Avison Young estimates that sublease availability now exceeds 200 million square feet – more than all the office space in Houston or Boston. And this pool of vacant space is multiplying. Cushman & Wakefield calculates that sublease space accounts for 40% of the empty space added in 2022. This vast reservoir of shadow vacancies not only competes with regular vacancies, pressuring market rents, but also serves as a leading indicator for future landlord vacancies.

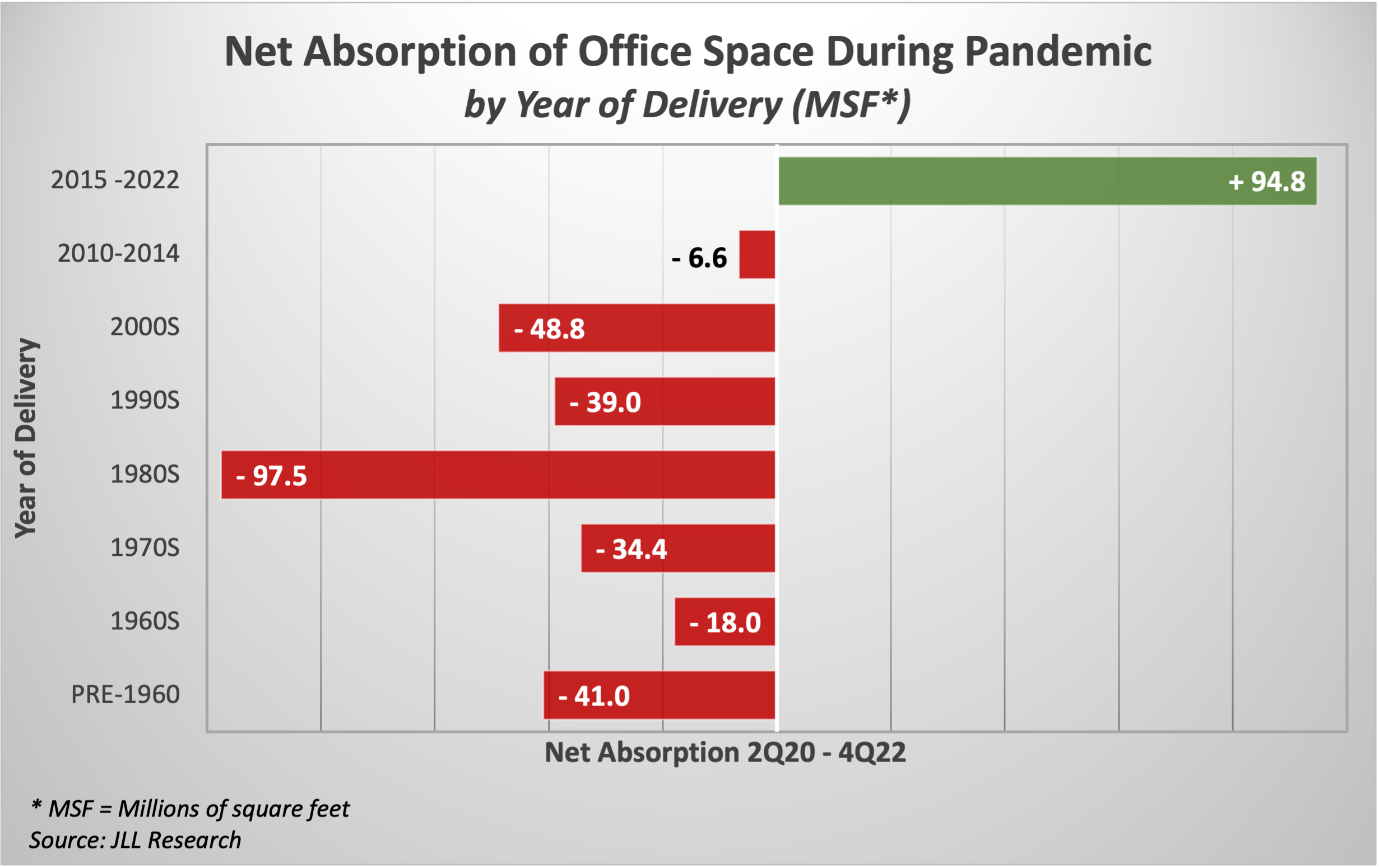

This means property revenues will decline as both occupancy and rent levels fall. The pain will not be shared equally across the office landscape, however. The office sector is experiencing a tenant flight to quality that mirrors the split that has bisected the retail sector for over a decade. In this “trophy or trauma” market, tenants are paying record rents for the best new buildings, even as owners of older offices face rising vacancies and falling rents. Data compiled by JLL Research shows that buildings completed since 2014 are seeing strong tenant demand, but net absorption since Covid hit has been negative for every other vintage of construction – particularly offices from the 1980s, when much of today’s inventory was delivered (Exhibit 10).

{kind=link}

Many of these buildings were considered “Class-A” until recently but now are increasingly regarded as toxic, unwanted by tenants at anywhere near their former lofty rents. Changing tenant requirements have rendered them functionally obsolete because rents cannot justify the enormous costs of renovating them to modern standards in the Covid era.

The Coming Wave of Foreclosures and Distressed Sales

This permanent decline in tenant space demand is prompting a decisive swing in investor demand away from office product and a corresponding drop in values. Exactly how much is hard to gauge because there are so few sales for non-trophy properties. MSCI reported that the deal volume in the office sector fell 25% in 2022, the most of any primary property type. Ironically, average office prices continue to rise in many markets because only the best assets are selling. However, a wide bid-ask spread for the rest means deals are not getting done as the market is still in the process of price discovery.

Nor have there been many distressed sales or foreclosures. But that will be changing as leases expire and property debt matures. As tenants give up space, owners will face the difficult decision of whether to invest additional capital in not only tenant space improvements but also building-wide system upgrades that tenants now require. Many landlords will find that the likely rent streams do not justify these investments. Further, many of these owners will face maturing debt that can only be replaced at much higher interest rates – if they can satisfy the operating covenants. As a result, we can expect a wave of distressed sales and foreclosures as owners capitulate to the new market reality.

Examples are multiplying. Last week RXR, a prominent property owner focused on the New York market, announced they are preparing “give the keys back to the bank” for around 10% of its office portfolio. Then Vornado Realty Trust ( VNO ) announced they are taking a $480 million impairment charge – on top of a previous charge of $409 million – on a portfolio of midtown Manhattan assets, equal to a 35% write-down in all. And now, this week, GFP Real Estate has defaulted on a $103 million CMBS loan on an iconic Art Deco-style building. Not all markets have fared as poorly as New York, but this market accounts for a disproportionate share of assets in office REITs and institutional investor portfolios.

The coming market distress will accelerate value declines, further reducing returns on office REITs and private office portfolios. Not all offices. Even as space in older buildings goes wanting for tenants, there’s still plenty of new high-end construction. At the same time that RXR is giving up on some of its older assets, it is still proceeding with 175 Park, a $3 billion office building in midtown, which will be the tallest building in the country when completed.

This duality is at the heart of the new office market dynamics. The best buildings will continue to attract capital, while many older buildings will languish as tenants use less space overall and opt for more modern buildings when they do lease space. Like the proverbial guy who jumps out of a high-rise (office?) and halfway down thinks, “so far, so good,” investors should not be reassured by the relatively moderate losses to date. There’s a lot more downside to come.

For further details see:

Pain In The Office Property Market Isn't Over Yet