PALAF - Paladin Energy: Gearing Up For Langer Heinrich Restart In 2024

2023-04-12 07:30:00 ET

Summary

- Paladin Energy owns a majority stake in the Langer Heinrich Uranium mine in Namibia.

- The mine was placed on care and maintenance in 2018 but will be back in production in 2024.

- The steady-state production rate will be achieved in 2025, resulting in a production rate of 6 million pounds (on a 100% basis) at an AISC of just over $30/lb.

Introduction

In 2017, I expected Paladin Energy ( OTCQX:PALAF ) to face very difficult times as the company was facing a liquidity crunch . Now, six years later, Paladin is getting ready to restart the production at its Langer Heinrich uranium mine in Namibia which was put on care and maintenance in 2018 due to the low uranium price. Paladin has cleaned up its weak balance sheet and was able to raise A$200M in an equity financing in 2022 although it estimated it only needed about A$116M in capex to get the mine up and running again. As we are now getting closer to the reopening of the Langer Heinrich mine, this could be a good moment to update my view on the company.

{kind=link}

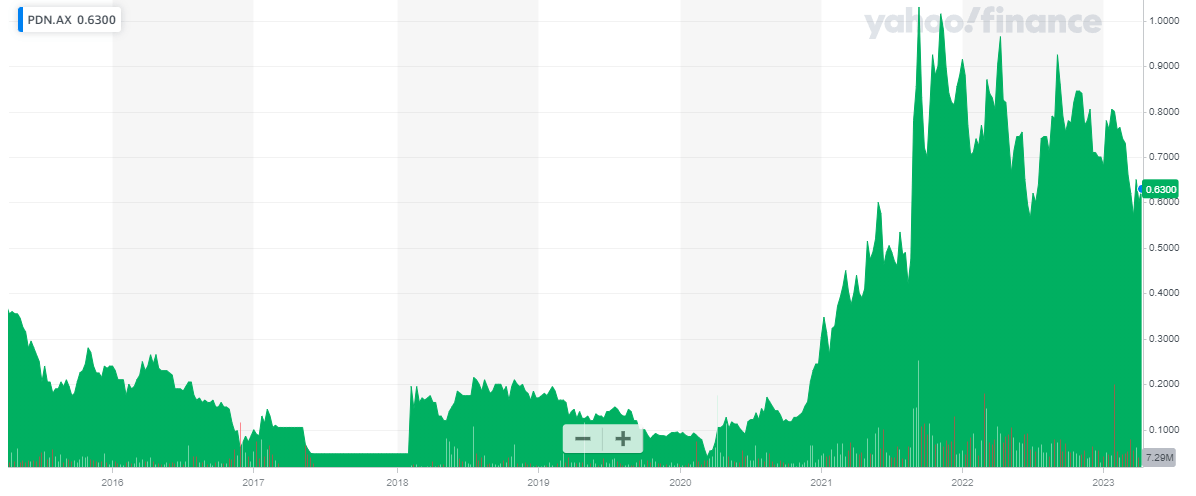

Paladin Energy has its primary listing in Australia where it is listed with PDN as ticker symbol on the ASX. As of the end of December, Paladin Energy had 2.98 billion shares outstanding, resulting in a current market capitalization of A$1.88B. Using the current exchange rate, that’s approximately US$1.25B. As of the end of December, Paladin had US$163M in cash and just $84M in long-term debt on the subsidiary level ( obtained from CNNC , its 25% partner in the project and major offtake partner at Langer Heinrich): Paladin is debt-free on the Paladin level.

Counting down to the Langer Heinrich restart

The plan to restart the Langer Heinrich mine was designed in 2020. The initial capex to restart the mine was initially estimated at US$81M but due to the impact of inflation in the mining sector, this has now been revised to US$118M . In hindsight, the company definitely made the right decision by raising A$200M back in 2022 as it provides additional flexibility when it comes to raising a potential (working capital) funding shortfall. The current cash position of US$163M should be sufficient to complete all activities and cover the working capital needs during the ramp-up phase so based on the current situation, Paladin is fully funded.

A wise decision, and the construction activities are in full swing. As per the latest update in Q1, there are about 500 employees and contractors on site and the site work activities have commenced.

{kind=link}

An interesting element in the reopening process is that while Paladin Energy has increased the capex estimate by more than 40%, the anticipated production cost has remained virtually unchanged at approximately US$27.4 per pound of uranium. That’s an increase of just around 2% compared to the 2020 study and an increase of more than 50% compared to the C1 cost before the mine was placed on care and maintenance.

Of course there’s more than meets the eye here and the breakdown below shows the anticipated transportation cost and sustaining capex are estimated at $4.20 per pound of produced uranium. This would indicate the all-in sustaining cost per produced pound is just below $32.

Paladin Energy Investor Relations

Keep in mind there is a 3.25% royalty and export levy that will be withheld based on the effectively realized uranium price. So if the uranium price is $50/pound, Paladin will receive $48.40 per pound. And using the anticipated all-in sustaining cost of US$32/pound, the net margin will be approximately $16.50 on a pre-tax basis.

I don’t anticipated Paladin to become a tax payer in the first few years after restarting the mine as the company had access to hundreds of millions in tax losses while it will also be able to depreciate about $350M in investments over the remaining mine life. This will provide a very welcome boost to the economics considering the standard corporate tax rate in Namibia is 37.5%.

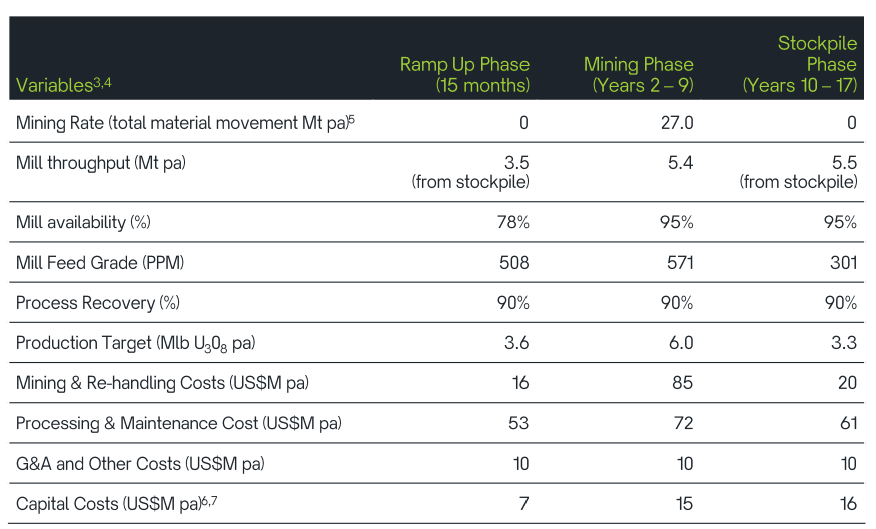

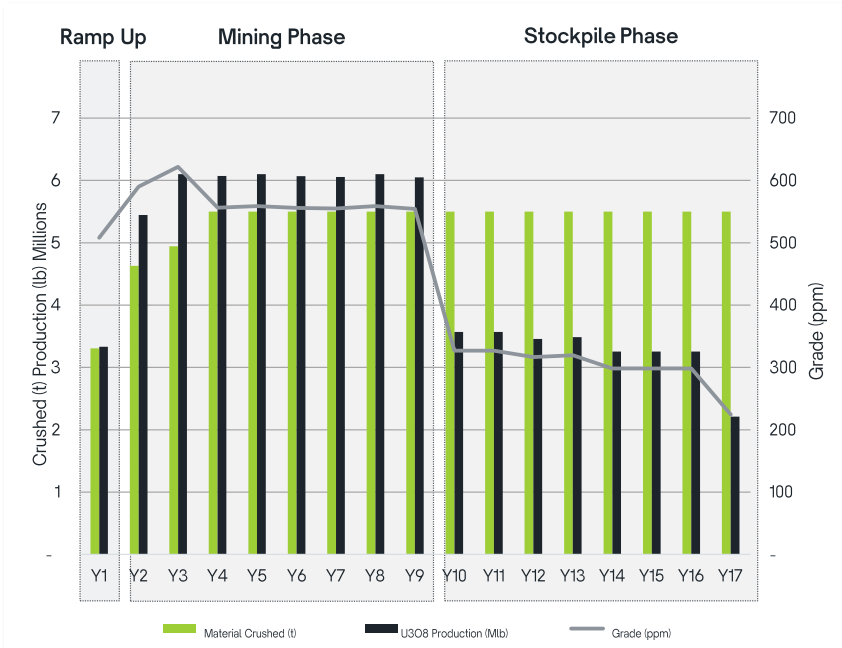

The new mine plan calls for a 15 month ramp up period wherein about 4.5 million pounds of uranium will be produced. The actual full production will happen in years 2-0 where the mine should achieve a steady state production rate of approximately 6 million pounds of uranium per year followed by an additional 8 years of processing low-grade material that will be mined during the first decade but will be stockpiled due to the lower grade nature of the ore.

{kind=link}

This also provides us with a better look under the hood to see the actual economics during the ‘mining phase’. We see the mining and processing costs will be $157M per year while an additional $25M per year is earmarked for G&A and sustaining capex. This means the total all-in operating costs will be just $182M per year or just over $30 per pound of uranium. That’s lower than the life-of-mine average as the AISC will increase when the stockpile phase starts.

This is where it gets interesting.

Using the aforementioned uranium price of $50/pound, the net margin in the mining phase will be approximately $18 per pound. That’s US$108M per year in net cash flow on a pre-tax basis and as mentioned before, Paladin’s operating subsidiary has hundreds of millions of tax losses and I don’t anticipate the company to be paying any meaningful taxes before the end of this decade. Paladin has a 75% stake in the project which means its attributable cash flow on the operating level is approximately US$80M per year.

{kind=link}

While this means the company is currently already trading at its undiscounted cumulative net cash flow, Paladin still offers an interesting call option on the uranium price. As per the mine plan, its attributable net uranium production is approximately 50-55 million pounds of uranium over the entire 17 year mine life. For every $10 increase in the uranium price, Paladin will generate approximately US$500M in additional pre-tax net cash flow. Even if you would apply a 37.5% tax rate on that, every $10 increase in the price of uranium would boost the after-tax value per share by approximately A$0.15.

Investment thesis

So while Paladin does not appear to be very cheap based on the Langer Heinrich economics at the current uranium price, it does have several other elements working in its favor. First of all, it is a past-producing mine so there should be no major issues during the ramp-up phase. Secondly, Paladin has some other uranium projects in its portfolio. Those projects are in the resource stage but aren’t close to being brought to production. Nonetheless, these projects do have value.

The near-term restart of the Langer Heinrich uranium mine makes Paladin Energy valid call option on the uranium price. The company appears very fairly valued based on the current spot price of uranium but provides decent leverage in case you expect a substantial increase in the uranium price in the next decade.

For further details see:

Paladin Energy: Gearing Up For Langer Heinrich Restart In 2024