AYX - Palantir's Business Model That Failed

- In this article, I take a critical look at Palantir Technologies' Q2 2022 results released today.

- Palantir's business model, in my opinion, will not allow the company to quickly break free from SBC dependence.

- I review the sell-side analysts' assessment of how Palantir compares to the other application software stocks on the SBC site.

- Despite the strong negative market reaction after the report, Palantir's share price is still too high, in my view.

- I reaffirm my Sell rating and do not recommend buying PLTR on the dip.

Introduction & Thesis

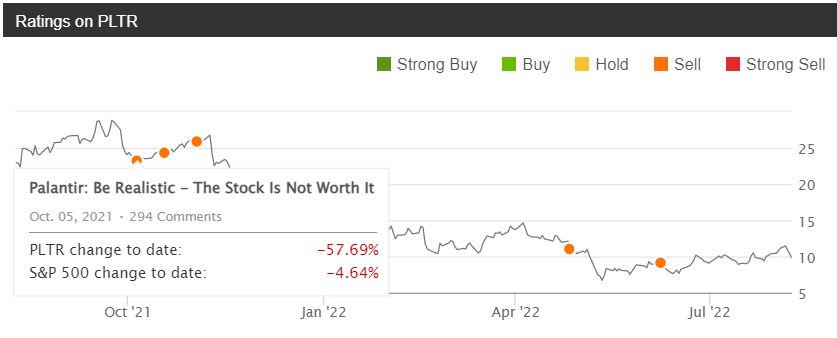

I have been covering shares of Palantir Technologies Inc. ( PLTR ) on Seeking Alpha since early October 2021 and have been increasingly pessimistic about the company's prospects ever since.

{kind=link}

The company's problems, which I wrote about back then, are still making themselves felt - we can see this in the example of the quarterly report for Q2 2022 , which was published today before the stock market opened.

Despite all the bullish optimism surrounding this company, I feel it is my duty to periodically remind all investors looking to buy PLTR on drawdowns of the risks of such an approach in this particular case - Palantir stock seems to me to be quite overvalued given its current growth rates and stock-based compensation ("SBC"), which is down but still one of the highest (relative to revenue) among other application software companies.

What's wrong with Palantir's Q2 2022 results?

Anyone looking at yesterday's market reaction to the company's quarterly report will wonder - what is wrong with them? Why is everyone selling so hard?

Revenue of $473 million beat consensus estimates of 9 Wall Street analysts by $1.29 million, which is not a great result (+26% y/y for a fast-growing company with high valuation multiples). Earnings per share, which I think is more important, were on par with Q4 2019 (-$0.1), $0.4 lower analyst expectations.

{kind=link}

It can be seen that management has begun to think about finally freeing the company from the SBC dependency I have written about many times before - this is reflected in the extensive reduction of this type of expenditure in the structure of operating expenses ((OPEX)) and cost of sales ((COGS)):

{kind=link}

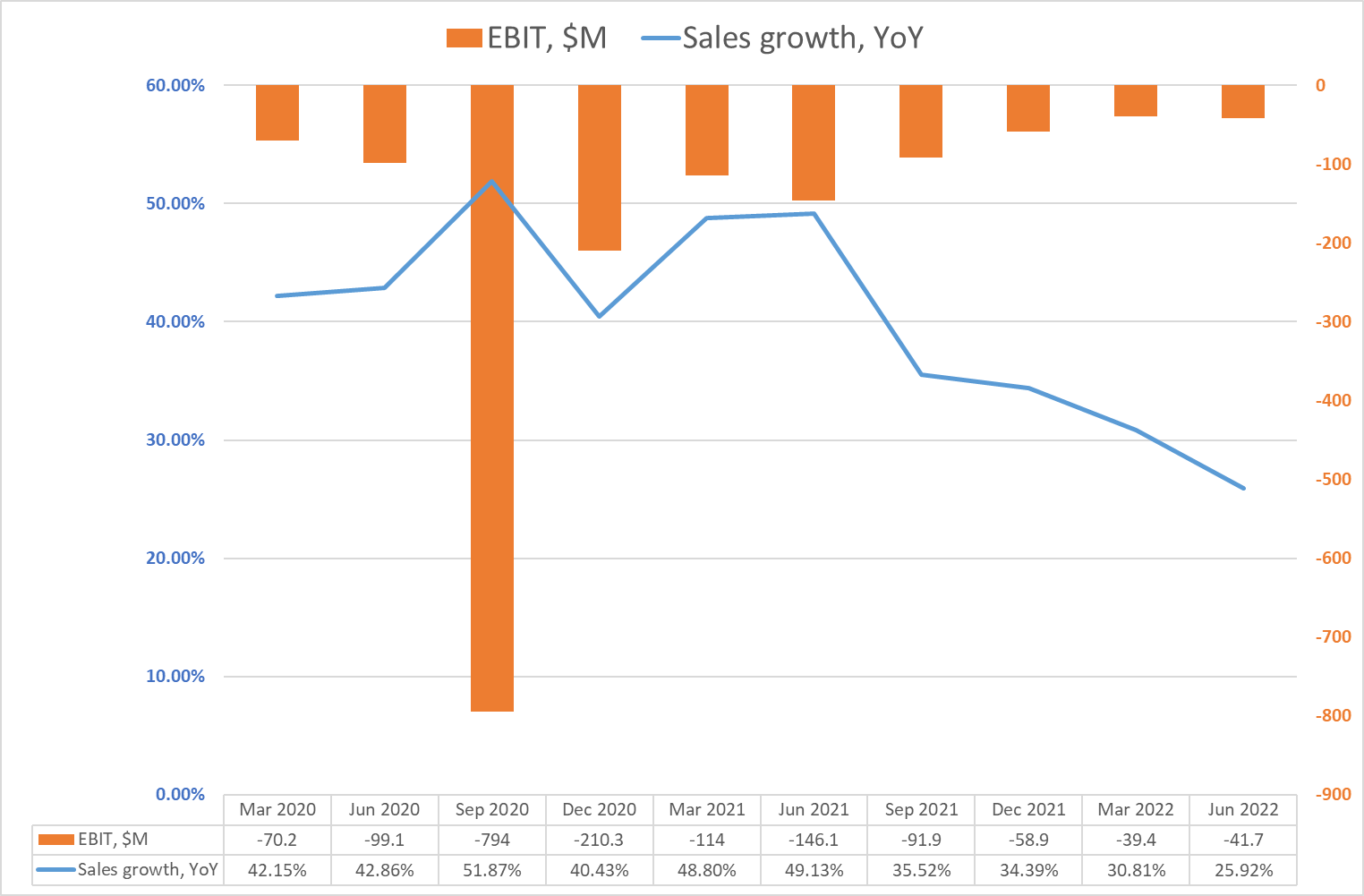

One would think that such a large reduction in costs should have led to a significant improvement in the bottom-line figures. What happened, however, was what I had warned about earlier - the attempt to eliminate the stock option program will inevitably lead to a decline in top-line growth. As we see in practice, everything that goes below revenue does not change it in any qualitative way for the company.

{kind=link}

A moment from yesterday's press conference (beginning of Alex Karp's speech) where I choked while drinking my coffee:

In the last 3 years, we have grown Palantir from a 743 revenue business with hundreds of millions of dollars in actual loss to, in the last 12 months, a $1.74 billion business with $300 million in free cash flow, which represents a 41% CAGR. 41% CAGR on a business that is now in its 18th year is very unusual. There are many reasons for this strong growth, but you live by the same sword that you pay the price for. And we deal with very, very large contracts. And the USG has some of the large -- our largest contracts, and they have been pushed out. But because of uncertainty towards the end of the year, we're revisioning guidance down to $1.9 billion.

I personally remain very optimistic that the next 3 years will look a lot like the last 3 years, again, where we took a money-losing business and made a business that throws off free cash flow, where we ended up as of today with $2.4 billion in the bank and no debt, and that the large and chunky nature of our contracts will continue to be in large part an advantage because these contracts do not disappear.

Source: PLTR's earnings call [Aug. 08, 2022]

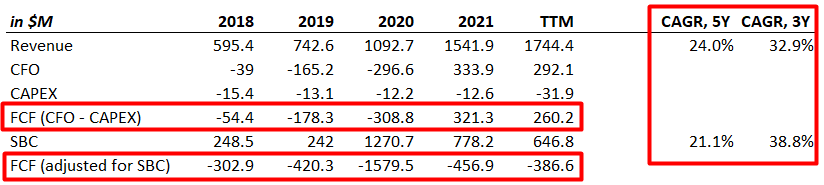

First, what is $300 million FCF? Actually, in the last 12 months ((TTM)) Palantir was able to generate $292 million in cash flow from operations and spend $31.9 million on CAPEX [Seeking Alpha data], i.e. according to the classical free cash flow formula, PLTR's FCF is not $300 million, but $260.2 million (13.27% less). In my opinion, this was too rough a rounding on the part of the CEO.

Second, what 41% CAGR is Alex Karp talking about? If we take the TTM figures and calculate the CAGR values over the last 3 years [as Mr. Karp says], it turns out that the only thing that has grown the closest to 41% is SBC in the cash flow statement structure:

{kind=link}

The company is still burning huge amounts of money "in deferral mode," shifting responsibility for funding operations to current shareholders, and then boasting that there is no debt on the balance sheet. In my opinion, it should work differently - for 18 years, the company had to find a way to fund itself through its operations, not through SBC adjustments, the divestment of which is now being managed by slowing sales growth.

How does this all compare with other companies in the sector?

I read very often from bulls that Palantir's desire to reward its engineers with shares is normal. Besides, the company is far from being the "worst" in this respect compared to some other representatives of the IT sector.

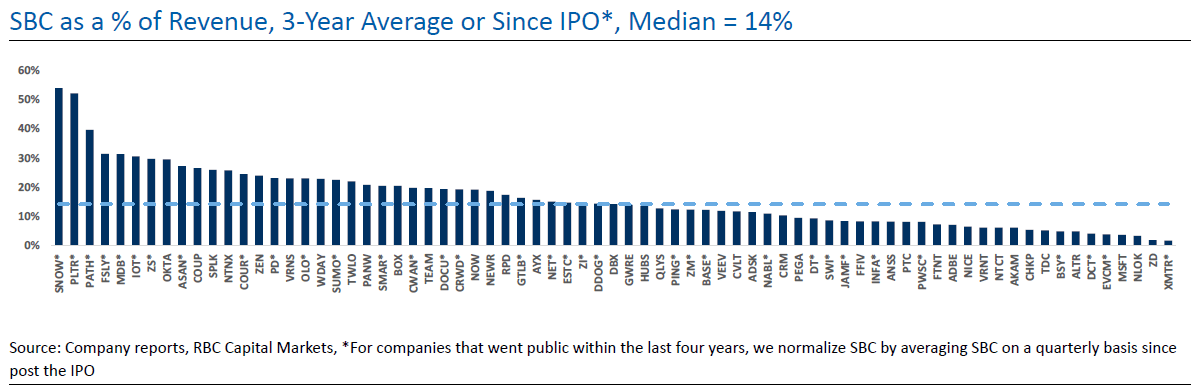

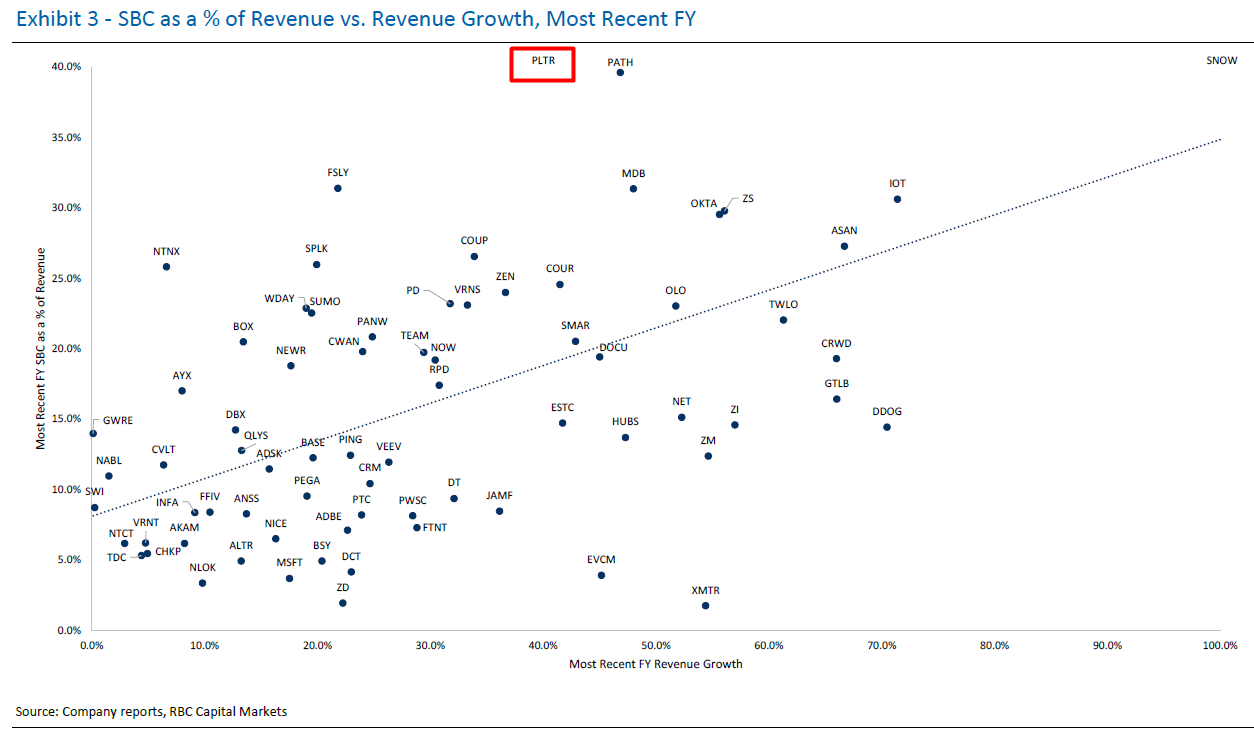

To verify this, it was necessary to collect data from all application software industry representatives and conduct a cross-sectional analysis of their financial data, which seemed too time-consuming. So I was very pleased to receive the recent RBC Capital Markets report [dated August 1, 2022] in which Rishi Jaluria , Matthew Hedberg , Dan Bergstrom , and other analysts of the bank conducted such an analysis of this industry (73 companies) and compared the SBC approaches of various companies. Here are their general conclusions from the report:

Based on our analysis, we would highlight ( BSY ), ( CHKP ), ( DT ), ( FTNT ), ( HUBS ), ( MSFT ), ( NLOK ), ( VEEV ) as showcasing the most reasonable approaches to SBC, while we would point to ( BOX ), ( COUP ), ( DOCU ), ( FSLY ), ( NTNX ), ( PATH ), ( PD ), PLTR , ( SPLK ), ( VRNS ) as having the most room for improvement.

Yes, PLTR is far from the only company in the sample that the analysts scolded. But that is not a justification, in my opinion. The company turned out to be one of the most SBC-dependent companies in the entire sample analyzed:

{kind=link}

Despite 12.83% dilution over the past 7 quarters, PLTR management has repeatedly cautioned investors against looking at SBC's role in share dilution, noting that fully diluted shares have generally been flat or even declining on an annual basis and that SBC will begin to normalize over the next 1-2 years. Most likely, SBC will indeed continue to decline quarter-on-quarter, especially considering RSU grants (muted in recent quarters), but this decline has been very slow lately, which confirms my thesis that the company is unable to break even without pain on GAAP metrics.

Author's calculations, based on Seeking Alpha

Bulls also like to talk about Palantir growing fast enough to compensate current investors for these SBC costs and dilution. Well, if you are a bull too, the following chart should upset you a bit:

{kind=link}

Given the TTM data, PLTR's point on the chart should be southwest due to more modest growth and a decline in the SBC sales ratio, but even then Palantir does not look like the fastest growing or most shareholder-friendly company compared to others.

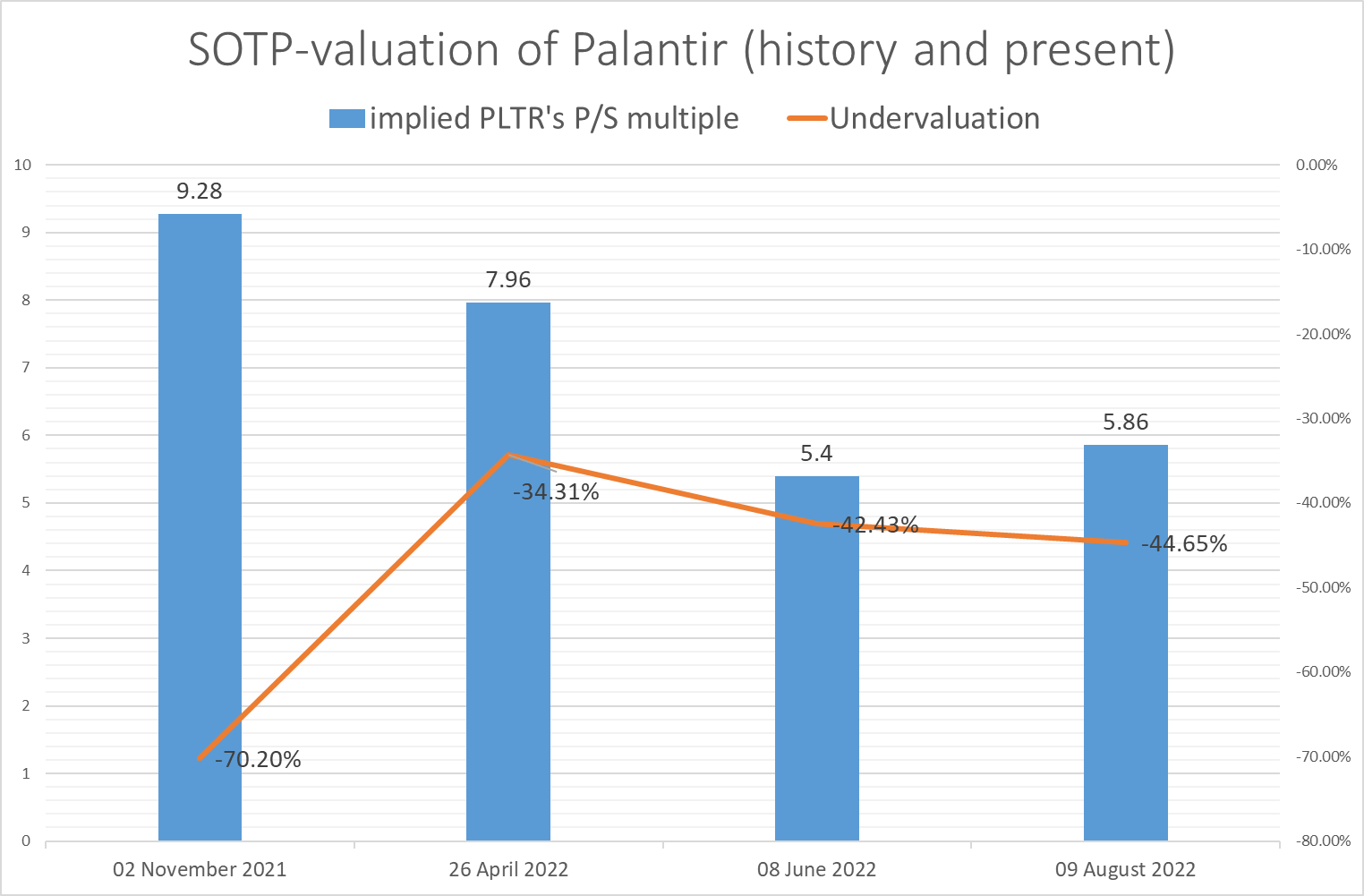

If we try to translate these growth rates and compare them to the price-to-sales multiples to do a sum-of-the-parts valuation analysis, as I have done in 3 of my previous articles, we will see that PLTR is still highly overvalued despite the sharp price decline yesterday.

| Government = |

| 55.60% |

| Company name |

| P/S ((FWD)) |

| Sales growth, last quarter, YoY |

| Booz Allen Hamilton ( BAH ) |

| 1.39 |

| 6.28% |

| Science Applications International Corp. ( SAIC ) |

| 0.7 |

| 6.28% |

| Leidos Holdings ( LDOS ) |

| 0.96 |

| 4.32% |

| Average |

| 1.017 |

| 5.63% |

| Commercial = |

| 44.40% |

| Company name |

| P/S ((FWD)) |

| Sales growth, last quarter, YoY |

| Tyler Technologies ( TYL ) |

| 9.34 |

| 15.99% |

| Verint Systems Inc. ( VRNT ) |

| 3.42 |

| 8.46% |

| Splunk Inc. |

| 5.44 |

| 34.27% |

| Cognizant Technology Solutions Corp. ( CTSH ) |

| 1.8 |

| 7.00% |

| Alteryx ( AYX ) |

| 5.52 |

| 50.43% |

| Average |

| 5.104 |

| 23.23% |

| Gov's P/S per 1% sales growth |

| 18.07 |

| Com's P/S per 1% sales growth |

| 21.97 |

| Palantir's Gov growth, 2Q, YoY |

| 13% |

| Palantir's Com growth, 2Q, YoY |

| 46% |

| implied PLTR's FWD P/S |

| 5.86 |

| vs. current P/S ((FWD)) |

| -44.65% |

Source: Author's calculations based on Seeking Alpha

So Palantir's overvaluation remained almost unchanged despite the decline in the share price:

{kind=link}

Bottom Line

I am aware that my thesis carries certain risks that you need to consider before shorting PLTR stock (which I do not recommend due to the excessive love of retail investors for this stock).

The first point on which I can be wrong is the share dilution. This is the cornerstone of my entire thesis. If the company can operate more efficiently in the commercial space than I think it can, then its growth should dwarf dilution and lead to the creation of shareholder value.

The second moment is the rally in tech stocks, which have fallen sharply since November 2021 due to widespread multiple contraction. Now we are seeing a rebound in most of its names. Both the S&P 500 Index and the NASDAQ Composite Index have moved out of bearish territory in the last month, although the risk of recession remains high.

If the risk of a recession was priced in, but it does not occur (as Mr. Powell assures us), then the logic of things should be that companies with a long duration (like PLTR) will be revalued, leading to an increase in their shares.

Despite these risks and some convincing arguments from bulls, I cannot bring myself to change my rating from Sell to Neutral.

In my opinion, the reason why Palantir still cannot become truly profitable without all possible adjustments is due to the specifics of its business model. Originally, PLTR was created to serve government purposes - to this day, this is the company's largest business segment. In terms of the quality of the systems sold and their customization, Palantir did - and still does - an excellent job as promised. However, maintaining the implemented systems requires a great deal of technical effort, and thus the involvement of expensive specialists who are not as plentiful in the marketplace (with today's critically low unemployment in the United States, this problem is even more acute in the IT area). The company sells its software to the commercial market as part of its existing business model, so the claim that PLTR is not an IT consulting firm is only partially true (otherwise SBC would not take in more than 1/3 of its revenue).

Any company facing a really important operational problem that requires setting up ETL processes is likely to bring in data consultants from BCG-Gamma or McKinsey & Co. who know the business through interaction with the ordinary consulting department. Palantir does not have that advantage - it only has engineers who can set up ETL processes and install software to process incoming data, probably at the price of Big 3 firms that do the same thing but know the client's needs intimately. That's why this article is titled the way you see it - I honestly do not understand PLTR's moat and how this company can meet its $4.5 billion revenue growth target without additional debt or subsequent share dilution. And even if that target is met, how much of those billions will end up as net income?

Against this backdrop, I reiterate my Sell and do not recommend buying PLTR after yesterday's share price decline.

Final note: Hey, on September 27, we'll be launching a marketplace service at Seeking Alpha called Beyond the Wall Investing , where we will be tracking and analyzing the latest bank reports to identify hidden opportunities early! All early subscribers will receive a special lifetime legacy price offer. So follow and stay tuned!

For further details see:

Palantir's Business Model That Failed