PALL - PALL: Blessing Turn Into A Curse

2023-11-11 04:43:33 ET

Summary

- Palladium has been the worst-performing precious metal in the past few years due to declining demand in automotive applications. Auto accounts for 80-85% of palladium demand.

- Palladium is usually produced as a byproduct of mining other metals like silver and copper. Supply is price-inelastic. This was a blessing when demand exceeded supply, leading to squeezes.

- However, in the coming years as palladium for catalytic converters is phased out, the blessing will turn into a curse as supply of palladium will not decrease with lower prices.

A few months ago, I penned a bearish article on the abrdn Physical Palladium Shares ETF ( PALL ), as I felt demand for palladium in automotive applications is entering a terminal decline phase. Since my article, the PALL ETF has declined by 18%, as the market appears to agree with my assessment (Figure 1).

Figure 1 - PALL has declined by 18% (Seeking Alpha)

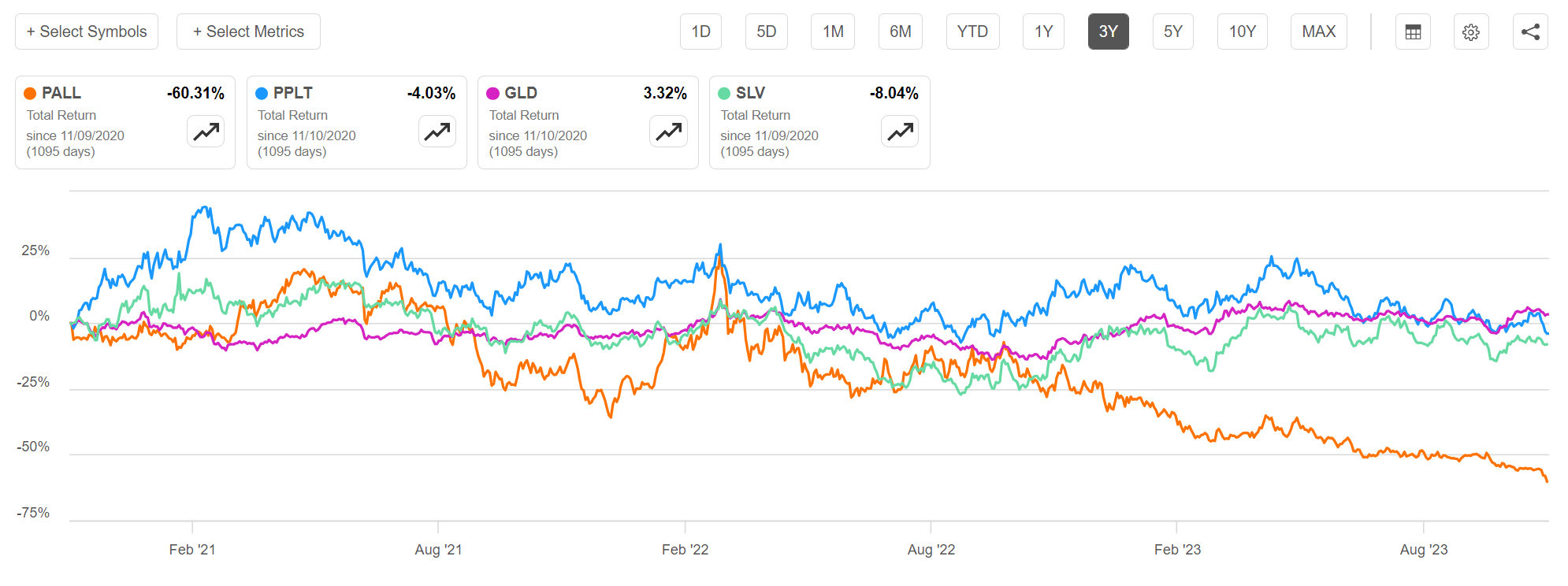

In fact, palladium has been the worst performing precious metal in the past few years as speculators exit the metal most commonly associated with gasoline catalytic converters (Figure 2).

Figure 2 - PALL has massively underperformed other precious metals (Seeking Alpha)

{kind=link}

With the share price of PALL declining by more than 40% year-to-date, is there a possibility of a mean reversion trade?

Brief Fund Overview

The abrdn Physical Palladium Shares ETF is a simple to understand fund; the PALL ETF issues shares to investors and uses the proceeds to buy physical palladium bars that are held in vaults in Zurich and London. The PALL ETF is relatively small, with only $177 million in assets and charges a 0.6% expense ratio.

As I wrote in my prior article, the end-use of palladium is mostly automotive applications (i.e. catalytic converters), as that makes up 80-85% of demand (Figure 3).

Figure 3 - Automotive applications make up 80-85% of end-use (Sprott Asset Management)

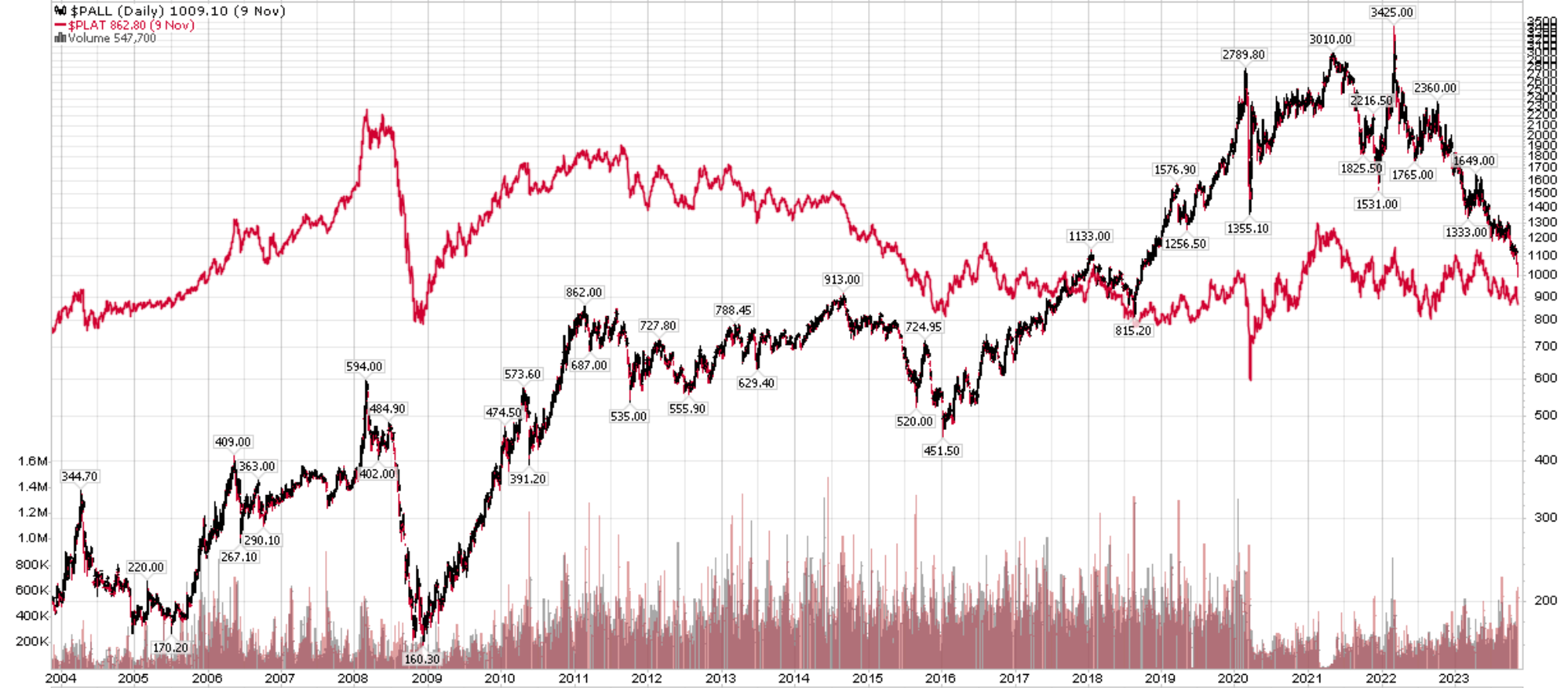

Palladium enjoyed a tremendous boom in the 2010s due to tightening emission standards and technological advances that allowed palladium to be substituted for platinum at a 1:1 ratio. Combined with the physical rarity of palladium (palladium is 15 times rarer in nature compared to platinum), this allowed palladium prices to skyrocket, outperforming that of Platinum (Figure 4).

Figure 4 - Palladium prices outperformed platinum in the 2010s (Author created with price chart from stockcharts.com)

{kind=link}

Limited Mine Supply Is A Blessing And A Curse

One major reason palladium enjoyed such a large boom in the 2010s was because palladium is a very small market, with Russia and South Africa controlling 46% and 39% of global reserves respectively (Figure 5).

Figure 5 - Palladium is a small market (Sprott Asset Management)

Furthermore, palladium is typically produced as a byproduct from mining other metals like silver and copper. So even when prices surged in the 2010s, there was little supply-side response, as miners were not going to expand copper mines to produce more palladium (Figure 6).

Figure 6 - Palladium supply is price-inelastic (Sprott Asset Management)

This byproduct dynamic was a blessing when demand exceeded supply, as there are few dedicated palladium deposits and mines, so prices squeezed higher as emission standards tightened, requiring more palladium content per vehicle.

For context, each catalytic convert contains 2-7 grams of palladium, or a few hundred dollars worth. Compared to the total cost of a passenger vehicle, the value of contained palladium is only a rounding error and hence demand from the automotive industry was relatively price inelastic.

However, the same byproduct dynamic can turn into a curse when demand is less than supply, as we have seen in recent years as electric vehicles replace internal combustion engines on the road. Miners focused on producing copper and silver as their primary output simply do not care enough about palladium byproduct credits to slow down production when there is excess supply of palladium.

EVs Increasingly Gaining Market Share; Will Surpass ICE In Late 2020s

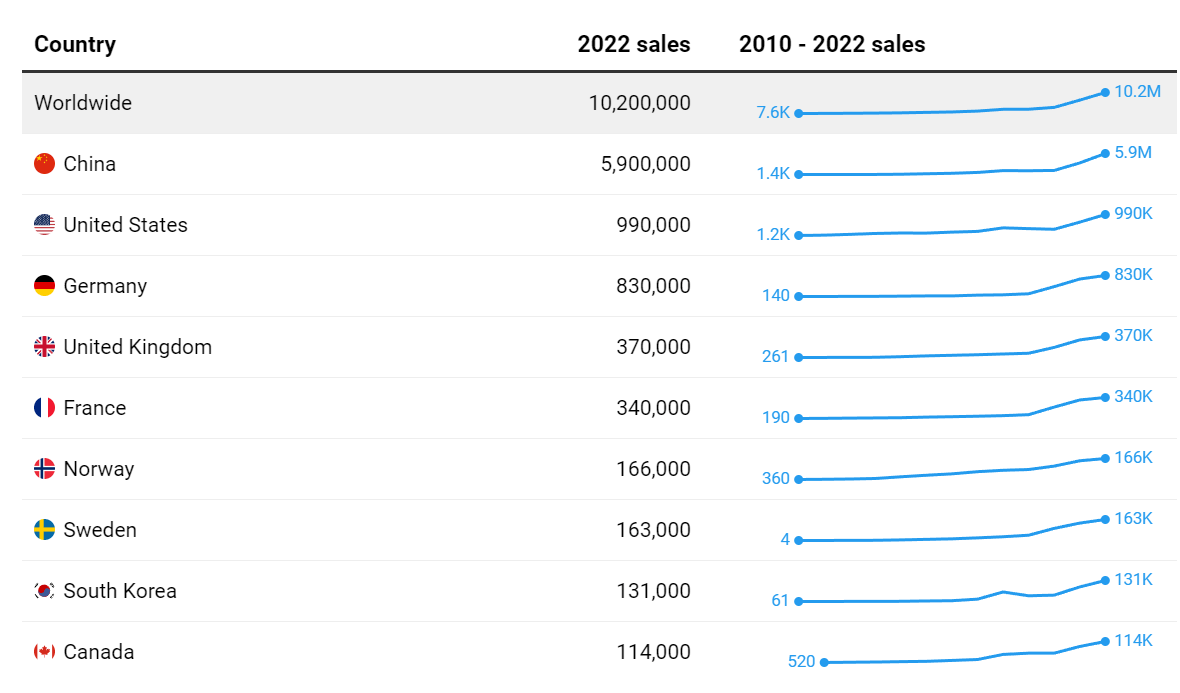

My bearish thesis on palladium is very simple to understand. Globally, about 70 million passenger vehicles are sold every year. Electric vehicles have gone from nil to over 10 million units in 2022, taking approximately 14% market share (Figure 7).

Figure 7 - EVs accounted for over 10 million vehicle sales in 2022 (aljazeera.com)

{kind=link}

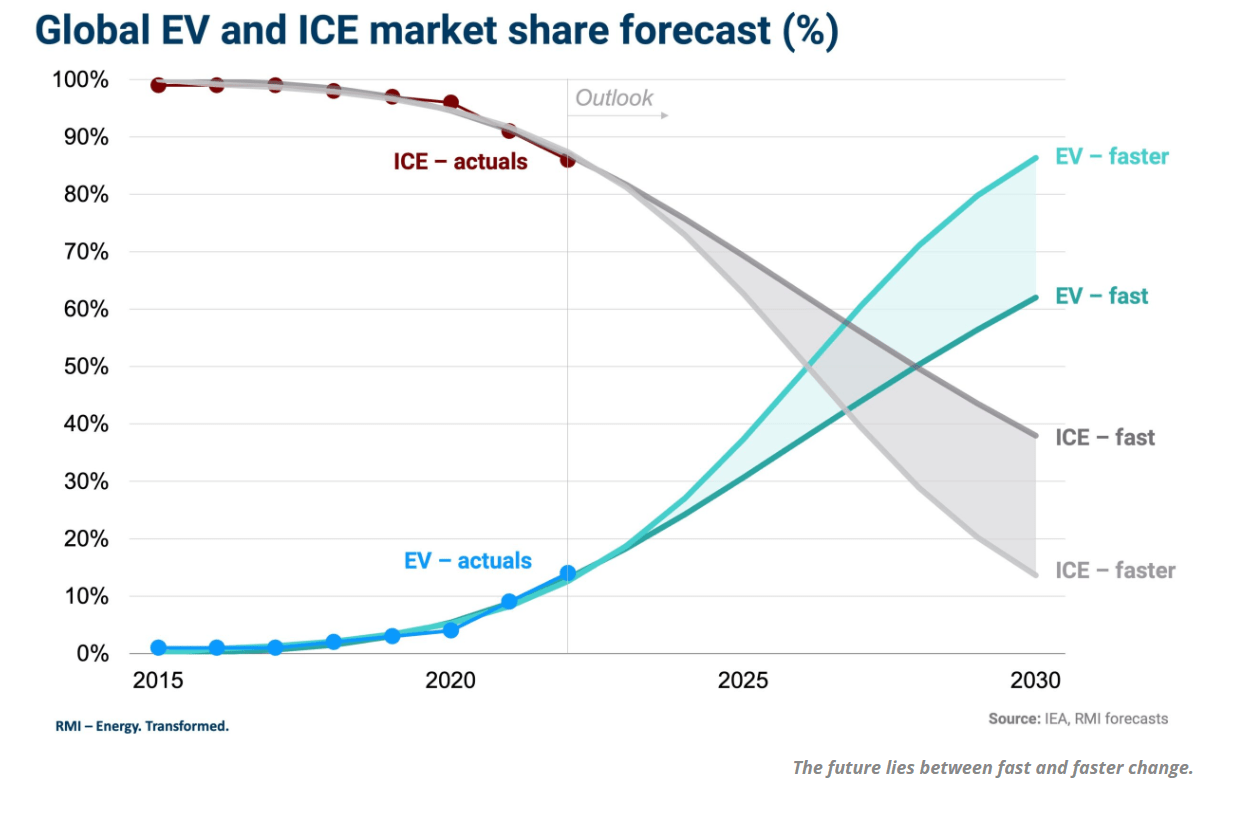

So far in 2023, EV sales are on pace to grow 40% YoY and many analysts expect EV sales to surpass ICE powered vehicles in the next few years (Figure 8).

Figure 8 - EVs is expected to exceed ICE vehicles in late 2020s (cleantechnica.com)

{kind=link}

With collapsing demand for palladium in catalytic converters, it is no surprise that the price of palladium and PALL have been in freefall.

UAW Strike May Have Been The Cause Of Latest Plunge

In the short term, the recent 7 week strike by the United Auto Workers ("UAW") union may have exacerbated weak market dynamics and caused the price of palladium to plunge. According to some industry estimates , the strike impacted vehicle production by ~43,000 per week, so the lengthy 7-week strike could have stopped production of ~250,000-300,000 vehicles in total between the 3 detroit automakers.

With the strike now resolved, we should see production lines restart and demand for inputs like palladium normalize. So I would not be surprised if the price of palladium finds some near-term stability.

However, the long-term decline in palladium demand is inevitable, so I would urge holders of the PALL ETF to use any rallies to exit.

Conclusion

The abrdn Physical Palladium Shares ETF provides pure exposure to the price of palladium. Due to the exponential growth of EVs, my outlook for palladium is negative.

In the short-term, the recent UAW strike could have negatively impacted gasoline vehicle production, so I would not be surprised if palladium prices stabilize as striking workers return to work. However, looking long-term, EVs are set to overtake internal combustion engines in the next few years, leading to significantly lower demand for palladium in catalytic converters.

Since palladium is typically a byproduct of other metals' production, lower prices will not prompt any supply response from the miners. What was a blessing when prices were rising due to demand exceeding supply will turn into a curse for palladium investors in the coming years as supply exceeds demand.

I maintain my sell rating on PALL.

For further details see:

PALL: Blessing Turn Into A Curse