PANDY - Pandora: Potential If Sustainable Growth Can Return

2023-05-09 06:15:05 ET

Summary

- Pandora A/S designs, manufactures, and markets contemporary jewelry globally.

- Revenue has grown at a CAGR of 12% in the last decade, although the last 5 years have been poor due to greater competition.

- Margins are fantastic but are declining as Pandora is investing in reinvigorating growth.

- Pandora's valuation looks attractive but we are concerned with the current performance and the lack of catalysts.

Investment thesis

Our current investment thesis is:

- Pandora is a great business with unavoidable problems.

- The good characteristics are that it is a market-leading business with great margins.

- The bad is that the business is facing greater competition and poor results.

- The factor swaying our rating is the lack of a positive catalyst.

Company description

Pandora A/S ( OTCPK:PNDZF ) designs, manufactures, and markets contemporary jewelry globally. The company offers earrings, bracelets, rings, and necklaces, among other products.

{kind=link}

Pandora

Share price

Pandora's share price has experienced big gains and big losses, with the net position being 200%+ up in the decade. This is a reflection of both improving performance and periods of revenue decline.

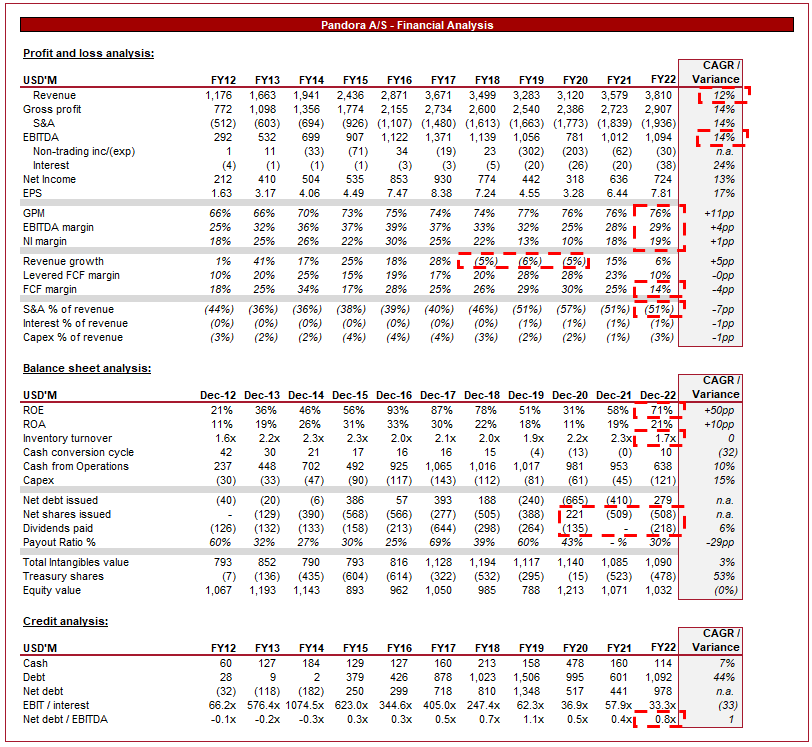

Financial analysis

{kind=link}

Pandora financial performance (Tikr Terminal)

Presented above is Pandora's financial performance for the last decade.

Revenue

Pandora has grown revenue at a CAGR of 12% across the last decade, although this hides 3 consecutive years of negative growth leading to the pandemic.

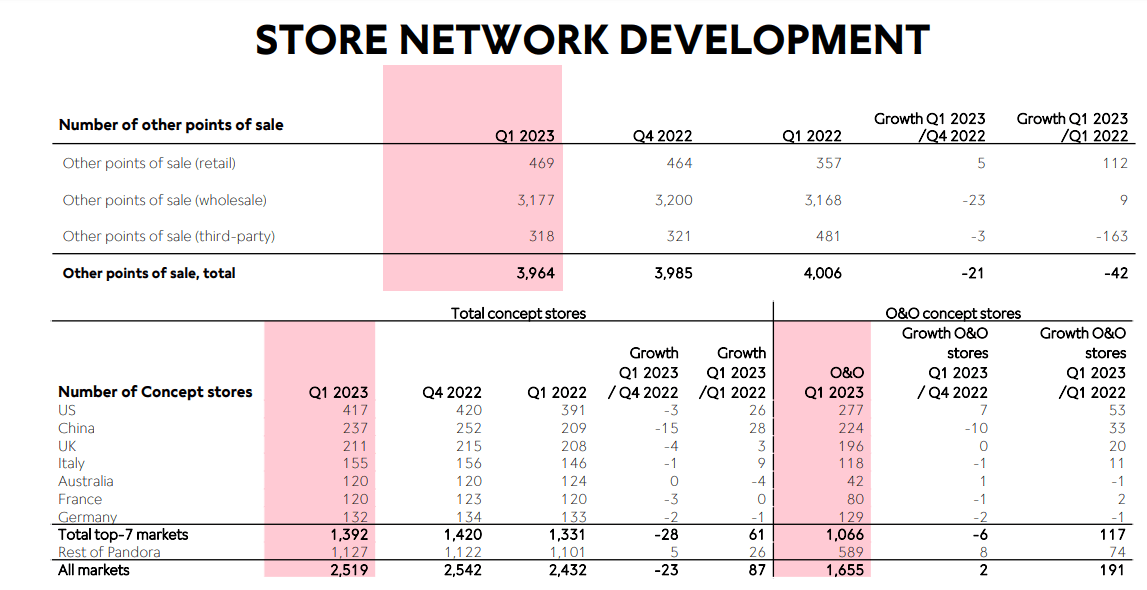

Pandora currently generates the majority of its revenue from 7 key markets, which in total represent 68% of Q1-23 revenue.

Revenue by location (Pandora)

The business is heavily weighted toward a retail footprint, with several thousand locations worldwide.

{kind=link}

Store network (Pandora)

As with other retail industries, the jewelry segment is undergoing a digital transformation, with many companies investing in e-commerce. Many of these e-commerce companies are dropshipping cheap goods shipped from locations such as China, significantly undercutting Pandora. Pandora has seen its competitive position diminish as a result of e-commerce retailers, forcing a response. The issue is that it is difficult for Pandora to compete on parity, as it still has fixed location costs and so is less price competitive. Pandora is investing heavily in digital as a means of driving online sales while reducing its store count. Our view is that Pandora has a global brand that will continue to help it maintain market share, but its ability to grow unrestricted has now stopped. The business must innovate to outperform.

Further, Pandora is also facing competition from the luxury end of the spectrum, as the economics of jewelry retailing (high margins, targeted at women who are the biggest retail spenders) encourages new entrants. Affordable luxury brands like Swarovski and Alex and Ani are gaining market share in the jewelry industry, putting pressure on Pandora to respond. Swarovski is very similar in strategy also, with a large number of physical locations, allowing the business to directly compete for footfall.

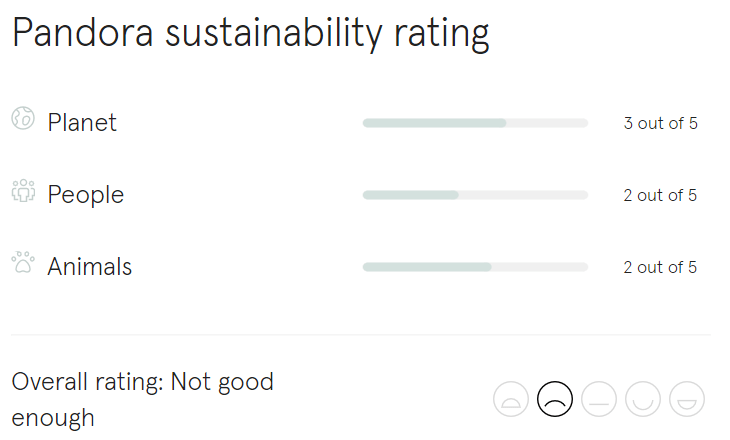

The jewelry industry is facing significant pressure to improve the sourcing of its materials. This was primarily in relation to diamonds, but this has now extended to sustainable production methods. Pandora is committed to becoming carbon neutral by 2025 and has also launched a new recycled silver and gold jewelry collection. The company considers itself a top performer in sustainability but according to Goodonyou, the business is not doing well enough. This is likely a reflection of its pricing, as Pandora targets the affordable segment, which means costs need to be minimized.

{kind=link}

sustainability score (Goodonyou)

An opportunity here is Pandora's expansion into lab diamonds, which provides consumers with identical diamonds (if not superior) to discovered diamonds, at a fraction of the price. This extends the company's reach beyond small gifts and creates the long-term opportunity to move into a higher price bracket with further products. The key here is for the company to improve its sustainability score and develop the expertise to produce higher-quality products.

Economic considerations

We are currently experiencing heightened inflation and elevated rates. This is contributing to a slowdown in discretionary spending as consumers see their cost of living rising.

This is an issue for Pandora as it discourages discretionary spending on products that consumers can forego. With Pandora's products being affordable and targeted at women, our expectation is for the impact to be proportionately less. This is because women are generally less elastic in demand and cheaper products remain affordable.

Looking ahead, our view is that FY23 will continue to be difficult with inflation remaining stubborn.

Margin

The key selling point of Pandora is its fantastic margins. The company boasts an EBITDA-M of 29% and a NIM of 19%.

Margins have declined from their all-time high in FY16 due to the increased competition Pandora now faces. The dilution is a reflection of increased S&A spending, which is now 51% of revenue. GPM has actually reached an all-time high, despite inflation, due to scale economies.

Our view is that further dilution is more likely than improvement, given the current competitive environment. With growth returning, the increased spending/margin dilutions look to be a required expenditure.

Q1 results

Growth (Pandora)

Management's view is that the 1% organic growth & 0% LFL reflects resilience. Although potentially harsh, we believe this is disappointing given the company's leading position in the market. Although consumption is softening, we are not in a recession and many retailers are still growing.

{kind=link}

US Growth (Pandora)

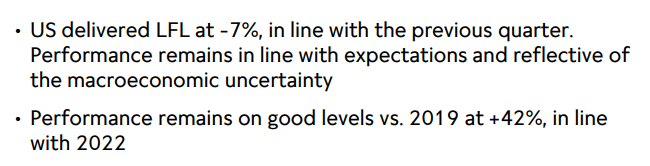

Interestingly, the weakness is from the US relative to Europe, which goes against everything we have seen with other retailers.

With LFL sales down 7%, we are potentially seeing the market normalize following a boom post-Covid.

Europe Growth (Pandora)

The performance in Europe is more in line with what we would expect from the business. Germany and the UK are generating growth while economically are in a weaker position than the US.

{kind=link}

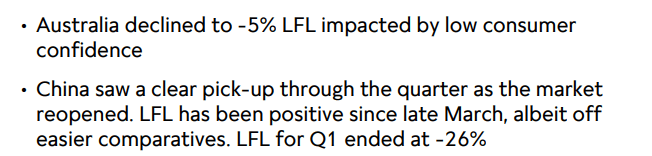

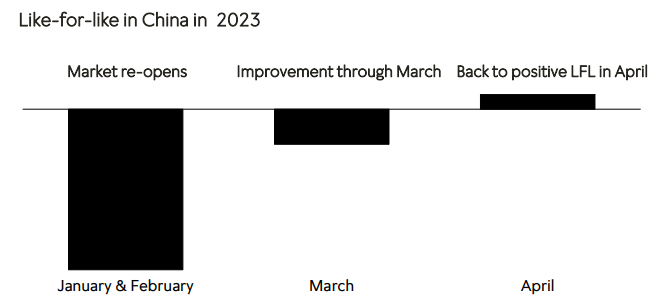

APAC growth (Pandora)

Sales in China were impacted by the country's zero-covid policy, which led to several lockdowns and uncertainty in the country. This was lifted in late 2022 and with an uptick in cases following this, the country is likely returning to normal. This has the potential to drive short-term improvement in performance, as we see a similar uptick in activity that was observed in the West during 2021.

{kind=link}

China post zero covid (Pandora)

Balance sheet

Pandora experienced a slight decline in its inventory turnover in FY22, down from 2.3x to 1.7x, this was likely an indication that demand has begun to slow. On an absolute basis, this level of turnover is poor in our view and means a greater amount of cash needs to be held.

Pandora is conservatively financed, with a ND/EBITDA ratio of 0.8x. This gives the company the ability to conduct M&A if required or fund organic growth.

Historically, distributions to shareholders came in the form of both dividends and buybacks. This looks to continue in the coming years, following the impact of the pandemic. With the company generating c.$1bn in cash from operations, the current level of distributions is unlikely to be sustainable in the near term until more cash is accumulated.

Outlook

{kind=link}

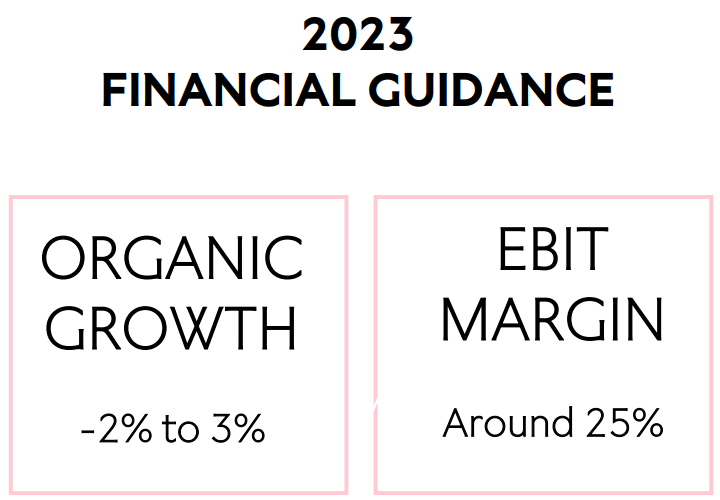

Management guidance (Pandora)

Presented above is Management's guidance for the coming year. Given the decline in Q1, the current revenue forecast looks appropriate. This said, it reflects what will be a poor year for the business if the mid-to-low range is achieved, as we feel the business has the capacity to outperform this.

What is disappointing to see is that margins are expected to slip further (FY22: 26%), although the use of the word "around" leaves this ambiguous.

{kind=link}

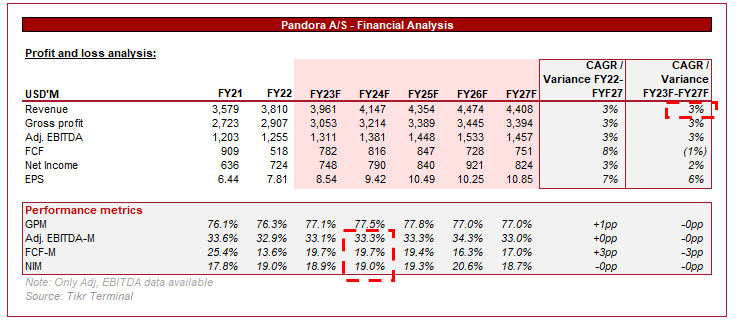

Outlook (TIkr Terminal)

Presented above is Wall Street's outlook on the business.

Revenue growth is expected to be mild at 3%, with a gain of 4% in FY23. The wider forecast looks to be a reasonable expectation, as Pandora has not shown enough evidence in our view that growth is truly back. The FY23 forecast is interesting, however, as it is above what Management is guiding. Analysts potentially believe Pandora is currently underperforming and has scope to outperform this current forecast, which aligns with our view.

Margins are expected to remain flat, which looks reasonable based on our assessment. If Pandora continues to struggle with competition, this could decline further, otherwise flat is reasonable.

Valuation

Valuation (Tikr Terminal)

Pandora is currently trading at an 8x EBITDA and 11x earnings. This represents a discount to its historical average, although it must be noted that the company has experienced several spikes in its multiples due to unexpected poor results.

The question then becomes the degree to which a discount is justified.

Based on our analysis, the key bull arguments are:

- Growth, although small, has returned, which will allow Management breathing room to fix its competitive positioning.

- Margins remain impressive on an absolute basis, which will fund sustainable shareholder returns.

- Improving its sustainability score and investing in lab diamonds could help the business move more upmarket.

The bear arguments are:

- The business is underperforming in FY23 so far, with Management guidance suggesting a poor year.

- E-commerce has allowed businesses to close the gap to Pandora, meaning the coming years will be far less fruitful for the business, potentially leading to higher customer acquisition costs.

- Significant underperformance in the US suggests problems in Pandora's largest market.

Although this paper has been mainly negative, we lean toward the bull argument, that the business is fundamentally good despite several critical problems. The issue is 3 key things in our view:

- The FY23 weakness means we are unlikely to see positive price action, with it potentially turning negative if analysts revise forecasts or Pandora misses.

- There is no clear evidence to suggest the discount is sufficiently unjustified to imply upside, given the struggles the company faces.

- The potential for distribution cuts could also turn investors sour in the near term.

Final thoughts

Overall, assessing Pandora is difficult. Its financial performance is attractive, with high margins and cash conversion. Further, although the business experienced periods of decline, we were never under the impression it was truly in trouble. The concerns, however, are serious. Its competitive positioning is difficult to assess due to the impact of Covid and the current economic conditions. Our view is that the business is certainly weaker and growth will be closer to single digits.

Our hold rating is primarily due to the 3 factors noted above, even though the business looks attractively valued.

For further details see:

Pandora: Potential If Sustainable Growth Can Return