PZZA - Papa John's Is Undercooked

2023-06-07 16:27:07 ET

Summary

- Papa John's shares have fallen 23% in the past four months, and the company's increase in debt may limit future dividend growth.

- The stock is not considered cheap at the moment, and investors can get higher risk-adjusted returns elsewhere.

- Despite improved profitability, the market's assumptions about the company's future growth make it a risky investment.

It's been about four months since I recommended investors avoid Papa John's International Inc. (PZZA), in an article with the very original title "Avoid Papa John's International", and in that time the shares have fallen about 23% against a gain of about 4% for the S&P 500.

I thought I'd check back on the company today because the company has posted financials again, and those deserve comment. Additionally, a stock trading at $71 is, by definition, a less risky investment than that same stock when it's trading at $93.50.

Welcome to the "thesis statement" portion of the article. This is where I give you the gist of my thinking up front. I do this because I know some of you are a busy crowd, and some of you would rather not have to wade through an entire one of my articles, full as they are of bad jokes, bragging, and proper spelling. I won't be buying back in to Papa John's today for a few reasons. I think the increase in debt is going to crowd out the possibility of future dividend increases. Given that I'm of the view that the dividend growth will be sclerotic at best over the next few years, I feel compelled to compare the yield to the risk-free rate, and the comparison isn't good for the stock. Investors who buy this business are getting paid about 285 basis points less than they would with a risk-free government instrument. We investors generally want higher risk adjusted returns, not lower. Additionally, it's not obvious that the stock is cheap at the moment. I may miss out on some gains if the market catches fire at this point, but I'd rather miss out on some upside than risk capital. Additionally, what the market giveth, the market may taketh awayeth.

Financial Snapshot

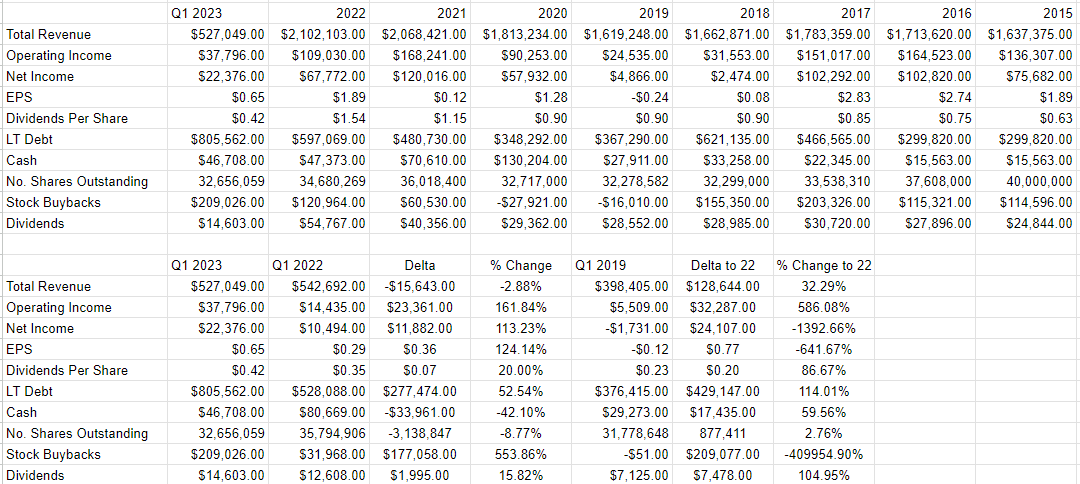

In spite of a 2.9% reduction in revenue, net income during the most recent quarter increased by 113%. I have to admit that when I poured over the latest financials, I was half expecting to see a one-time event to explain this seemingly anomalous behaviour. It turns out that the reason net income during Q1 of this year was about $11.9 million higher than the same time last year is because the company held the line on expenses. In particular, "G&A" expenses were down by about $13.9 million or 21% in 2023 relative to 2022. So, I'm impressed on some level.

Much more troubling to me is the fact that long term debt has spiked by $277 million, or 53% from last year to this, and is up about $208 million over the past three months.

I've plucked the following from page 71 of the latest 10-K for your enjoyment and edification.

Papa John's Debt profile as of December 2022 (Papa John's 2022 10-K)

{kind=link}

Below this table are explanations of the specifics of the senior notes and revolving credit facilities. In order to save you the hassle of going to look it up for yourselves, I'll give you the highlights below. You're welcome. Anyway, the $400 million of senior notes matures on September 15, 2029, so there's little "roll risk" from that component of the long term debt. These carry an interest expense of 3.875%, which I don't consider to be ludicrous.

The revolving credit facility is more troublesome in my estimation. First, it matures three years earlier than the notes. Second, it allows the company to borrow up to a maximum of $600 million, so the recent uptick in debt comes from here. The rate on this debt is a bit more complex, but it is either LIBOR + 1.25%-2%, or the federal funds rate +0.5%. Either way, that would put the rate on this portion of the debt at about 5.6%, which is fairly expensive in my view.

This may explain to some degree why the interest expense is up by about $4.7 million over last year to $9 million. The approximate $36 million annualised interest expense runs the risk of crowding out dividend increases, obviously. For this reason, I'd buy only if the valuation is very compelling at current prices.

Papa John's Financials (Papa John's investor relations)

{kind=link}

The Stock

I consider the stock and the company to be very different things. The company sells pizza to people. The stock, on the other hand, is a traded bit of virtual paper that represents a claim on the future cash flows of the underlying business, and it moves around quite a bit. I think it moves around at too high a rate, given changes in the business, actually. For instance, the shares are down about 23% over the past few months in spite of the fact that the profitability has improved. The stock, in short, is driven by the crowd's views, and the crowd can be capricious. This is because the crowd is driven by thoughts about the future demand for pizza relative to other dining options, the direction of interest rates, the change in input costs, labour rates etc. Additionally, a given stock may be buffeted by the crowd's ever-changing ideas about the attractiveness of "stocks" as an asset class. It's impossible to prove as it's a counterfactual, but it's interesting to contemplate how much lower Papa John's might be if the market hadn't produced a small gain since I last reviewed the business.

In my experience, the only way to trade stocks profitably is to spot the discrepancies between the crowd's assumptions and subsequent results. So, if the crowd is too optimistic it's good to avoid the shares, and vice versa. I really hate to remind you of my success here, but this is how I managed to avoid a 23% loss on this stock. I uncover my views about the crowd's assumptions based on a few tools that range from the simple to the more complex.

Additionally, I like to buy stocks that are cheap because I think they offer the best risk-reward characteristics. They're less risky because they have less far to fall than high flyers. They offer greater rewards because if they post even moderately good news, the stock may spike in price.

When I last reviewed Papa John's, I decided to avoid the shares because the market was paying a price to sales ratio of 1.587 and the dividend yield was 1.29%. Fast forward to the present and we see that shares are about 25% cheaper, on a price to sales basis as you might expect per the following:

Although the shares are cheaper than they were previously, they're still valued on the high side relative to a longer swath of time. Additionally, the dividend yield has spiked by 108 basis points, and is near a multi-year-high. The problem is that the yield is still well below the risk-free rate by about 286 basis points. If there was a chance that the dividend would rise dramatically from current levels, that would be less of a problem. The fact that interest rates crowd out that chance to some degree suggests we would be wise to not expect much in the way of increases from here.

As I wrote above, I want to use relatively simple and more complex tools to work out what the market is "assuming" about a given company's future. Ratios are one of the more simple ways to explore this. I also apply a bit of high school algebra to the task, and employ methods described in books like "Accounting for Value" by Penman, and "Expectations Investing" by Mauboussin and Rappaport. Both of these books introduce the idea that stock price itself offers a wealth of information about growth assumptions. The greater the assumptions about future growth, the more risky the investment. Applying this way of thinking to Papa John's at the moment suggests the market is assuming that this company will grow earnings at a rate of about 5% going forward. That's a lotta pies! Given that the shares aren't objectively cheap, and given the fact that the dividend is likely not going to grow for a while, and given that you can get over 285 basis points more income risk-free, I'm going to pass on Papa John's again.

For further details see:

Papa John's Is Undercooked