PZZA - Papa John's: Near-Term Headwinds Keep Me On The Sidelines

2023-04-18 12:28:38 ET

Summary

- The near-term headwind of guest traffic slowdown is a concern for revenue growth.

- The benefits of moderating inflation and pricing should be offset by higher G&A and cost to support U.K. franchises.

- While the valuation is lower than the historical average, I would prefer to wait for near-term headwinds to subside before turning positive on the stock.

Investment Thesis

Papa John’s International, Inc. ( PZZA ) is facing a slowdown in guest traffic amid an inflationary and challenging macroeconomic environment, which could impact its comparable revenue growth in the near term. The company's premium product offering compared to its peers may also result in market share loss due to consumers opting for lower-priced options. Although PZZA plans to introduce new premium product innovations to offset the decline in traffic, it may not be easy given consumers' extreme price sensitivity in an inflationary environment. In terms of margins, although inflation is expected to moderate, the high costs of supporting franchises and increased G&A as a percentage of sales YoY could offset the moderating inflation and lead to flattish margins for FY23.

Despite trading below historical averages, the stock's near-term concerns keep me on the sidelines. I would prefer a wait-and-see approach to gauge the traction of the company's initiatives over the next few quarters. Currently, I have a neutral rating on the stock.

Revenue Analysis and Outlook

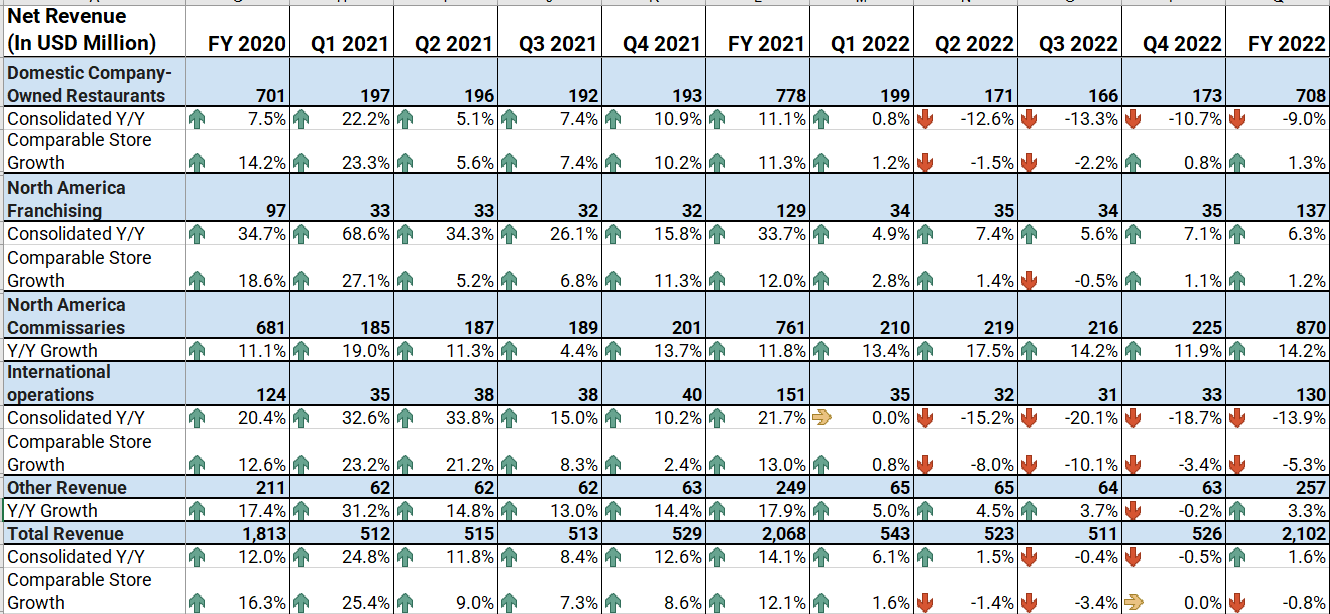

Papa John's achieved good revenue growth during the pandemic, thanks to its delivery-focused model, which benefited from a shift in consumer preference towards online food delivery. The trend of online delivery growth continued throughout 2021. However, as the economy reopened and outdoor mobility increased, people spent less time at home and ordered fewer pizzas, which along with tough comparisons from the pandemic years impacted sales growth in 2022.

In the fourth quarter of 2022, in addition to tough comparisons from prior years, lower comparable transactions (guest traffic growth) and a decline in international comparable sales due to lower consumer sentiments in the U.K. (Papa John's second-largest market outside the U.S., comprising 20% of international sales) adversely affected sales growth. However, positive comparable sales in North America, mainly driven by high-single-digit menu price increases, offset these declines. As a result, total company comparable sales was flat YoY, while reported sales declined 0.5% YoY to $526 million.

{kind=link}

PZZA’s Historical Revenue (Company Data, GS Analytics Research)

Looking ahead, I expect near-term headwinds from macro-related lower guest traffic to put pressure on PZZA’s sales growth. This should be partially offset by menu price increases and new innovations. Over the longer term, the company’s sales growth should benefit from new unit growth and global footprint expansion.

PZZA implemented price increases throughout last year to cover inflationary input costs, following the industry trend, which supported its sales growth. Going forward, the carryover impact of these price increases from the second half of 2022 should continue to have a positive impact on increasing ticket size and supporting sales growth.

However, the benefits of price increases should be somewhat limited, as the company does not anticipate further price increases moving forward. This is due to the decline in comparable transactions (guest traffic). Papa John’s pizzas and other food items have typically been on the premium side when compared to other large pizza chain peers. This has led to a decline in comparable transactions as consumers trade down to more affordable food delivery options in an inflationary environment. The slowdown in comparable transactions was further exacerbated by price increases last year. To avoid further declines in guest traffic due to increasing consumer price sensitivity, management is not planning for more price hikes, which means less upside from price increases in the future, compared to some of its peers which are still raising prices. Moreover, the premium price points and consumer trade-downs to less expensive food items could also lead to market share losses to competitors.

Papa John's has always placed emphasis on premium product innovations in driving guest traffic, which has worked in the company’s favor in the past. In the fourth quarter, it launched its new innovation, Crispy Parm Pizza, which has a premium price and is in its early rollout phase. According to management, PZZA has a good pipeline of new premium innovations to be launched throughout 2023. While these premium innovations may have worked in the past in attracting guest traffic when consumers were less sensitive to high prices, I believe the current inflationary environment should limit their effectiveness. Thus, I anticipate that the near-term headwinds from guest traffic slowdown in an uncertain macroeconomy will continue to impact sales growth in the upcoming months. I would prefer a wait-and-watch approach to gauge how much guest traffic these new premium product innovations attract in a recessionary environment before gaining confidence in management's premium innovation strategy.

In the long term, the company holds potential for revenue growth as it continues to expand in new and existing international markets. PZZA opened 244 net new units (excluding Russia) in 2022 and plans to accelerate its net new unit openings in the current year by opening 270-310 net new units. The company has set a target of reaching 1,400 to 1,800 net new units by the end of 2025, which implies an annual new unit growth of 6% to 8% between 2023-2025. To support this target, the company has a good pipeline of new restaurant growth in international markets. For instance, the company recently signed a deal with one of its largest global franchisees to expand into two new countries and add 100 new restaurants, bringing the total commitment to operating over 335 stores in four countries by 2030. One of these new countries, Jordan in the Middle East, opened in Q4’22, while the other is expected to open in 2023. Therefore, the company's longer-term revenue growth prospects should be supported by capturing new opportunities in international markets and expanding its global footprint.

Margin Analysis and Outlook

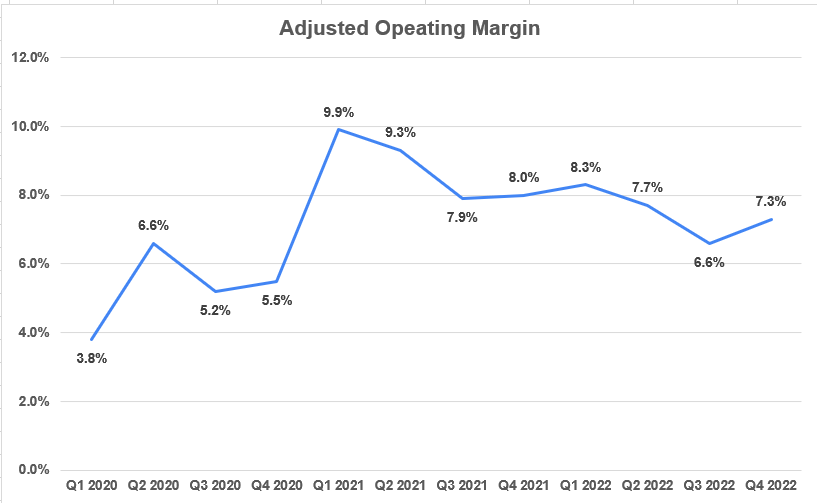

Over the past year, PZZA's adjusted operating margin was negatively impacted by inflationary pressures on company-owned restaurant margins due to high commodity costs, particularly cheese, and high labor wage inflation.

In the fourth quarter, commodity and labor costs remained elevated and were a 550 basis point headwind to company-owned margins. Additionally, sales deleveraging in the U.K. also impacted the operating margin in the quarter. However, the company was able to partially offset these headwinds through price increases. Overall, this resulted in a 70 basis point decline in the adjusted operating margin to 7.3%.

{kind=link}

PZZA’s Historical Adjusted Operating Margin (Company Data, GS Analytics Research)

Looking ahead, I anticipate that PZZA's margins will likely remain relatively flattish year-over-year. While inflation is expected to ease as we progress through the year, the incremental costs associated with supporting franchises in the U.K. are likely to offset the moderating inflation. The U.K. market is the company's second-largest market outside of the U.S., and in the face of an uncertain macroeconomic environment marked by high inflation, rising interest rates, an energy crisis, slowing economic growth, and volatile exchange rates, it is becoming increasingly challenging for franchises to operate efficiently. As a result, PZZA is expecting to make incremental investments in its franchise, including marketing initiatives in the U.K. market to boost demand. Additionally, the company anticipates that G&A as a percentage of sales should increase year-over-year due to higher performance-based compensation and costs associated with the return of the franchisee conference in Q2 2023 after a three-year pandemic hiatus. These elevated costs should somewhat offset the benefits of carryover price increases from 2H22 and moderating inflation. Consequently, margin should remain flattish in 2023.

Valuation and Conclusion

The company's current P/E (forward) ratio based on the FY23 consensus EPS estimate of $2.88 is 26.94x. While it is lower than its historical 5-year average of 38.74x, there is a good reason for it as demand has slowed down meaningfully in recent quarters. The near-term concerns stemming from the broader macro environment and its impact on PZZA's guest traffic make me cautious. It would be wise to wait and see how much traction the company's premium product innovation gains in an environment where consumers are highly price-sensitive and prefer less expensive dining options, both in-person and online. Therefore, despite the lower-than-historical valuation, I rate the stock neutral for now due to the near-term headwinds.

For further details see:

Papa John's: Near-Term Headwinds Keep Me On The Sidelines