PZZA - Papa John's: Worth A 'Buy' At The Right Price

Summary

- Good restaurants tend to be valued at a high premium due to the conservative and safe nature of their cash flows, even during a Recession.

- Papa John's has a bit more of a volatile up and down than one might expect from restaurants. COVID-19 impacts were present, but the company grew earnings significantly in 2021.

- However, 2022 is expected to be another declining year, and this has sent share prices tumbling from their highs.

- I show you my thesis on Papa John's.

Dear readers/followers,

My personal experience with Papa John's ( PZZA ) is limited to visiting the chain a few times with my ex when I was in the US for a longer time period. Restaurant and food serving stocks aren't exactly overrepresented in my own personal portfolio, due to their typical valuation, which tends to be on the high side.

However, after this decline and where the company is now trading - along with knowing something about the company, I decided to take a closer look and establish a basic thesis for Papa John's.

Papa John's Pizza - Good enough to eat?

Papa John's is the 3rd-largest delivery restaurant chain in the pizza sub-segment in all of the US as well as the world. The company has headquarters in the south of the country, found in Kentucky and Georgia, and a history of almost 40 years. The story behind Papa John's is a very good example of the American Dream, for it started when the founder, John Schnatter, installed an oven in a broom closet in the back of a tavern, of all things. He sold his Camaro to buy used pizza equipment in the amount of $1,600, his equity investment into the business, and began selling pizzas out of this converted closet.

Within a year, his pizzas proved so popular that John was able to move into an adjoining space, and the rest, as they say, is history.

The company has expanded to over 5,500 stores - and the founder actually bought back the Camaro he sold, only at a premium of $250,000 back in 2009.

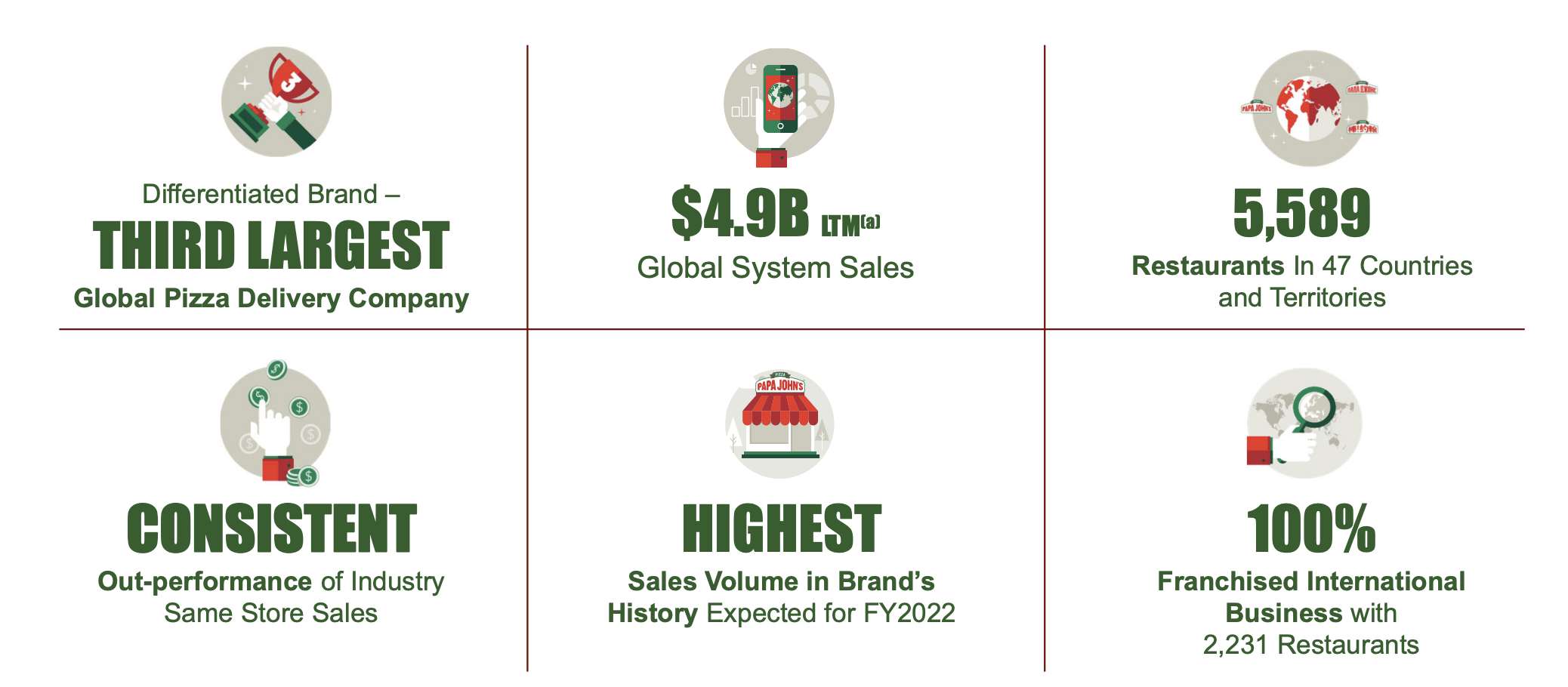

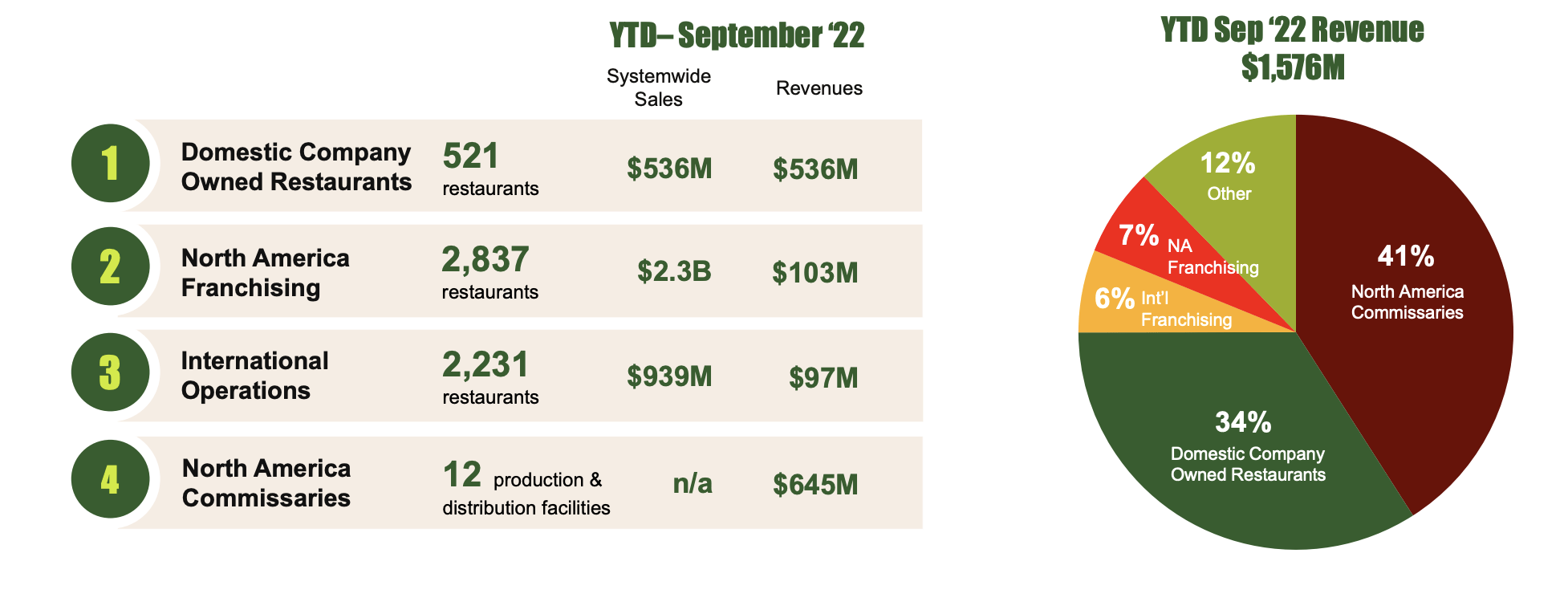

Today, Papa John's International Incorporated has a market capitalization of nearly $3B, and generates $4.9B in global system sales. The restaurants are found in 47 countries/territories, and the company is a consistent same-sector outperformer.

Papa John's operates a franchised business model on the international side, with 2,230+ restaurants found on the franchise side, and FY22 is expected to bring the highest sales on record.

Papa John's IR (Papa John's IR)

{kind=link}

Papa John's is a well-managed, and very "corporate" sort of business, which I view as a positive in this space. What I mean by this is that the company's management and board has very diverse experience from a large number of companies in the Fortune 500. I would have liked to see more straight experience in the pizza space, because I don't view it as that easy to get into on a high level, but experience in other ancillary food sectors can also be said to be an advantage.

Papa John's IR (Papa John's IR)

{kind=link}

The company has a number of product advantages. Its current supply chain and feedstock sourcing is already adjusted to meet what I would consider to be the needs and demands of the market. It's always fresh dough made out of "good" ingredients, meaning no MSG, BHA, BHT preservatives, cellulose, and no partially-hydrogenated oils. No HFC or Palm oil is used, and Papa John's is the first national pizza chain to remove artificial flavors and synthetic colors. This has been "standard" in Europe for perhaps 150 years, but it's good to see chains in the US catching up.

What I'm saying is that Papa John's makes "good" Pizza. I found myself liking it - not as much as the home-made pizza my ex made, but that's not the point of eating at Papa John's. The point is convenient, good pizza - and the company delivers this.

Papa John's IR (Papa John's IR)

{kind=link}

As I mentioned, Papa John's has delivered same-store outperformance both annually and on a longer perspective - and through the pandemic as well. The company has been able to generate higher transaction volume, as well as ticket size - meaning customers are buying more often and buying more per order. Customer retention is up, all the while managing a hell of supply-chain complexities and increased costs that have been hounding the industry - and others - for going on 1-2 years at this point.

Papa John's strategy for improving unit-level profitability - or maintaining it, is growing sales and incentivizing customer behavior while working to increase the premiumization of the Papa John's brand and optimizing its labor processes. There are no mentions of trying to increase efficiency in terms of input costs - only input processes to increase throughput, meaning Papa John's is likely not cutting corners in terms of ingredient quality, instead choosing to try and pass this along as much as possible.

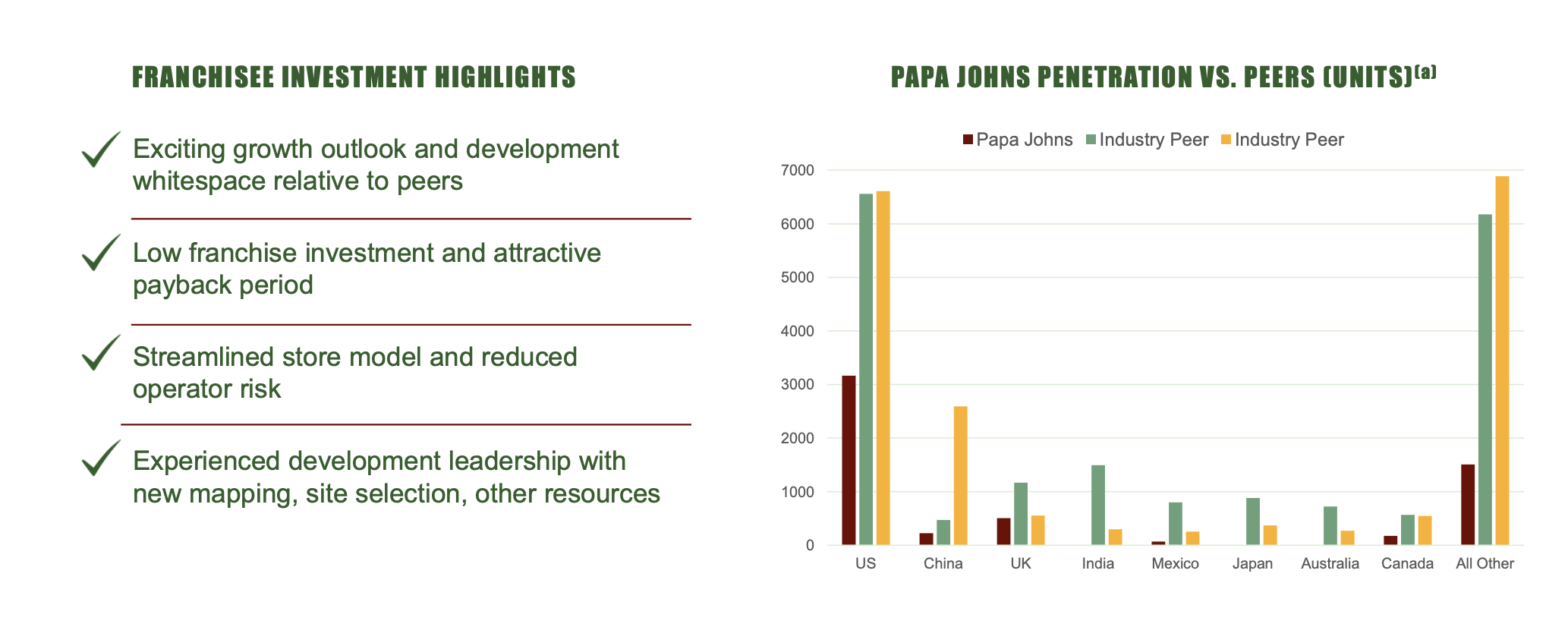

Unlike many US-based restaurant chains, international expansion is a focus for Papa John's - the company is significantly underrepresented compared to those peers that do have an international presence.

Papa John's IR (Papa John's IR)

{kind=link}

So Franchisees are likely to see advantages to taking a Papa John's franchise as opposed to something else - a company in the growth stage is always likely to offer more favorable terms for the interested parties here.

The company has been showcasing very impressive growth, and there's even talk about expanding to areas like Sweden, which would be welcome, since it's a different style of pizza that we have here.

This is how the current split looks.

Papa John's IR (Papa John's IR)

{kind=link}

So, what we're looking at here is a Pizza business looking to increase its already significant international footprint. The global pizza market is very attractive, and the company is already in a position where its able to deliver sustainable growth. The franchise business that you're investing in here is very asset-light, and on a high level, I would say Papa John's is very capably managed, given how it's managed to turn a profit even during the pandemic, and really hasn't dropped off significantly during any of the years we look at.

Instead, PZZA has spiked significantly, and long-term investors can be very happy. Investing $10,000 in PZZA 20 years ago would have generated returns of 12.9% per year. This isn't as high as say, Realty Income ( O ), which means that owning real estate technically was the better choice during the same timeframe, but it's still very impressive and market-outperforming, which is what we're looking for.

Papa John's also has a yield - that yield is currently 2%, which really isn't anything significant to write home about, but it's a dividend that has been growing and is likely to continue to grow here.

Q3 2022 results are the last ones we have. The positive momentum for the company has continued. The company is reporting average unit volumes for the NA sector of $1.1M, with a continued growth trajectory. This represents a 30% increase on a 3-year stack, which is peer-beating, due to menu innovation that has made Papa John's stand out as sort of the "premium" choice in Pizzas - and one I would agree with.

The international segment is focusing on growth, entering emerging markets before established ones, interestingly enough. 3,000 units are being built globally.

On a high level, 3Q22 saw sales in constant currency up 0.5%. Not the most impressive result "ever", but on top of an 11% increase in the prior year, which is actually good.

However, the bottom line here is down. Operating income and EPS declining, due to the company's costs and challenges being only partially offset by pricing actions and efficiencies. Additional headwinds in established international markets like the UK are also present, and PZZA confirms in the latest call that market circumstances have certainly changed.

In particular, these challenges hail from massive increases in food and labor costs, which are seeing ATHs. The high inflation is weighing things down - and Papa John's is not following the competition here , which has seen aggressive discounting to keep up with sales. While Papa John's provides value and promotions, it doesn't take the same approach, instead seeing it as an opportunity to differentiate itself as a "Premium" player.

This is likely what's going to drive the company for the foreseeable future - and this brings us to valuation.

The valuation for Papa John's is pretty attractive

Franchise companies have tended to trade at a relatively steep premium due to their business model being more resilient and less cyclical than your typical restaurants. Also, in owning the franchise, you're insulated from some of the cost risks, and more or less just own a part of royalties coming in, which is always an attractive sort of thing to have.

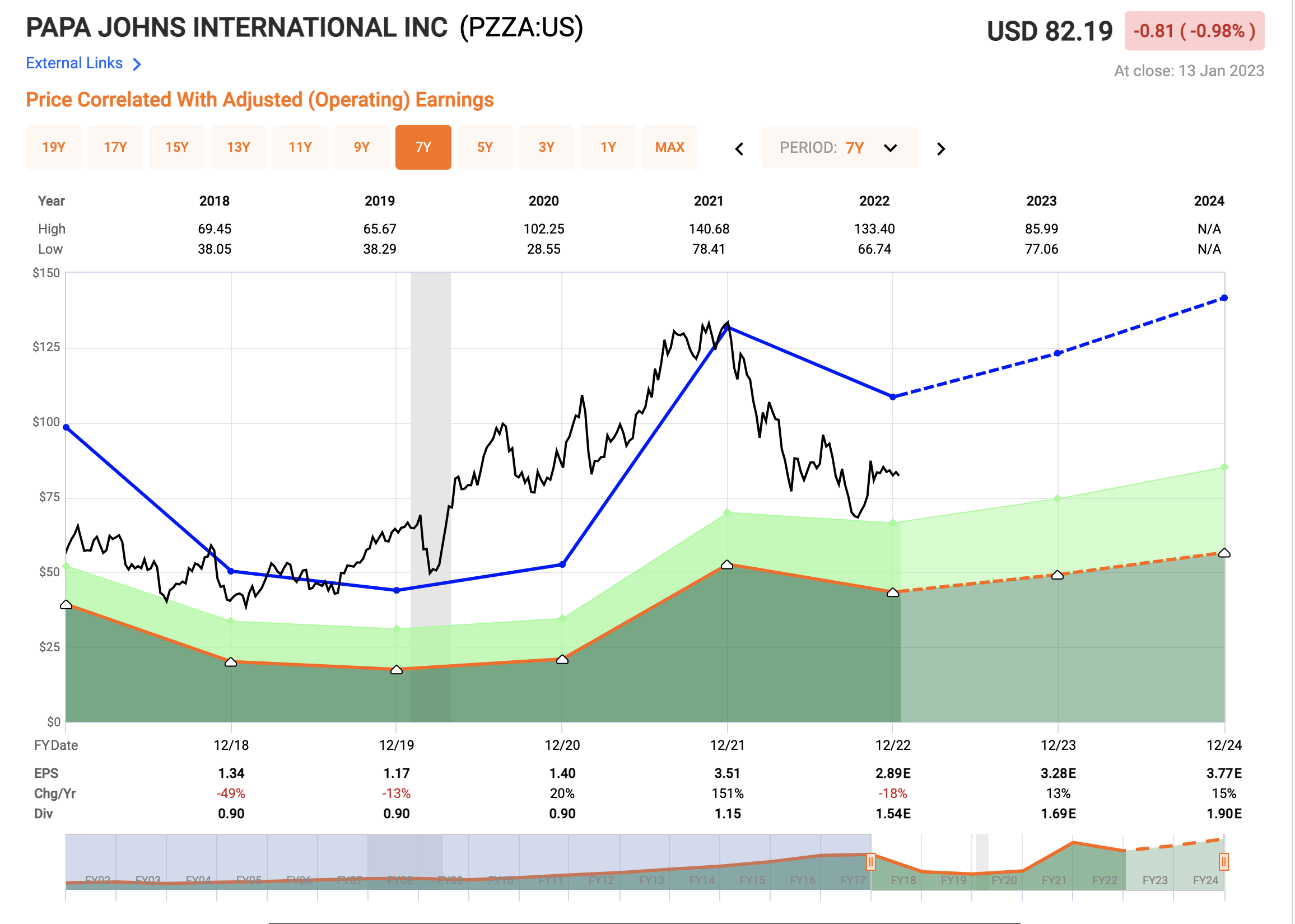

The company's 5-year typical trend is trading at around 37.5x P/E, which is high even on a peer basis. The current valuation has dropped to around 28.3x in the wake of the aforementioned cost challenges, and this is the lowest we've seen on a normalized P/E basis since 2017-2018 when the company was in a significant EPS decline.

PZZA valuation (F.A.S.T graphs)

{kind=link}

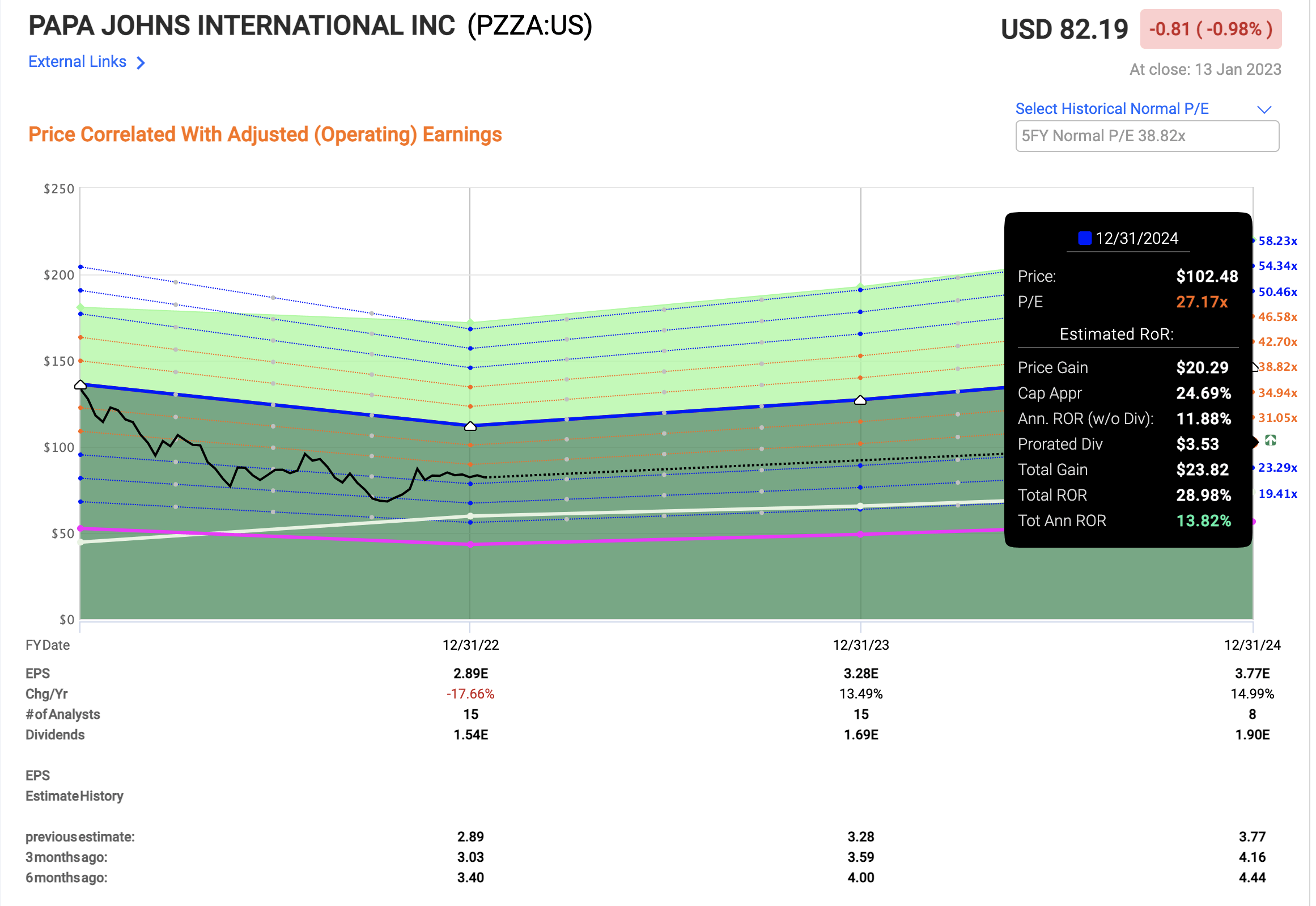

If we look at the 5-year, and the company's potential earnings trends, there is an upside to Papas here. Even just forecasting 27-31x P/E, the upside for Papas begins in the double digits at nearly 14% and goes up to nearly 30% conservatively.

{kind=link}

The question is of course what will happen to the company's P&Ls, given the current ups and downs in costs and inflation. That 13 - 15 % annually upon which this forecast is based on forecast accuracy that historically has been better than terrible. Negative misses only occur 17% of the time, at least for the past 10 years, but it's worth noting that those negative misses have exactly been during the latest declines.

I say that the company does deserve a premium, but it's uncertain if this degree of premium is justified. The analysts following the company - 14 of them - consider the company a "BUY" based on $82 low and $127 high with an average of $95/share. 10 of the 14 analysts are at a positive "BUY" or equivalent here.

Peers in the sector include companies like McDonald's ( MCD ), Starbucks ( SBUX ), Chipotle ( CMG ), and many others. It can be said that at current levels, PZZA is cheaper on a P/E basis than most of the peers - except Darden ( DRI ) and Restaurant Brands ( QSR ). A sector average lies at that 29-33x p/E average, and below this is where I would consider the company attractive overall.

So, based on this, I would consider PZZA to be an attractive investment here. It's still at a premium, but the premium could be considered justified here.

A couple of different ways to play this - here is my Thesis for the company.

Thesis for the common share

- Papa John's is an attractive company based on its position as a global pizza leader (among them). The company is an attractive franchise business with great overall upside at the right valuation.

- I believe the current price for PZZA isn't bad at all - at least not from an overall peer average, or potential where the company might go.

- At the same time, there are risks to how low the company could fall due to inflation and earnings pressure, and how "high" things may be expected to go.

- I give Papas a PT of $85/share, towards the lower end of the range. It's a "BUY" here.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

The company fulfills all of my demands, and I view it as attractive here.

Thesis for the Options

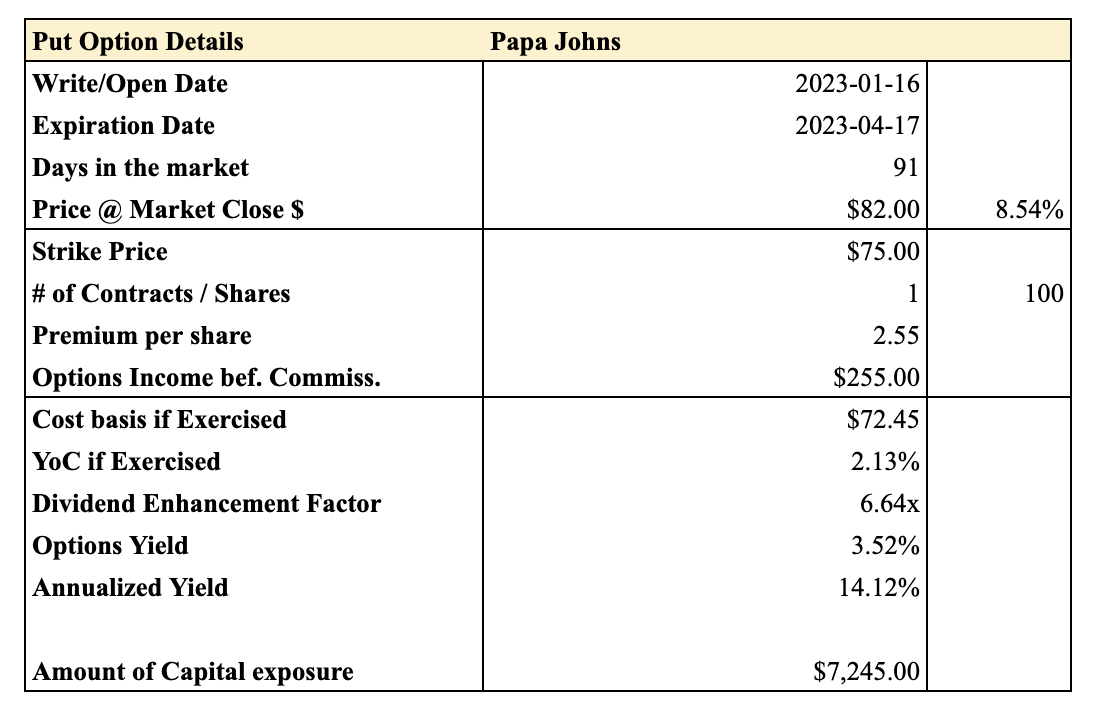

However, PZZA may also be an attractive options play if you're willing to write some puts. You could potentially get a somewhat lower cost basis - or just a great premium - if you're willing to put around $8,000 on the table here.

Take a look at this put (based on Friday market data).

{kind=link}

Now, that's a very decent RoR for the risk you're taking, as I see it. It's good enough and conservative enough that I may put some money on the line here until April.

Those are some ways you could go into PZZA here - but as things stand, this company is a "BUY".

For further details see:

Papa John's: Worth A 'Buy' At The Right Price