PARR - Par Pacific Holdings: Low Valuation But Seemingly Deserved

2023-08-08 11:03:38 ET

Summary

- Par Pacific Holdings, Inc. has seen substantial growth in the oil and gas refining and marketing industry, with a 93% increase in share price.

- The company's investment in Hawaii Renewable Fuels is expected to drive future growth and provide exposure to markets with strong demand.

- PARR has a successful history of strategic acquisitions, fueling growth and expanding its market share.

Investment Summary

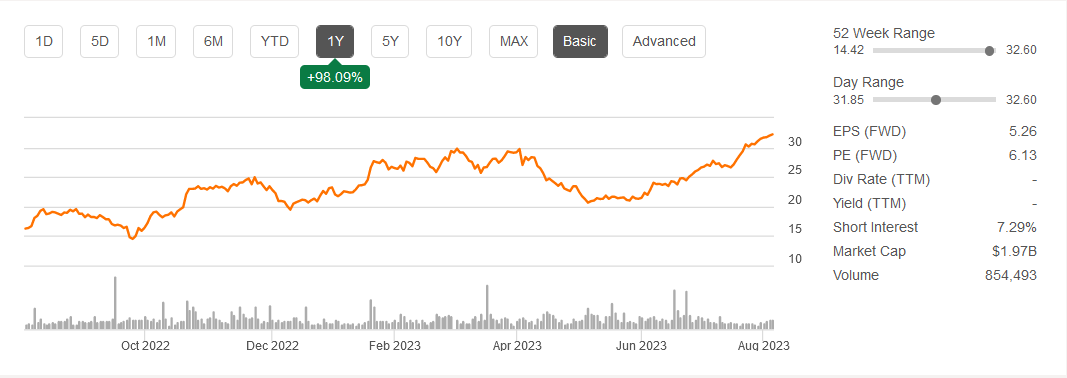

Par Pacific Holdings, Inc. ( PARR ) is operating in the oil and gas refining and marketing industry where it has seen substantial growth over the last 12 months. The share price has increased by 93% and this is still not putting PARR at an overvalued place, I think. With strong oil price outlooks, the future seems very positive for the company. Operations span the United States and PARR has a very successful history of strong acquisitions to fuel more growth.

The significant investment that PARR made into Hawaii Renewable Fuels should be a driver of growth going forward. The strategic position this lets the company has is enabling them to have better and broader exposure to markets offering strong demand. With the favorable valuation of the company but unfortunately, the company tends over the years to dilute shares. This is putting some risk on the side of investors as the share price might plummet if a quarter produces a disappointing result. Share dilution seems necessary as the net margin is still not that high. To make strategic and valuable future acquisitions it seems that dilution will be one of the ways of PARR to do this. This is however not making PARR out to be a buy, but rather a hold in my opinion.

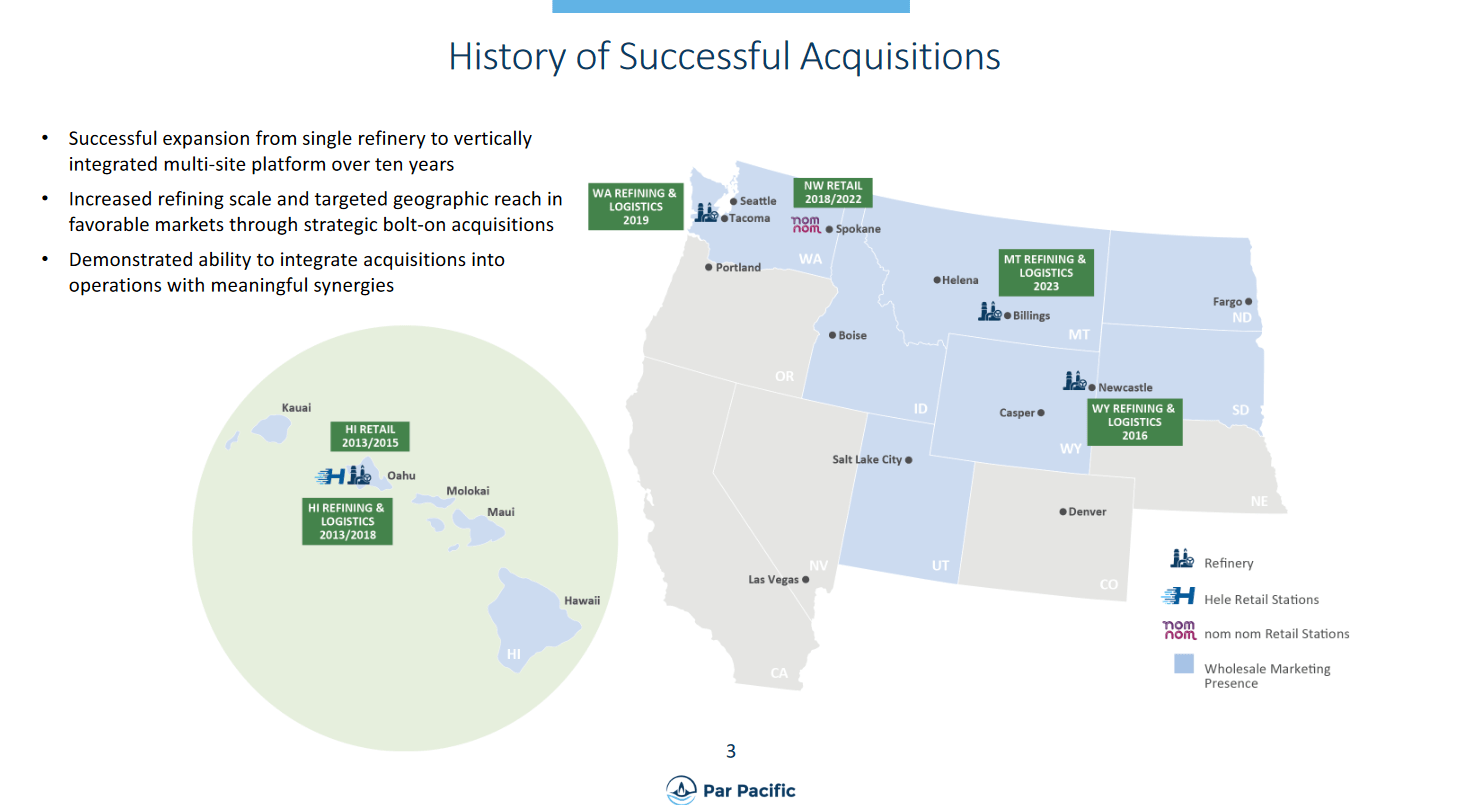

Strategic Acquisitions Are Fueling Growth

Over the years, PARR has been quite successful in making acquisitions to fuel growth and deliver strong reports. Acquisitions are also lending a broader expansion and market share for PARR.

Company History (Investor Presentation)

{kind=link}

Some of the notable operations are currently in Hawaii where PARR has invested in Hawaii Renewable Fuels. Back in April, the company announced a capital investment of $90 million to help support the development of a production facility for liquid renewable fuels. The aim is to capture some of the tourist demand in Hawaii as many flights are coming to and from the island. As PARR invested to gain exposure to sustainable aviation fuels ((SAF)) they have gained a strong foothold here as a result.

Besides this though, the company is also making acquisitions in other markets. On June 1 the company completed the acquisition of Exxon Mobil Billings Refinery and related upper logistics systems.

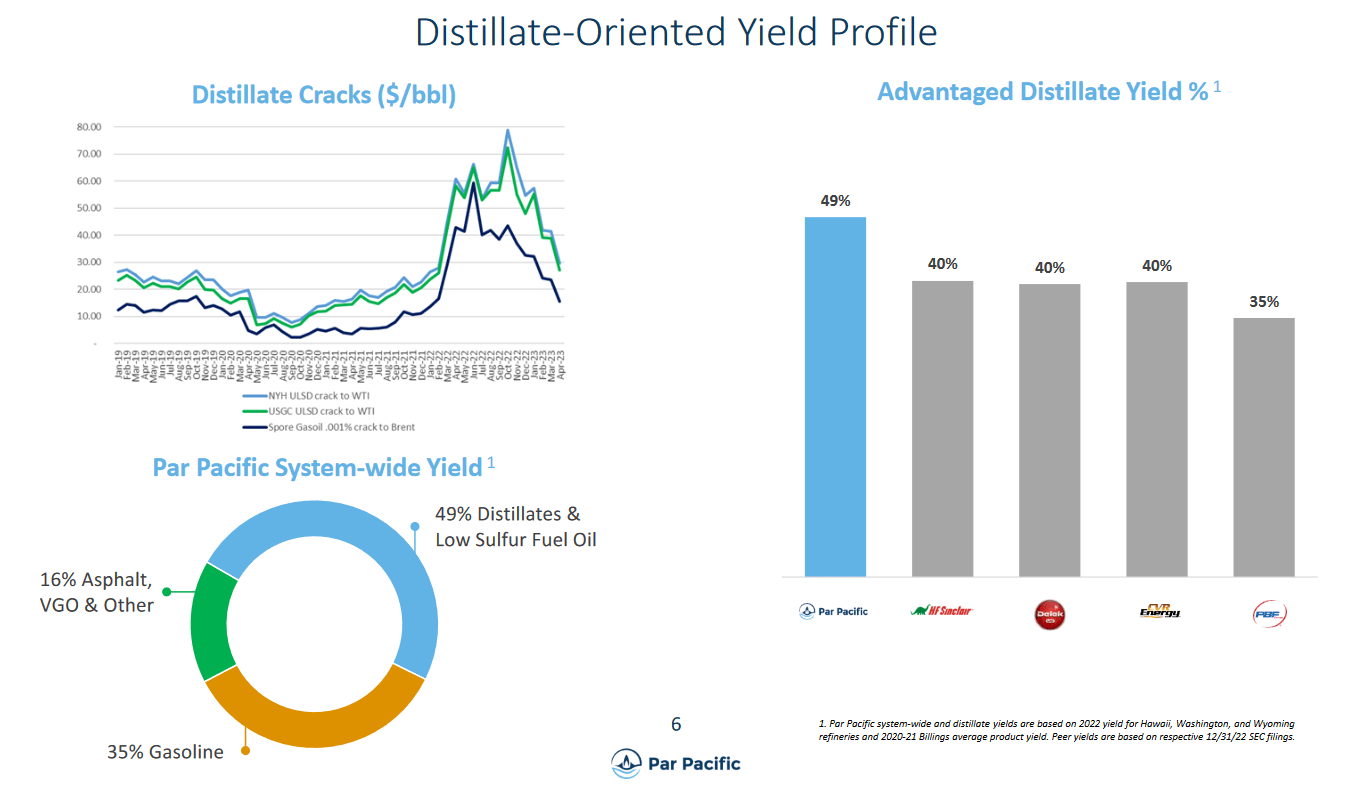

Yield Profile (Investor Presentation)

{kind=link}

With PARR, you are seemingly getting a very favorable investment opportunity right now it seems. The company has a very high distillate yield compared to peers at a 49%. The company-wide yields are also quite well diversified as 35% comes from gasoline and 16% from asphalt, VGO, and others. The remaining part is from Distillates & Low Sulfur Fuel Oil. This is creating a very well-diversified risk profile for PARR and cause for the hold rating being supported.

The company also quite recently released earnings which showed a solid beat on both the top and bottom lines.

Earnings Release (Seeking Alpha)

{kind=link}

If these results seem to be able to be maintained then I think it will be interesting to see where the share price might head in the coming quarters. If PARR proves that it can beat out market challenges and still perform then I could reconsider the rating of the company, but time will tell if that is true or not.

Risks

The company's operations exhibit a notable seasonal pattern, heavily influenced by fluctuations in highway traffic and consumer demand for gasoline in the Rockies and Northwest United States. During the summer months, when travel and outdoor activities peak, the demand for gasoline surges, driving higher revenue for the Wyoming and Washington refineries. However, as winter arrives, and with it reduced travel and outdoor activities, the gasoline demand typically decreases, leading to potentially lower financial and operating results for the first and fourth calendar quarters.

Market Position (Investor Presentation)

{kind=link}

The seasonality of the business can present both opportunities and challenges for the company. On one hand, the peak summer months offer a revenue boost, as consumers hit the roads for vacations and outdoor adventures. This period of increased demand can be advantageous for maximizing profits and generating healthy cash flow.

Financials

Looking at the financials of the company it is in a much better place right now than some years ago. The net debt is negative which presents a very sound financial position for the company.

The liquidities of the company are at the highest levels it has been at, sitting at $750 million as of the last report. The net debt is negative at $111 million which ensures that PARR can make strategic acquisitions like they have and not risk overleveraging themselves too much.

Financials (Investor Presentation)

{kind=link}

The cash position of the company is also decently at $191 million which has grown from levels two years ago when cash was $112 million instead.

What has been greatly helping the financial state is the fact that PARR has been very efficient in raising its operational performance. In Q2 FY2023 the net cash from operating activities totaled at $145 million. This is a strong improvement from the negative $7.7 million a year prior.

Valuation & Wrap Up

Looking at the valuation of PARR I think it can look quite intriguing sitting at a p/e of just under 6. But some improvements are necessary to make this company a buy in my book. My first concern with the company comes from the fact they are diluting shares at an alarming rate. Shares outstanding sit at 60 million, up from 50 million in 2019. That is a CAGR of 5%. This is enough to hurt an investment and dilute the long-term returns.

{kind=link}

The company does have a solid balance sheet where the cash position is at the highest level ever so I don't see the necessity exactly of diluting shares like this. I would much rather prefer to see a slowing cash buildup and a complete stop in dilution. This would most likely also help raise the share price to a valuation more in line with the overall sector, a p/e of 9 or so. Until we see these improvements, I won't be able to make PARR a buy, but given the appealing markets they are entering, I think it's enough to justify a hold rating at least.

For further details see:

Par Pacific Holdings: Low Valuation But Seemingly Deserved