PAR - PAR Technology Is Much Better Under The Hood

2023-09-06 01:48:11 ET

Summary

- PAR Technology had a bad quarter with widened losses, but underlying growth is strong and expected to continue.

- Large chains are seeing integrated SaaS solutions as a necessity, not just an investment.

- PAR's Operator Solutions segment showed healthy growth, while Payments module has a large opportunity for expansion.

PAR Technology ( PAR ) seemingly had a bad quarter as losses widened despite significant ARR growth (24/3% in Q2). However, we will claim that:

- Underlying growth is very strong and likely to remain strong for the foreseeable future.

- Loss widened as a result of investments in growth in order to scale solutions, margins will recover in H2 also on the automatic scaling of Payments.

- OpEx remains constant at the Q4/22 level, underneath there is great operating leverage.

Large chains are starting to see integrated SaaS solutions not just as an investment, but as a must-have solution ( Q2CC ):

But in today's world, they are also trying to reduce costs, mitigate risk and convert cost centers to profit centers... For years, they viewed technology as a capital investment, and today, they are coming around to the idea that software is now a key investment in the OpEx line of their P&Ls.

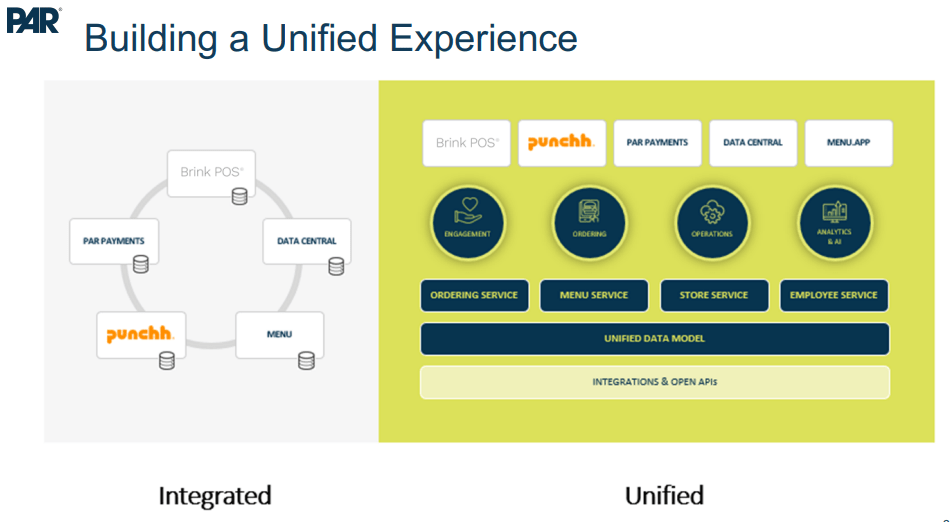

The demand for the type of unified solutions that PAR provides is significant and management is hopeful that they can break through into the enterprise segment.

{kind=link}

Three segments

- Operator Solutions (Brink + Payments)

- Guest Engagement (MENU + Punchh)

- Back Office (Data Central)

They also have a hardware business (POS terminals with McDonalds as a customer) and a legacy government defense business that they will sell.

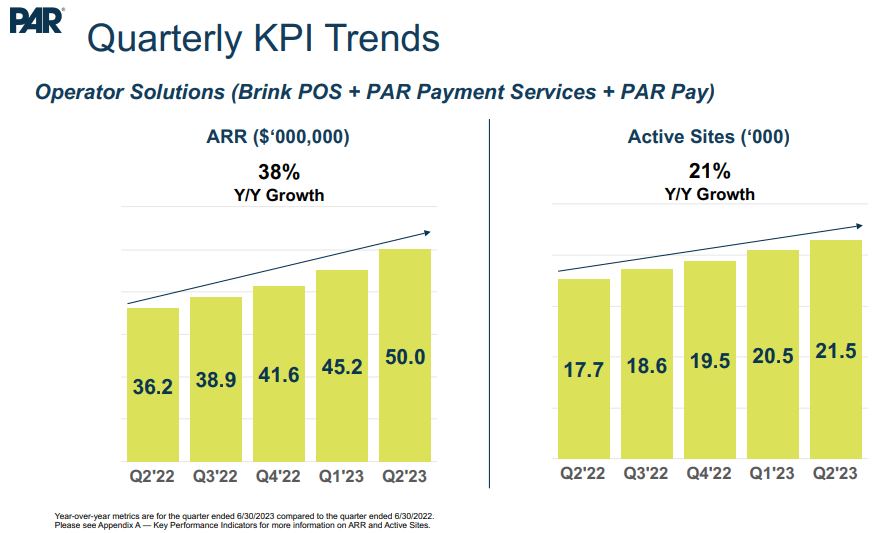

Operator Solutions

{kind=link}

This segment showed very healthy ARR growth at 38% y/y, and 11% q/q, adding 115 new stores and 1100 new bookings with annualized churn at just 3.6% for Brink in Q2.

Brink's ARPU increased 14% as a result of better pricing in new contracts and payment attachments which is very significant as the vast majority of customers are on lower old contracts, many of which are very low as Brink was just starting up and needed customers. Payments attachment is still very low.

Payments

PAR spent years developing this module and the first data point to a large opportunity, which isn't surprising as competitors tend to get most of their revenue out of their payment modules.

There is a large road ahead as not even 10% of Brink customers are on it but it's already processing over $1B in GPV and producing meaningful revenue in the Operations segment.

Margins are still lower but will increase to just under SaaS margins when it scales. Planned innovations will add to the payments solution, enabling it to become a real differentiator.

For instance, the company has already fully rolled out its one-tap loyalty solution powered by Apple Pay with Salsarita's.

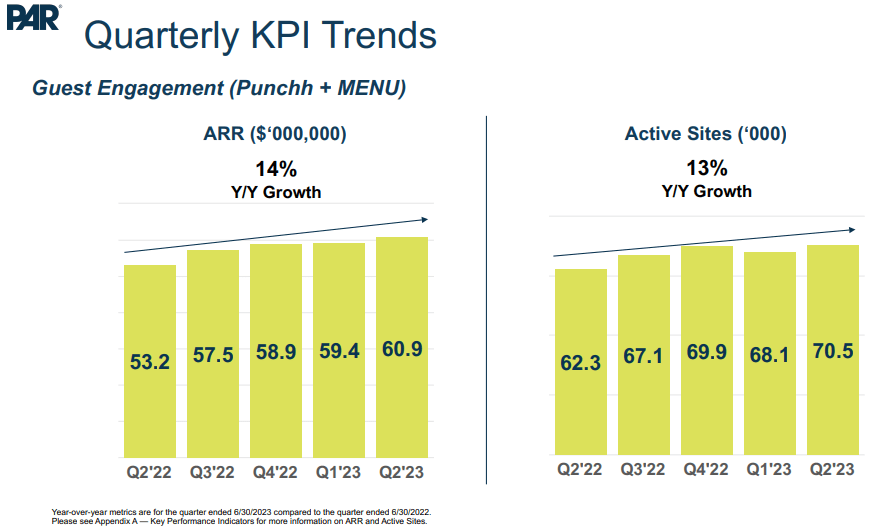

Guest Engagement

{kind=link}

The company launched a new fast-casual chain with 2400 locations.

The usage of Punchh (loyalty programs) has increased four-fold in a year, so fast that it challenged the infrastructure, leading to an investment surge (also for MENU). This is part of what the market got wrong in their initial reaction after the Q2 figures were published.

Management regards MENU ( acquired a year ago ) as the best electronic ordering software on the market. It was mainly used in Europe but management has introduced it in the US and the response has been very good, although this has increased the cost as well. Management sees revenue growing strong from Q3 onwards.

MENU signed more than three chains and has another three in the final stages of signing three additional brands in Q3 already, more than doubling the store count.

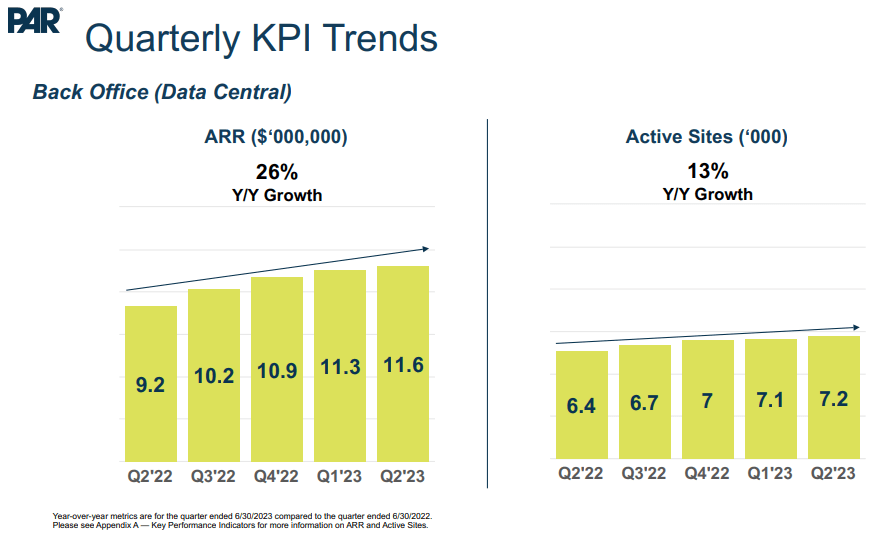

Back Office

{kind=link}

Back office is also still growing nicely and offers upselling and cross-selling opportunities.

Government business

Revenue from their government/defense business grew 48.2% to $31M and there are even better times ahead as the backlog ballooned 61% to a whopping $297M.

And that's not even all, after the quarter closed this business won another big contract . Perhaps now is a good time to sell the government business and concentrate on the restaurant business.

Hardware business

We should not forget the company also sells POS terminals to the likes of McDonalds, but the nature of this business is quite lumpy so this quarter saw a 7% decline to $26.4M although sequentially the business was flat.

That was actually ahead of forecasts and management sees strong hardware sales, with existing Tier 1 customers as well as across its Brink customer base. Margins did improve 450bp to 19.2% though.

Q2 Finances

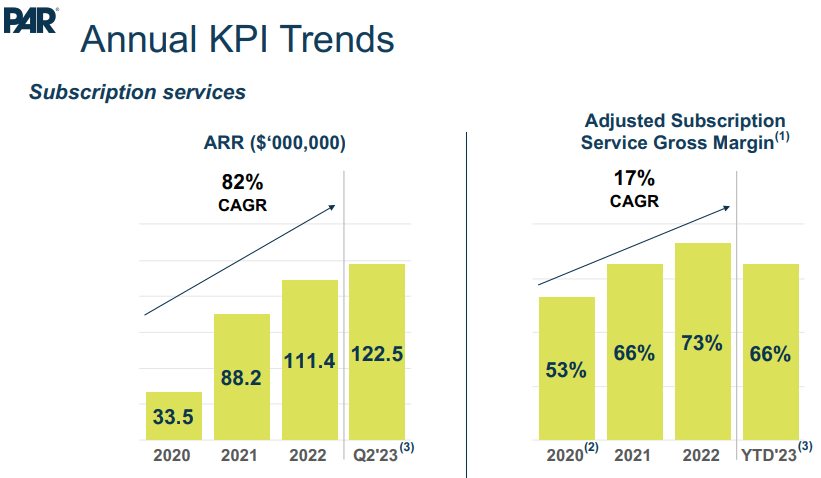

The most important metric is ARR growth, which came in at 24.3% in Q2

{kind=link}

The H1 decline in subscription margins is due to one-off investment (see below). Some additional metrics

- Revenues +18/2M to $100.5M

- ARR +24.3% to $122.5M

- AEBITDA -$9.9M versus -$5.8M in Q2/22

- Hardware revenue -7% to $26.4M flat q/q

- Subscription services revenue +31.2% to $30.4M

- Government business +48.2% to $31M

- Government contract backlog +61% to $297M

- Professional service revenue +1.1% to $12.8M

- Adjusted net loss of $14.1M (-$0.52 EPS)

PAR Q2/23 10-Q

Margins

The most notable item was the decline in gross margins at 61% which is the result of investments mostly for enabling the growth in Punchh and MENU and Payments. Management expects gross margins to recover in H2 as:

- 1) These investments peaked in Q2

- 2) Applications like Payments and MENU scale

- 3) New contracts have much better pricing, increasing ARPU

- Hardware margin + 450bp to 19.2%

- Subscription services margin -1060bp to 43.3% due to the growth of early phase products which have a lower margin while scaling up

- Professional service margin -910bp to 7.7% driven by one-time charges and will move back up to the mid-teens in H2.

- Government contract margin -680bp to 4.3% but will move back to higher single digit in H2.

- GAAP SG&A -$0.8M to $25.6M y/y

- Net R&D +$4.8M to $14.9M (backing out non-GAAP adjustments and MENU +$2.4M or +24%).

- Net interest expense $1.7M down from $2.5M in Q2/22 due to increased interest income.

Cash flow is still quite negative but improving fairly rapidly:

The company already produced a positive operational cash flow of $4M in Q2.

Valuation

- 1M options and 880K RSUs for a total share count of 29.33M shares fully diluted

- A market cap of $1.23B (at $42 per share)

- $390.2M debt ($$376.6M long-term)

- $85.38M in cash and equivalents

- FY23 revenue estimated at $407M

- EV of $1.53B or an EV/S of 3.75x

On an estimated year-end ARR of roughly $140M the shares trade 11x EV/S which is in line with competitors but investors get the government and hardware business for free.

Conclusion

We see many positive developments that make the stock attractive:

- Increasingly complete platform offering a unified experience that is becoming attractive for larger customers

- Relentless ARR growth with ample cross-selling opportunities

- PAR payments just starting to scratch the surface

- MENU has huge opportunities in the US as its revenue mostly came from abroad before the acquisition and it's a best-in-breed app.

- The company is making its first inroads into the much larger table-service segment

- Booming government business with a ballooning backlog and could be sold at any moment.

On the negative side, the company still has a substantial debt and produces significant losses and cash bleed, but these problems are declining and we think the company has enough cash to last them to cash flow positive, and they could always sell their booming government business should things get tight.

For further details see:

PAR Technology Is Much Better Under The Hood