PAR - PAR Technology: Large TAM And A Strong Product

2023-10-12 13:26:38 ET

Summary

- I recommend a buy as PAR has a strong product offering and potential for growth in the digitalization wave of the restaurant industry.

- PAR's main business is point-of-sale systems in fast food restaurants, with customers including McDonald's, Yum! Brands, and Burger King.

- Despite recent profitability challenges, PAR has a large total addressable market and a track record of winning deals and upselling.

Overview

My recommendation for PAR Technology ( PAR ) is a buy rating, as I expect the business to continue gaining share in this large TAM by winning deals and upselling (improving ARPU). PAR has a strong product offering that makes it competitive and well-positioned to ride on this digitalization wave in the restaurant industry.

Business

PAR’s main business is point-of-sale [POS] systems in fast food restaurants, where its main customers are from big players like typical enterprise-level restaurants like McDonald’s (MCD), Yum! Brands (YUM), and Burger King (new exclusive agreement). PAR’s POS is commonly known as Brink POS, which is a cloud POS system that charges a subscription fee for continuous usage. The nature of a cloud POS system enabled PAR to integrate Brink with multiple other point solutions like self-ordering kiosks, food delivery ordering systems, enterprise reports, etc.

Recent results & updates

PAR has done very well over the past few years as it emerged from the COVID period, where growth slowed significantly due to implementation delays (due to lockdowns). The growth data posted after the COVID period (FY20 to LTM) is a clear indication that PAR’s innovations and offerings are gaining significant adoption. For context, total revenue grew from $187 million in FY19 to almost $400 million in the LTM period. While revenue grew staggeringly, profits did not follow through. PAR continues to be in the loss-making region on an adj. EBITDA basis. As of LTM 2Q23, PAR generated an adj. EBITDA loss of -$30 million or -7.4% margin, which is a deterioration from FY21 and FY22 levels of -6.3% and -5.4%, respectively.

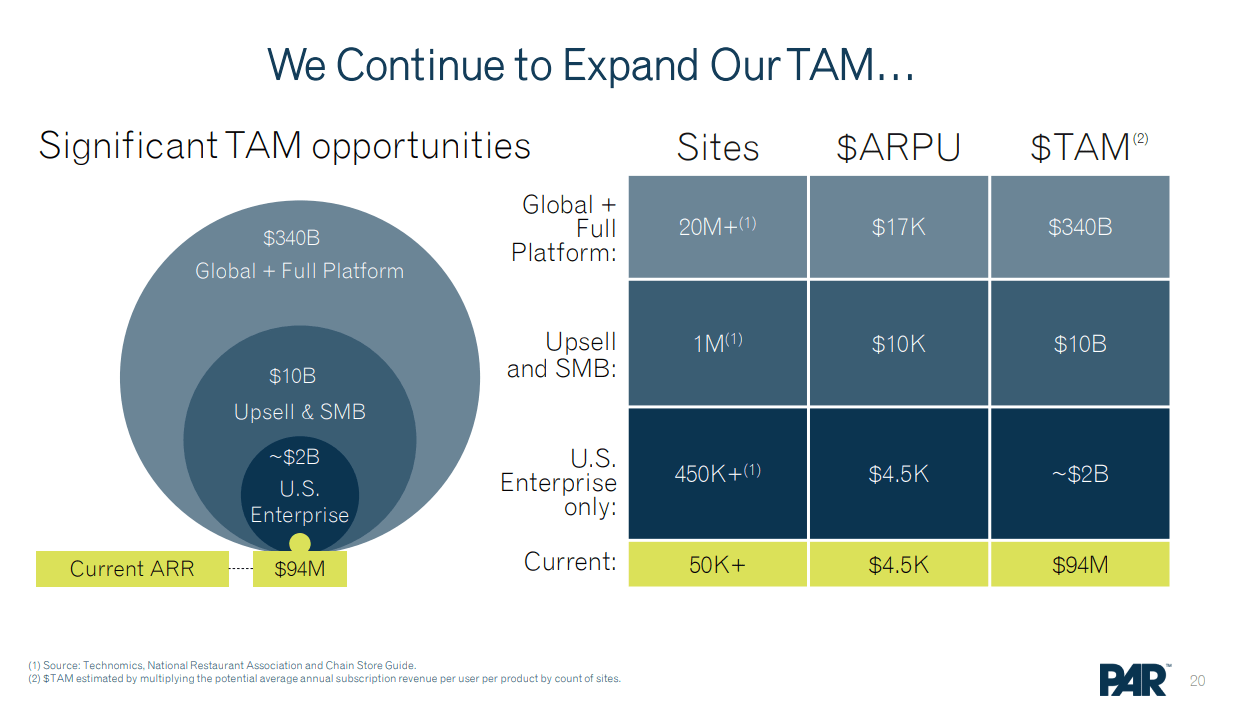

The second quarter was a mixed bag for PAR, with revenue exceeding expectations ($101 million vs. consensus $98 million). Despite this, profitability is still low because subscription gross margins have dropped significantly. This drop was attributed to increased investments in MENU and one-time credits for Punchh , becoming a Unified Commerce Cloud Platform for Enterprise Restaurants customers, due to increased demand and subsequent service disruptions. Even though short-term margin pressures are discouraging, I think it's wise to reinvest in the company since the TAM is so large. Based on the FY22 investor day, PAR has the potential to address a total TAM of $340 billion, which is just a fraction of that figure today.

{kind=link}

Management has, without a doubt, been attempting to reposition their product to attract a greater share of this TAM. In the conference held by Goldman Sachs , management stressed the firm's shift in emphasis to emerging brands at the enterprise level like Cava and Sweetgreen, both of which have experienced rapid growth over the past decade. This is a step forward from the traditional focus on large enterprise-level quick service restaurants [QSR] like McDonald’s. I believe the PAR unified commerce solution has a strong value proposition for restaurants that are using disparate point solutions to operate their stores. For instance, when all of the platforms are brought together in one place, the company can easily reconcile data because everything is done in the cloud. While point solutions can be integrated, they are often not seamless (i.e., data syncs every 24 hours and is not live).

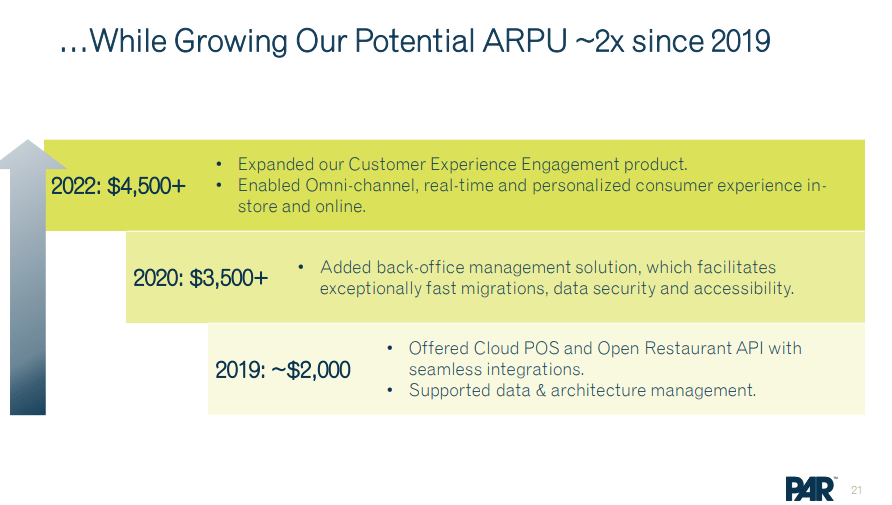

On this end, I really like PAR’s approach of gradually consolidating point solutions under its own wings (the acquisition of Punchh and MENU), which enables them to rewrite the backend code to integrate with PAR seamlessly. The economics of a PAR unit show that this strategy has been effective. Over the years, POS ARPU has increased from $1.9k to $2.3k, which I expect to continue to increase over time as PAR continues to upsell solutions that work seamlessly with PAR. As the world becomes more digitalized, restaurants have no choice but to keep up. As such, PAR’s growth constraint is not on the demand side; it is on the supply side (sales strategy). Encouragingly, PAR has had a good track record of selling, as seen by the growth of ARPU over the years.

{kind=link}

The fact that PAR was able to secure a deal with Burger King is the best evidence yet that their product is among the best on the market. In a press release issued last week, PAR announced that they had signed an exclusive Unified POS Agreement with Restaurant Brands International Inc. ( QSR ) to become the sole provider of software and services (specifically, Brink POS and MENU) for Burger King's classic restaurants in North America. Considering the history of trust and cooperation between PAR and other major QSR chains, this is not shocking to me at all. Nonetheless, I think the victory cements PAR's position as a leading POS provider and sets the stage for further deal competition.

I'd also like to mention PAR's payments solution, which, as the company expands, has the potential to be a key factor in increasing ARPU. So far, the attachment rate is around 50% (according to management during the Goldman Sachs conference), which I expect to increase over time as the unit economics are very attractive for the restaurants. Management claims that their payment processing solution is helping eateries cut costs by as much as 70 percent while making it much simpler to implement. Viewed holistically, restaurants that adopt PAY’s payment solutions will also have access to more well-rounded data that could drive further business insights. Hence, I expect the attachment rate to continue increasing.

Valuation and risk

Author's valuation model

According to my model, PAR is valued at $48 in FY24, representing a 20% increase. This target price is based on my growth forecast of 13% CAGR through FY25. The rationale for using 13% is based on annualizing 1H23 revenue and assuming that PAR can sustain this growth rate in the near term given the large TAM and good track record of winning deals and upselling. I did not model an acceleration, as I remain conservative on the macroeconomic timing of recovery.

PAR is now trading at 3.15x forward revenue, which I believe it should maintain at this level as its premium compared to peers is within the historical average of 1.8x. PAR deserves this premium due to its market position, targeting enterprise-level restaurants that have lower churn and better unit economics relative to peers that are targeting lower SME restaurants (Toast and Lightspeed). When compared to NCR Corporation (which also targets enterprise restaurants), PAR deserves a premium as it is growing much faster (10+% vs. NCR in mid-single digits).

{kind=link}

The risk here is if smaller players continue to gain traction and build a strong product that enables them to have a footing in the enterprise restaurant market. We should not forget the fact that PAR built its product through acquisitions ( Brink was acquired in 2014 ), which means peers could go down the same path to build a similar product. Suppose this comes true. PAR’s growth could be slower as competition increases.

Summary

With a solid product offering, a substantial TAM, and a history of rolling out the right products, the company is well-positioned for growth in the restaurant industry's digitalization wave. Despite recent profitability challenges, the focus on expanding its product suite and appealing to emerging brands demonstrates a strategic shift that can enhance its competitiveness. The exclusive agreement with Burger King underscores PAR's industry leadership, and the payments solution offers additional potential for increasing ARPU.

For further details see:

PAR Technology: Large TAM And A Strong Product