PAR - PAR Technology Looks Set To Have Another Good Year

2023-04-05 15:12:01 ET

Summary

- State-of-the-art integrated SaaS solution still has a lot of market to go after with a host of cross-selling opportunities remaining as well.

- ARR, ARPU and gross margins are rising inexorably with operational cost set to stay constant this year, producing steady narrowing of losses and cash bleed.

- While the shares are not cheap, the company kept growing even during the pandemic so we see few risks ahead.

- We see this as a long-term compounder.

PAR Technology ( PAR ) is a supplier of POS systems and SaaS software solutions mostly for the fast-casual segment, selling to restaurant chains. They also have a legacy government defense business that has been perking up lately and could be sold.

While the company still makes significant losses, financials are steadily improving and the company has plenty of cash and other options (like selling its legacy government business) for us not to worry about today's losses.

Investment thesis

- State-of-the-art software.

- The inexorable rise in ARR through adding labels, restaurants, and cross-selling.

- Steadily improving financials through gross margin expansion and operational leverage.

- Opportunity to go beyond fast-casual to table service restaurants.

{kind=link}

Let's start with the state-of-the-art software:

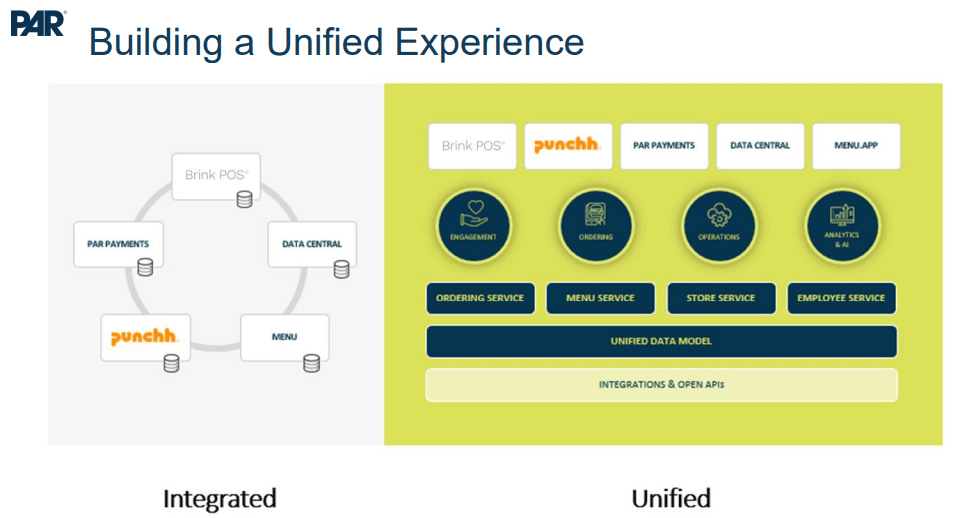

Unified Experience

Through in-house development and smart acquisitions, the company now has a complete in-house offering of software solutions for restaurants consisting of three segments:

- Operator Solutions (Brink POS + PAR Payment Services + PAR Pay)

- Guest Engagement (Punchh + MENU)

- Back Office (Data Central)

{kind=link}

The idea is that the whole offers better value than the sum of the parts, as it enables clients to get a unified experience based on a unified set of data and a consolidation of vendors.

The company has restructured its sales process and assigned teams to clients to increase accountability and identify cross-selling opportunities and management clearly thinks it's a growth driver ( Q4CC ):

we think our ability to maintain our growth rates is differentiated, driven by the unified approach. Our customers continue to buy more than one product and once unified, we're able to drive price in the given the value we provide... Now we've mapped out every single account where the opportunities are when they're -- not when their RFPs come up, but when they -- when the next expiry of a contract happens. And then we have so much more data now to build off of and say, okay, they have Brink, -- they have data central, they have MENU, here's the opportunity for payments and here's how that picture works. So it's really a focus on cross-sell... Our operator solutions of Brink and payments has become a dynamic combination in the attachment of Data Central and soon MENU comes next... As we look and see decelerating growth around the sector, we think our ability to maintain our growth rates is differentiated, driven by the unified approach.

This is driven by producing a superior ROI, and also because the Unified Experience generates tons of data (Q4CC):

To the unified experience offering, PAR has massive amounts of real-time actionable data for customers that provides the foundation for machine learning-based personalization and analytics. This includes transactional data for Brink, customer identity data for Punchh and employee inventory data for Data Central.

The company has switched R&D expenditures away from dealing with existing products to generating new ones and we should see additions this year, especially in Payments.

The company also signed its first two big deals opening up a whole new segment, Table Services . While it varies considerably, on average this is a really high ARPU product, even at low-end chains it adds meaningfully to ARPU (Q4CC):

Table service clients in general, pay higher monthly subscription rates as they require more terminals and functionality than our QSR customers and will drive our continued ARPU expansion.

And what's more, these deals also came with payments and back office attached, payments will also produce higher ARPU under Table Services (even if it needs to scale in order to generate higher margins). They will start rolling these customers out at the end of H1/23.

The company received RPFs in the past when they weren't ready but given that these first two customers are well-known chains, management expects these RPFs to come back. They already have a pipeline of smaller chains.

The company continues to sign up new customers and activate new stores:

- Guest Engagement: 2.8K new store activations with 69.9K active sites.

- Operator Solutions: 1.2K new store activations with 19.5K active sites.

- Back Office: 350 new store activations with 7K active sites.

Punchh signed several new customers in Q4, including a 3K restaurant fast-casual chain, and went live with 10 new logos.

Back office signed a popular casual dining wings brand as a new logo, displacing the market leader for labor scheduling. It also went live with 7 new logos in the quarter and continues to sell to existing Brink and Punchh customers.

Payments was added by 17 new customers in Q4, including at a 3K fast-casual chain, 80% of new Brink deals have payments attached, which is much higher than management expected when payments were launched.

M&A is another growth avenue with the last two acquisitions, Punchh (loyalty and guest engagement, April/21) and Menu (digital ordering, July/22), and the smaller Drive-Thru (March/22).

Management has especially high hopes for Swiss-based Menu, which it raves about as a state-of-the-art tech and they spend lots of time comparing solutions with Menu coming out on top. Menu can be introduced to lots of their US-based customers.

The environment for additional M&A deals is very good with valuations coming down a lot and the IPO market much more difficult.

Financials

Some historical context, from the 10-K :

PAR 10-K

Some highlights this year:

{kind=link}

There are three trends:

- There is solid revenue growth, the most important metric is ARR (annual recurring revenue) which increased 26.4% to $111.4M.

- Gross margin is increasing on improved hosting utilization, process improvements within support services, and pricing (see below). Management also argues that Menu and payments, which generate lower gross margins, can increase to reach the company average in the coming years on scale economies.

- OpEx (ex-acquisitions) will be flat next year (as it was flat in 2022 if one takes out the acquisitions).

PAR 10-K

ARR includes subscription services and hardware support contracts within professional services. For subscription services (their recurring revenue):

{kind=link}

The three trends conspire to rapidly reduce net losses in 2023. Still, there is a considerable loss of $13.5M in Q4 (down from $25.6M in Q4/21) so improvements are required. While improving, there is also still quite a bit of cash bleed:

Management expects the trends (20%-30% ARR growth, expanding gross margins, flat OpEx) to continue so we should see further improvements.

There is some softness in Punchh in H1/23 because of caution on inflation and price elasticity. but that should turn around in H2/23 according to talks management had with customers and other parts like back office are likely to accelerate growth.

Also, there are some supply chain issues that limit the growth of payment services but management expects these to clear "later this year."

Menu was integrated with Brink in Q4, which will allow the company to start targeting existing customers aggressively.

The company still has $70.3M in cash, $40.3M in short-term investments, $60M in AR and $37.6M in inventories (which they aim to reduce by another $3M-$5M in H1/23), so they are not under cash constraints.

Even if that should happen, which seems unlikely to us, they can sell their legacy government business, which had a pretty good quarter growing 42.1% to $26.7M with a huge 71% increase in the backlog to $334M.

There was temporary pressure on the gross margin in the government business to just 4.3% on temporary factors and management expects that to revert to the normal 6-8% range this year.

Valuation

There are also 1M in outstanding options and $7.6M of outstanding RSUs for a total market cap of $1B (at $35 per share).

The company also has $389.2M in long-term debt, most of it ($265M) consisting of the 1.5% 2027 convertible notes and $120M of the 2.875% 2026 convertible notes.

With cash at $70.3M and a further $40.3M in short-term investments, the EV is $1.28B. That seems to result in a high 11x EV/S on the ARR ($111.4M), but keep in mind they have non-ARR generating businesses that are actually considerably bigger:

- Hardware business (POS terminals) $114.4M

- Government business $93.4M

- Professional services $50.4M

Total FY22 revenue is $355.8M which yields an EV/S multiple of 3.6x. Revenues are expected to rise further to $431.6M or an FY23 EV/S of just under 3x.

Analysts still expect considerable losses this year (64 cents per share, down from $1.13 in FY22). In the previous quarter's earnings PR , management predicted being cash flow positive exiting FY23.

Conclusion

We see plenty to like:

- State-of-the-art software with a large TAM to go after with Menu and Payments as recent additions creating plenty of cross-selling opportunities and Table Services as a new significant segment.

- Rising trends in ARR and ARPU continued even during rough periods

- While there are still considerable losses and cash bleed, growth, gross margin expansion, and stable OpEx will produce significant improvements with cash flow breakeven coming in sight this year.

- The company can sell its government business to concentrate on its restaurant business and eliminate some of the debt.

- Given how the company survived the pandemic, it's hard to see a significant risk in the form of a scenario where ARR stops growing.

For further details see:

PAR Technology Looks Set To Have Another Good Year