PGRE - Paramount Group: Key Tenancy Risk Relating To Fallout Of SVB Failure

2023-03-13 11:57:37 ET

Summary

- Paramount Group owns and operates Class-A office properties in two primary markets, New York and San Francisco.

- The company is reporting promising strength in their largest market, New York, which represents more than 70% of their business.

- Continued weakness in the West Coast, however, is holding back overall results. The status of one large-block expiration in the region also adds an additional level of uncertainty.

- In addition to near-term expirations, the company also faces heightened near-term tenancy risk relating to the potential fallout of the SVB failure.

- For investors, it is best to err on the side of caution until there is further clarity on both their leasing efforts and the status of their key tenants.

Paramount Group ( PGRE ) has an interest in Class-A office properties in select central business district submarkets of New York and San Francisco.

Their operations are more concentrated in the New York market. The region, for example, represents over 70% of their business. Furthermore, they are dependent on a few key buildings and a select group of tenants.

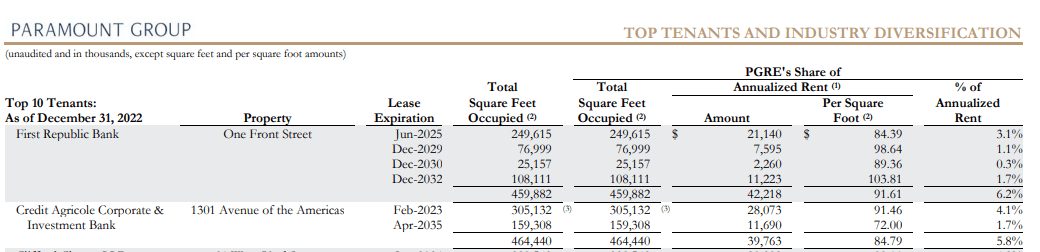

Their top tenant is First Republic Bank ( FRC ), which currently represents 6.2% of total annualized rent (“ALR"). The concentration here is concerning , given the possible fallout from the recent collapse of SVB Financial Group ( SIVB ). Another concern is the recent onboarding of SVB Securities in space previously vacated by Credit Agricole.

Q4FY22 Investor Presentation - Partial Summary Of Top 10 Tenants

{kind=link}

For investors seeking new positioning, PGRE’s share price appears dislocated to the underlying value of their properties. However, a significant risk premium is necessary due to recent events. The exposure to headline tenants, such as First Republic and SVB Securities, is an untimely risk on top of an already uncertain leasing outlook in their West Coast markets. Though it may not make sense for many to sell at current pricing, considering how far shares have already fallen, the stock is at heightened risk of further declines due to the threat of cascading aftershocks from the failure of SIVB.

Recent Performance and Current Portfolio Metrics

In the final quarter of fiscal 2022, PGRE reported core funds from operations (“FFO”) of $0.25/share. This was slightly above both consensus estimates and the midpoint of their guidance. For the year, core FFO came in at $0.98/share, representing 6.5% YOY growth.

In the same-store portfolio, they reported YOY cash basis growth of 1.7%. The results here were led by their New York portfolio, which grew 6.9%. The strength on the East Coast, however, was largely offset by weakness in their San Francisco market, which lost 270 basis points (“bps”) of occupancy and turned in same-store losses of 8.7%.

Overall, year-end same-store portfolio-wide leased occupancy held at 91.3%. This is down 10bps from the prior quarter but up 70bps YOY. In their New York market, occupancy grew 180bps from last year to 92.1%. Furthermore, since their lows in the second quarter of 2021, occupancy in the market has improved by 560bps. This is even as the availability rate was up 50bps over the same period.

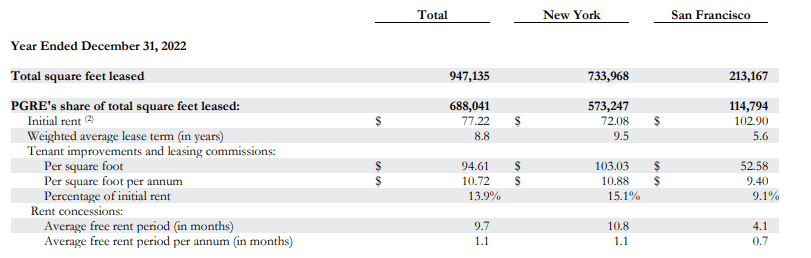

During the quarter, their New York market captured 74% of the total leasing volume of 205.5K SF. Given that this market represents over 70% of their business, weighted activity in this region isn’t unexpected. For the year, in fact, New York accounted for nearly 80% of total leasing volume of 947K SF.

Looking ahead to 2023, management sees core FFO tracking in the range of $0.88 to $0.94/share or $0.91/share at the midpoint. This represents about a 7% decline from 2022, due primarily to expected weakness in same-store cash NOI growth, which is expected to create a $0.08/share headwind to results. Lease expirations by Credit Agricole and Uber (UBER) would be the two prime drivers of the same-store weakness.

Higher interest expense of $0.05/share is also expected to hit earnings in 2023. Partially offsetting these negatives, however, are lease commencements, which is expected to add $0.04/share, and a lower share count from their recent repurchasing activity, which is expected to create a benefit of $0.03/share.

The growth targets would be in conjunction with leasing targets of between 600K SF and 900K SF and a same-store leased occupancy rate between 90.8% and 91.8% or 91.3% at the midpoint.

The Bull View

PGRE logged nearly 950K SF of leasing for the full 2022 fiscal year. This came in above the midpoint of their most recent guidance range, despite a challenging market environment. Strength in their New York market is also promising. Total leasing volume in the region, for example, was above the annual market total over the last five years.

The company also made headway in addressing their large-block vacancies, such as the pre-leasing of over 50% the space vacated by Credit Agricole.

February 2023 Investor Presentation - Snapshot Of Large-Block Vacancies

While their expiration schedule is top-heavy to more recent periods, the expiration profile in their largest market, New York, which represents over 70% of their business, is more manageable, at 3.1% through year end.

February 2023 Investor Presentation - Lease Expiration Schedule

And though weakness in their San Francisco market has proved sticky, the upside potential is sizeable. Initial rents are about $30/SF higher than in their New York market. In addition, the market commands a lower degree of concessions. With occupancy down 270bps YOY, there is a sizeable opportunity for improvement, which should figure to be a key driver of earnings in future periods.

Q4FY22 Investor Supplement - Breakout Of Annual Leasing Activity By Market

{kind=link}

PGRE also is maintaining a sizeable liquidity position of +$1.2B, about +$450M of which is held in cash. Based on the current share count, that represents about $2/share in cash. At current trading levels, this indicates their remaining operations are valued at less than $3/share. This seems widely out of line, considering the implied cap rate on their operating results.

The company has taken advantage of this market dislocation by opportunistically repurchasing their shares. In addition, key insiders have also increased their stake within the company in recent periods, further validating the value potential in the shares.

The Bear View

Though PGRE has made progress on their leasing efforts, their upcoming expirations are still sizeable. In the San Francisco market, for example, 9.3% at share is expiring through year end. While most of this is related to the expiration of the Uber space in July 2023, the company hasn’t made any meaningful progress on backfilling the space.

Though inquiries on the space is a positive spin, it does little to assuage wary investors, especially since there is just a few months left before the known vacate.

In addition to the Uber space, one must also reassess their recent leasing results on Credit Agricole’s space. Over the final two quarters in 2022, management successfully pre-leased over 50% of the 300K SF of space vacated by the company.

But the majority of this leasing came from two key tenants, one of which was SVB Securities. While there are reports of discussions surrounding a buyback, exposure to the tenant following the collapse of SIVB creates undue uncertainty in an already uncertain leasing environment.

Q4FY22 Investor Supplement - Highlight Of Key Tenant Within A Top Operating Asset

{kind=link}

And even more concerning is their exposure to FRC, which is their single largest tenant. In recent days, the stock has exhibited notable volatility resulting from the aftershocks of the SIVB collapse. The loss of FRC, should they face a similar fate as SIVB, would prove material for PGRE.

The company also has near-term maturities that will need to be addressed. +$200M at share is maturing in 2023 and +$478M at share matures in 2024. On top of this, nearly 15% of their total debt stack is variable rate at a current weighted average interest rate of 5.7%.

Their dividend payout that is currently yielding nearly 6.5% offers one draw to income-focused investors. Solid coverage levels also provides some assurance of continuity. One cannot, however, rule out an eventual cut, due primarily to either an exercise in caution by the Board, given their current leasing environment, or for taxable income purposes.

Final Thoughts

PGRE’s top market, New York, held up strongly in 2022. The region experienced strong occupancy gains on the back of robust leasing volumes. Additionally, the company made significant progress in de-risking their largest expiration in 2023. And despite the challenging operating environment, management still expects overall 2023 occupancy levels to hold flat in relation to 2022.

At just 5.3x forward FFO, shares trade at a significant discount to their underlying value. For perspective, the company has about +$450M in cash on hand, which, itself, represents about $2/share, meaning their remaining operations are valued at less than $3/share. This is despite an unencumbered asset pool that generated over +$60M in net operating income in 2023.

The company has pounced on the dislocation through opportunistic share buybacks, as well as select insider purchases.

For some investors, the upside potential may outweigh the risks. For others, new initiation for the upside wouldn’t be enough to overcome the highly uncertain outlook.

PGRE has significant near-term expirations, for example. The fact that one is in their struggling West Coast market doesn’t provide confidence, especially since there hasn’t been any measurable progress on it.

In addition, the company recently backfilled a large quantity of space at another large-block vacancy. But one of the two tenants that came in was SVB Securities. This creates another uncertainty to their portfolio, which should already be under greater scrutiny due to their overweight exposure to First Republic Bank.

And since their operations are highly concentrated in select properties and regions, these uncertainties weigh more heavily than if their operations were more diversified. Though the upside potential is there, investors would be better off playing it safe.

For further details see:

Paramount Group: Key Tenancy Risk Relating To Fallout Of SVB Failure