PGRE - Paramount Group: More Progress Needed On Upcoming Expirations

Summary

- Paramount Group, Inc. has an interest in a targeted portfolio of Class A office properties in select central business districts in New York and San Francisco.

- The company has favorable exposure to the Legal and Financial sectors, two industries with higher return rates to in-person office work.

- This is offset by their elevated tenant and building concentration and their upcoming expirations in 2023.

- While the company has made measurable progress in addressing their near-term expirations, more progress is needed.

Paramount Group, Inc. ( PGRE ) is a New York City-based real estate investment trust (“REIT”) that has an interest in a targeted portfolio of Class A office properties located in select central business districts in New York and San Francisco.

Overall, the company’s portfolio is 91.4% leased with an average lease term of 6.4 years. Most recently in Q3FY22, however, signings have been completed at a weighted average term of 12.5 years. This is indicative of the continuing demand for quality office space, despite the rise in the number of companies downsizing physical spacing needs.

The company also has favorable exposure to the Legal and Financial sectors, who together represent over 40% of annualized rents. This is notable since the two generally have higher return rates to in-person work.

This is offset in part by their exposure to Tech, which is their third largest industry served and a sector that is generally more accommodative to permanent offsite working arrangements. In addition to tech exposure, the company is also exposed to tenant and building concentration risk.

A few upcoming expirations in 2023 amplify this concentration risk and present uncertainties for prospective investors. While the company has made measurable progress in addressing a sizeable portion of the near-term expirations, there is still work to be done. It may be best, therefore, to remain neutral until there is further clarity on the status of these ongoing negotiations.

Recent Performance

In the most recent quarter ended September 30, 2022, PGRE completed approximately 290K square feet (“SF”) of total leasing. This was about 40K SF more than what they signed in Q2 and 90K more than Q1. YTD through September, the company has now signed a total of over 740K SF of space.

Of their two operating markets, New York and San Francisco, New York accounts for about 80% of total leasing activity. In the current quarter, though, the market represented over 90% of the total activity.

In Midtown, New York, quarterly activity was 4.5% above their pre-pandemic 5-year quarterly average and was the second highest quarterly leasing total since Q4 of 2019.

This has been led by an acceleration of workers returning to the office, particularly in the Financial Services sector, a key industry in PGRE’s total operating portfolio that represents about 20% of their annualized rent. In the current quarter, the sector represented about 46% of the total activity in Midtown. This far exceeds the 32% share of occupancy that they currently represent.

In addition, the market logged another quarter of positive net absorption, the fourth such time in the past five quarters that this has occurred.

While their San Francisco market continues to underperform when stacked against New York, the market is, however, benefitting from tenants seeking quality office space. This is evidenced on renewals on second-generation space, where rents have increased about 14.7% and 1.6% on a GAAP and cash basis, respectively. This compares favorably to their New York market, which has seen rents increase just 1.5% on a GAAP basis and a decline of 11.6% from a cash standpoint.

In both markets, upcoming expirations are manageable in the near-medium term, with limited rollovers in Q4 and about 6.4% and 7.8% of annualized rent expiring per annum through 2024 in New York and San Francisco, respectively.

Notably, PGRE made significant headway in addressing the expiration of their lease with Credit Agricole, their second largest tenant who is a primary occupant of 1301 Avenue of the Americas, a building that represents nearly 20% of their gross asset value.

As it was, 305K SF was set to expire in February of 2023. But during Q3, the company signed on law firm O’Melveny & Myers to 142K SF of space that would have been vacated by Credit Agricole. This satisfied about 47% of the total upcoming expiration.

While the progress is certainly a positive, the company still needs to address over 500K SF of either upcoming expirations or, in the case of Barclays ( BCS ), space that is already vacant.

November 2022 Investor Presentation - Snapshot Of Notable Upcoming Expirations

Liquidity And Debt Profile

PGRE benefits from having ample liquidity. At present, the company has +$1.3B in total liquidity, comprised of +$508M of cash on hand and +$750M of availability on their revolving credit facility.

They also have generated +$174M in operating cash through nine months of the year. This has been enough to fully cover their investing activities during the year.

Their debt profile is also manageable. As a percentage of total enterprise value, net debt stands at 45%. Similarly, total debt as percentage of assets was 44% at quarter end. This is comfortably below their covenant requirement of 60%.

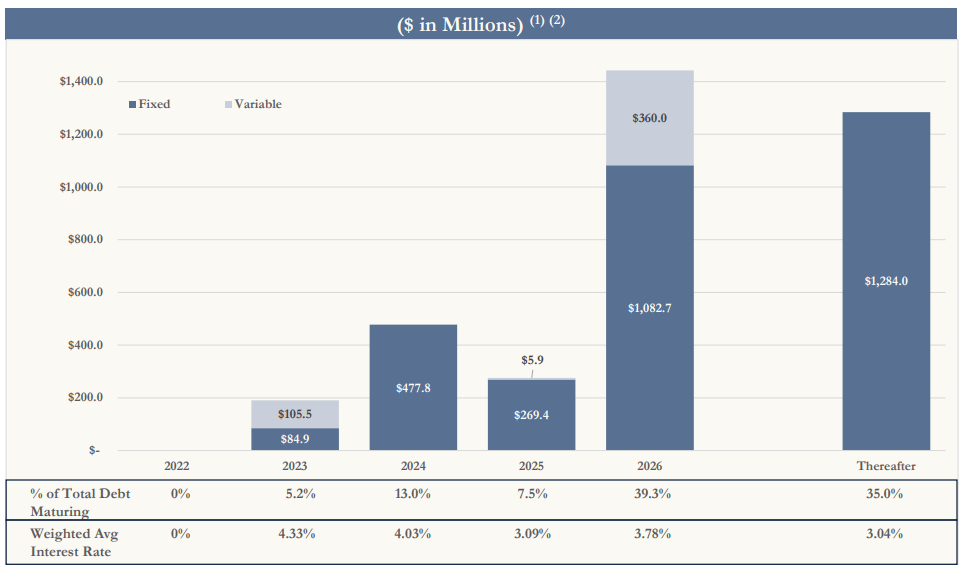

In addition, total debt composition is weighted 87.2% to fixed-rate holdings, and the company has limited near-term maturities. This minimizes their exposure to both interest rate and refinancing-related risks.

November 2022 Investor Presentation - Debt Maturity Schedule

{kind=link}

Dividend Safety

PGRE currently provides a quarterly dividend payout of $0.0775/share, which represents an annualized yield of 5.2% at current pricing. This is a lower yield than what is offered by other office-related names. Shares in Brandywine Realty Trust ( BDN ), for example, are currently offering a yield of over 12%.

But upside does exist, as the current payout is still 29% below the $0.10/share quarterly payment provided through the first three quarters of 2020. This is even after having been increased 10.7% in the current year. If the payout were in fact to return to its former level, the yield on cost would be approximately 6.7%.

And at just 32% of core funds from operations (“FFO”) and about 46% of funds available for distribution (“FAD”), PGRE does have the safety and capacity for further increases. And even when considering their repurchasing activity, the company still has about +$105M left over after paying out dividends to their common shareholders with operating cash flows. This excess is about $20M over their current investing activities.

While a dividend cut can’t be ruled out, especially if the company were to face vacancy headwinds from their large-block tenants, the payout appears safe at present based on current coverage levels and cash generation through nine months of 2022.

Takeaway

PGRE continues to make headway in leasing, especially in their New York market, where return-to-office trends are further along than in their San Francisco market, a market that is more heavily tilted towards the Tech sector as opposed to the more diversified makeup in New York that includes the more office-centric Financial and Legal industries.

Though the company notably addressed 47% of their upcoming Credit Agricole expiration, 53% of the space still needs to be satisfied. In addition, 234K SF of space occupied by Uber Technologies ( UBER ) is a known vacate in Mid-2023.

Though management did note that there is positive activity on the space, prospective investors will need to stay abreast of any further developments regarding these expirations on their Q4 earnings release.

Uncertainties pertaining to the upcoming expirations are counteracted by the company’s strong liquidity position and their conservative dividend payout that remains adequately covered by available funds.

In addition, at just 6x forward FFO, shares appear heavily discounted, especially when taking into consideration the $12/share buyout offer the company received earlier in the year.

Still, given PGRE’s relatively small portfolio that is tenant and building concentrated, progress surrounding their three large-block vacancies is of paramount importance. Until there is further clarity on the status of these expirations, investors may be best positioned on the sidelines.

For further details see:

Paramount Group: More Progress Needed On Upcoming Expirations