GPRK - Parex Resources: A Best In Class Debt Free Bet On Colombian Oil

Summary

- Overblown perception of risk leaves Parex heavily undervalued.

- Best-in-class debt-free intermediate oil producer.

- Solid portfolio of exploration and development assets.

Rising oil price volatility and recent tax reforms in Colombia coupled with the government's plans to end contracting for hydrocarbon exploration have put the spotlight firmly on the Andean country's energy patch. There are fears that recent tax hikes for the hydrocarbon sector coupled with rising violence have made Colombia a risky and unprofitable jurisdiction in which to operate. This along with softer oil prices has caused the market value of drillers operating in Colombia to tumble creating opportunities for more risk tolerant investors. One intermediate upstream oil producer which stands out is Parex Resources ( PARXF )( PXT:CA ), long considered by many pundits to be the best intermediate upstream oil producer operating in Colombia. I last covered Parex in July 2020 at the height of the pandemic and much has changed since then, making now the time to review the driller's outlook, particularly considering recent developments in Colombia.

Company overview

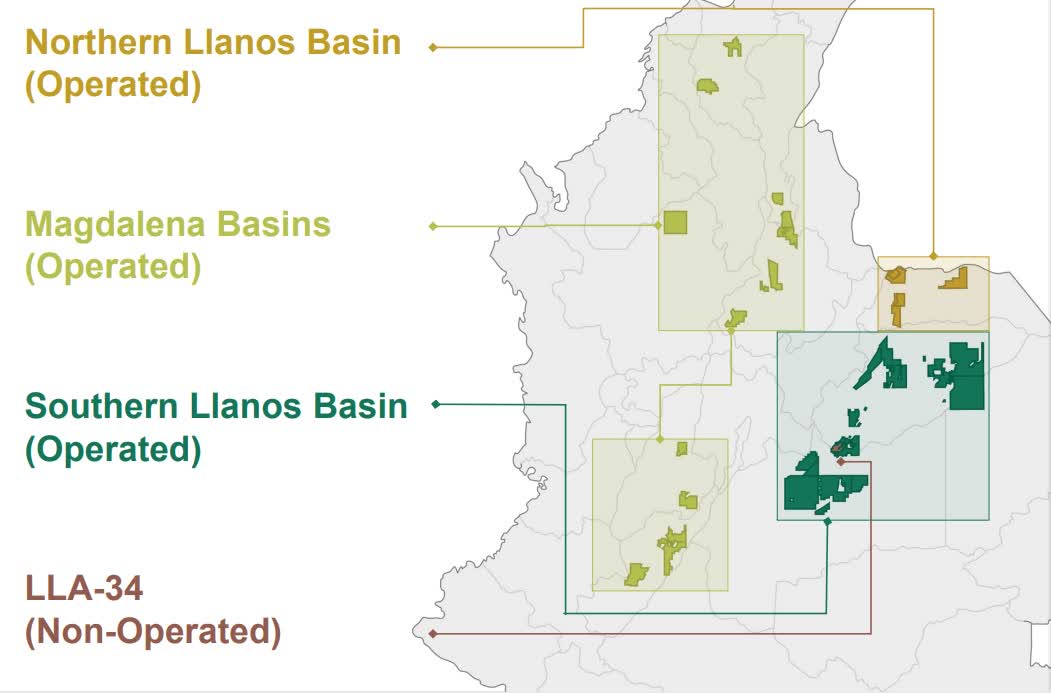

Parex, which is Colombia's largest oil producer after national oil company Ecopetrol ( EC ), holds 5.8 million acres in Colombia composed of 42 blocks. The company operates 41 of those blocks with one Block LLA-34 being non-operated.

Parex Oil Properties (Parex Resources)

{kind=link}

Source: Parex Presentation Capital Markets Day 6 December 2022.

Block LLA-34 located in the Llanos Basin in which Parex owns a 55% interest is operated by 45% partner Chilean driller GeoPark ( GPRK ). That asset is responsible for most of Parex's oil production, with it accounting for 64% of oil pumped during the third quarter 2022. To offset the risks associated with most of oil production coming from a non-operated asset Parex is investing heavily in developing its operated blocks. The company's 2023 budget allocates 75% of expenditures, forecast to be $425 million to $475 million or $450 million at the midpoint, to Parex's operated assets. That capex will be used to drill 65 wells during 2023. There are 35 to 40 wells planned for LLA-34, another 13 to 15 for the 100% owned and operated Cabrestero Block with the remainder of wells to be drilled across LLA-26/81, LLA-122, VIM-43, Arauca and Capachos Blocks.

Parex's 41 operated blocks hold considerable exploration upside with all of them located in tested oil basins that contain existing producing operations. The company plans to invest $45 million during 2023 on an exploration well drilling campaign for the Arauca, VIM-43 and LLA-122 blocks. The 100% owned Cabrestero and 50% controlled Capachos Blocks will drive Parex's production growth. Both are operated by the driller and primed to deliver additional production as operational wells are drilled and developed.

Parex's properties in Colombia hold net proven reserves, otherwise called 1P reserves, of just under 107 million barrels of oil equivalent and 59 million barrels of probable reserves. That gives the driller total net proven and probable reserves, also known as 2P reserves, of nearly 166 million barrels. Parex's 2P reserves have a life of nine years at the current rate of average daily production which was 50,000 barrels per day for the third quarter 2022. The driller had an impressive 125% 2P reserve replacement rate for 2021, indicating that with a ratio of greater than 100% Parex is growing its reserves and not only replacing the crude oil produced. Much of that reserve growth came from the Arauca and Capachos Blocks in the northern Llanos Basin, which are 50% owned by Parex with the remainder held by Ecopetrol. It is Parex's oil reserves which give the company its value.

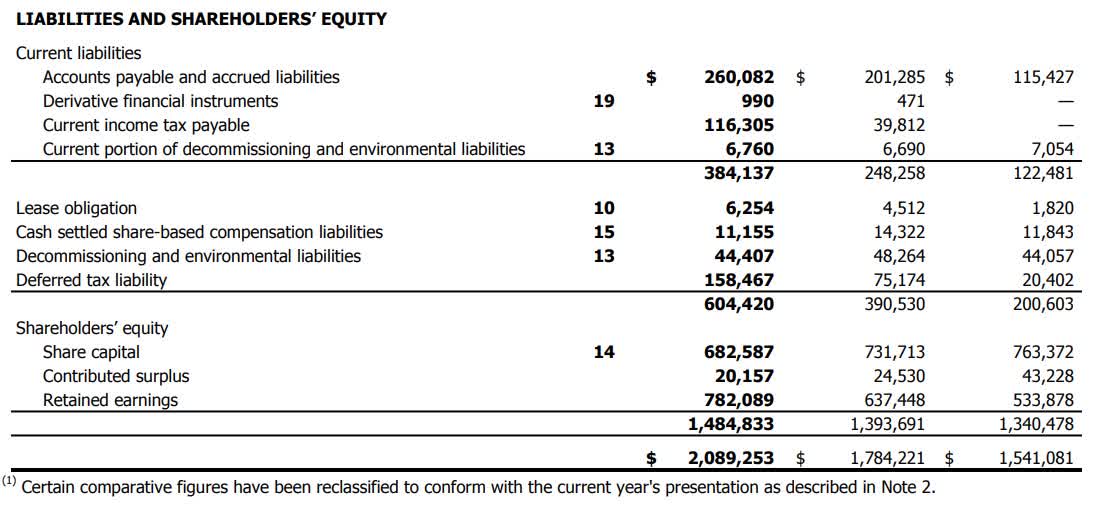

Importantly, Parex is debt free giving it a considerable advantage when compared to more indebted peers, especially during difficult operating environments caused by sharply lower oil prices. Current liabilities totaled $260 million at the end of the third quarter 2022 while long-term liabilities composed of lease obligations ($6.2 million), share based compensation payments ($11 million), Decommissioning and environmental liabilities ($44.4 million) and deferred tax liability ($158.5 million) totaled a modest $220.3 million.

Balance sheet liabilities (Parex Resources)

{kind=link}

Source: Parex Financial Statements September 30, 2022.

This gives Parex considerable financial flexibility and has been a key reason for the driller's solid performance and ability to deliver value for shareholders for a decade. It removes much of the risk associated with investing in intermediate upstream oil companies which were badly buffeted by a prolong period of sharply weaker prices that saw many heavily indebted companies face bankruptcy.

Finding Parex's fair value

The industry accepted means of determining the indicative fair value of an upstream oil producer is to calculate the company's net asset value or NAV per share using the after-tax net present value with a 10% discount rate applied (NPV-10) of its 2P reserves. Based on the after-tax NPV-10 for Parex's 1P reserves the driller has a NAV of $19.91 per share as the table below shows.

NAV Valuation (Author)

Source: Parex Annual Information Form 2021, September 30, 2022 Financial Statements and authors own calculations.

With Parex's pink sheets listing trading at $17.15 at the time of writing the after-tax 1P NAV per share indicates that the driller is 16% undervalued by the market. That is not a large premium to justify that Parex is undervalued particularly when elevated geopolitical and regulatory risks in Colombia are accounted for. It is worth noting that the NAV was calculated using the after-tax value of Parex's oil reserves and a conservative price deck was used with a 10-year average Brent price of $76 per barrel which is roughly $10 per barrel less than the current market price. Any notable increase in the Brent price, which is the benchmark for Colombia crude oil grades, will substantially boost the value of Parex's after-tax 1P NPV-10.

Nevertheless, this is not the industry accepted valuation methodology for an intermediate upstream oil producer, with the after-tax 2P NAV per share being the recognized approach.

NAV Valuation (Author)

Source: Parex Annual Information Form 2021, September 30, 2022 Financial Statements and authors own calculations.

When it is considered that Parex pink sheet stock is selling for $17.15 that fair value estimate indicates that the driller is undervalued by 64%, indicating that there is not only considerable upside ahead but also a large margin of safety. That is further supported by the conservative price deck used to calculate the after-tax NPV-10 of Parex's oil reserves, with a 10-year average Brent price of $76 a barrel, as well as the potential for high proven and probable reserves.

Parex reported a 2021 2P reserve replacement ratio of 125% indicating that proven and probable reserves grew, thereby bolstering their value compared to a year earlier. According to the driller's 2021 independent reserves assessment gross 2P reserves grew by 11% per share, Parex's reserves will have expanded during 2022 and will keep growing thereafter because of its credible drilling and development program. Any expansion in the intermediate oil producer's reserves will boost Parex's NPV-10 and its NAV per share, as will higher Brent pricing and an improved outlook for oil prices since the end of the pandemic.

Solid exploration and development plan

Parex is focused on expanding its acreage while simultaneously expanding its oil reserves and production. At $80 per barrel Brent Parex plans to spend $145 million on exploration drilling between 2023 and 2025 on 15 exploration prospects. This exploration program during 2023 will be funded by a $45 million investment with the primary objectives being:

- A near field exploration well in the Capachos Block where Parex is the operator and holds a 50% working interest, with the remaining half held by Colombia's national oil company Ecopetrol during 2023.

- The Arauca-8 wildcat well in the Arauca Block where the driller is also the operator and has a 50% working interest.

- The Arantes wildcat well on Block LLA-122 in the Llanos foothills where Parex is the operator and holds a 50% interest with the remainder held by Ecopetrol.

Parex is also investing $270 million in a development plan during 2023 with injection, appraisal and production well on the Arauca, Capachos, Cabestro, LLA-26, LLA-34, LLA-80 and LLA-40 blocks. That tremendous investment combined with a rising tempo of operations and Parex's drilling success rate points to a solid reserve replacement ratio and reserve growth during 2023.

Geopolitical risks likely not as severe as believed

Among the many headwinds weighing heavily on Parex and its peers operating in Colombia was the decision by the strife-torn country's first leftist president to hike taxes for extractive industries. This saw the national government in Bogota implement an incremental levy on oil companies which increase as the Brent price rises. The levy starts at 5% which is payable when Brent is selling for $67.30 to $75 per barrel then rises to 10% at $75 to $82.20 a barrel with a 15% levy imposed when the price exceeds $82.20 per barrel. Base royalty payments have also been removed from deductions that can be applied when calculating income taxes payable in Colombia.

Those measures sparked considerable controversy among industry bodies and thinktanks in Colombia. Fedesarollo, a Colombian economic thinktank, claimed they nearly doubled the effective tax rate for the oil industry from 36% to 70.3%. Nevertheless, the impact does not appear to be as severe as initially thought, with Parex's calculations indicating that with Brent at $80 per barrel the company's effective tax rate increases from 22% for 2022 to 23% during 2023. If Brent averages $90 per barrel, then the effective 203 tax rate will be 38% or 15% greater than before the tax amendments became effective while the effective rate rises to 39% at $100 a barrel. For these reasons, the impact of the tax reforms is not as significant as originally thought, as Parex's own calculations demonstrate.

President Gustavo Petro's plans to ban contracting for hydrocarbon exploration are also weighing on Colombia's oil industry and drillers such as Parex. The government has made it abundantly clear that existing production sharing agreements will be respected, and there are even signs that the Petro administration may even ease its approach to Colombia's petroleum industry. Crude oil is an important economic driver export responsible for around a third of exports by value, a fifth of government income and 3% of gross domestic product. There is also considerable pressure on the Petro administration to boost spending, notably on education, health and social programs to alleviate poverty, while reining in massive budget deficits which ballooned out during the pandemic as well as after. These are reasons driving Petro's decision to hike taxes for Colombia's oil industry, with increased revenues covering a large spending shortfall.

Another specific risk for Parex is growing insecurity in Colombia. Violent crime including kidnapping and extortion are rising once again as are the activities of illegal armed groups, notably the National Liberation Army , known by its Spanish initials ELN, and FARC dissidents. The sabotage of pipelines, wellheads and other industry infrastructure is a persistent problem as is ever growing petroleum theft, primarily conducted by applying illegal taps to oil pipelines. There is also growing social unrest regarding Colombia's oil industry which is spurring court action against various operations and community protests. While this is not as serious as Peru or Ecuador it can still impact industry operations and production. I have discussed those risks at length in my earlier article on Frontera Energy (FEC:CA) Colombia's third largest oil producer behind Ecopetrol and Parex.

Conclusion

Parex's indicative fair-value is the after-tax NAV of its proven and probable oil reserves, which at $28.14 per share indicates there is potential upside of 64% with a decent margin of safety. While that is not as high as Frontera or Gran Tiera Energy where their after-tax 2P NAVs are 148% and 268% higher than their current market price it does indicate that Parex is indeed undervalued by the market. That margin of safety is enhanced by the conservative price deck used to calculate Parex's NPV-10 with a 10-year average Brent price of $76 per barrel, well below the $86 per barrel at the time of writing. The risk associated with investing in Parex is further reduced by the fact that the company is essentially debt free with no major long-term liabilities other than decommissioning and environmental liabilities, deferred tax payments, and lease obligations. It may take time for Parex to realize the indicative fair value calculated because of what I see as an overblown sense of risk associated with operating in Colombia, but the driller is a best-in-class investment in comparison to its direct peers.

*Important note: While Parex is not listed on a U.S. exchange, the company's stock is highly liquid with the driller listed on the Toronto Stock Exchange with a market cap of C$2.52 billion and an average daily trading volume of around 567,000 shares.

For further details see:

Parex Resources: A Best In Class Debt Free Bet On Colombian Oil