PARXF - Parex Resources: Deeply Undervalued And Remains A Buy (Rating Upgrade)

2023-04-27 06:15:34 ET

Summary

- The heightened geopolitical risk associated with operating in Colombia is weighing on Parex's market value.

- Parex has mapped out a solid growth path and holds quality onshore oil assets.

- The company's solid financial position and long-term debt-free balance sheet make it an extremely attractive investment.

- Parex has a proven history of growing oil reserves and production.

- Parex is heavily undervalued because of the market's overblown perception of risk.

The strife-torn South American country of Colombia continues to garner a leery outlook from energy investors and deservedly so given the sharp increase in uncertainty surrounding the outlook for the country's oil patch. While risks certainly abound so do opportunities and one such prospect is Canadian small-cap intermediate oil producer Parex Resources (PARXF) (PXT:CA). I last covered the intermediate driller on January 25, 2023 , since then the company announced some solid 2022 numbers, confirmed its 2023 outlook and hiked the dividend by 50% giving the company a juicy 5.5% yield. Despite the various political, regulatory and security headwinds buffeting energy companies operating in Colombia there are signs that Parex is not only heavily undervalued but remains a best-in-class operator.

Latest results

For 2022, Parex reported yet another impressive annual result. Revenue surged by 45.6% year over year to $1.3 billion and on the back of that strong increase the driller reported record funds flow provided by operations of $725 million which was a notable 26% increase compared to a year earlier. This saw Parex announce record annual net income of $611 million or just over double the $303 million reported for 2021. Those strong results were the outcome of a combination of higher oil prices with Brent averaging $99 per barrel over the course of 2022 and Parex's focus on maintaining the efficiency of its operations.

Parex's efficient operations saw it report a notable 2022 operating netback of $59.06 per barrel despite higher production and transportation expenses which rose 8% and 29% year over year. Transportation expenses frequently fluctuate primarily because pipeline outages force Parex to truck the crude oil produced, at a far higher cost, to the Caribbean port of Coveñas where it can be shipped to international markets. This is a key risk associated with operating in Colombia where pipelines, which are the only cost-effective means of shipping crude in bulk through the rough terrain, are the targets of frequent sabotage by various illegal armed groups.

Aside from materially higher Brent prices during 2022 it is Parex's ability to consistently grow production that was another key driver behind those strong results. Average annual 2022 production of 52,049 barrels per day represents an impressive 11% increase over 2021. That solid growth can be attributed to Parex's quality onshore Colombian oil acreage and drilling program. The driller has been steadily expanding its onshore acreage in Colombia since 2011 adding 18 blocks during the country's 2021 bid round. Parex now holds 40 onshore blocks comprised of 5.8 million acres making it Colombia's largest independent oil acreage holder.

This was also responsible for Parex's all-important oil reserves expanding during 2022 which has given the driller's after-tax net asset value, or NAV, a solid boost. Parex's 1P reserves at the end of 2022 grew 4% year over year to 131.7 million barrels while 2P reserves increased 1% to 200.7 million barrels which are 93.6% weighted to crude oil with heavy oil making up 68% of the company's total 2P reserves. The key Colombian petroleum grade Vasconia, which is a blend of various heavy oils has an API of 24.3 degrees and 0.83% sulfur content, trades at a discount typically of $1 to $2 per barrel less than the international Brent price.

Most of Parex's oil reserves, 57% of total 2P reserves, are contained in its flagship LLA-34 Block located in the Llanos Basin in which Parex holds a 55% working interest with the remainder held by GeoPark (GPRK), which is also the operator. LLA-34 is also responsible for 62.5% of Parex's oil output. For these reasons, as a non-operated block, it creates a risk, albeit at the lower end of the scale, for Parex because the company is dependent upon GeoPark being able to successfully execute its exploration and development program.

Parex has a long history of expanding its oil reserves. Last year, 2022, was the 12th consecutive year of reserves growth and this combined with a higher forecast 10-year average Brent price of $84.30 per barrel gave the after-tax NPV-10 of Parex's reserves a healthy boost. The after-tax NPV-10 for Parex's 1P reserves at the end of 2022 grew 9% year over year to $2.5 billion while the after-tax 2P NPV-10 rose 13% to $3.4 billion.

This coupled with the company reducing its share count through an ongoing buyback scheme saw the weighted average number of outstanding diluted shares at the end of December 2022 total 113.7 million a 9.5% reduction compared to 2021. For the first month of 2023, Parex announced it had purchased another one million shares reducing the diluted share count to 112.7 million shares further bolstering its NAV per share.

As a result of those developments, I have recalculated Parex's after-tax NAV per share using the following updates to the company's financial position as per the most recent financial information:

- After-tax 1P NPV-10 of $2.5 billion;

- After-tax 2P NPV-10 of $3.4 billion;

- Total long-term liabilities of $90.8 million;

- Cash totaling $419 million; and

- 112.7 million diluted shares outstanding.

Using those numbers, I have calculated that Parex has an after-tax 1P NAV of $ per share as the table below shows.

1P NAV Calculation (Parex and author's own work)

That amount is 26% higher than Parex's U.S. pink sheet listed stock which is trading at $19.79 at the time of writing. While that indicates the company is undervalued it is the after-tax NAV of Parex's 2P reserves which gives the best indication as to the driller's indicative fair value in accordance with accepted industry standards.

Using the same numbers as above, I have determined that Parex's after-tax 2P NAV is $33.41 per share as illustrated by the chart below.

Parex After-Tax 2P NAV (Parex and author's own calculations)

That number is 69% higher than the market value of Parex's U.S. pink sheets listing of $19.79 at the time of writing. This indicates there is not only considerable upside available but also that there is a solid margin of safety for investors.

Solid financial position

While small-cap intermediate oil producers are typically risky investments because of their exposure to commodity prices and market risk, much of that is mitigated by Parex's solid balance sheet. The company is one of the few drillers of its size to have no long-term debt and a mere $91 million in long-term liabilities comprised of leases, share-based compensation, decommissioning and tax liabilities. Not only is Parex generating sufficient funds flow from operations to pay for annual capital expenditures, but the driller is also generating healthy free funds flow which for 2023 is projected to be $295 million at an average annual Brent price of $80 per barrel.

The strength of Parex's financial position coupled with growing production leasing to higher cash flows allowed the driller to hike its dividend by 50% from CAD$1 to CAD$1.50 thereby rewarding investors for their patience. That gives Parex a juicy 5.6% yield at the time of writing. Importantly, the dividend is sustainable with a payout ratio of 20% of 2022 net income and 62% of 2021 net income. For U.S. investors it is worth noting that a 15% withholding tax is imposed on dividend payments for non-residents although it can be claimed as a tax credit with IRS and any holding is withholding tax exempt if the shares are held in a U.S. retirement account.

Robust growth prospects

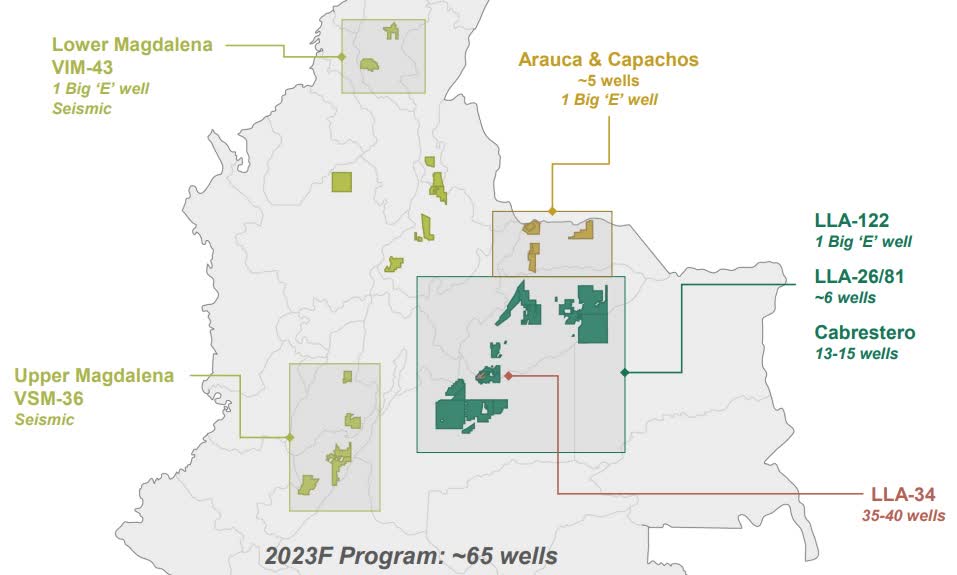

Parex possesses considerable growth prospects holding interests in a quality portfolio of Colombian on shore oil acreage and a large drilling inventory. For 2023, Parex plans to invest $425 million to $475 million developing its existing acreage, with 75% of that capital to be directed to operated acreage and the remaining 25% to non-operated LLA-34. During 2023, Parex plans to use that investment to fund the drilling of 65 wells consisting of up to 40 wells in the prolific LLA-34 Block, 15 wells in Cabrestero, six wells in LLA-26/81, five wells in the Arauca and Capachos Blocks along with a single exploration well in LLA-122.

{kind=link}

That development and exploration drilling will allow Parex to grow production with the company forecasting that average annual oil output will rise from a forecast 60,000 barrels per day during 2023 to 67,000 barrels daily by 2025. This will act as a powerful driver for earnings growth as well as the expansion of Parex's reserves and hence after-tax NAV per share.

The Cabrestero Block where Parex is using waterflood as an enhanced recovery technique will become a key driver of production growth. Parex also commenced enhanced recovery at the VIM-1 Block, where it is the operator with a 50% interest and the remainder is held by Frontera, in the Lower Magdalena Valley Basin. Gas is being reinjected, which has roughly doubled production to 4,000 barrels per day for March 2023. The driller intends to use that technique for the VIM-43 Block also in the Lower Magdalena Valley Basin.

Parex's 100% owned and operated VIM-43 Block in the Lower Magdalena Valley Basin is expected to function as a powerful growth driver for the driller. The company describes it as a transformational exploration prospect with three potential reservoirs. Parex is currently drilling the Chirimoya prospect with results expected to be announced during the second quarter 2023, with it anticipated that if the wildcat well is successful the block can support 10 or more development wells.

Company specific risks

Like any small-cap intermediate upstream driller Parex is exposed to a range of risks, notably commodity price, market and financial risk. In Parex's case, most of that risk is mitigated by its rock-solid essentially debt free balance sheet and ability to generate strong cash flow even if oil prices soften further. Nonetheless, the driller like its peers operating in Colombia is facing specific geopolitical risks which I have discussed at length in earlier articles, with most recent being my April 17, 2023, review of fellow Canadian driller Frontera Energy (FECCF) (FEC:CA). I will, however, summarize those risks here.

Regulatory risk

Colombia's first ever leftist president Gustavo Petro, who is a former guerrilla, emerged victorious in a second-round presidential run-off to enter office on August 7, 2022. He campaigned on a platform focused on reducing Colombia's dependence on fossil fuels and transitioning to cleaner renewable forms of energy. A key plank of that policy is his plan to ban contracting for hydrocarbon exploration . Despite speculation Petro would dial down his plan, Minister for Mines and Energy Irene Velez reiterated at the World Economic Forum in Davos that the administration will proceed with banning oil exploration.

This was confirmed by newly appointed Ecopetrol ( EC ) CEO David Roa, who stated that Colombia's national oil company will respect the guidelines issued by the government and not seek new exploration contracts. He went on to say Ecopetrol will learn to work with existing contracts which Colombia's Energy Ministry confirmed will not be affected by the decision to end contracting for hydrocarbon exploration.

Colombia is also moving closer to a total ban on hydraulic fracturing with a recent bill from the Petro government seeking to do so being passed by the Senate and sent to the lower house for review. A fracking ban will weigh heavily on Colombia's petroleum industry because of the country's limited proven hydrocarbon reserves, estimated at the end of 2021 to total 2 billion barrels of oil and 3.2 Trillion cubic feet of natural gas. Those reserves have a limited production life of around eight years.

Colombia is believed to hold considerable unconventional hydrocarbon potential. The U.S. EIA estimated Colombia has over five billion barrels of recoverable shale oil resources and 20 trillion cubic feet of shale gas. A fracking ban will limit the commercial lifespan of Parex's existing oil acreage much of which is situated in basins containing shale formations as well as the value of the company's VMM-9 Block in the Middle Magdalena Basin.

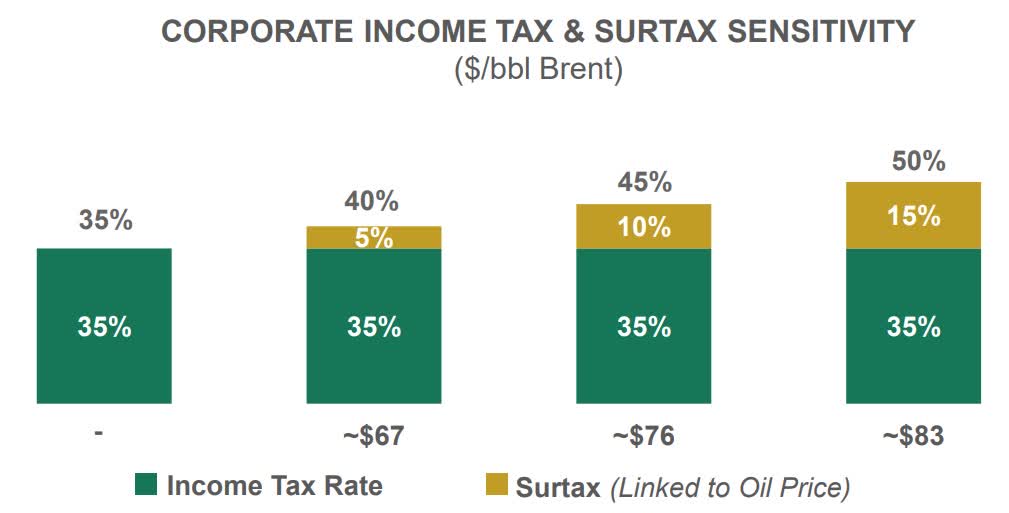

Petro's oil industry tax hikes, which were approved by Colombia's Congress during November 2022, are affecting the profitability of petroleum operations. This saw royalties removed as an income tax deduction and a scalable levy applied to oil sales when Brent exceeds certain levels. An additional 5% tax is payable when the Brent price ranges from $67.30 to $75 per barrel, which rises to 10% at $75 to $82.20 per barrel and then an additional 15% is payable when prices exceed $82.20 a barrel.

While some sources such as Colombian economic thinktank Fedesarrollo forecast that this could cause the industry effective tax rate to almost double from 36% to 70% other sources such as Colombia's Finance Ministry have calculated that it will only rise to 47%. This accords with Parex's own estimates with the driller forecasting an effective tax rate of 35% to 50% depending on the price of Brent and the surcharge applied as per the chart below.

{kind=link}

That means the impact of the new tax regime will not be as severe as initially believed and still leaves Colombia among the more tax friendly jurisdictions for energy companies in the Americas.

Security risk

Serious security risks continue to plague Colombia's oil industry with community protests against operations a constant hazard. Blockades of oilfields and even attacks on wellheads along with other infrastructure are once again becoming frequent events as the industry's social disintegrates. This is being magnified by frequent oil spills and other environmentally damaging industry emissions.

Another constant hazard is the sabotage of oil pipelines, typically by the last leftist guerrilla group the National Liberation Army, known by its Spanish initials the ELN, which frequently bombs the Caño Limon and TransAndino pipelines. Those occurrences along with the application of illegal valves to pipelines to steal petroleum, which is occurring more frequently, is impacting industry operations and production with drillers forced to shutter wells.

These hazards are weighing heavily on the outlook for upstream oil producers in Colombia and explain why Parex is trading at a deep discount to its after-tax NAV per share, but the market's perception is overblown.

Bottom line

Parex's 2022 full year results confirmed that the driller remains a best-in-class intermediate oil producer which is being buffeted a range of headwinds related to its operations in the strife-torn country of Colombia. An overblown perception of risk sees Parex trading at a deep discount to its after-tax NAV per share. By my calculations I have determined that the driller has an after-tax 2P NAV of $$33.41 per share which is 69% higher than the market value of $19.79 per share at the time of writing. That indicates Parex offers risk tolerant investors seeking exposure to oil prices considerable upside and a solid margin of safety, making now the time to buy. While investors wait for Parex's price to appreciate they will be rewarded by the company's juicy 5.6%.

For further details see:

Parex Resources: Deeply Undervalued And Remains A Buy (Rating Upgrade)