PARXF - Parex Resources: Risks From The New Colombian Government But Undervalued

- Parex Resources presents itself as the largest oil and gas producer in Colombia.

- Very recently, there was a change in the government in Colombia. We don’t really know whether the new administration expects changes in the oil and gas taxes or regulations.

- Parex Resources announced fantastic guidance with double-digit production growth, and noted more hiring in 2022 and long-term agreements for equipment.

- The undervaluation appears substantial.

Parex Resources Inc. ( PARXF ) delivered double-digit product growth expectations. Management is hiring more personnel, and signed a long-term contract for equipment in 2022. Everything indicates that the company's financial numbers are going to get much better in 2022 and 2023. I do see several risks from the new government in Colombia, changes in taxes or regulations, and potential impairment of reserves. However, under a conservative discounted cash flow model, Parex appears significantly undervalued. I will be building a position at the current price mark.

Parex Resources

Parex Resources presents itself as the largest oil and gas producer in Colombia with a land position of 5.8 million net acres and outstanding ESG performance.

Presentation

In my view, the most interesting is the company's production and PDP reserve growth. Management reports business growth of more than 18% CAGR, and forecasts further growth.

Presentation

From 2022, Parex Resources announced an expanded capex program of around $525-$575 million, which would allow production of more than 60k boe/d in Q4 2022. Management even offered a forecast of 100k boe/d for 2027. More production will likely mean further revenue growth, so I decided to run a financial model to assess the company's valuation.

Presentation Presentation

Parex Resources Does Not Report Financial Debt

As of March 31, 2022, Parex reported $362 million in cash and $1.9 billion in total assets. The company's financial situation appears quite beneficial with almost no financial obligations.

10-Q

Among the list of liabilities, there is only a lease obligation worth $6 million, which may worry investors. In my view, if Parex Resources decides to receive financing from banks, I wouldn't see many problems.

10-Q

My Model Leads To A Fair Price Of $49 Per Share

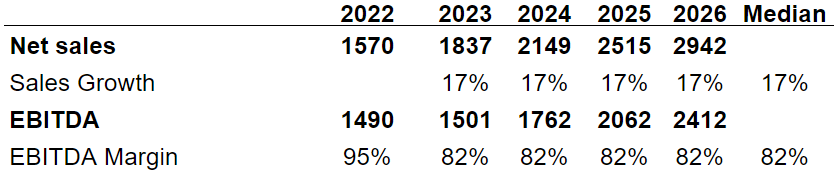

In order to assess the company's valuation, I had a look at the guidance given by Parex. Parex expects its 2022 capex to be close to $550 million, and the free funds flow would stand at $353 million. Besides, the company expects production growth to be close to 17%-29%.

Presentation Presentation

Apart from the beneficial guidance given by Parex, I believe that production will likely increase because Parex is hiring more personnel in Canada and Colombia. Let's note that the number of employees went from less than 300 in 2016 to more than 350 in 2021.

Ycharts

Besides, the company secured rights and signed long-term contracts for new equipment. More production will likely lead to revenue growth if the oil price does not increase.

Presentation

I assumed sales growth of 17%, which is in line with the forecast made by management in terms of production. Also, with an EBITDA margin of 82%, I obtained 2026 EBITDA close to CAD2.41 billion and 2026 revenue of CAD2.9 billion.

{kind=link}

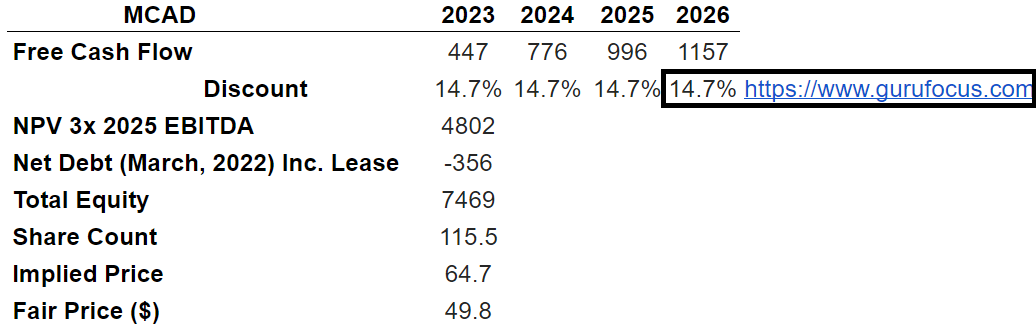

My CAPM model includes a cost of equity of 14%, cost of debt of 0.2%, and a beta of 1.9. The resulting weighted average cost of capital is equal to 14.6%. With a net debt of -CAD356 million, exit EV/EBITDA of 3x, and a share count of 115 million, the implied fair price would be $49 per share.

{kind=link}

Let's note that I am quite conservative with my exit multiple. The company trades right now at 2x EBITDA, but it traded in the past at 6x EBITDA, so 3x EBITDA seems conservative.

With A Decline Of 40% In Sales Growth, The Implied Fair Price Could Stay Close To $15

Parex didn't have any reason to fear the guerrillas in Colombia. However, in the future, the company may suffer attacks, kidnappings, or production stoppage. As a result, I expect not only reputational damage, but also declines in revenue growth. If the free cash flow declines too, the company's valuation would decline. In the last annual report, Parex gave an explanation of minor issues on the Capachos Block:

Since 2017 Parex has been performing work on the Capachos Block located approximately 75 kms from the Venezuela border, in the department of Arauca. In 2018, work on the Capachos Block was temporarily suspended for 20 days, due to security concerns for Parex contractors and equipment. During the current year Parex commenced additional operations on the Arauca block which is in close proximity to Capachos.

To date this escalation has not had a material impact on the Company's operations. As part of the activities against the Colombian government there are occasional pipeline bombings and disruption of the Cano Limon pipeline. The Company has no oil production that is transported via this pipeline. Source: Annual Report

Very recently, there was a change in the government in Colombia. We don't really know whether the new administration expects changes in the oil and gas taxes or regulations. If Parex has to renegotiate contracts with Ecopetrol ( EC ), or necessary capex increases, expected free cash flow would decline. If the fair valuation of Parex declines, the stock price would likely decline.

Any changes in the ruling government need to be agreed with Congress and are subject to Constitutional control which require a certain degree of consensus between the Executive, Legislative and Judiciary branches of power. Changes regarding oil and gas or investment regulations and policies or a shift in political attitudes in Colombia in which the Company operates are beyond its control and may significantly reduce its ability to expand its operations or operate a profitable business. Source: Annual Report

Climate change transition may have a detrimental influence on the company's access to liquidity, borrowing costs, or its reputation. We also don't really know how the new government in Colombia will be dealing with climate change. The company warned about these issues in the last annual report:

The Company's business, financial condition, results of operations, cash flows, reputation, access to capital, access to insurance, cost of borrowing, access to liquidity, ability to fund business plans may, in particular, without limitation, be adversely impacted as a result of climate change and its associated impacts. Source: Annual Report

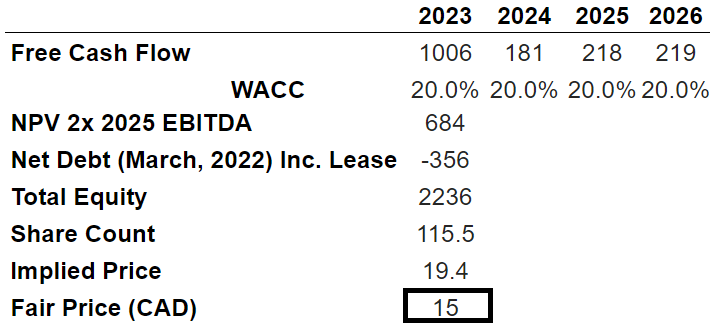

In the past, I saw revenue declines of close to -40%, so I believe that running a financial model with that level of sales growth makes sense. The Colombian market is expected to grow at a CAGR of 1.5% until 2025, so I also used that type of sales growth.

The Colombian oil and gas market is expected to register a CAGR of more than 1.52% during the forecast period of 2020-2025. Factors, such as increasing production and increasing consumption of oil and gas, are expected to boost the demand in the Colombian oil and gas midstream market during the forecast period. However, regular supply disruption by rebels caused unreliability in the industry and created large-scale losses for the pipeline companies. This factor is expected to hinder the growth of the market studied in the coming years. Source: Colombia Oil and Gas Midstream Market

Ycharts

With -40% sales growth in 2023 and 1.5% growth until 2026, 2026 revenue stands at CAD986 million. If we also assume an EBITDA margin of 60%, 2026 EBITDA would be CAD591 million.

Lubo Ycharts

With the previous assumptions, my results included a decline in free cash flow from CAD1 billion in 2023 to CAD219 million in 2026. Let's note that I am assuming a significant decline in capital expenditures and a change in working capital/sales of 4%. I assumed a conservative EV/EBITDA of 2x, net debt of -$356 million, and a weighted average cost of capital of 20%. The results were equal to an implied price of $15.

{kind=link}

Impairment Of Reserves Is Likely

Parex continues to drill, explore, and assess its current reserves. Engineers could make mistakes, and overestimate the company's proven reserves. In the worst-case scenario, management may have to decrease the total amount of reserves, which would reduce the expectations for free cash flow, and may diminish the company's fair valuation. If journalists or equity researchers do notice, the decline in the share price could be significant.

The Company expects that over time its reserve estimates will be revised upward or downward based on updated information such as the results of future drilling, testing and production levels. Reserve estimates can have a significant impact on net income, as they are a key component in the calculation of DD&A and for determining potential asset impairment. A downward revision in reserves estimates or an increase in estimated future development costs could result in the recognition of a higher DD&A charge to net income. Source: Annual Report

My Takeaway

Parex Resources announced fantastic guidance with double-digit production growth, and noted more hiring in 2022 and long-term agreements for equipment. The balance sheet includes a large amount of cash to invest in capital expenditures, and shows no debt. In my view, under normal circumstances, Parex could be worth $49 per share. There are some risks from impairment of reserves, new regulations, and taxes. I cannot really explain the current price mark. However, the undervaluation appears substantial.

For further details see:

Parex Resources: Risks From The New Colombian Government, But Undervalued