PKE - Park Aerospace: Highly Profitable And Shareholder-Friendly With Good Long-Term Prospects

2024-01-03 18:01:44 ET

Summary

- Revenues keep recovering after the coronavirus hit in fiscal 2021.

- Margins are expanding as demand returns while headwinds ease.

- The balance sheet is very robust thanks to very high cash and short-term investments and zero debt.

- This represents a good opportunity for long-term dividend investors as the dividend yield currently stands at 3.4%.

- I don't expect significant surprises in the second half of fiscal 2024, but I strongly recommend averaging down due to volatility risks.

Investment thesis

Park Aerospace Corp. ( PKE ) is expected to report fiscal 2024 Q3 results soon, so many investors might be wondering what to expect. In principle, no surprises are expected given the progression of recent quarters, so the share price should not be significantly impacted. After steady revenue growth achieved in the aerospace business since the divestment of its Electronic Business in December 2018 until the coronavirus pandemic, the company has been facing a series of headwinds that have impacted its operations since fiscal 2021, which is why the share price is still below pre-pandemic levels. In fiscal 2021, the coronavirus pandemic caused a 22.89% decline in revenues to $46.3 million due to self-imposed restrictions around the world, and although these increased by 15.78% in fiscal 2022 and by a further 0.89% in fiscal 2023, this recovery was accompanied by a contraction in profit margins caused not only by weak volumes but also by supply chain issues, increased freight costs, and inflationary pressures.

Historically, the company has generously rewarded shareholders through relatively high dividend yields and high special dividends, and I believe that it will continue to do so in the long term as sales are recovering at an acceptable rate while profit margins, although temporarily contracted, are very high, making the company highly profitable. Still, special dividends will likely be lower (or even non-existent) in the short and medium term due to operational weakness. Nevertheless, the balance sheet is robust thanks to high cash and short-term investments and zero debt, and the company has recently expanded its manufacturing facility and is planning to increase its workforce to increase production capacity as the management expects demand to continue increasing in the coming years.

For these reasons, I believe that Park Aerospace is a company worth owning from a dividend perspective as dividend investors will likely continue to be rewarded both in the short and the long term as the ordinary dividend yield is currently at 3.4%. Nevertheless, regarding potential share price volatility, I advise those investors with more conservative approaches to average down, especially due to the complex macroeconomic landscape and potential risks.

A brief overview of the company

Park Aerospace is a global developer and manufacturer of materials used to produce composite structures for the aerospace industry. Founded in 1954, the company's market cap currently stands at ~$297 million as it employs 119 workers. Also, insiders own 6.32% of the company's outstanding shares, which means that the management benefits from the good share performance and dividends.

In recent years, the company has undergone a significant transformation as it divested its Electronic Business in 2018 to focus exclusively on the aerospace industry, which is the reason why its name changed from Park Electrochemical to Park Aerospace in 2019.

The company's products are used to produce the structure of a wide range of aircraft vehicles for both commercial and military uses, and it also manufactures specialty ablative materials for rocket motors and nozzles, as well as materials for radome applications. Most of the company's revenues are generated within North America as revenues in the region accounted for 92.6% in fiscal 2023, whereas 6% were generated in Europe and 1.5% in Asia, and although both demand and profit margins have recently shown strong signs of recovery, they are still impacted by current headwinds, which is why the share price is still below pre-pandemic levels.

Currently, shares are trading at $14.65, which represents a 54.84% decline from decade-highs of $32.44 reached in July 2014. However, it is important to note that the company's sales have declined by two-thirds in recent years as it divested its Electronics Business in 2018 to focus on the Aerospace segment, which generally enjoys wider margins. In terms of the value based on revenues, the company's P/S ratio used to stay in the 2-3.5 range until 2018, whereas it currently stands at 5.41 as investors give more value to the sales of the remaining segment due to higher margins. Now, whether the price recovers will depend on management's ability to expand the Aerospace business, but it will likely take years to get there as expansion plans are still in process. In the meantime, investors should be able to keep collecting generous dividends.

The company began a capacity expansion project of its manufacturing facility in August 2019, and current plans involve increasing the number of workers in the coming years to adapt operations to a future in which the management expects sales to continue increasing. Despite this, the recovery is being relatively slow as the coronavirus pandemic fully impacted the aerospace industry in fiscal 2021 and the exclusive focus on the aerospace industry is relatively recent for the company while inflationary and supply chain headwinds continue to be part of the macroeconomic landscape.

Revenues remain weak, but the recovery continues

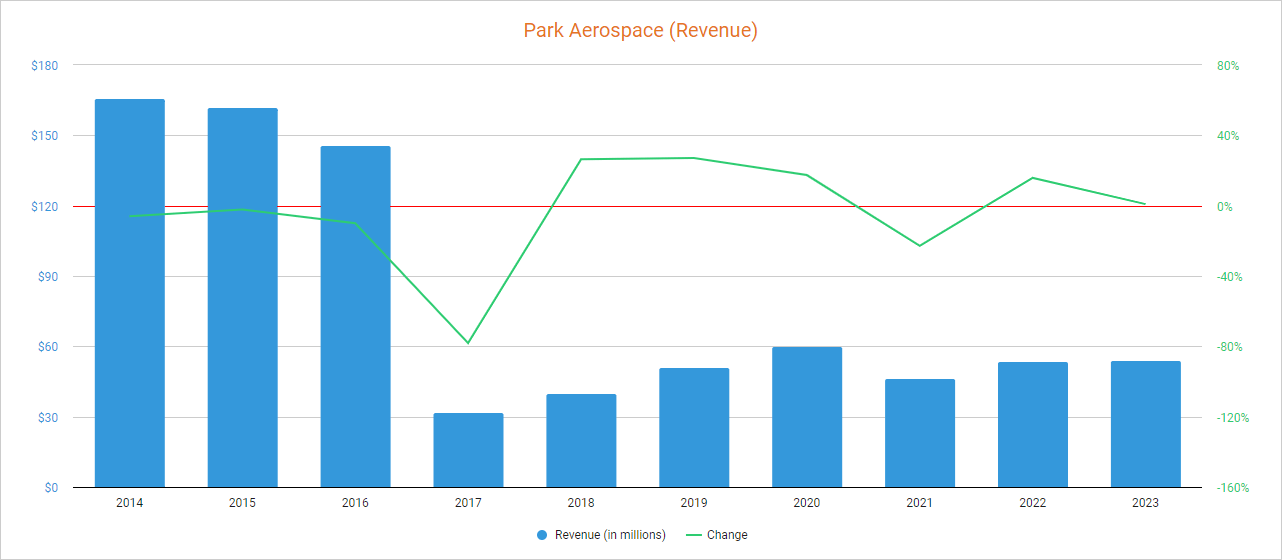

In December 2018, the company divested its Electronics Business for $145 million, and revenues declined significantly as a consequence as it was generating ~$70 to $80 million per year at the time of the sale. The remaining Aerospace business had been growing to $60 million in fiscal 2020, but the coronavirus pandemic outbreak caused a 22.89% revenue decline in fiscal 2021 as it impacted the airline industry significantly. Nevertheless, this decline was followed by a 15.78% increase in fiscal 2022 and a further 0.89% increase in fiscal 2023.

Park Aerospace revenue (Seeking Alpha)

{kind=link}

As for fiscal 2024, revenues increased by 21.65% year over year in Q1 but declined by 10.05% year over year in Q2. Quarter over quarter, this represented a 19.87% decline caused by a $3.1 million decline coming from the GE Aviation Jet Engine Program due to inventory destocking by MRAS (Middle River Aerostructure Systems), which supplies the project with Park's products. Nevertheless, trailing twelve months' revenues of $55.4 million are still 2% higher compared to fiscal 2023, and the management expects the recent decline to normalize by the end of Q3 as it is caused by high customer inventory, so it seems that sales should continue the growth path in Q4.

The company keeps launching products as it launched Aeroadhere FAE-350-1 in May 2023, a film adhesive product used for composite-to-composite, composite-to-honeycomb, composite-to-metal, metal-to-metal and metal-to-honeycomb bonding applications as the management is seeking to gain new customers now that its production capacity is being expanded. In this regard, its largest customer- approved production expansion in April 2023 is to support all of its aircraft programs, which should contribute to sales growth in the coming years.

The management expects to increase the number of workers from 119 currently to 134 in the foreseeable future, so it will be important to ensure that the increased production capacity is followed by increased demand as profit margins still suffer from the headwinds derived from the reopening of the global economy after the pandemic of the coronavirus pandemic. If demand does not increase as production capacity does, margins could be temporarily damaged due to unabsorbed labor. Even so, I consider that this potential scenario could be part of the process as it will take time for the new staff to gain experience within the company.

Certainly, investors are not as optimistic as they used to be before the coronavirus pandemic as the P/S ratio declined significantly to 5.411, which means the company generates $0.18 in revenues for each dollar held in shares by investors, annually.

This ratio is 0.64% below the average of the past 5 years but represents a 48.60% decline from the peak of 10.52 reached in the first half of 2019, which reflects the setback caused by the coronavirus pandemic and the subsequent supply chain issues, inflationary pressures, and increased freight costs. Furthermore, expected revenue growth is now (arguably) lower as not only the macroeconomic landscape is marked by these headwinds, but recessionary concerns continually fly over investors as recent interest rate hikes could cause a global recession, which could not only slow down revenue growth but negatively damage it and impact profit margins due to lower volumes at a time when manufacturing capacity is expanding.

Margins remain contracted, but the company is highly profitable

The company is highly profitable as it typically enjoys gross profit margins of over 30% and EBITDA margins of over 20%. These margins have recently been impacted by supply chain issues, increased freight costs, and inflationary pressures, but are already showing strong signs of improvement as the trailing twelve months' gross profit margin currently stands at 31.04%, and the EBITDA margin at 19.56%.

In Fiscal 2018, the Aerospace segment generated only 36.17% of the company's revenues, yet it provided 55.59% of overall operating income. Before the sale of the Electronic business, the gross profit margin barely exceeded 30%, while the EBITDA margin was always below 20%. For this reason, I believe that the share price could recover in the long term if the company manages to replace a significant part of the sales lost during the sale of the Electronic business.

Both gross profit and EBITDA margins continued improving in Q2 2024 as the gross profit margin increased to 32.68% and the EBITDA margin to 20.55% as headwinds are easing while volumes are returning to more healthy levels. Now, the company plans to increase the number of employees by 15 in the foreseeable future, which would represent a 12.6% increase compared to the present, as it expects to see increased demand in the coming years. If demand does not continue to increase as it has in fiscal 2023 and 2023, profit margins could be temporarily damaged as it needs to absorb the planned increase in labor, but the trend is so far positive and the company is highly profitable as it has reported positive net income year after year.

Thanks to high profit margins and positive net income, the company enjoys a robust debt-free balance sheet, although it has been deteriorating in recent years due to the very generous special dividends distributed among shareholders. In this regard, the company still has the resources to keep issuing (smaller) special dividends in the foreseeable future, but it seems that the time is coming to focus more on ensuring that revenue growth continues as operations can't keep up with such high dividends.

The balance sheet is very strong

The company paid down all its debt in January 2018 and has remained debt-free since then. Still, the balance sheet has deteriorated in recent years as the company has issued special dividends and maintained (and even increased) its ordinary dividend despite operations being much smaller in size after the divestment of the Electronic Business. In this regard, cash and short-term investments decreased from $108.23 million in fiscal 2018 to $74.21 million today, which means that special dividends are not sustainable at present. Still, the ordinary dividend seems safe thanks to the fact that cash and short investments are very high compared to a dividend that costs around $10 million per year, so the company still has the resources to keep covering the dividend while operations continue improving.

It is also worth saying that although cash and short-term investments declined by $31.2 million in the first half of fiscal 2024, inventories increased by $1.7 million and accounts payable decreased by $3 million while accounts receivable decreased by just $0.6 million. Furthermore, the company repurchased $2.9 million worth of shares in the same period and paid $21 million in special dividends in April 2023 (Q1 2024), which is why the company has actually generated a positive net income of $3.6 million in the first half of fiscal 2024.

In this regard, the company is profitable and the recent drop in cash and short-term investments is rather due to a strengthening of inventories and a decline in accounts payable, as well as a recently paid special dividend. Therefore, I believe that the current operations and balance sheet make the ordinary dividend very safe and could even leave some room for more special dividends in the future while sales continue to recover, although it is quite likely that investors will not see special dividends until sales increase sufficiently, which will likely take a few more years.

The ordinary dividend is safe

The company has paid dividends uninterruptedly for 38 years through a relatively low quarterly dividend, as well as high special dividends as long as conditions and the balance sheet have allowed it. Traditionally, the company had been paying an ordinary quarterly dividend of $0.10 per share, but it announced a 25% raise to $0.125 per share and quarter in February 2023. Considering a share price of $14.65, this represents a 3.4% dividend yield.

As for special dividends for the past 10 years, the company paid $2.50 in fiscal 2013, $2.50 in fiscal 2014, $1.50 in fiscal 2015, $3 in fiscal 2018, $4.25 in fiscal 2019, $1 in fiscal 2020, and $1 in fiscal 2024. Considering that there are ~20.5 million shares outstanding, one can get an idea of how much cash these special dividends cost the company. In comparison, the ordinary dividend, which amounts to $0.50 per year, is relatively small and will cost the company around $10 million each year. Judging by the increase in the cash payout ratio in recent years, the recent raise might seem reckless, but taking into account that the company holds $74 million of cash and short-term investments, investors can assume that the company has plenty of time ahead to continue growing its aerospace business to make said dividend more affordable.

| Fiscal year |

| 2015 |

| 2016 |

| 2017 |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| 2023 |

| Cash from operations (in millions) |

| $29.0 |

| $13.9 |

| $13.2 |

| $3.3 |

| $7.5 |

| $5.2 |

| $13.0 |

| $8.2 |

| $6.5 |

| Ordinary dividends paid (in millions) |

| $8.3 |

| $8.2 |

| $8.1 |

| $8.1 |

| $8.3 |

| $8.2 |

| $8.2 |

| $8.2 |

| $8.2 |

| Cash payout ratio |

| 29% |

| 59% |

| 61% |

| 245% |

| 111% |

| 552% |

| 63% |

| 100% |

| 126% |

Additionally, capital expenditures are very low at $0.78 million ('TTM') after the expansion of its manufacturing facility, which is located in Newton, Kansas, for which the company invested over $20 million. From now on, this increased manufacturing capacity should allow the company to cover more projects and thus continue with the growth path it has followed in recent quarters (except Q2 2024), which should ultimately lead to higher revenues and thus a safer ordinary dividend.

Still, I would not expect more special dividends in the short and medium term as the management could decide to limit itself to paying the ordinary dividend as a precautionary measure due to the worrying increase in the cash payout ratio derived from lower demand, both due to the sale of Electronic Business and the impact that the coronavirus pandemic (and the reopening of the global economy) has had on sales and margins.

Risks worth mentioning

Although Park Aerospace has been operating since 1954 and enjoys very generous profit margins, there are certain risks that I would like to highlight, especially for the short and medium term.

- Recent interest rate hikes could cause a global recession, which could have a direct impact not only on the company's sales but also on profit margins due to lower volumes, especially in the case of Park Aerospace as it is planning to increase the workforce in the near term.

- Profit margins could be seriously damaged if demand does not increase in the coming years due to the recent expansion of manufacturing capacity, especially once the workforce is increased.

- A further spike in inflation rates could once again hurt profit margins.

- If cash from operations does not increase in the coming years, the company could be forced to cut the dividend once cash and short-term investments approach worrying levels.

- Investors who invest expecting special dividends could run the risk of the company not being able to continue issuing them.

- 71% of the company's revenues came from the ten largest customers in fiscal 2023. Furthermore, 41% of revenues were provided by sub-tier suppliers of General Electric Company ( GE ). A significant drop in demand from one of these 10 customers, or from General Electric, would cause a noticeable hit to sales.

Conclusion

Despite a recent drop in sales in the last quarter due to inventory destocking by a major customer, it appears that sales are following a recovery trend since the reopening of the global economy following the coronavirus pandemic, which took place in fiscal 2021, and I don't expect any surprises in Q3 2024 as the progression has been quite stable. Furthermore, profit margins are improving, which should ultimately lead to higher cash from operations.

For my taste, the management has distributed too much cash in the form of special dividends in recent years, and I would have preferred to see a significant acquisition instead, although it seems that management's plans are more aimed at growing the aerospace business slowly through the recent expansion of its manufacturing facility. Also, the recent increase in the ordinary dividend seems too hasty for my taste still pending an increase in demand. As a potential investor, I would not expect more special dividends until cash from operations improves due to the decline in cash and short-term investments that the last special dividend caused.

But despite this, the balance sheet is very robust thanks to very high cash and short-term investments and zero debt, and current headwinds are, in my opinion, of a temporary nature due to their direct link to the current macroeconomic context. Furthermore, the recent expansion of the company's manufacturing facility opens the door to a new stage of growth, which should help reduce the cash payout ratio of the current dividend. For these reasons, I consider that Park Aerospace is a company worth owning from a dividend perspective, but that investing should be done cautiously by averaging down from current share prices as the risk of volatility is relatively high due to the current complex macroeconomic landscape and, more specifically because the company has very recently undergone a transformation process that continues to this day.

For further details see:

Park Aerospace: Highly Profitable And Shareholder-Friendly With Good Long-Term Prospects