PKE - Park Aerospace: Results Tumble But Long-Term Upside Remains

2023-10-06 04:43:54 ET

Summary

- Park Aerospace stock has gained 40% since coverage, outperforming the broader market.

- Q2 2024 results showed a decline in revenues, but margins remained strong, while a decrease in missed shipments suggest easing supply chain issues.

- The company has significant growth drivers and a bright future, making it a buy despite near-term uncertainty.

Park Aerospace ( PKE ) is one of the small aerospace suppliers that I am following and is a buy in my book. Since my last report covering the stock, Park Aerospace has gained 15%, outperforming the broader market, and since my first buy rating for Park Aerospace stock, the stock gained 40% compared to the 3.6% loss for the broader market, which I believe demonstrates the appeal of the aerospace industry even though capacity constraints continue to exist. Since my first buy coverage and buy rating on stock, the returns have been even more remarkable and perhaps demonstrate why I am favoring investment in aerospace suppliers over the companies operating commercial airplanes. Since my coverage on Park Aerospace, the company has shown a 46% return compared to 10% for the broader markets demonstrating the outperforming nature of some industry players.

In this report, I will be discussing the Q2 2024 results for Park Aerospace. I follow many aerospace companies and the earnings calls and presentations from Park Aerospace are among the trickiest ones to analyze because they are incredibly lengthy and the CEO tends to spend way too much time discussing items that are not quite interesting to investors or are simply repetitive. So, investors can benefit from this condensed analysis which looks at the most important items for investors as well as a price target assessment.

Park Aerospace Revenues Fall To Multi-Year Low

{kind=link}

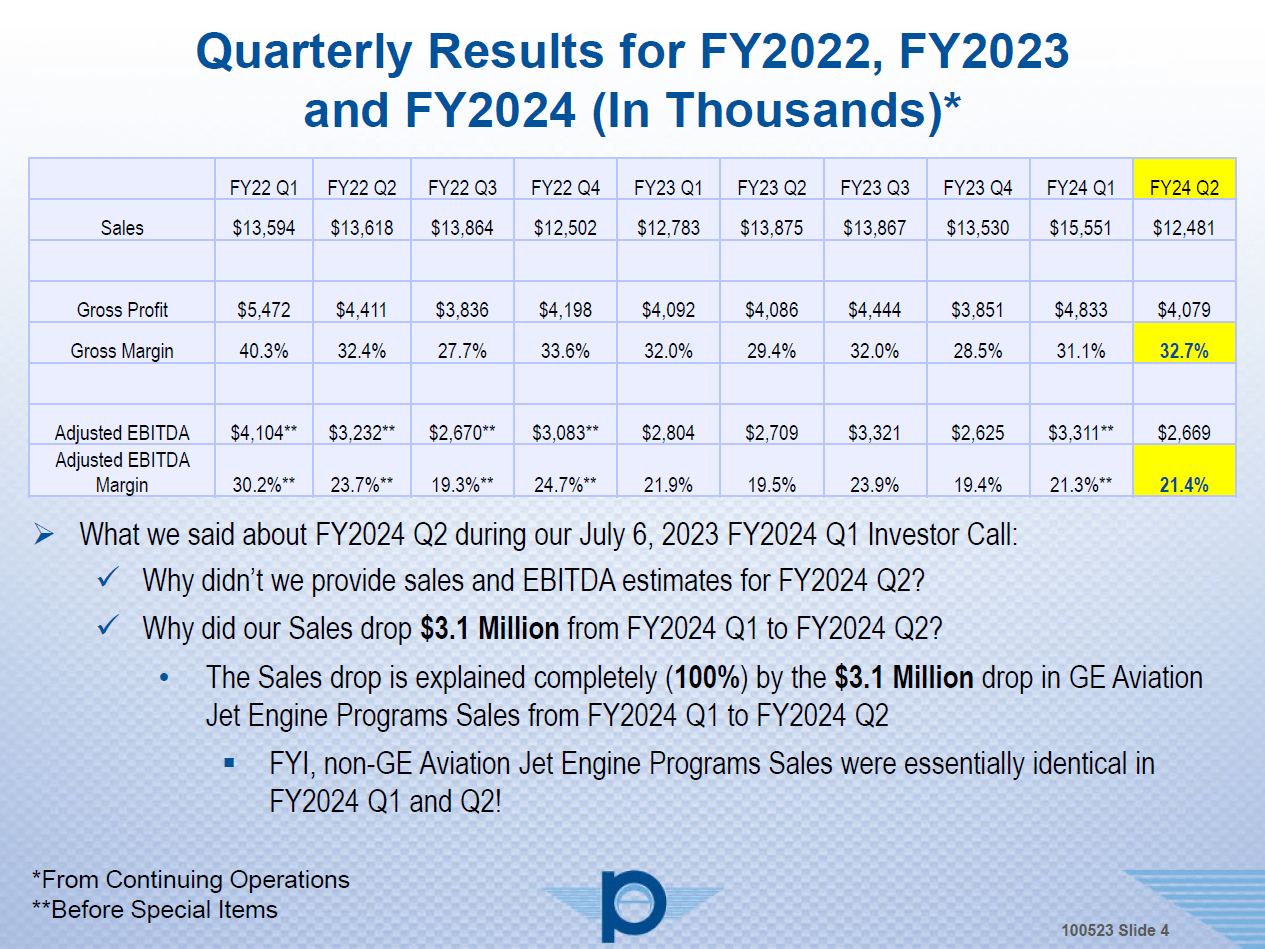

The FY24 Q2 results were actually not that great. The company had already not issued any guidance for the quarter, which did show some unquantifiable impact for Q2 was expected. The results were $3.1 million lower quarter-over-quarter and 10% year-over-year while also marking a multi-quarter low.

Interesting to note is that this was not caused by missed shipments as those are actually trending in the right direction with only $220,000 in missed shipments during the quarter. The missed shipments have been in the $0.6 million to $0.8 million range for many quarters and last quarter it was $0.4 million and Q2 has been seeing half that amount in missed shipments. How fast the decline in missed shipment reductions will be remains to be seen, but the missed shipment quantities do suggest that supply chain issues are somewhat easing.

This does not quite rhyme with the $3.1 million in lower sales, but that was driven by the MRAS or former GE Aviation programs where inventory burndown requires companies to be procuring less material from Park Aerospace. The company has previously expressed its displeasure on that topic but marked MRAS a strong partner in its Q2 earnings discussion.

While sales went down the drain, the margins stood strong at a 32.7% gross margin and 21.4% adjusted margin. So, excluding the timing variability for the GE Aviation programs the results were quite good. Moreover, Park Aerospace has suggested that the depletion of inventory could result in more demand for its product in the back half of the year.

Due to the uncertainty of the timing of procurement as a function of inventory depletion at its customers, Park Aerospace is currently unable to render a meaningful guidance for the next quarter or FY24. That is of course disappointing, but I also believe Park Aerospace is a company that should not solely be assessed on its quarterly performance but also its longer-term prospects.

What Will Be The Growth Drivers For Park Aerospace?

{kind=link}

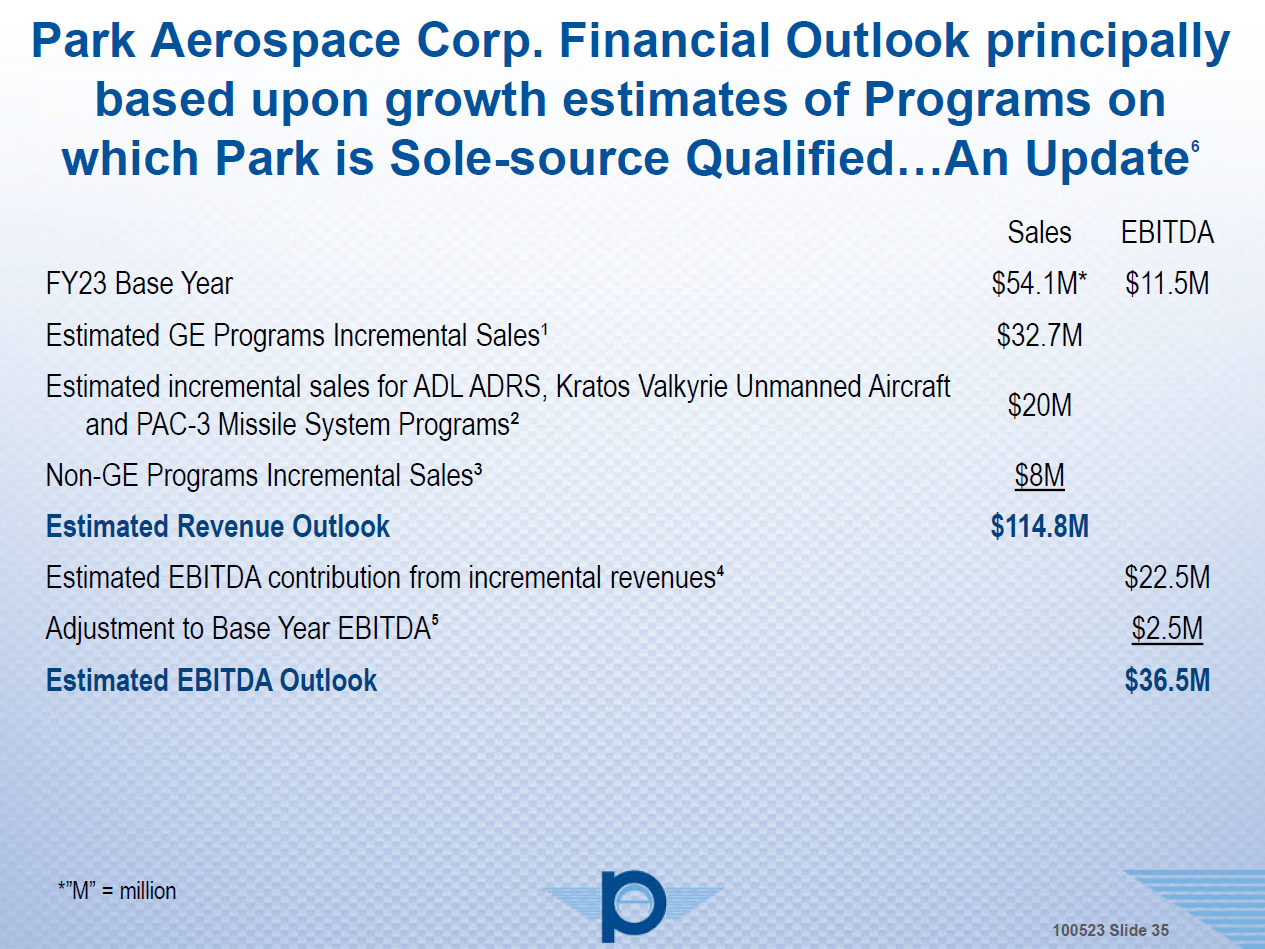

What I can appreciate is the insight that the company provides on its growth drivers. There is no particular year for which this outlook is applicable as the ramp up of commercial airplane programs is applicable, but on existing programs when those rates are hit, the company could generate around $115 million in revenues mostly driven by the production ramp up for commercial programs.

Furthermore, incremental sales on the ADL ADRS program and PAC-3 Missile Systems have room to grow even though I had expected the ALD ADRS contribution to be bigger as this drag reduction kit is applicable to a large quantity of Boeing 737 airplanes that could be retrofitted. With an installed base of thousands of Boeing 737 NG airplanes, I think there could be more upside to what is currently modelled.

The outlook could also grow more as Park Aerospace is also looking to participate on new programs that are not part of the current outlook. Compared to last quarter, the EBITDA outlook also improved from $34.8 million to $36.5 million on better cost control and reduction in lag effect. Furthermore, it should also be pointed out that pricing on the GE Aviation programs will go up in 2025 and 2029 which could provide additional growth.

Is Park Aerospace A Buy?

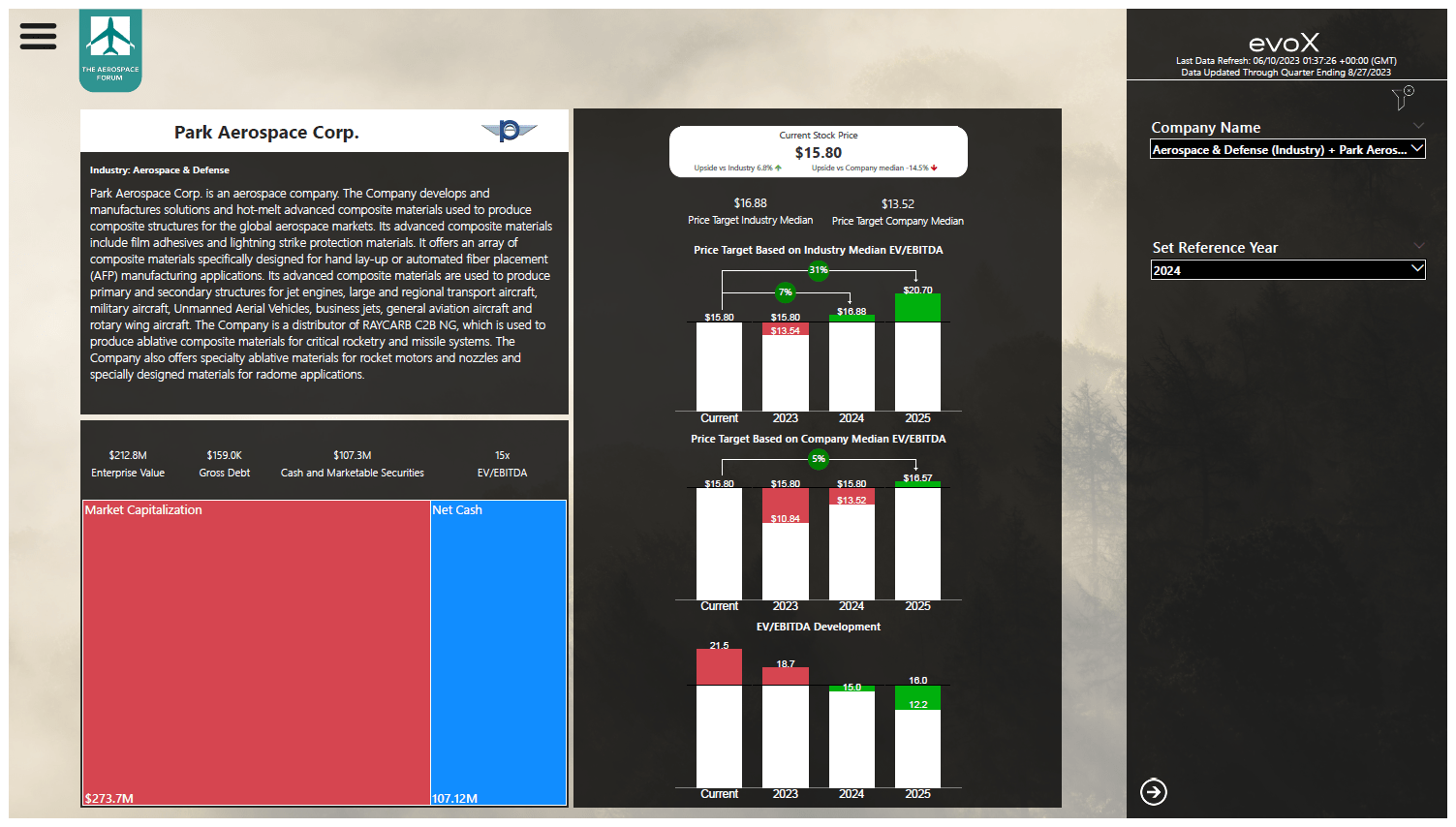

Park Aerospace stock valuation using evoX Financial Analytics (The Aerospace Forum)

{kind=link}

In my previous report, I marked the shares a buy with 26% upside. Since then, the stock has appreciated by 15%, so we see a significant portion of the upside filled which makes it highly interesting to assess whether there is appealing upside remaining. One thing that should be kept in mind is that the company has no long-term debt, and while future additions to the work force will increase costs, there is no major CapEx planned as Park Aerospace already went through the majority of its capital expenditures previously. With the Q2 earnings in, my targeted fair value for Park Aerospace based on its median has dropped by $0.08 to $13.52 showing that, with FY2024 earnings in mind, the company is not trading at a discount and provides around 5% upside as investors are already pulling FY2025 into the valuation.

The industry EV/EBITDA median provides 7% upside for FY24 and 31% upside towards FY25. So, the upside has shrunk somewhat, but that is also caused by the stock appreciating since my last coverage. Furthermore, one should keep in mind that Park Aerospace is already in its FY24, so pulling ahead FY25 into the valuation is not excessive. Although the industry median does show upside of 31%, I am currently not adopting that as a price target. The reason for that is that this assumes multiple expansion and double-digit EBITDA growth. The Q2 earnings discussion did show some uncertainty on revenue generation on the MRAS programs due to the inventory burndown issue. So, in fact, the FY24 earnings already are surrounded by uncertainty. Park Aerospace did highlight the possibility for elevated demand by the end of FY2024 and into FY2025. So, this is a bit of plunge into the unknown regarding 2024; it could continue to be weaker than previously seen through the financial year only to see a bump in FY2025, or some missed sales from Q2 and probably Q3 could shift to Q4. With that in mind, I do maintain my buy rating, but the upside for the near term has reduced and the risk or uncertainty has increased. That is something investors should be well aware of. What makes me more comfortable maintaining the buy rating is the fact that the company has significant growth drivers, and while those growth drivers will not be instantaneous as there is a stepped ramp up and ramp up timeline for each program, there should be significant upside for airplane production and subsequently for Park Aerospace.

Conclusion: Park Aerospace Stock Remains A Buy

The Q2 2024 earnings showed disappointing topline results but strong margins despite lower sales. Those strong margins are encouraging as is the further decline in missed shipments which point at supply chain constraints relaxing somewhat. Due to the uncertainty regarding the MRAS inventory burndown, there is no guidance from management and coming up with EBITDA estimates in the absence of any sell-side analyst coverage it is quite difficult to assess the impact for FY2024. That means that FY2024 could be worse than initially anticipated and below historical growth rates or it could positively surprise. That is not a great coin to flip. However, what remains the big positive is the growth platforms for the company.

Park Aerospace has a bright future if we look at the growth trajectory ahead. However, we do not quite know when those projections will materialize given the uncertainty on the ramp up profiles for single aisle jet production for Airbus ( OTCPK:EADSF ), which is the growth driver via the CFM LEAP-1A exposure that Park Aerospace has.

So, we see a set of mixed sentiments in the near-term as well as the long-term, which provides upside on an open-ended timeline. However, to me that is not enough to step away from my buy rating for the simple reason that whether the Airbus rate hikes that Park Aerospace is counting on happen in 2025 or 2026 or even 2027, it is going to be providing an upside to the stock that is beyond anything in our current projections. I think it is not worth to sell Park Aerospace stock now on near-term uncertainty and miss out on the longer-term prospects. In case the stock sells off followings is Q2 results announcements, I would consider that to be an even nicer entry point for long-term investors.

For further details see:

Park Aerospace: Results Tumble, But Long-Term Upside Remains