PK - Park Hotels & Resorts: Buy Into The Disconnect Between Market Value And NAV

2023-03-22 11:16:11 ET

Summary

- The hotel industry has survived the pandemic and, after a disastrous 2020/2021, robust travel recovery has allowed earnings to bounce back in 2022.

- Park Hotels & Resorts trades at a large discount to various NAV estimates and despite recession fears I see the REIT as a potential takeover target if the current discount persists.

- My own conservative assessment leans towards an NAV of $21 per share, meaning 75% potential upside from the current price. In the meantime, enjoy a 5% dividend yield. BUY.

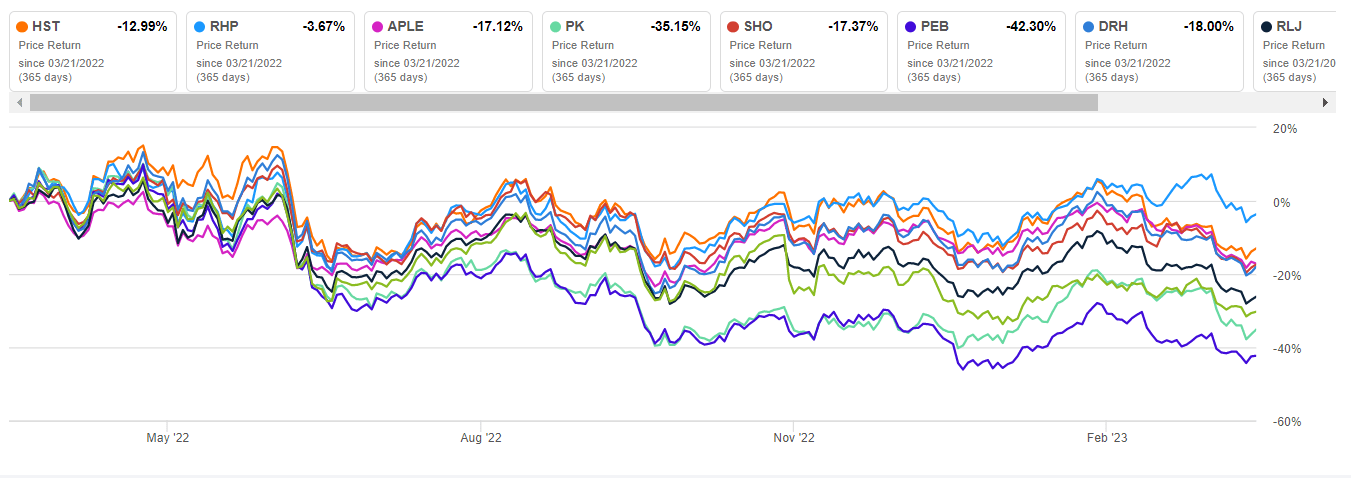

Park Hotels & Resorts ( PK ) is a well-known lodging REIT, and I assume most readers are familiar with the company. In terms of market capitalization, PK ranks fourth behind Host Hotels & Resorts ( HST ), Ryman Hospitality Properties ( RHP ), and Apple Hospitality REIT ( APLE ). However, PK has a higher gross asset value ((GAV)) for its properties compared to both RHP and APLE, so it's also referred to as the second-largest lodging REIT. Other notable companies in the industry include Pebblebrook Hotel Trust ( PEB ), DiamondRock Hospitality Company ( DRH ), Xenia Hotels & Resorts, Inc. ( XHR ), and RLJ Lodging Trust ( RLJ ). In general, the industry has underperformed the broader market over the past 12 months, with RHP being the best performer, declining only by 4%. PK and PEB have given up the most gains, declining by 35% and 42%, respectively.

{kind=link}

Given the current concerns of capital markets over a global slowdown and the rising borrowing rates, I see a bearish stance justified. Among REITs, lodging REITs have the shortest lease duration and are the first ones to be impacted by low occupancy rates during a recession, which can quickly jeopardize their profitability. Additionally, as REITs, they generally have high leverage. The lodging segment also incurs high fixed property costs, CAPEX requirements, and has a low EBITDA margin compared to other REITs.

The key top-line metric for the lodging industry is revenue per available room (RevPAR), which typically decreases during a recession due to hotels competing to offer high discounts to attract customers. Furthermore, the emergence of home-sharing services such as Airbnb has increased competition and weakened the pricing power of well-established hospitality brands.

Considering the intersection of industry-specific challenges with the current macroeconomic situation, it seems challenging to justify initiating a long position in PK today. In fact, shares could continue to trend downward in the coming months. However, as it often happens, when the market smells danger, we smell opportunity. Markets have a tendency to overreact to fears, and I believe that Park Hotels' shares are already an interesting speculative buy at around $12.

Investment thesis

The reason for my bullish call is simple: I see the current discount between the market price and Park Hotels' intrinsic value of assets as significant enough to justify it. Although the market seems unwilling to pay fair value for PK's assets at the moment, I expect it to eventually reverse course and agree. The properties are worth much more than Park's current $2.6B market capitalization. To prove this, I have not only reviewed the details of the net asset value ((NAV)) estimates provided by Park Hotels & Resorts, FactSet, and Morningstar, but I have also conducted my own conservative assessment. All valuations indicate a fair value above $20 per share.

In addition, I believe it may be wise to establish a position in PK now, rather than wait for the market to hit bottom, because I see PK as a potential takeover target. A large private real estate player such as Blackstone ( BX ) may be interested in making a move for a few reasons. Firstly, Blackstone is no stranger to the Hilton ( HLT ) brand, as they are well aware of its attractiveness. Park Hotels & Resorts began its stock market existence as the result of a spin-off of the Hilton real estate portfolio in 2017. Although PK has since sold non-core assets and acquired Chesapeake Lodging Trust, it still owns several Hilton-branded properties.

Secondly, I believe that the current price is already sufficiently attractive when considering the net asset value. Nobody can predict with certainty when a crash may occur, and even if it were to happen, it could become more difficult to get the board and shareholders to agree on an acquisition value that is heavily influenced by a rock-bottom price. With shares currently sitting at the same level they traded at back in 2020, the current shareholder base could be more susceptible to a deal offering a relatively small premium to the current market price.

Thirdly, Blackstone could be interested in Park Hotels & Resorts due to its limited exposure to hotels currently, but also because lodging REITs can serve as a great hedge against inflation. Additionally, with Covid-19 behind us, even in a recession, Park's properties are unlikely to experience lower vacancy rates than those during the pandemic. The business has shown resilience, and recovery is expected to continue through 2023, particularly due to PK's significant exposure to coastal markets such as San Francisco, where international tourism is yet to fully normalize. BX has broad enough shoulders to sit back and wait while PK weathers a potential storm, which should turn out to be just an average tropical storm in comparison to the C-19 typhoon that the company just survived.

Most importantly, I simply do not see a case where PK’s strong asset value is permanently impaired: as the recession subsides, these hotels are still set to be worth their intrinsic value. In my opinion, a deal could be the catalyst providing PK shares an immediate upside, but a lowball offer would negate the full fair value of the company if accepted.

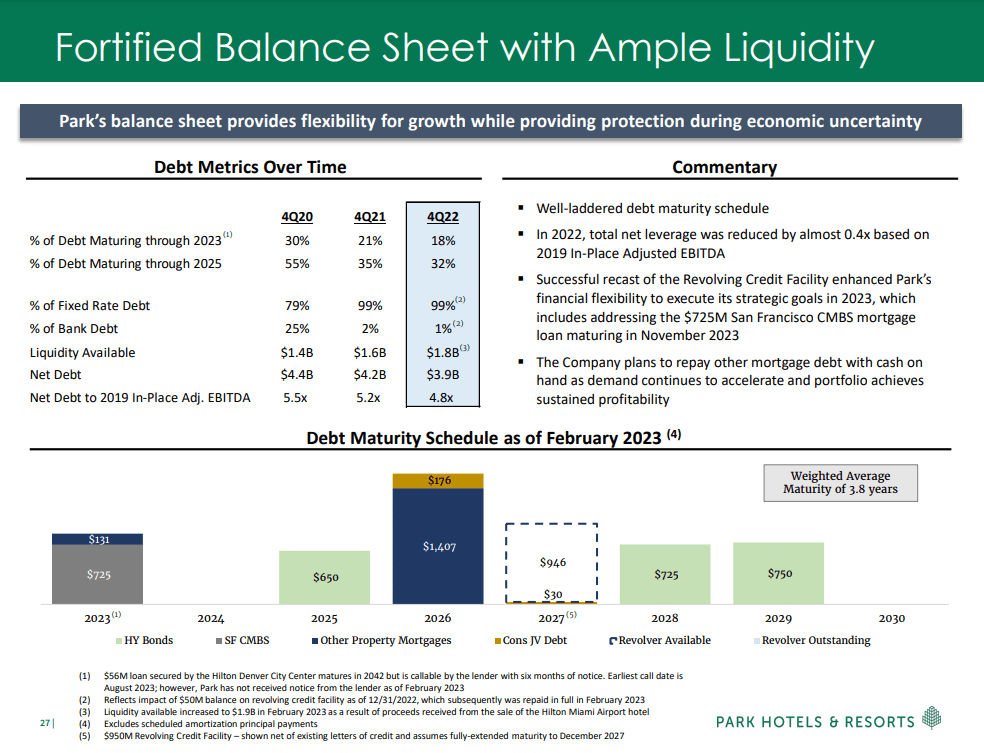

Debt maturities and balance sheet

For those who may be concerned about PK's debt and the potential impact of rising interest rates, I want to point out that the company has staggered debt maturities and manageable leverage. Additionally, PK reduced its Debt/EBITDA ratio by 0.4x during 2022, and its EBITDA is expected to grow faster than peers. PK is also open to divestitures as a means of both recycling capital into new opportunities and reducing leverage.

The following is from the latest investor presentation provided this month by Park Hotels and Resorts:

{kind=link}

The $725 million repayment due soon should not be a concern, as Park has approximately $0.9 billion in cash to cover it. Refinancing the maturity seems unlikely in the current market situation, and Park still has an additional almost $1 billion available on its revolver, bringing its total liquidity to $1.9 billion. Furthermore, PK has no upcoming maturities in 2024, giving it ample breathing space.

99% of the debt is fixed rate and while no immediate impact is expected on cash flow, it is highly unlikely that PK will refinance its current debt load at even similar terms. Incremental EBITDA generated from 2024 could still possibly cover most of the impact, but it is also possible that PK will take the road of further asset sales and debt repayment. This seems to have been the route taken for the 2023 maturity, with PK selling the Miami Hilton Hotel in February and raising more than $400 Million from sales during the last 12 months.

99% of PK's debt is fixed rate, and while there is no immediate impact on cash flow, it is highly unlikely that PK will be able to refinance its current debt at similar terms. Incremental EBITDA generated from 2024 could potentially cover most of the impact, but it is also possible that PK will continue with its approach of selling assets to repay debt. With the sale of the Miami Hilton Hotel in February, Park Hotels & Resorts raised over $400 million from sales in the last 12 months. The multiple transactions that have taken place on the private market, and their multiples implying cap rates in the 6%-7% range, further support my belief that NAV can be used as a reasonable benchmark for assessing the value of Park Hotels and Resorts.

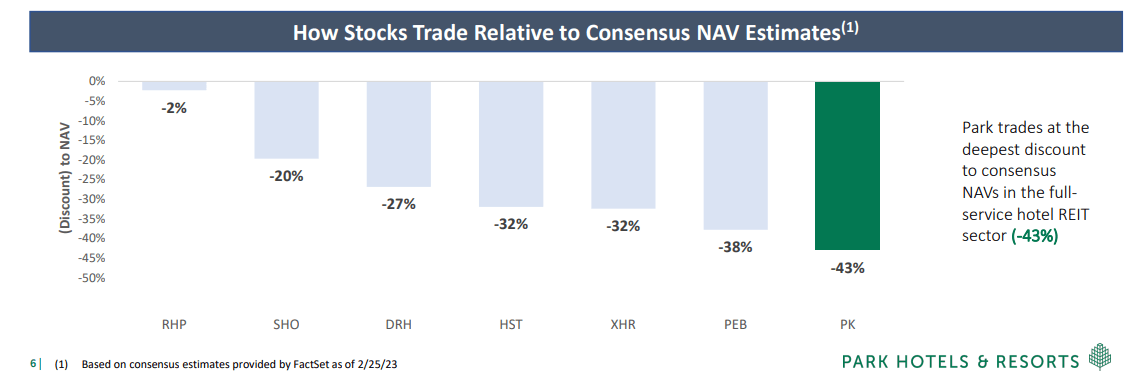

Valuation

The company has recently been vocal about the significant gap between its market value and the intrinsic value of its assets. Additionally, it has pointed out that its discount appears to be the widest among its peers and that this discrepancy seems unjustified.

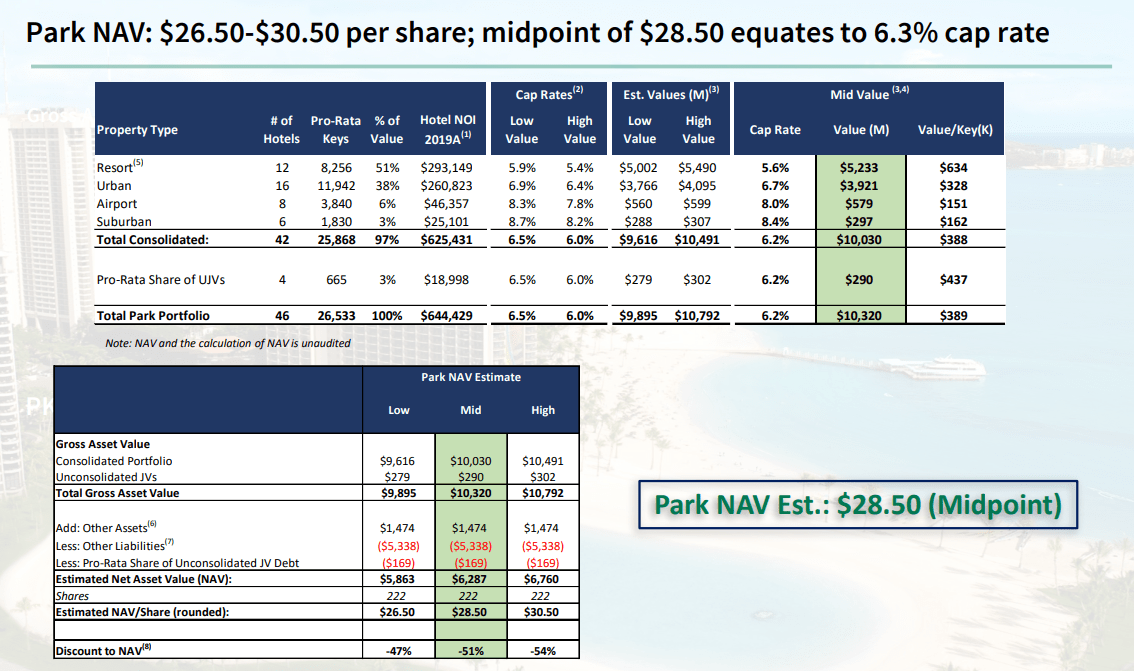

{kind=link}

The information released by PK allows for the derivation of FactSet's estimated NAV by retrieving the share price on February 25th ($13.92). According to FactSet, Park Hotels and Resorts has a NAV of $24.50, which is slightly more conservative than the company's own estimated range of $26.50-$30.50, but still represents a doubling from the current market price.

{kind=link}

While I do not necessarily buy into the management assessment, I find the effort to not only showcase the assessment’s result, but also the assumptions on which the model is built upon worthy of praise. NAV assessments are only as good as the inputs on which they are based, and even if I were to believe management has overstated certain figures, at least I would know how they derived the $28.50 value and how not only the final result, but also my own various inputs compare with theirs.

The importance of such transparency becomes apparent when checking the fair value assigned to PK by Morningstar. Morningstar is also bullish on PK, with shares trading in 5-star territory and an assigned fair value of $26.50. The analyst following the stock supports his target as also based on a NAV estimate but states that his NAV assessment for PK is only equal to $22.00. Interestingly, he values the stock at a premium to NAV, and the cap rate used is 8.0%, much higher than management assumptions.

Solving for $22 and 8% and considering the same balance sheet as provided by Park (that side of the equation shouldn’t really be subject to estimation anyway) I derived that Morningstar’s analyst assumption for PK total NAV is ~1.0B lower, but his assumed NOI is higher at about $710M.

This does not necessarily mean anybody is wrong. Management has used a 2019 figure, then implied there is significant upside (+38%) from the current EBITDA levels to $810M. Using the same methodology (NOI equal to ~94% of EBITDA) the forward NOI could potentially rise upwards of $750M, which is higher than the Morningstar’s NOI figure. This just shows financial modeling is part art and part science, and differences in style preferences can lead to significant changes in reported value.

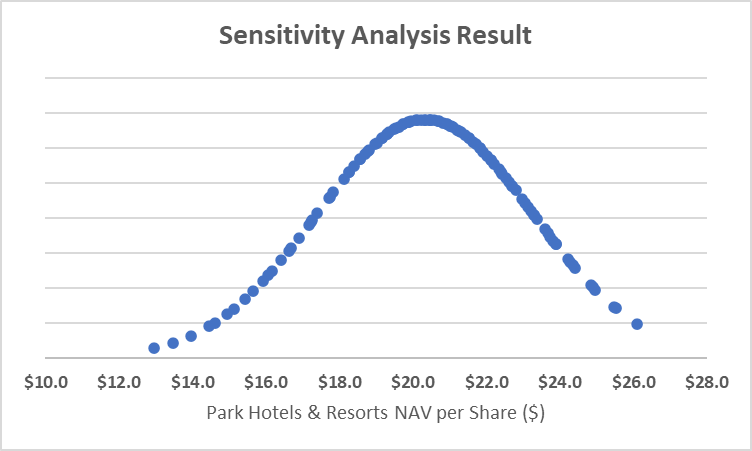

For my assessment, I used a NOI figure of $650 million which is roughly in line with PK's management and achievable as the high-end of their 2023 guidance. However, I used a blended cap rate of 7.5%, which is more on the conservative side. This estimate points at an NAV value of $21. To further analyze the sensitivity of the estimate, I conducted a range of possible outcomes using a 7% to 8% cap rate and roughly ±50 million in NOI. The graphic below shows the results of the sensitivity analysis.

{kind=link}

Conclusion

Despite the macro uncertainties, I am rating Park Hotels & Resorts a BUY here. The material disconnect between market price (around $12 as I submit this article) and my NAV assessment of $21 imply a 75% potential upside which seems too good to pass up. A slow position buildup, potentially looking at further weaknesses in the short term to accumulate shares, seems like the most prudent course of action. However, I do not recommend a wait-and-see approach here as the NAV discount could be already wide enough to attract a bidder for the whole company.

For further details see:

Park Hotels & Resorts: Buy Into The Disconnect Between Market Value And NAV