PK - Park Hotels & Resorts Is A Risky Buy

2023-08-04 17:41:16 ET

Summary

- Park Hotels & Resorts is an attractive REIT with high dividend yield.

- The company's fundamentals are improving, with revenues almost back to pre-pandemic levels.

- The stock seems undervalued, trading at a deep discount to NAV, making it an attractive investment opportunity despite some significant risks.

Introduction

As a dividend growth investor, I seek new investment opportunities in income-producing assets. I often add to my existing positions when I find them attractive. I also use market volatility to my advantage by starting new positions to diversify my holdings and increase my dividend income for less capital.

The real estate sector seems attractive nowadays as the interest rates are higher. These higher rates are pressuring some REITs, and investors can find high-quality REITs trading with a high dividend yield. One interesting REIT is Park Hotels & Resorts ( PK ), which I sold when it cut its dividend during the pandemic. As the pandemic is over and people enjoy more vacations, it is time to revisit the company.

I will analyze the company using my methodology for analyzing dividend growth stocks. I am using the same method to make it easier to compare researched companies. I will examine the company's fundamentals, valuation, growth opportunities, and risks. I will then try to determine if it's a good investment.

Seeking Alpha's company overview shows that:

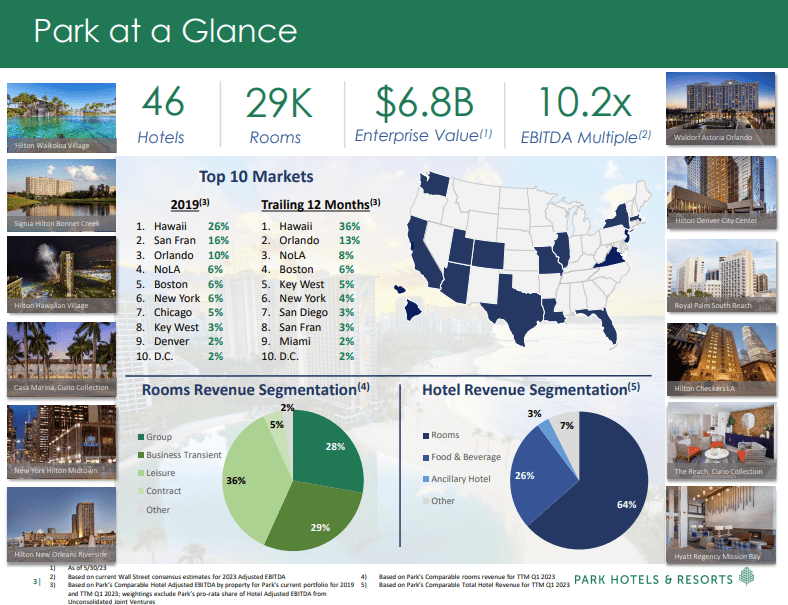

Park Hotels & Resorts is one of the largest publicly traded lodging REITs with a diverse portfolio of iconic and market-leading hotels and resorts with significant underlying real estate value. Park's portfolio currently consists of 46 premium-branded hotels and resorts with over 29,000 rooms primarily located in prime city center and resort locations.

Fundamentals

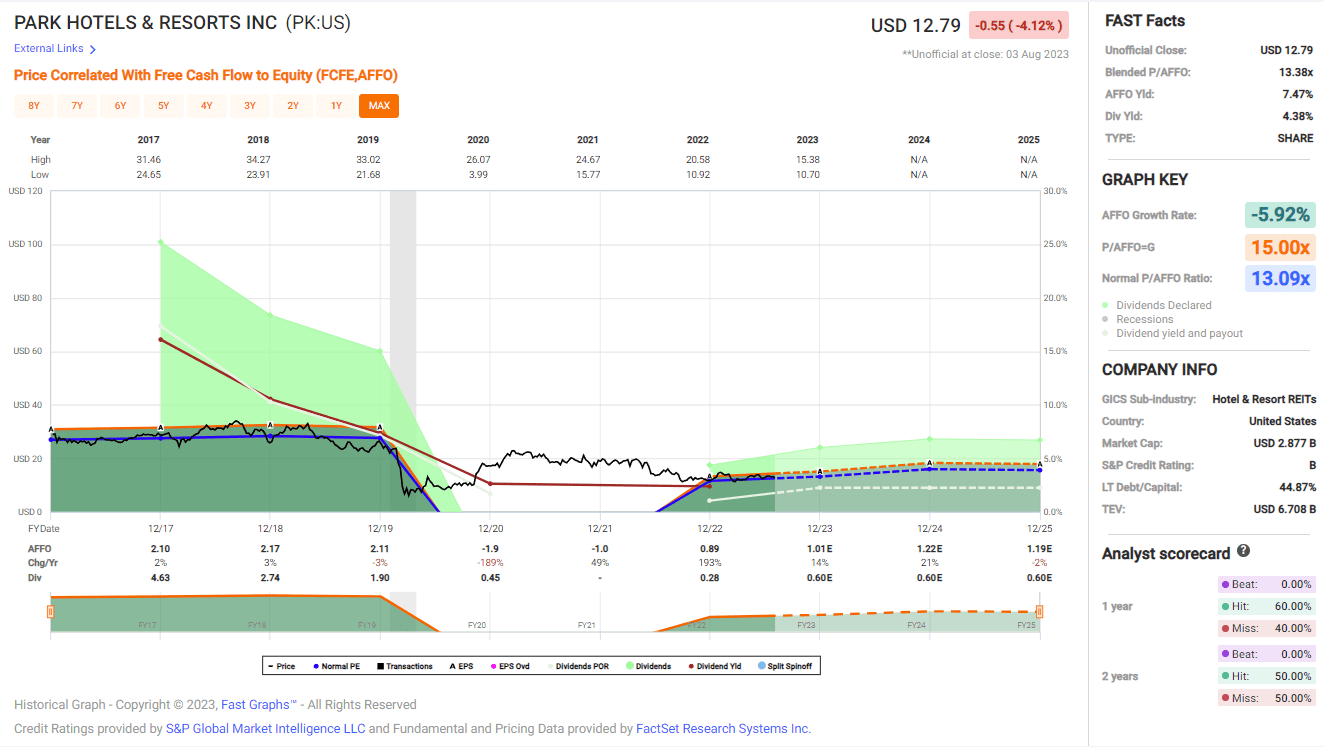

The revenues of Park Hotels & Resorts stayed flat since 2015. Park has almost entirely returned to its pre-pandemic revenues, as the revPAR (revenue generated per available room) is only 1% away from its 2019 highs when excluding San Francisco. The company is shedding its San Fransisco assets, as the market is fragile, and deploying it in more robust markets to support revenue growth. In the future, as seen on Seeking Alpha, the analyst consensus expects Park Hotels & Resorts to keep growing sales at an annual rate of ~5% in the medium term.

The FFO (funds from operations) is a prominent metric used to assess the profits of a REIT as it measures the cash flow generated. The FFO has decreased by 80% since 2016. When looking at the Adjusted FFO, which considers costs, the decline is more modest, with a roughly 50% decline from 2019. As the company is recovering from the pandemic's effect, it expects to see its AFFO increase by 28% in 2023. In the future, as seen on Seeking Alpha, the analyst consensus expects Park Hotels & Resorts to keep growing FFO at an annual rate of ~12% in the medium term.

The dividend paid by Park Hotels & Resorts has decreased significantly following the pandemic. While the current quarterly payout of $0.15 is much lower, it is also a relatively safe payment in my opinion. The company pays only 21% of its AFFO as dividends, leaving much room for buybacks, debt payments, and growth while maintaining an attractive yield of 4.4%. The company will have room to grow its dividend as the AFFO grows, and therefore, investors should expect mid to high single digits dividend growth.

Companies return capital to shareholders via dividends and buybacks. REITs usually do not buy back shares and tend to issue shares to fund their growth. Lowering the number of shares supports FFO per share growth. Since 2017, the number of shares outstanding has increased by 9%. While the number of shares has increased, I think the focus should be on the trend since 2020 and, more importantly, since 2022. We see increased buyback activity, including $105M in Q1 2023 alone. Buybacks are efficient when the share price is low.

Valuation

When using the 2023 FFO and AFFO estimates, the price-to-AFFO ratio stands at 6.6, and the price-to-FFO stands at 7. Real estate as a sector is trading for 14 times AFFO . Therefore, the Park Hotels & Resorts shares look undervalued. Moreover, the shares are trading 43% below their NAV (net assets value). While many peers trade for a discount, PK trades for a very deep discount at the moment, making it an attractively valued REIT and justifying the buybacks, which allow it to buy $1 of assets for 53 cents.

The graph below from Fast Graphs also emphasizes how Park Hotels & Resorts is attractively valued. The company is trading for 6.6 times future AFFO, while the average price-to-AFFO ratio since 2016 was 13. It's true that since the spin-off, the company struggled to achieve stable and steady growth, and therefore, some discount makes sense. However, the current discount to NAV and its average valuation look attractive.

{kind=link}

Opportunities

High-end assets in premium locations are the first growth opportunity for the company. The company focuses on luxury hotels in the city centers and attractive resort areas. It protects the company from competition from Airbnb as it offers a different experience with full service, unlike more basic offerings. As the company keeps growing by acquiring more premium assets, it will enjoy growth in demand for vacations and business travel.

{kind=link}

Diversification is another key growth opportunity. Park Hotels and Resorts have a presence in 15 states, with access to dozens of markets. Not relying on a limited number of markets protects it from downturns and weaknesses in specific markets, as we see now in San Fransico. Moreover, it allows it to grow in more markets and allocate capital to the most attractive markets at any given time.

{kind=link}

Park Hotel & Resorts needed to be rebuilt and adjusted following the pandemic and the weakness in San Francisco, which accounted for 16% of its revenues in 2019. I think thfe company's management is competent and is actively managing the portfolio. It sold less attractive assets, focused on the U.S., and used capital to acquire assets in attractive markets. Therefore, the revenues per room are almost at the same point they were in 2019. I think management's ability to allocate capital wisely is critical and will support the REIT's growth and allow it to offer higher dividends based on higher AFFO.

{kind=link}

Risks

The company is dealing with a high debt level, which may be more problematic as the interest payments increase. The company has stopped paying the loan for two of its assets, and they will be removed from its portfolio. Still, the company deals with $4.5B in debt and only $800M in cash. The current debt to EBITDA stands at 9.8, and even when looking at the forward forecasted EBITDA and using net debt, the ratio is above 6, which is high. High debt limits growth ability and carries high-interest payments.

In addition, the company is also susceptible to recessions. While the economy has managed to avoid a significant recession, we still see a slowdown. As the interest rates are higher, consumers and corporations have less capital to spend on vacations and needed work trips. If the situation deteriorates into a recession, Park Hotels & Resorts will be among the first to suffer, as travel is usually discretionary.

Another risk that may hinder growth and shareholder returns is the trust of investors and creditors in the company. The company trades 43% below its NAV. Investors are unsure that the company can capitalize on its potential and trade for a massive discount. Moreover, creditors who have seen the company avoid paying its loans, may be more suspicious before giving another loan to the company, and it may have to pay above market interest. Retaining the trust of creditors and investors may take time, as the company must show excellent execution. In the meantime, it means that returns are lower, and the ability to raise capital with stock or debt is more expensive.

Conclusions

To conclude, Park Hotels & Resorts is still recovering from the pandemic. The company stabilized its fundamentals by recovering its sales and improving its AFFO. That allows it to offer its investors an attractive dividend and buybacks at an attractive price. I think the current price is attractive given that the company trades for almost half its NAV. Together with some growth opportunities, mainly due to its profile and diversification, the company is poised to grow.

While the company looks on track to grow and deliver, there are some significant risks. The lodging segment is susceptible to recessions, and with the high debt level and low trust by investors, it may escalate quickly. Therefore, I believe shares of Park Hotels & Resorts are a BUY, yet a risky one with significant upside and a significant downside. It only fits investors who seek riskier plays.

For further details see:

Park Hotels & Resorts Is A Risky Buy