PK - Park Hotels & Resorts: Strong Growth Levers To Sustain Impressive Financial Performance

2023-12-28 12:09:02 ET

Summary

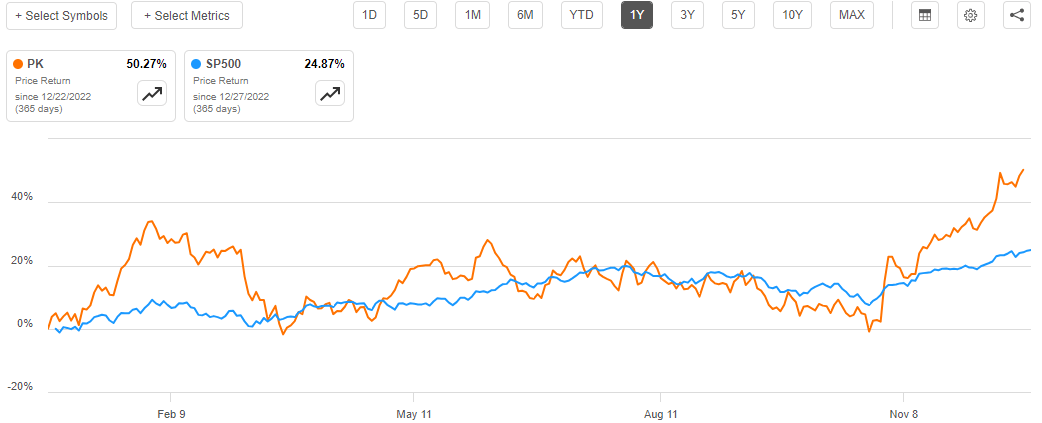

- Park Hotels & Resorts Inc. has seen a strong upward trajectory, gaining about 51% over the last year.

- The company's improving financial performance and strong growth levers make it an appealing investment opportunity.

- PK has consistently created value for shareholders through increases in revenue and profit, outperforming its peers and returning capital through dividends and share repurchases.

Investment Thesis

Park Hotels & Resorts Inc.(PK) has been on an upward trajectory gaining about 51% over the last year and beating the industry with a margin of about 25%.

{kind=link}

This strong performance, I believe, is a result of the company's improving financial performance since 2020, with both revenues and profits increasing consistently over the three years. I am bullish on this stock given its strong growth levers such as the recovery of demand in the hospitality industry.

Furthermore, I believe this company is a good investment because it has consistently created value for investors, as evidenced by a higher total return than the industry average, among other factors I will discuss in this analysis. Given the company's improving financial performance and impressive total returns, I recommend this stock to potential investors because it is undervalued based on relative valuation metrics and has strong growth levers.

Financials: Growing Impressively

Every investor is likely to be interested in a company that is demonstrating strong financial performance. A company's financial performance is important because it demonstrates how well it can use its assets to generate revenue, manage liabilities, and satisfy the interests of its shareholders. For this reason, this section will cover PK’s financial performance. To begin with, the company has consistently improved its revenues and profits since 2020, growing revenues from $852 million in 2020 to $2.5 billion in 2022 marking a growth of about 193%. This strong revenue growth, I believe, has been driven by the lodging industry's recovery from the impact of Covid 19, which increased demand for travel and hospitality services. The company's reopening of most of its hotels, which increased occupancy and average daily rate across its portfolio, also played a role.

Further, the company’s profits have also improved significantly with its operating loss of $558 million in 2020 turning to positive operating profits of $200 million in 2022, marking a growth of about 136%, and its net loss of $1.4 billion in 2020 growing to a positive net income of $162million in 2022 marking a growth of about 111%.

Market Screener

I believe its profits have grown significantly due to the strong growth in revenues coupled with strict cost control from the implementation of cost-saving measures . These measures have maintained the company’s total operating expenses relatively low as revenues increase significantly translating to higher profit margins.

YCharts

In terms of cash flows, PK’s cash flow from operations has increased significantly from a negative figure of $438 in 2020 to its positive current value of $447 million. This shows the company’s improving ability to generate cash flow from its sales and cover its operating expenses. It also underscores the company’s improving liquidity and flexibility to invest in growth opportunities, repay debt as well as return money to shareholders.

The company appears to be on its strong financial performance even in the MRQ a confirmation that its financial growth trajectory is still on. In the MRQ , revenue came in at $679 million a growth of 2.57% YoY. In conclusion, PK has consistently improved its financial performance, making it an appealing investment opportunity in my opinion. Given the company's strong growth levers, I anticipate that its financial performance will continue to improve and become even stronger in the coming fiscal years.

PK’s Solid Growth Levers

After evaluating PK, I found that the business has solid growth levers that will, in my opinion, support the company's continued success. First off, the hospitality industry is seeing a resurgence in demand , particularly in the luxury and upper-upscale segments. In H1 2023, ADR and RevPAR increased in almost every market, particularly in the luxury and upscale sectors. To demonstrate how PK is benefiting from this recovery, in the MRQ, its RevPAR increased 3% over Q3 2022, or an impressive 4.8% excluding its Casa Marina Resort hotel, where operations were suspended for a comprehensive renovation throughout the third quarter.

Tom Baltimore,” RevPAR increased 3% over Q3 2022, or an impressive 4.8% excluding our Casa Marina Resort hotel, where operations were suspended throughout the third quarter for a comprehensive renovation. Despite facing difficult year-over-year comparisons in July, our portfolio produced solid results with RevPAR including Casa, increasing 3.2% during the month followed by a 7.3% increase in August and a 4.2% increase in September, which were driven by improvements in both rate and occupancy.”

The hospitality industry's ongoing recovery is driving demand, resulting in higher rates and occupancy, which bodes well for the company's top and bottom lines. During this period of recovery, the hospitality industry is expected to grow at a CAGR of 10.62% by 2027. I believe that this expansion will result in higher occupancy and rates, which will boost the company's financial performance.

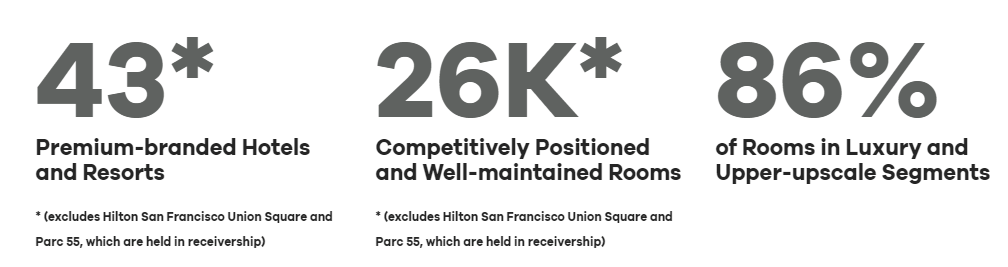

The company's other growth driver is its disciplined external growth strategy , which focuses on acquiring upper-upscale and luxury branded hotels in the top 25 US cities and premium resort markets, while also unlocking significant embedded value across its core portfolio through targeted capital investments. The company currently has 86% of rooms in luxury and upper-upscale segments.

{kind=link}

This upper upscale segment means that they offer high-quality amenities and services to their guests. To me, these facilities are critical to PK because they generate higher revenues per available room and attract more loyal customers than lower-tier segments. Furthermore, upper upscale rooms have high barriers to entry , which means they face less competition from new entrants in the market.

As a result, given the high barriers to entry and the presence of facilities in the top 25 markets where I expect occupancy and rates to be high, I believe this disciplined external growth strategy is not only a growth lever but also a competitive advantage.

Lastly is the company’s active capital recycling program that expands its presence in target markets with a focus on brand and operator diversification, while reducing exposure to slower growth assets and markets. In essence, the plan calls for the sale or disposal of non-core or underperforming assets, with the proceeds being reinvested in properties with higher growth potential or higher quality. By March this year, the company had disposed 39 hotels for over $2.1 billion and acquired an 18-hotel Chesapeake portfolio for $2.58 billion.

{kind=link}

Based on this data, this program has resulted in significant improvements in its portfolio quality and performance, as well as its financial flexibility and liquidity. PK expects to continue with this initiative beyond 2023, as it seeks to optimize its portfolio and create long-term value for its shareholders.

In my view, this program is very impressive because it is giving the company a lot of financial flexibility where it doesn’t have to rely on debt financing to pursue acquisitions something which will help the company to manage its financial leverage. Further, it is giving the company an avenue to dispose of its non-core businesses while investing in high-quality opportunities. In conclusion, PK has very promising and strong growth levers which I believe will keep driving the company’s strong future performance.

PK Creating Value For Shareholders

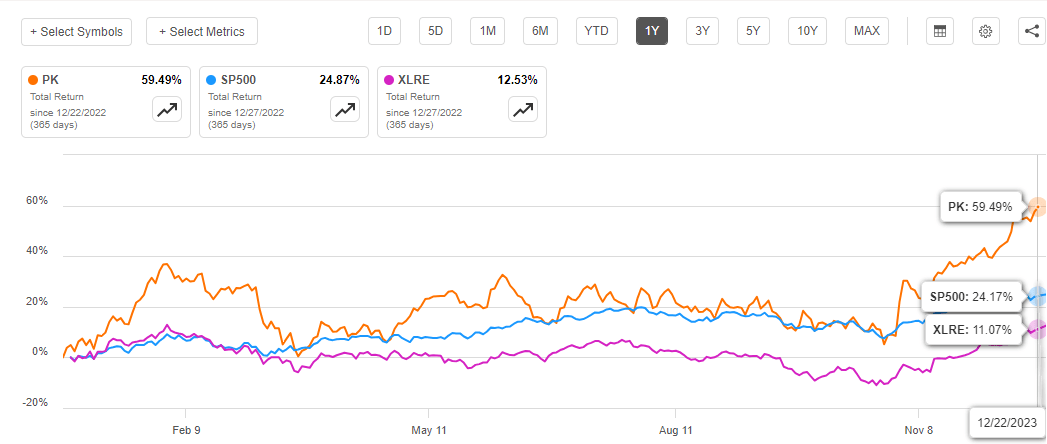

Based on my evaluation, PK has been creating value for shareholders something I believe makes it a good investment opportunity. In addition to the noteworthy increases in revenue and profit that have been reported since 2020, PK has proven its capacity to generate value for its investors in other areas as well. To start with, it has outperformed its peers and the broader market in terms of total shareholder return [TSR]. Its TSR is 59.49% for the last year, compared to 12.53% for the [[XLRE]] real estate sector Index and 24.87% for the S&P 500 Index.

{kind=link}

Secondly, PK has been returning capital to shareholders through dividends and share repurchases. It resumed its quarterly dividend payments in 2022, after suspending them in 2020 due to the pandemic. Its dividend yield grade of A- according to Seeking Alpha makes it an attractive dividend payer relative to its industry medians.

Seeking Alpha

The company also announced a $300 million share repurchase program in February 2022. Unless extended by the board, the stock repurchase program will expire on February 23, 2024. This reflects its confidence in its financial position and outlook. This program is still active, and in August 2023, a total of 5.8 million shares were repurchased under the existing repurchase program.

Lastly are its EPS and ROE. PK has seen both its EPS and ROE grow significantly over the last three years. With an EPS of 0.71, it implies that investors are earning $0.71 for every share they own, which is a major improvement from losses of about $6 per share in 2021. With a ROE of 3.69%, it shows that the company is generating a profit of about 3.69% on their invested equity.

YCharts

Given this context, it is clear that PK has been creating value for its shareholders, highlighting management's commitment to the company's shareholders.

Valuation

Based on relative valuation metrics, PK appears undervalued. The stock has a P/E NON-GAAP ratio of 25.46 compared to the sector median of 30.10, this signifies that PK is undervalued based on its earnings. Further, it has a forward P/E Non-GAAP of 21.50 which is lower than the sector median of 35.89. This suggests that PK is undervalued based on its future earnings potential.

With a P/S ratio of 1.38 which is lower than the sector median of 4.85, it implies that this stock is undervalued based on its sales performance. With most of the company’s relative valuation metrics below the industry medians, it is evident that this stock is undervalued which makes it an attractive entry point for potential investors.

Seeking Alpha

Areas Of Improvement

While I a bullish on this stock based on its strong growth levers, potential investors should be aware of the company’s fairly weak balance sheet. To begin with, the company has a high debt-to-asset ratio, which indicates a high financial risk. To begin with, the company has financial leverage of 1.064 which is fairly high and appears to be increasing since 2022.

YCharts

Further, the company liquidity is also fairly low with a current ratio of 0.98 and a cash balance of $726 million compared to total debt of $4.71 billion. Further, with an operating cash flow of $447 million, it implies that its cash flows can cover its total debt 9.49% which is very low coverage in my view. For these reasons, PK needs to strengthen its balance sheet to mitigate debt risks and avoid potential solvency problems.

Conclusion

In conclusion, KP has demonstrated strong financial performance, which, in my opinion, explains the company's increasing share prices. With the company's strong growth levers, I anticipate that its financial performance will continue to improve in the coming fiscal years. Given that this stock has rewarded shareholders through value creation and is undervalued based on relative valuation metrics, I recommend it to potential investors; however, be wary of its high financial leverage, which should be managed to mitigate debt risks.

For further details see:

Park Hotels & Resorts: Strong Growth Levers To Sustain Impressive Financial Performance