PRK - Park National: Still A Hold Despite The Recent Correction

2023-05-11 12:44:16 ET

Summary

- Real estate valuation increases propped up the non-interest income last year. This growth is unlikely to recur this year.

- Slight margin expansion and muted loan growth will keep the earnings from falling too low.

- The year-end target price suggests a small upside from the current market price. Further, PRK is offering a good dividend yield.

Earnings of Park National Corporation ( PRK ) will most likely dip this year due to lower non-interest income. However, topline growth will offer some support to the earnings. Overall, I'm expecting Park National to report earnings of $8.11 per share for 2023, down 10.5% year-over-year. Despite the recent stock price rout, the current stock price is still very close to the year-end target price. As a result, I'm adopting a hold rating on Park National Corporation.

Topline's Outlook is Somewhat Positive

The loan portfolio size declined by 0.7% during the first quarter. This fall was broad-based across the loan segments. Fortunately, the deposit book grew by 0.7% during the quarter, so the deposit run that hurt SVB Financial ( SIVBQ ) and First Republic Bank ( FRCB ) in March does not appear to have affected Park National. Deposit growth has, in fact, outpaced loan growth since 2021. Considering the trend, I think deposits can continue to grow for the remainder of the year. Easy fund availability will be conducive to loan growth going forward.

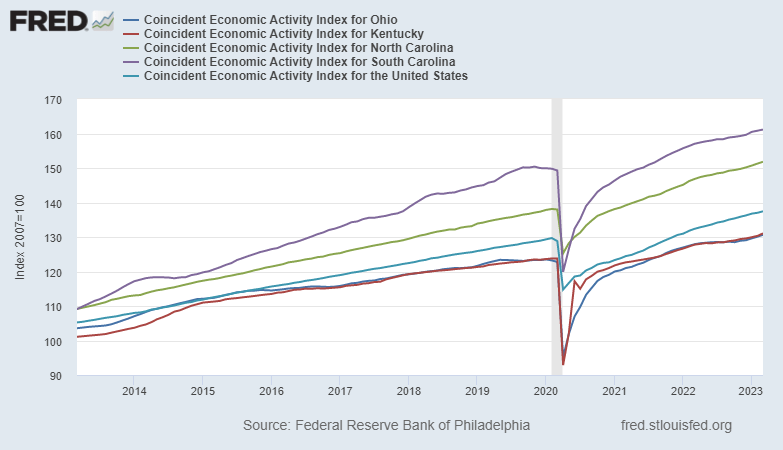

Further, strong labor markets bode well for loan growth in the near term. Park National operates in Ohio, Kentucky, and the Carolinas. Although most of these states have worse unemployment rates than the national average, their rates are very low from a historical perspective.

Moreover, the trend of the economic activity index for all four states is currently gently upward-sloping.

{kind=link}

Considering the state-level economic factors, I believe loan growth will remain positive in the year ahead, unlike the first quarter. I'm expecting the loan portfolio to grow by 0.8% in 2023. The following table shows my balance sheet estimates.

| Financial Position |

| FY18 |

| FY19 |

| FY20 |

| FY21 |

| FY22 |

| FY23E |

| Net interest income |

| 267 |

| 298 |

| 328 |

| 330 |

| 347 |

| 372 |

| Provision for loan losses |

| 8 |

| 6 |

| 12 |

| (12) |

| 5 |

| 5 |

| Non-interest income |

| 101 |

| 97 |

| 126 |

| 130 |

| 136 |

| 103 |

| Non-interest expense |

| 229 |

| 264 |

| 287 |

| 284 |

| 298 |

| 311 |

| Net income - Common Sh. |

| 110 |

| 103 |

| 128 |

| 154 |

| 148 |

| 132 |

| EPS - Diluted ($) |

| 7.07 |

| 6.29 |

| 7.80 |

| 9.37 |

| 9.06 |

| 8.11 |

| Source: SEC Filings, Earnings Releases, Author's Estimates (In USD million unless otherwise specified) |

The Risk Level Appears Satisfactory

Amid the recent bank failures, I believe Park National is a relatively safe investment because of the following two reasons.

- Unrealized losses on the available-for-sale securities portfolio amounted to $109.5 million at the end of March 2023, which is just 10% of total equity and 90% of the net income reported for 2022.

- Uninsured and uncollateralized deposits amounted to $1.2 billion at the end of March 2023, representing 14.6% of total deposits, according to details given in the 10-Q filing. This isn't worrisome as the unutilized funding available through various sources, including Fed Funds sold and FHLB borrowing capacity, totaled $2.74 billion at the end of the last quarter.

Adopting a Hold Rating

Park National is offering a dividend yield of 4.6% at the current quarterly dividend rate of $1.05 per share and an annual special dividend of $0.50 per share. The earnings and dividend estimates suggest a payout ratio of 58% for 2023, which is in line with the five-year average of 56%. Therefore, the dividend appears secure despite the earnings outlook.

I'm using the historical price-to-tangible book ("P/TB") and price-to-earnings ("P/E") multiples to value Park National. The stock has traded at an average P/TB ratio of 2.04 in the past, as shown below.

| FY19 |

| FY20 |

| FY21 |

| FY22 |

| Average |

| TBVPS - Dec 2023 ($) |

| 52.4 |

| 52.4 |

| 52.4 |

| 52.4 |

| 52.4 |

| Target Price ($) |

| 96.3 |

| 101.5 |

| 106.8 |

| 112.0 |

| 117.3 |

| Market Price ($) |

| 102.4 |

| 102.4 |

| 102.4 |

| 102.4 |

| 102.4 |

| Upside/(Downside) |

| (6.0)% |

| (0.8)% |

| 4.3% |

| 9.4% |

| 14.5% |

| Source: Author's Estimates |

The stock has traded at an average P/E ratio of around 13.5x in the past, as shown below.

| FY19 |

| FY20 |

| FY21 |

| FY22 |

| Average |

| EPS 2023 ($) |

| 8.11 |

| 8.11 |

| 8.11 |

| 8.11 |

| 8.11 |

| Target Price ($) |

| 93.7 |

| 101.8 |

| 109.9 |

| 118.0 |

| 126.1 |

| Market Price ($) |

| 102.4 |

| 102.4 |

| 102.4 |

| 102.4 |

| 102.4 |

| Upside/(Downside) |

| (8.5)% |

| (0.6)% |

| 7.3% |

| 15.2% |

| 23.1% |

| Source: Author's Estimates |

Equally weighting the target prices from the two valuation methods gives a combined target price of $108.30 , which implies a 5.8% upside from the current market price. Adding the forward dividend yield gives a total expected return of 10.4%.

Park National's stock price has dropped by 18% since March 8, 2023, when the collapse of Silvergate Capital ( SI ) first triggered panic in the banking sector.

Despite the rout, the market price is still only slightly above the year-end target price. Based on the total expected return and the risk level, I'm adopting a hold rating on Park National Corporation.

For further details see:

Park National: Still A Hold Despite The Recent Correction