PGPHF - Partners Group: Disappointing AUM Update Signals Challenging Times Ahead

Summary

- Partners Group misses the mark with its AUM update ahead of its FY22 earnings results.

- Guidance wasn’t great either, as the near-term headwinds for private equity continue to take their toll.

- I still like Partners as a way to ride the secular shift to alternatives, but given the tougher backdrop and the valuation, I am on the sidelines for now.

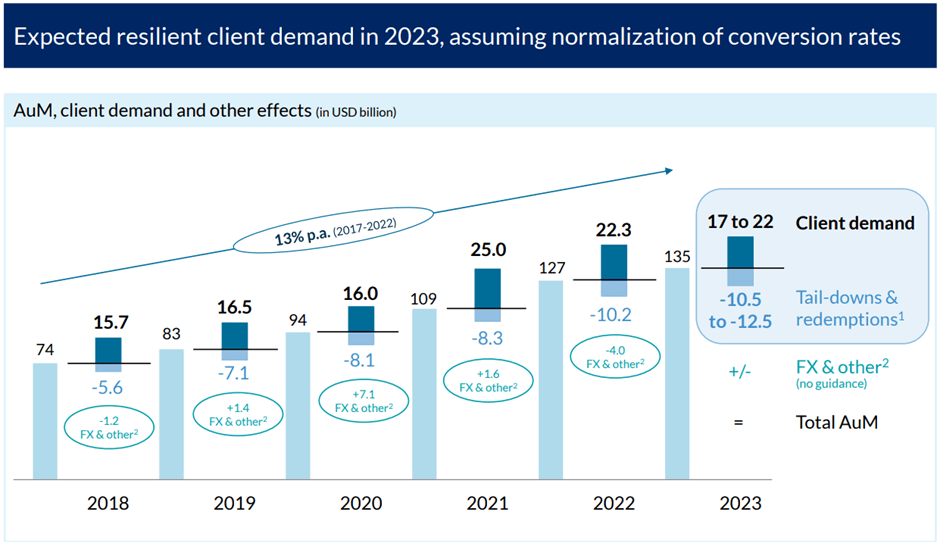

Alternative asset manager Partners Group (PGPHF) posted a disappointing FY22 asset under management ((AUM)) update, with gross client demand of $22bn coming in at the lower end of the prior full-year guidance of $22-26bn range. Alongside the report, management also pegged FY23 AUM at an even more disappointing $17-22bn in light of the challenging near-term outlook.

While private markets will face headwinds on the exit and fundraising fronts over the coming months, the mid-to-long-term bull case remains intact, in my view. And as private markets normalize, management is confident in returning to FY21 levels of fundraising – given the secular shift toward alternatives, I have no issue underwriting this view.

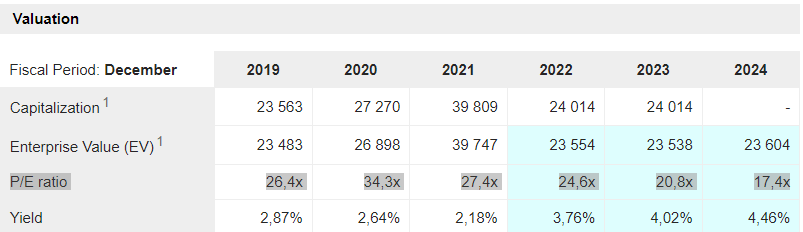

Yet, the muted performance fees outlook heading into H1 2023 and the prospect of more Fed tightening than expected following the recent jobs and inflation data means some caution is warranted for now. At ~20x fwd earnings, the stock seems fairly priced.

{kind=link}

Key Takeaways from the FY22 AUM Release

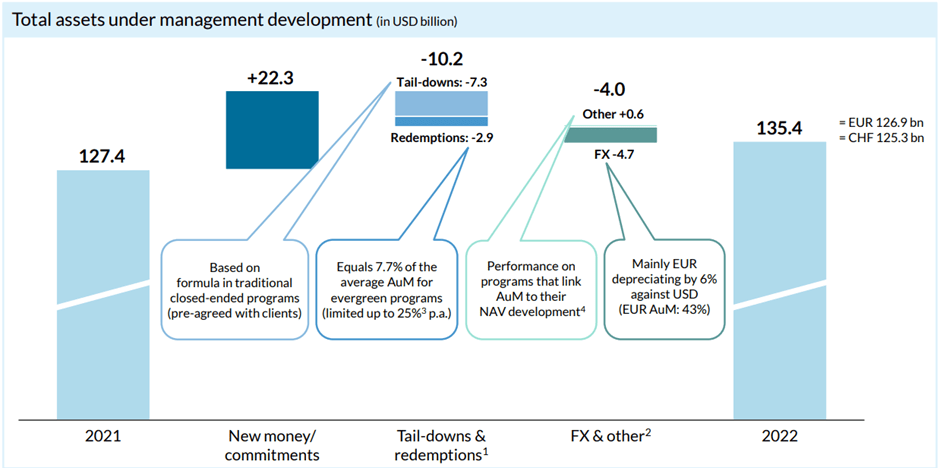

Partners Group lowered the bar heading into next month’s earnings report, disclosing a below-par $135bn AUM at the end of December 2022. The headline miss was driven by tail-downs and redemptions, offsetting higher client commitments. Still, there were silver linings. Of note, the private equity performance delivered surprisingly positive returns of 2.6% (vs. -2.6% in the prior nine-month period), helped by stronger portfolio growth and several liquidity events. Management was quick to temper expectations on the call (audio replay here ), though, cautioning that returns for the buyout sector will remain pressured for the foreseeable future amid increasing financing costs. In the meantime, asset transformation efforts (vs. purely leverage) should help to cushion the performance impact of less debt being used.

{kind=link}

Another statistic worth noting from the Partners Group AUM presentation was the disclosure that it had only deployed $12.6bn of assets in H2 2022 – well below the $18.6bn invested in H2 2021. Unsurprisingly, the slower pace of fundraising was the key culprit, though management stressed on the call that the lower “client conversion rates” was a temporary trend and that demand remained intact. In line with this view, the company’s mid-term guidance calls for a rise in allocations - in its base case scenario, private equity fundraising is projected to return to FY21-FY22 levels within the next three years (in line with broader rate normalization globally). As I stressed in my prior coverage , rising allocations to higher-performing alternatives like private equity are here to stay, and thus, I see an extended institutional allocation runway as well within reach.

Disappointing FY23 Guidance Amid Delayed Exits

As highlighted by its new guidance for $17-22bn of new client demand and $10.5-12.5bn of tail-downs and redemptions in FY23, the company will need to contend with similar private market headwinds throughout the coming year. For one, the Fed isn’t done tightening, and financing has been difficult, as banks pull back on debt financing and capital market investors demand a larger risk premium given the uncertainty. In response, the company is lowering its ticket size to $0.4-1bn (down from $1-1.5bn prior) and reducing its deal leverage to ~35% (down from ~50% prior). Alongside the lower AUM inflows, this means more disciplined capital allocation to sustain expected returns. Given the unfavorable pricing environment, though, the company is being forced to hold off on direct exits and liquidity events, so lower returns seem like a more realistic outcome for now.

{kind=link}

Another key concern is on the expense side – per management, hiring had ramped up throughout the year to make up for the lower hiring activity in the prior years. As a result, the year-end headcount stood at 1.8k, with hiring activity set to increase in line with the AUM level in the coming years. While management reiterated that operating margins would remain above the 60% guidance level, there could still be downside risk for EBIT margins in FY22/FY23 from the recent headcount additions. Plus, management’s reiterated performance fee/revenue guidance at an implied ~12-13% for the full year seems optimistic in light of the downbeat exit activity outlook. So unless there is some offset from client demand, I suspect there is downside risk to the performance fee guide as well.

Disappointing AUM Update Signals Challenging Times Ahead

The FY22 AUM and guidance update from Partners Group ahead of its earnings report were well below consensus expectations; following the announcement, it’s hard to see past the near-term downside. Still, there remains a lot to like for patient, long-term oriented investors - the company’s unique integrated platform model allows for customizable offerings, which has resonated with allocators thus far, allowing it to become the largest and most profitable listed alternative asset manager in Europe. Given its strong differentiation vs. more traditional asset manager peers, Partners Group is poised to capitalize on a secular shift to alternatives.

The catch is the unfavorable near-term dynamics for private equity, as higher rates have weighed on the entire cycle, from fundraising and financing to exits. Pending visibility into a sustained private markets recovery, the stock is probably fairly priced at ~20x fwd earnings.

For further details see:

Partners Group: Disappointing AUM Update Signals Challenging Times Ahead