PAX - Patria: Bet On Alternative Investments And LATAM

2023-09-04 11:05:22 ET

Summary

- Patria Investments is an asset management company representing the intersection between two emerging investment themes: LATAM revival and alternative investments growth.

- PAX has a healthy balance sheet with sufficient liquidity to expand its operations further. The company management has proven its capabilities to extract Alpha. Its funds consistently outperform the benchmarks.

- PAX offers an attractive dividend. In its last presentation, the company projects the distributable earnings per share to double.

- I give a buy rating despite the stock being overvalued based on the Dividend Discount Model. Investment in PAX is a long-term bet on LATAM with at least 24-month horizon. The current market price is an opportunity to start building a position and then use the price dips to add more exposure.

Thesis

Alternative investments will continue to attract investors' funds. Latin America is one of the world's regions with substantial untapped potential. Is there a company that gives exposition to both?

Patria Investments Limited ( PAX ) is an alternative asset manager investing in LATAM. The company has an experienced team that consistently outperforms its funds' benchmarks. Since the company's IPO, AUM has grown significantly via acquisitions and joint ventures. PAX has a clean balance sheet with liquidity ready to deploy for new acquisitions. PAX has ambitious plans to double its AUM and fee-related income.

I give PAX a buy rating despite being overvalued at 14% based on the dividend discount model. The current price is an excellent opportunity to buy with a fraction of the capital dedicated to PAX. Further price dips will offer another chance to buy more shares.

Why LATAM

I seek investment ideas in obscure places. Such ideas include uranium's looming deficit, litigation finance, and the revival of Latin America. I strongly believe in LATAM's potential for future growth. Its GDP represents 6% of the global, but its equity market capitalization is a mere 1%. The common wisdom says Latin America is too risky to invest in, and that is true. Moreover, that is part of the equation.

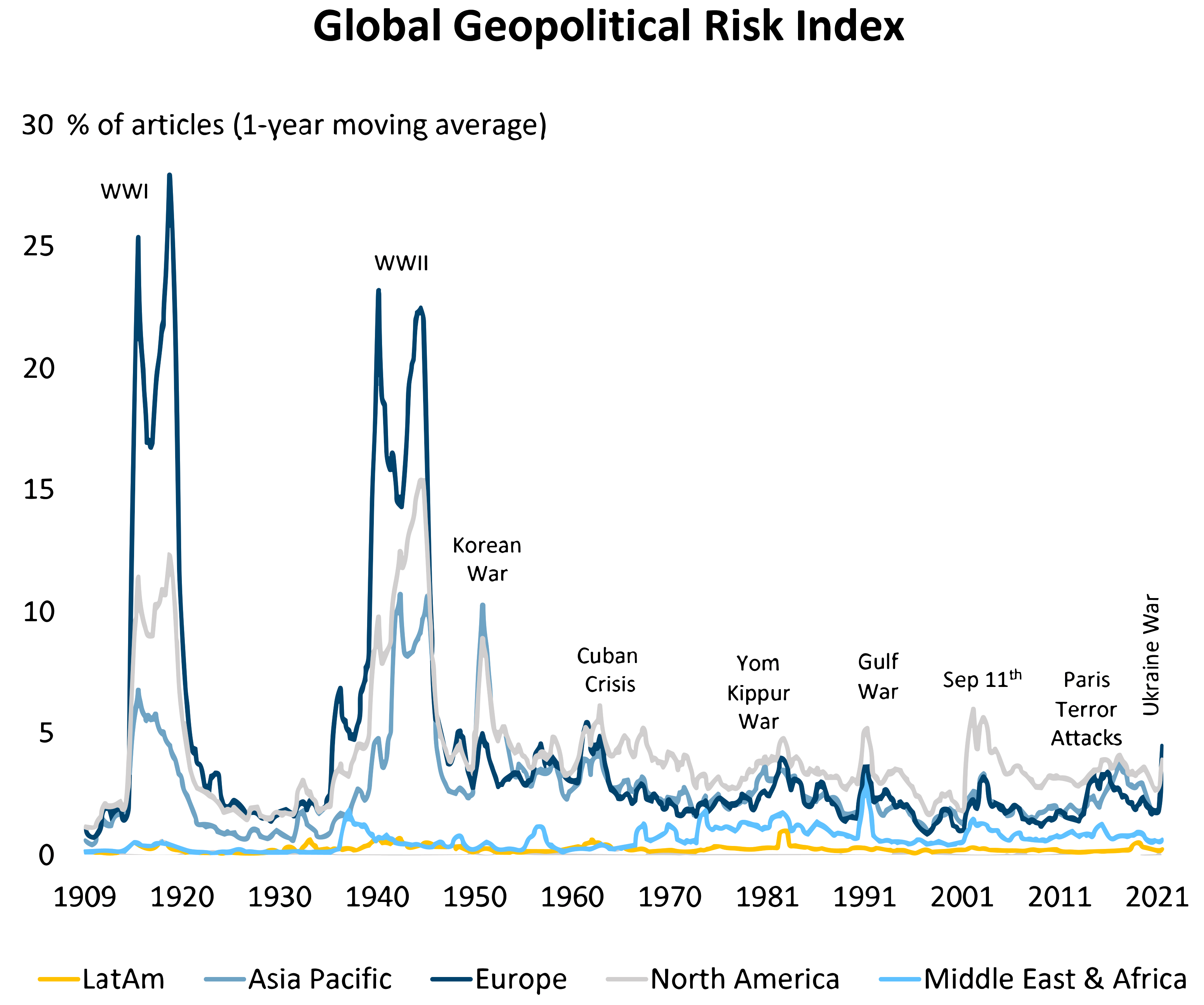

Measuring the risk is a multidimensional exercise, including a lot of variables. LATAM carries high political and economic risk, but the lowest geopolitical risk from all continents. The last continental armed conflict was The War of The Triple Alliance more than 150 years ago. The Falklands War does not count because the belligerents were Argentina and England. There have been border skirmishes between Columbia and Venezuela in the past, but they have been quickly resolved. The image below compares the geopolitical risks on all continents:

{kind=link}

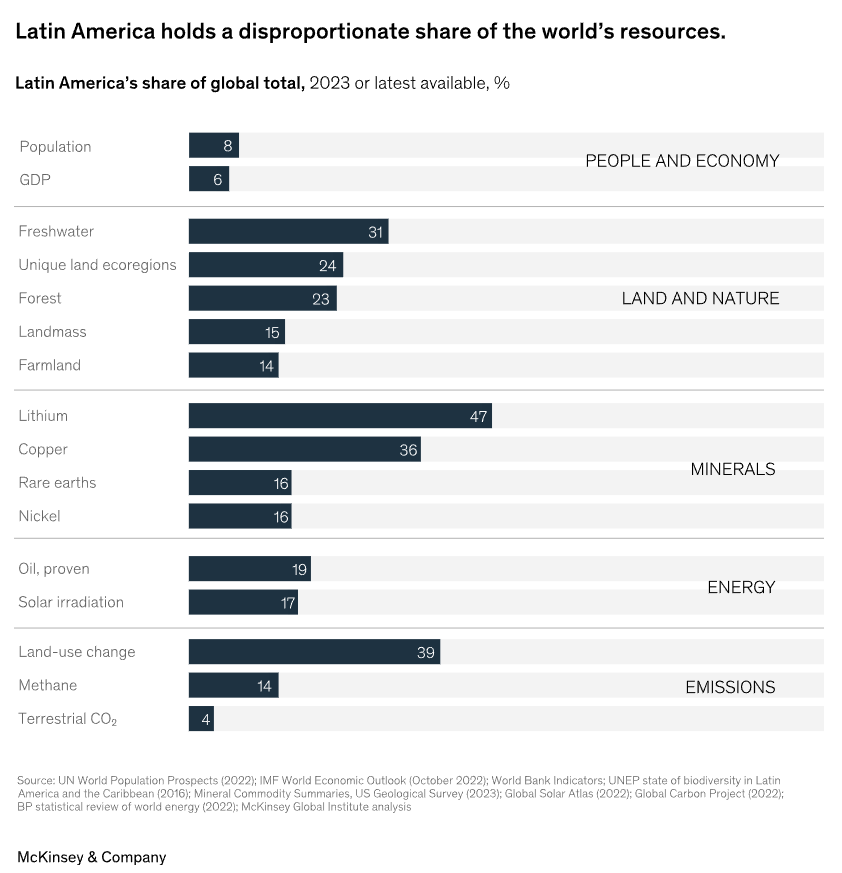

Global Macro investment thesis in one sentence: Latin America has a massive portfolio of assets on its balance sheet, bears the lowest geopolitical risk, and is valued at a significant discount. The chart below from McKinsey illustrates LATAM's abundance of natural resources:

{kind=link}

LATAM is among the wealthiest regions measured in resources per capita. Chile and Argentina host the largest lithium and copper deposits . Brazil is a leading agriculture exporter and host of the largest pre-salt oil reserves. LATAM has become increasingly important on the geopolitical map, considering the reshoring/friend-shoring trends and growing geopolitical tensions. It will attract significant investments. An example is Vaca Muerta, the second-largest shale oil basin in the world. Last June, Chevron announced a $500 million investment to develop Trapial block, part of the basin. Chevron's investment is just one example of the growing capital inflows to Latin America.

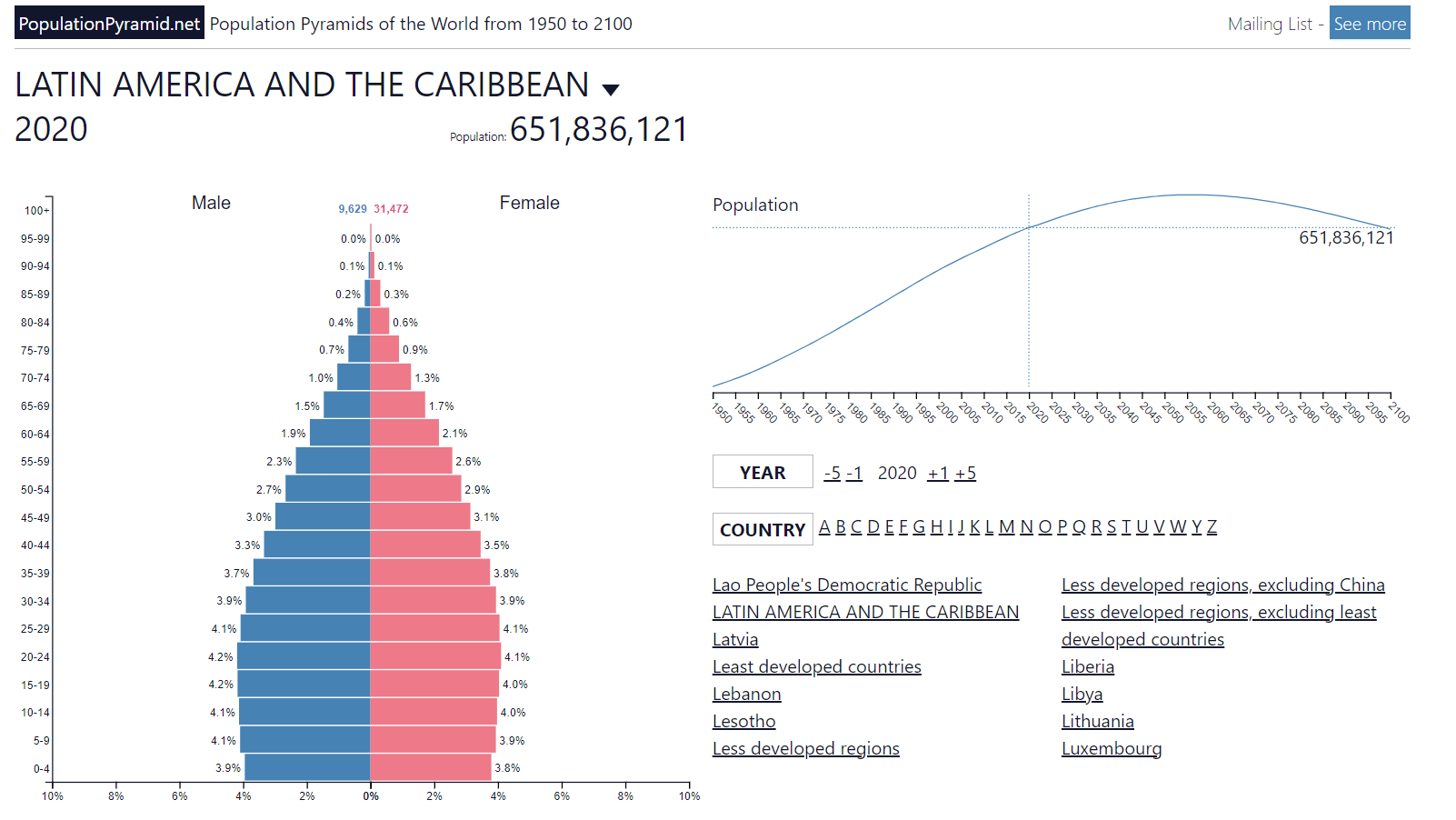

LATAM's demography is still good. Mexico and Brazil are among the biggest economies in the world and have robust population age structures. The image below illustrates the Latin American population pyramid.

{kind=link}

Latin American population structure is significantly better than that of China, Japan, and Europe. Only the USA has a healthy demography from G20 countries. Looking at the big picture, the Western Hemisphere has significant advantages over the rest of the world. Latin America will benefit greatly.

Alternative Asset Managers

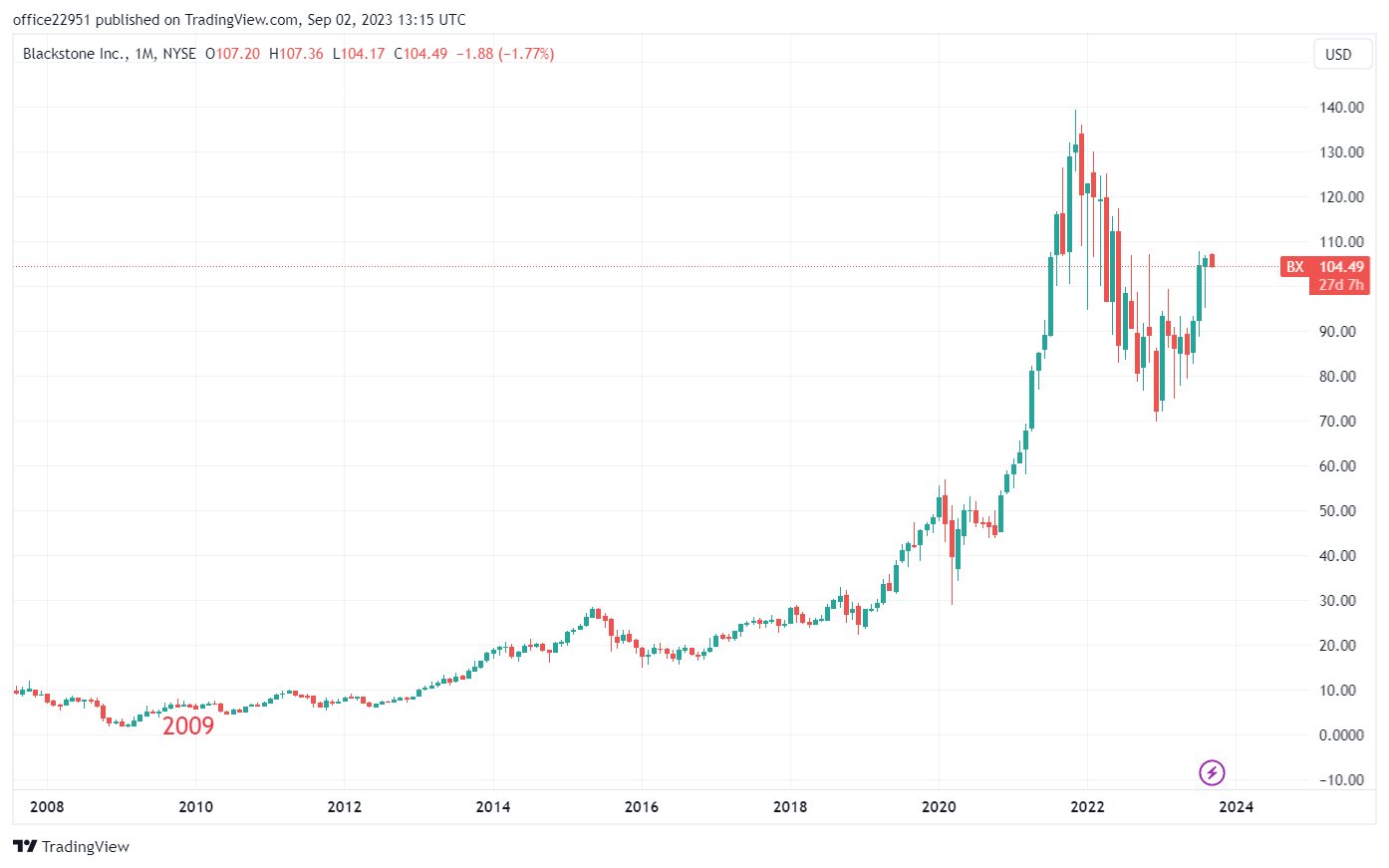

That means the company seeks opportunities in asset classes such as distressed debt, private equity, real estate, infrastructure, and collectibles. In recent years, alternative asset managers have become popular among sophisticated investors. A great example is Blackstone (BX). Its shares since 2009 realized x20 gains.

{kind=link}

The chart above is not an exception but a rule. Brookfield Corporation ( BN ) and Apollo Global Management ( APO ) achieved similar results to a lesser degree. The demand for alternative assets is apparent if we include collectibles such as cars, fine art, and watches. Watch Fund is an example of the discussed developments.

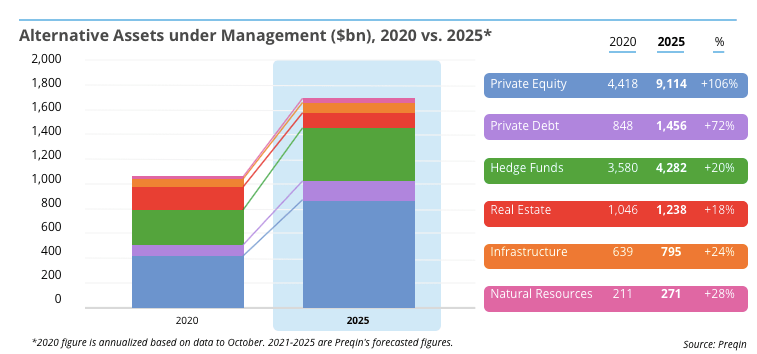

The alternative assets AUM are projected to reach $20 trillion in 2025. The table below illustrates the distribution of those gains among the asset classes:

{kind=link}

Being a client of an alternative investment fund is not achievable for the average investor. The minimum required investment varies greatly, but the lowest threshold is $100,000. This is not as bad as it seems. Instead of being customers, we can become shareholders in those funds. Being a shareholder often provides an even higher upside than investing as a customer.

Company Overview

Patria is a Brazilian alternative investment manager focused on Latin America. PAX represents the intersection between LATAM revival and the growing class of alternative investments. The company had an IPO in January 2021 and has grown its AUM consistently.

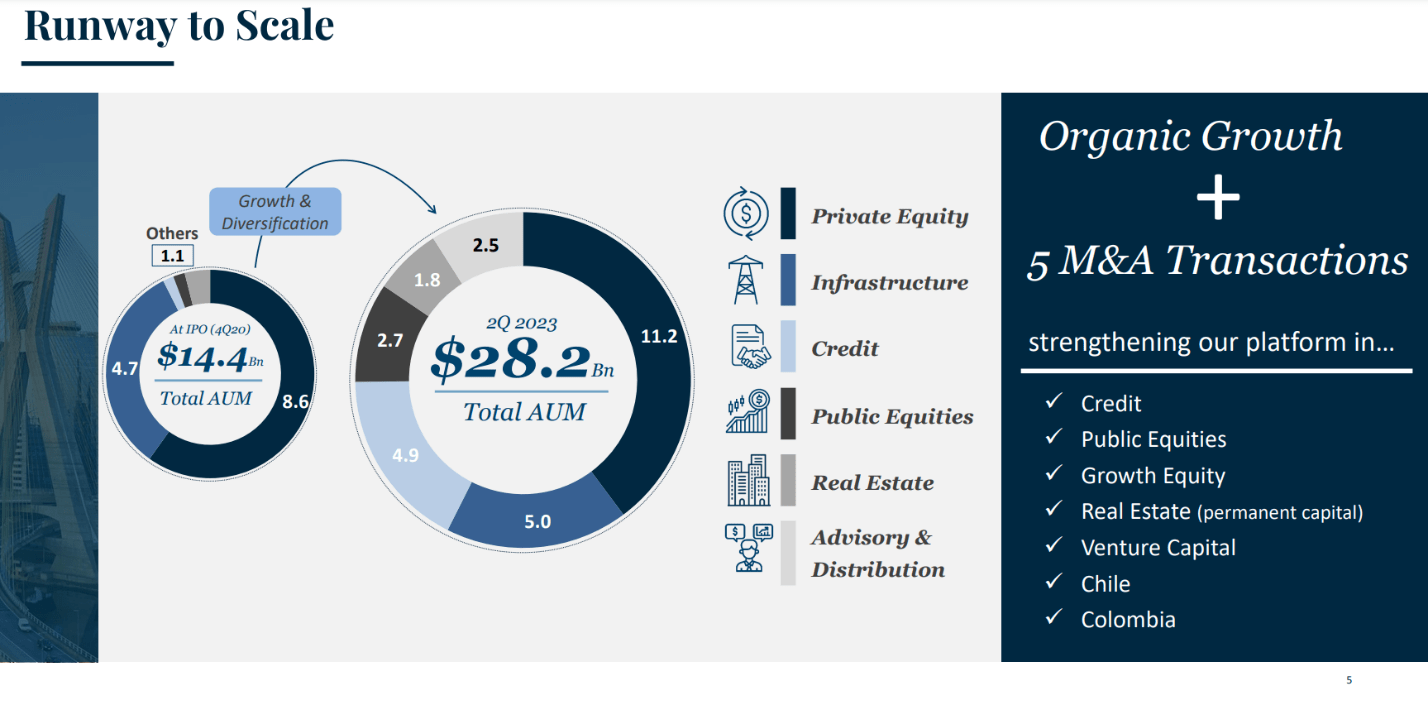

In December 2021, Patria acquired Moneda Asset Management, a Chilean company focused on Latin America. PAX AUM is $28.2 billion, and since the company's IPO, it has risen more than 300%.

{kind=link}

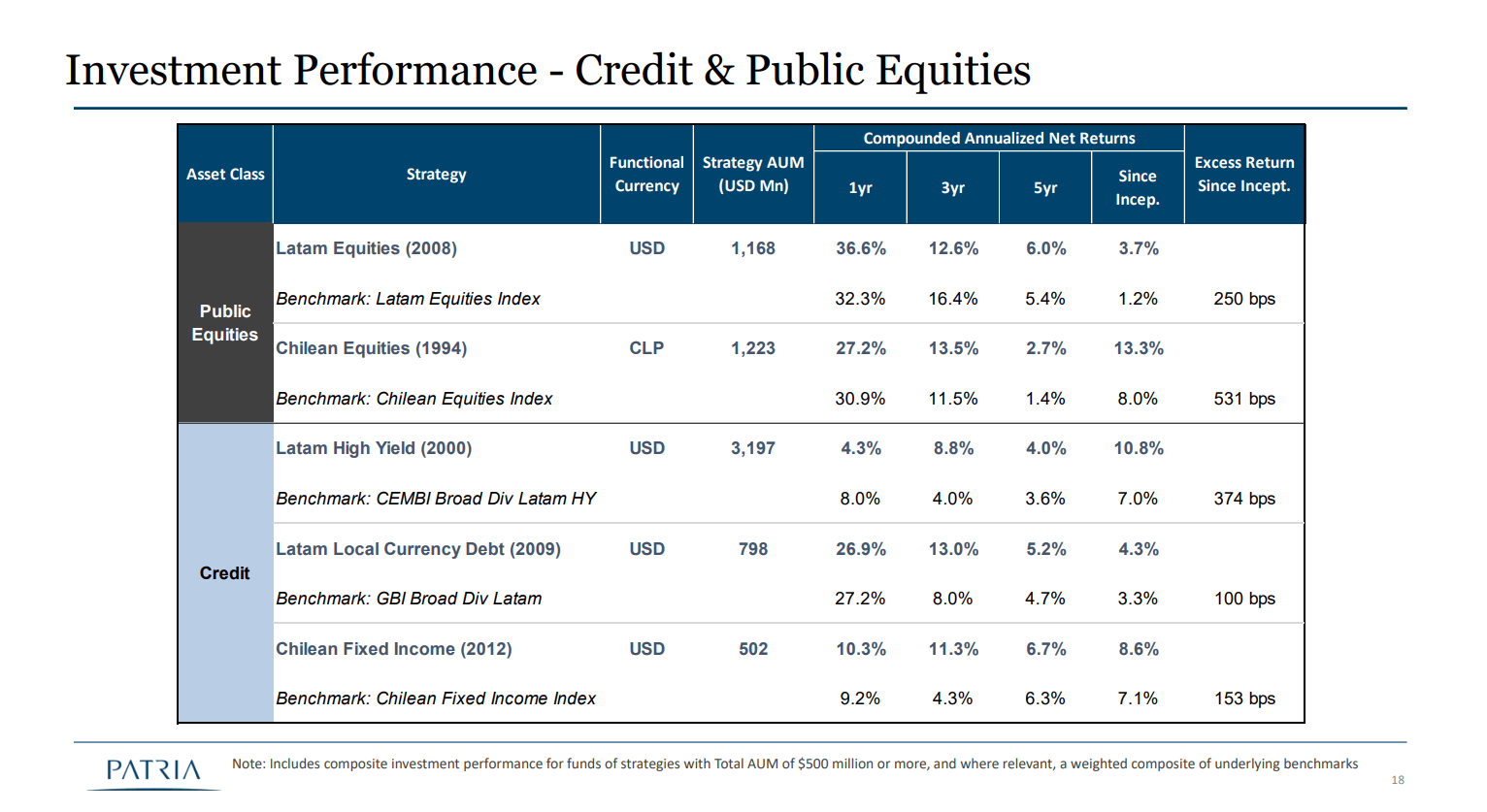

PAX's fund portfolio is focused on Public Equity, Infrastructure, and Credit. The company invests in real estate and public equities, too. PAX funds have been top performers in each category since their inception. The table below from the PAX Q2 presentation illustrates Public Equity and Credit funds' performance.

{kind=link}

All funds beat their benchmark indexes net of fees. The consistency of the performance is impressive, considering that some of the funds have been in operation for more than 20 years. Of course, past success does not guarantee a future, but it significantly increases the odds of solid performance.

Partnership with Bancolombia ( CIB ) adds $1 billion of permanent AUM, expanding PAX's capabilities to invest in Colombia. The new joint venture will be structured with 51% ownership of PAX and 49% by Bancolombia. The Colombian investments and savings market totals $145 billion, supporting the growing alternative assets management industry. The latter's share reached $10 billion and is expected to grow due to demand from institutional and private investors.

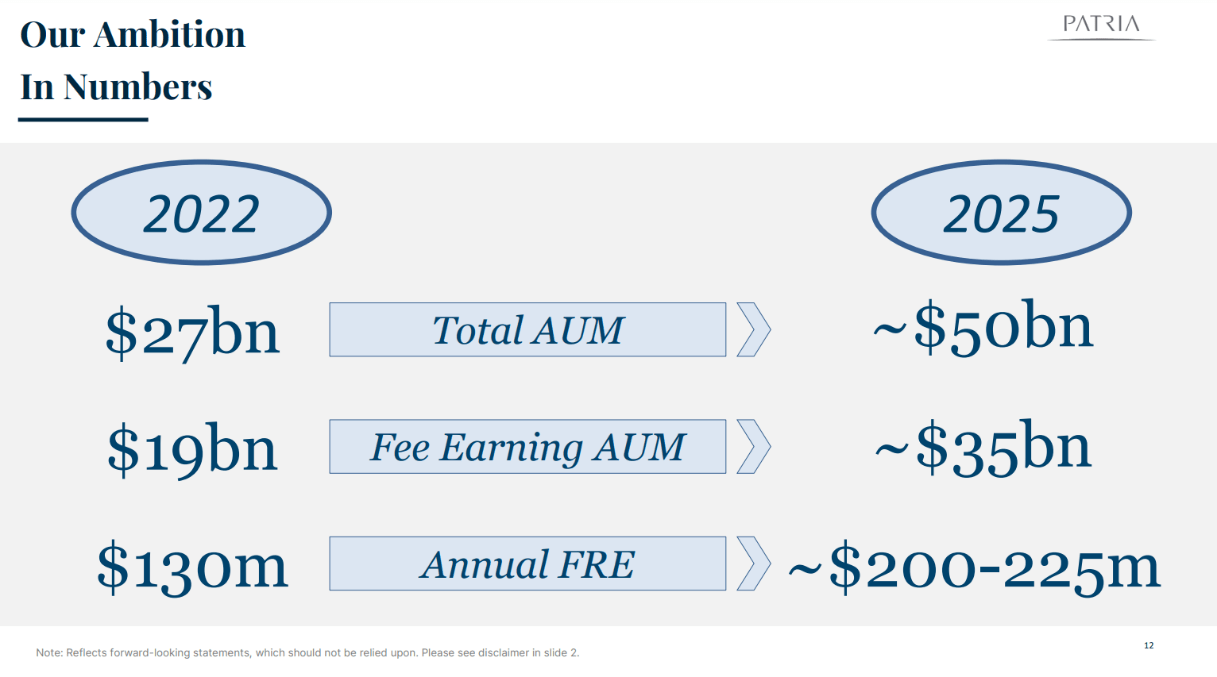

PAX has ambitious plans. The goals are achievable considering LATAM's potential, alternative investment growth, and PAX management expertise. The image below shows the 2025 company's targets.

{kind=link}

AUM growth will translate into higher recurring revenues. If the management maintains PAX's funds' net returns, the performance-related earnings will increase significantly, too.

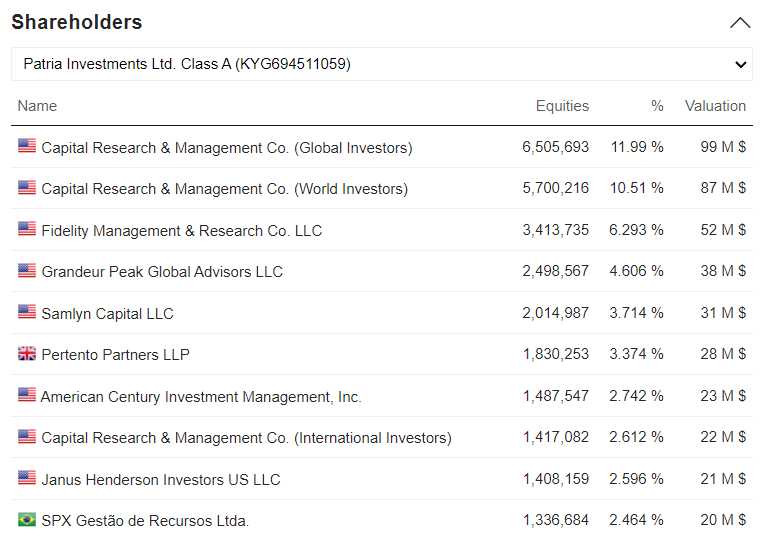

Blackstone backed PAX IPO in 2021. Their partnership started in 2010. Last year, they sold its shares. The current large investors are shown below:

{kind=link}

22% are held Capital Group subsidiaries. It is one of the largest financial service firms, with an AUM of $2.6 trillion. Other notable investors are Grandeur Peak Global Advisors LLC and Pertento Partners LLP. Those are boutique investment firms focused on small and mid-cap stocks.

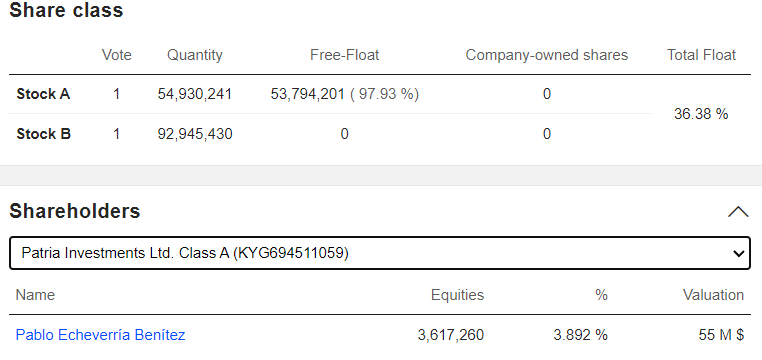

Pablo Echeverria Benitez, founder, and Chairman of Moneda, owns 3.89% of the company's stocks class A.

{kind=link}

Company Financials

Asset managers' balance sheets are easily deciphered because they are asset-light businesses. The PAX balance sheet offers downside protection due to the lack of debt. The table below illustrates the company's liquidity and solvency metrics. The data is from the PAX Q2 report.

| Quick ratio |

| 0.86 |

| Current ratio |

| 1.34 |

| Long-term debt/Equity |

| 26.9% |

| Total debt/Equity |

| 14% |

| Total liabilities/Total assets |

| 47% |

PAX has made a few acquisitions since its IPO, but the management did not sacrifice the company's solvency. The healthy balance sheet composition caps the downside risk in adverse scenarios such as fund withdrawals. PAX holds $22 million in cash and $205 million in short-term investments. The latter includes a trust account of Patria Latin American Opportunity Acquisition Corp. ( PLAO ) listed on NYSE. It is a Patria SPAC vehicle. PAX has sufficient funds to continue its expansion plans.

Measuring the profitability of an assets manager requires dissecting its earnings structure. They are a function of fee-related earnings and performance-related earnings. The former is the recurring income based on AUM, and latter, performance dependent. The data is from the PAX Q2 report and Seeking Alpha company profile. All parameters are TTM.

| Fee-related earnings /EV |

| 5.2% |

| Performance-related earnings/EV |

| 1.5% |

| Gross Margin |

| 62% |

| FCF Margin |

| 15.6% |

| ROE |

| 20.7% |

| ROI |

| 14.5% |

| Net Income per employee |

| $290, 020 |

PAX excels on all metrics against its peers. However, the numbers are lower compared to PAX's 5Y average. The last report shows rising FRE and PRE following increasing revenues. The expenses have grown, too, and the profit margins remain steady.

{kind=link}

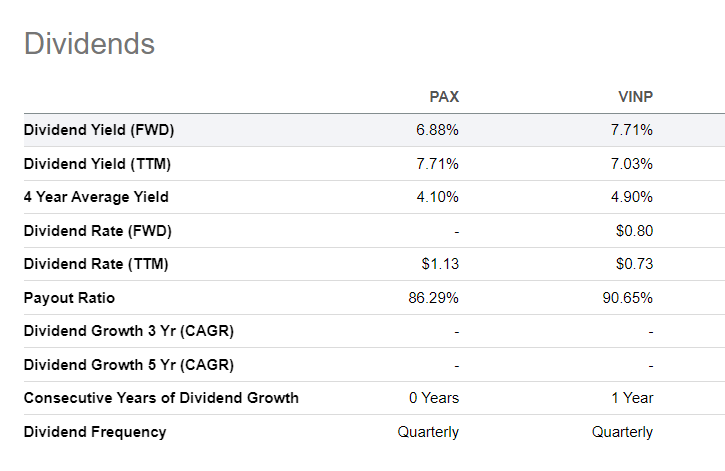

In the long term, PAX will achieve its goals by increasing revenues while maintaining FRE margins of 55-60%. The distributable earnings will grow, too, and the shareholders will benefit from dividends. The table below compares PAX and Vinci Partners ( VINP ) dividend metrics.

{kind=link}

Both companies offer similar yields and distribute dividends quarterly. In its last presentation, the company projects the distributable earnings per share to double. The growing importance of dividends is another factor that makes Patria an attractive proposition.

Valuation

I use the Dividend Discount Model and relative valuation against similar companies to estimate assets management firm value. The metrics I use are EV/AUM, EV/Sales, and EV/FRE.

To calculate PAX value with the Dividend Discount Model, I have to measure the price of the company's equity and levered beta.

To obtain those numbers, I use the following steps and assumptions:

- Risk-free rate equals the 5Y average of USA long-term Government bond Rate, 2.2%.

- Growth rate, g, equals the 5Y average of the USA long-term Government bond Rate, 2.2%.

- Brazil's equity risk premium is 9.57%.

- Asset managers' unlevered Beta 0.41.

- PAX Debt/Equity ratio 2.5%.

- Brazil's effective tax rate is 35%.

- PAX dividend ((TTM)) $1.13

1. Calculate Levered Beta with the formula below:

Levered Beta = Unlevered Beta * (1+D*(1-T)/E).

2. Calculate the discount rate (discount rate as the cost of equity) using the resulting value for leveraged beta. The formula I use is:

Cost of Equity = Risk-Free Rate + (Levered Beta * Equity Risk Premium).

3. Calculate the Terminal Value of dividends considering the Cost of Equity and Expected dividend growth:

Terminal Value = Dividend per share * (1 + expected dividend growth) / (Cost of Equity – Expected Dividend Growth)

4. Calculate the Present Value of Terminal Value assuming a constant discount rate for ten years.

For PAX, I get the following results:

Intrinsic value per share = $12.86

Current market price = $14.60 (09/01/2023)

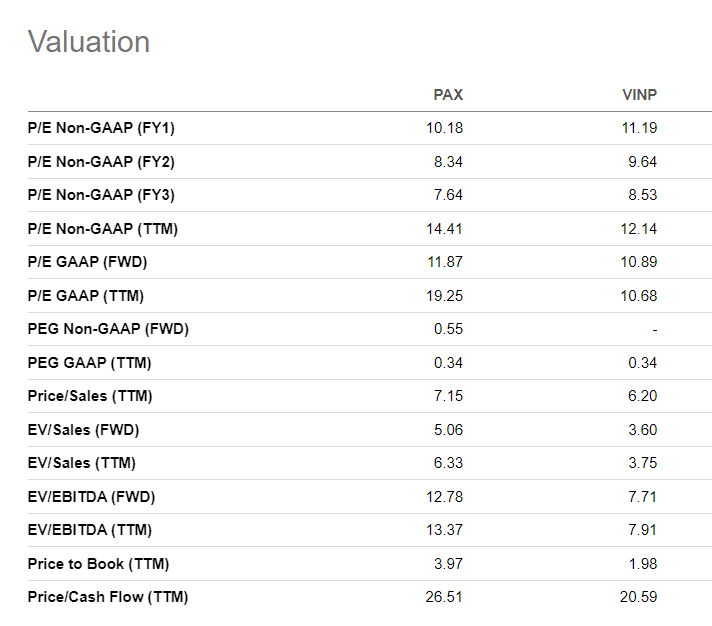

Estimating PAX's relative value is challenging due to the lack of direct competitors similar in market cap, AUM, and region. Comparison with Blackstone or even Blue Owl ( OWL ) is like weighing up apples and oranges. I use Vinci Partners Investments Ltd. ((VINP)). They are Brazilian alternative asset managers focused on LATAM.

{kind=link}

Using EV/EBITDA and EV/Sales PAX is more expensive. Another metric I like to use is EV/AUM and EV/FRE. The former estimates how much I pay for every dollar in AUM. PAX EV/AUM is 9.5%, and VINP is 4.6%.

EV/FRE measures how much I pay for every dollar enterprise value per dollar fee-related earning ((FRE)). It is like EV/EBITDA but counts the core sources of company profits, the fees. PAX EV/FRE is 18.8, and VINP is 15.5. These numbers confirm my conclusion PAX is expensive at this price level.

Risks

Asset management carries a few significant risks: liquidity, market, and economic risks. PAX is focused on LATAM, hence adding internal politics as a risk. Now, let’s look at every risk in detail.

The liquidity risk represents the adverse consequences of declining AUM. Increasing withdrawals drain the fund's capital, thus affecting its ability to achieve its goals. The investor decides to withdraw funds when anticipating unfavorable economic and market developments. Expectations for recession are associated with a potential bear market for commodities. Latin American economy is highly exposed to commodities.

I expect a strong decade for commodities and emerging markets. The chronic underinvestment in all commodities guarantees high prices in the future. The impact of the CAPEX cycle on commodity prices is among the few sure things in the markets. Copper, lithium, crude oil, and natural gas are primary exports for the region. My projection is their prices will increase notably in the next five years.

Market risk is more pronounced. A significant event, such as a global credit event caused by the steep interest rate hikes, will initiate selloffs. The unprecedented interest rate increase in 2022 will affect corporations relying on cheap money to survive. According to experts in the distressed debt industry, we are approaching the beginning of a new cycle of corporate defaults. For alternative asset managers, this could be a blessing. PAX has 16% of its AUM invested in distressed debt. Another round of bankruptcies will offer assets on fire sale, providing an opportunity to buy dollars for pennies. On the other hand, Private Equity has a relatively high correlation with the public equity markets. Hence, a market panic will adversely affect the PAX portfolio private equity component.

As I said earlier, LATAM is the most peaceful continent with the lowest geopolitical risk. Such cannot be said for the internal politics. The political pendulum swings abruptly and now moves from left to right. Argentina is an example. PAX has mitigated the internal political risk, focusing on Chile, Brazil, Mexico, and Colombia. They represent the lowest risk and uncertainty in the region. I would be delighted if the company expanded its investment activities in Uruguay. Uruguay is among the leading countries in LATAM according to metrics such as ease of doing business, crime levels, and standard of living.

Conclusion

PAX is an overlooked asset manager, offering exposure to two emerging investment themes: LATAM and alternative investments. The company's business is expected to grow due to increased interest in Latin America as an investment opportunity. The continent has an abundance of natural resources and strong demography. LATAM economy will benefit significantly from the nascent commodities bull market.

The acquisition of Moneda improved the company's portfolio and increased AUM. The latest joint venture with Bancolombia opened new investment opportunities in Colombia. PAX has a healthy balance sheet with sufficient liquidity to expand its operations further. The company management has proven its capabilities to extract Alpha. Its funds consistently outperform the benchmarks.

In a decade with rising interest rates, the appeal of dividends is growing. PAX offers an attractive dividend. In its last presentation, the company projects the distributable earnings per share to double.

I give a buy rating despite the stock being overvalued based on the Dividend Discount Model. Investment in PAX is a long-term bet on LATAM with at least 24-month horizon. The current market price is an opportunity to start building a position and then use the price dips to add more exposure.

For further details see:

Patria: Bet On Alternative Investments And LATAM