PAX - Patria Investments: Another South American Company That Income Investors Might Find Attractive

2023-03-21 09:00:00 ET

Summary

- Patria Investments is a private equity business focused on South America with a market cap of $2.1B.

- The company has over $27B in AUM, a figure that I think can grow for years to come.

- Shares have a P/E just under 14x, and the company is expected to grow earnings at double digit rates for several years.

- The company has a trailing yield just under 6%, but it's hard to project what this year's payout will be with their lumpy dividends. I do think that the dividends will increase over the next 3-5 years.

- I have a small position today, but I will be looking to add to my position in coming months.

I have been looking at investments outside of the US because many of the large companies trading on American markets look expensive outside of a couple specific companies that I have been pounding the table on, like Peabody Energy ( BTU ), Transocean ( RIG ), and Tidewater ( TDW ). I think South America is a particularly attractive alternative, and I have started to put money to work in markets there. Ecopetrol ( EC ) and Petrobras ( PBR ) ( PBR.A ) are my two largest positions in South American companies, but I own a tiny chunk of shares in Patria Investments ( PAX ). The company is relatively new to public markets, but if they can follow the private equity roadmap of North American companies like Blackstone (BX), Patria has the potential to be a compounder that might be worth owning for years to come.

Investment Thesis

South America has some interesting characteristics that I think will attract investors in coming years. I have been adding to positions in different stocks, but I think Patria Investments represents an interesting opportunity to invest in a high-quality asset management business focused on South America. The company has impressive margins and a solid balance sheet, and AUM continues to grow. The company has an attractive valuation with an earnings multiple just under 14x, and the company also pays a nice dividend which has potential to grow significantly as their AUM grows. I have a small position for now, but Patria is on my short watchlist as an interesting opportunity that has the potential to generate impressive total returns.

Annual Results

It’s a pain to hunt down annual results for Patria, but I wanted to go over them briefly to give investors a general idea of the company. Patria is a private equity firm focused on South America. They have grown significantly in recent years, and I think we will see AUM and earnings grow over the long term. The company had just over $147M in distributable earnings for 2022, but I would recommend investors interested in the company go take a look at the recent investor presentation which includes a lot of information about the business results. As long as AUM continues to grow, I think Patria could be an interesting opportunity to buy a high margin business with a long growth runway.

{kind=link}

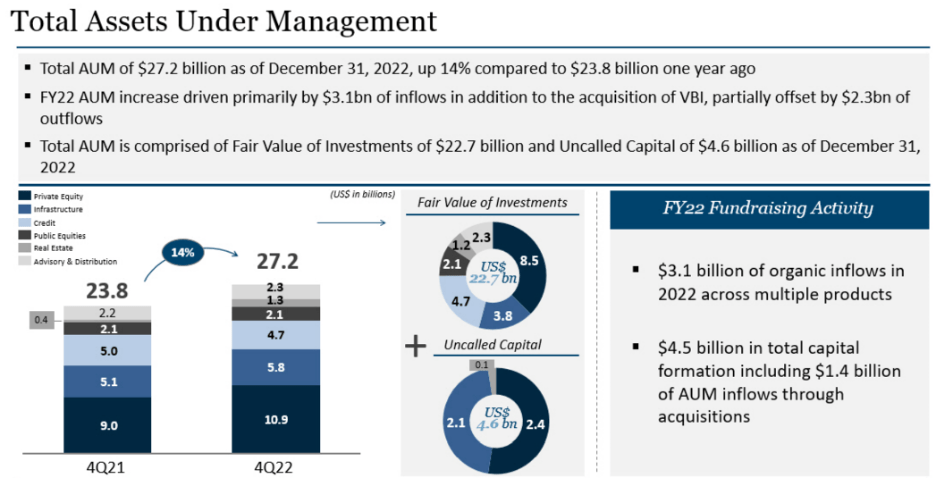

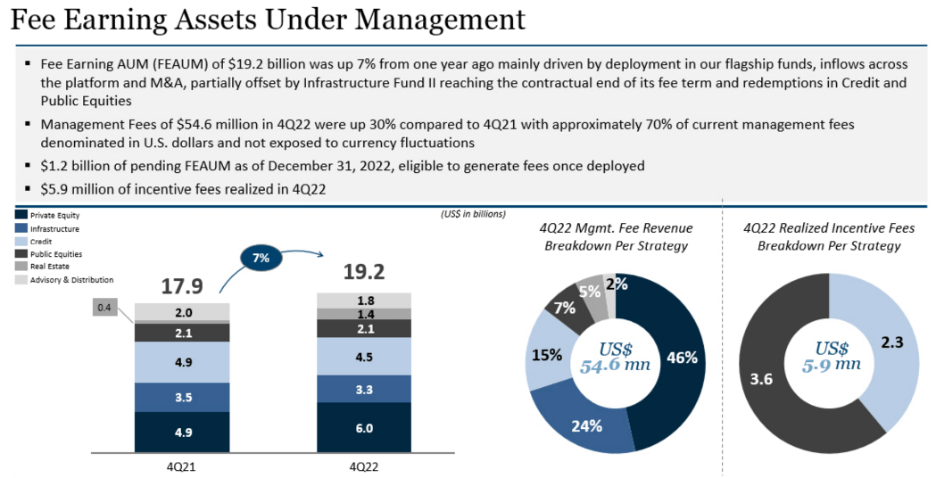

Patria had total AUM of $27.2B, up 14% from last year. Their largest segment is private equity, but they also have significant exposure to infrastructure and credit. Public equities, real estate, and advisory & distribution account for a smaller portion of AUM. Management fees differ depending on the segment, but on average their management fee is a bit over 1%. Their fee earning AUM was $19.2B, up 7% from last year.

{kind=link}

Patria has a market cap of $2.1B, so it isn’t the smallest company out there, but I think that there is potential for significant AUM growth for years as South America looks like a pretty attractive investment geography for the next decade. The valuation looks cheap today, especially if the company can grow as fast as the estimates.

Valuation

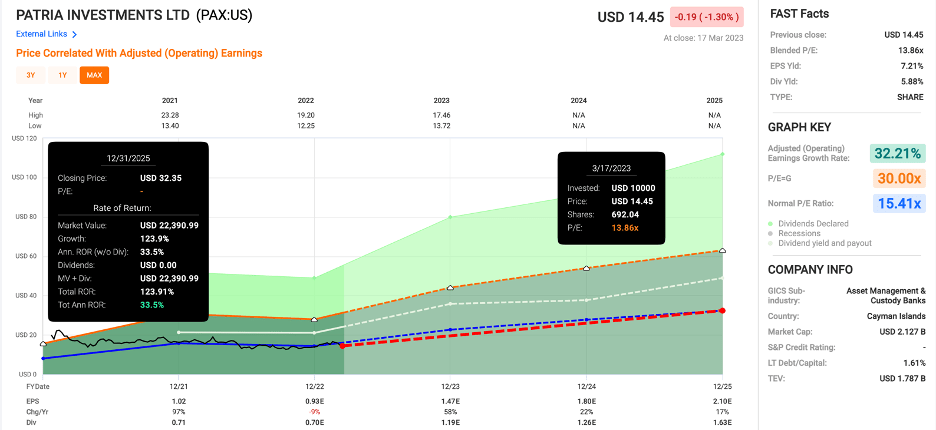

Shares of Patria have bounced around between $12 and $18 over the last year. Shares currently have an earnings multiple of 13.9x, and growth is expected to be impressive over the next couple years. I wouldn’t count on multiple expansion, but estimates are projecting double digit growth through 2025, so buying shares at the current valuation looks like a good risk/reward proposition.

Price/Earnings (fastgraphs.com)

{kind=link}

There are some things worth considering when you look at the valuation outside of the growth estimates. The first is the margin profile of Patria. The company already has impressive margins, but as AUM grows, I wouldn’t be surprised to see some margin expansion in coming years. The company also has a solid balance sheet and a nice dividend to boot.

The Dividend

In my last article on Patria, which was almost a year ago, I talked about the potential dividend growth due to the small size of the business. One thing that has become obvious with the dividend is that it won’t grow consistently. They had a couple hikes leading into that article, with smaller payouts for a couple quarters after that. The company declared a dividend of $0.308 for the most recent quarter, a nice quarterly payout for a stock trading below $15. The dividend actually gets paid tomorrow. Over the last four payouts, Patria paid investors $0.85, for a trailing yield of 5.9%.

The lumpy dividend payouts are more typical of international companies, but it is difficult to project what dividends will look like moving forward. One thing that is nice about Patria’s dividends is that there is no dividend withholding tax. Like I said, I don’t want to make too many assumptions about Patria’s dividend over the next 12 months, but I think we will see a yield of at least 4-5%. Over the longer term (3-5 years), I think we will see dividend growth for Patria, even if the quarterly payouts remain lumpy.

Conclusion

While American stocks have dominated for years, that has left some of the most popular stocks with rich valuations. International markets have cheaper valuations on average, and depending on the company, the growth potential is much better. I think Patria is one of those companies. They already have over $27B in AUM, a number that I expect will continue to grow for years to come. As AUM grows, I wouldn’t be surprised to see margin expansion, and the company already has a solid balance sheet.

Shares have been cheaper at times over the last year, but I think the risk/reward looks good for long term investors with shares trading under 14x earnings. I am a bit skeptical that the company can grow earnings over 50% next year like the FastGraphs 2023 estimate, but I think double digit earnings growth for several years is realistic. The company has a trailing yield of nearly 6%, but it’s hard to project the payout moving forward due to the lumpy dividend payouts. On a longer time horizon, I do think that the annual dividend has the potential to grow significantly. I own a small position right now, but I will be watching Patria stock closely and I plan to add shares in coming months.

For further details see:

Patria Investments: Another South American Company That Income Investors Might Find Attractive