LCII - Patrick Industries: The Ride Higher Isn't Over

2024-01-04 10:24:11 ET

Summary

- RV and construction markets have been heavily impacted by inflation, high interest rates, frontloading, and economic uncertainty.

- Patrick Industries, a company that supplies components for RV and construction industries, has seen its stock rise 31% since July 2023.

- Despite declining revenue and weakening fundamentals, the long-term outlook for Patrick Industries remains positive due to expected recoveries in the RV and housing markets.

Inflationary pressures, high interest rates, a significant amount of frontloading, and economic uncertainty have all coalesced to create the perfect storm for some industries. Few spaces have been hit as hard over the past year or so as the RV (recreational vehicle) and construction markets. Fundamentally speaking, businesses that are engaged in either or both markets have suffered. A great example of this can be seen by looking at Patrick Industries, Inc. ( PATK ), which produces and sells components that are used in the construction of RVs and marine products, and also products that are used in the construction industry for housing and other uses.

Even in light of a weakening fundamental picture, shares of the company have rocketed higher over the past few months. Since I last reiterated my "buy" rating on the stock back in July of 2023, the stock is up a whopping 31% at a time when the S&P 500 (SP500) has risen only 7.5%. In that article, I acknowledged that there was weakness in the market that was likely to continue. However, I also believed that shares were cheap and that the long-term outlook for the company and its investors would be positive. And since my first bullish article on the firm in 2022, shares are up 50.9% compared to the 6.9% rise seen by the S&P 500. Fast forward to today, and I recognize that the easy money has been made. Even so, I would argue that additional clarity in the market makes me more confident than I was previously. And when you weigh the data objectively, it's difficult to be anything other than bullish about this particular opportunity.

An interesting ride so far

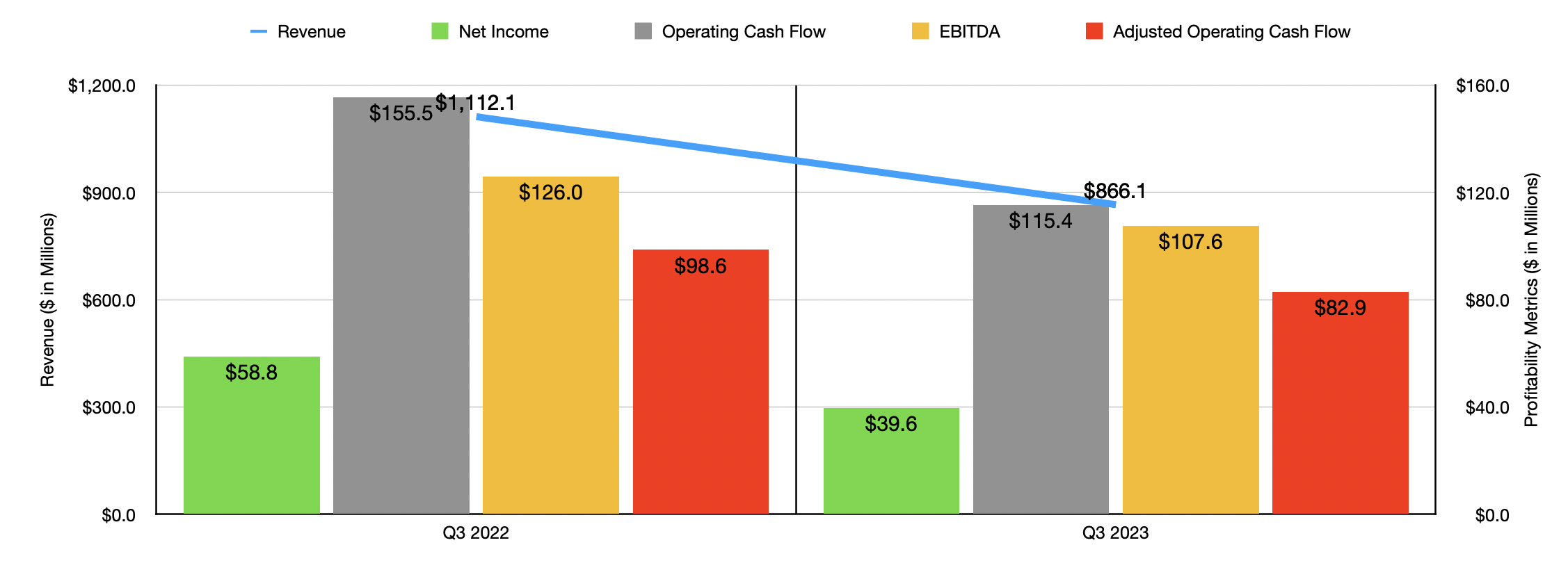

If you were to look solely at the fundamental picture regarding Patrick Industries, you might be scared away. To see what I mean, let's touch on financial performance for the latest quarter . This is the third quarter of the 2023 fiscal year. During that time, revenue for the company came in at $866.1 million. That represents a decline of 22.1% compared to the $1.11 billion generated the same time last year.

There are multiple drivers behind this drop in revenue. For starters, management said that a reduction in wholesale unit shipments in the end markets in which it operates, combined with lower pricing, more than offset market share gains to push revenue lower. In particular, RV market sales dropped by $123.5 million, equating to roughly 24%, because of a drop in production by its RV OEM clients. A similar decline of 24%, amounting to $65.9 million, involved the marine products that the company sells. That drop is due to a wholesale shipment decline.

When it comes to the manufactured housing market that the company plays into, revenue dropped 17% thanks to a reduction in demand for housing, combined with higher inflation and borrowing costs. Meanwhile, industrial sales declined about 19% that management chalked up to a slowing down of housing starts over the span of two quarters.

{kind=link}

Although I have not dug into the marine market on its own all that much, I have touched on both the housing market and the RV space. I would recommend that you read a couple of my housing-related articles, such as this one and this one .

In short, in early 2022, I was rather bearish about the housing space. I saw the writing on the wall and felt as though we would be in for a decline in the market that would last for a year or two. I was pleasantly surprised when, halfway through 2023, I had to back away from that bearish narrative. Although backlog and orders had plunged while cancellation rates surged, as the year progressed, new orders started to flood in. That trend continues today.

{kind=link}

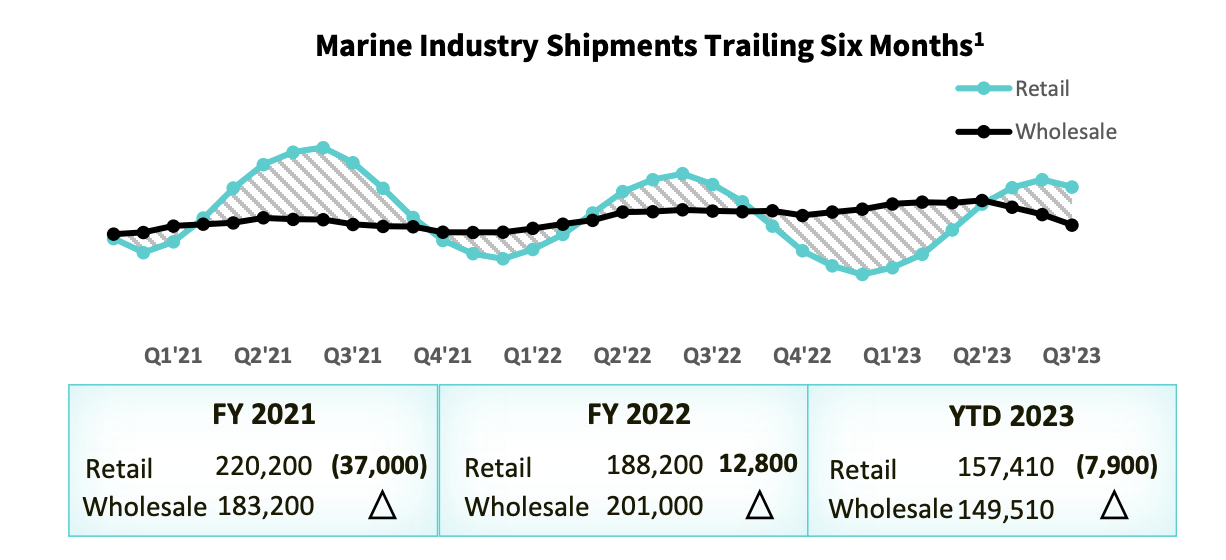

When it comes to the marine industry, we only have data covering through the third quarter of 2023. But that data does not look all that bad. Shipments, using a trailing 6-month approach, don't seem to be down all that much, especially compared to the other markets in which Patrick Industries operates. And with this particular space accounting for 28% of the company's revenue, it's nice to see some relative stability that isn't present elsewhere for the enterprise to enjoy.

{kind=link}

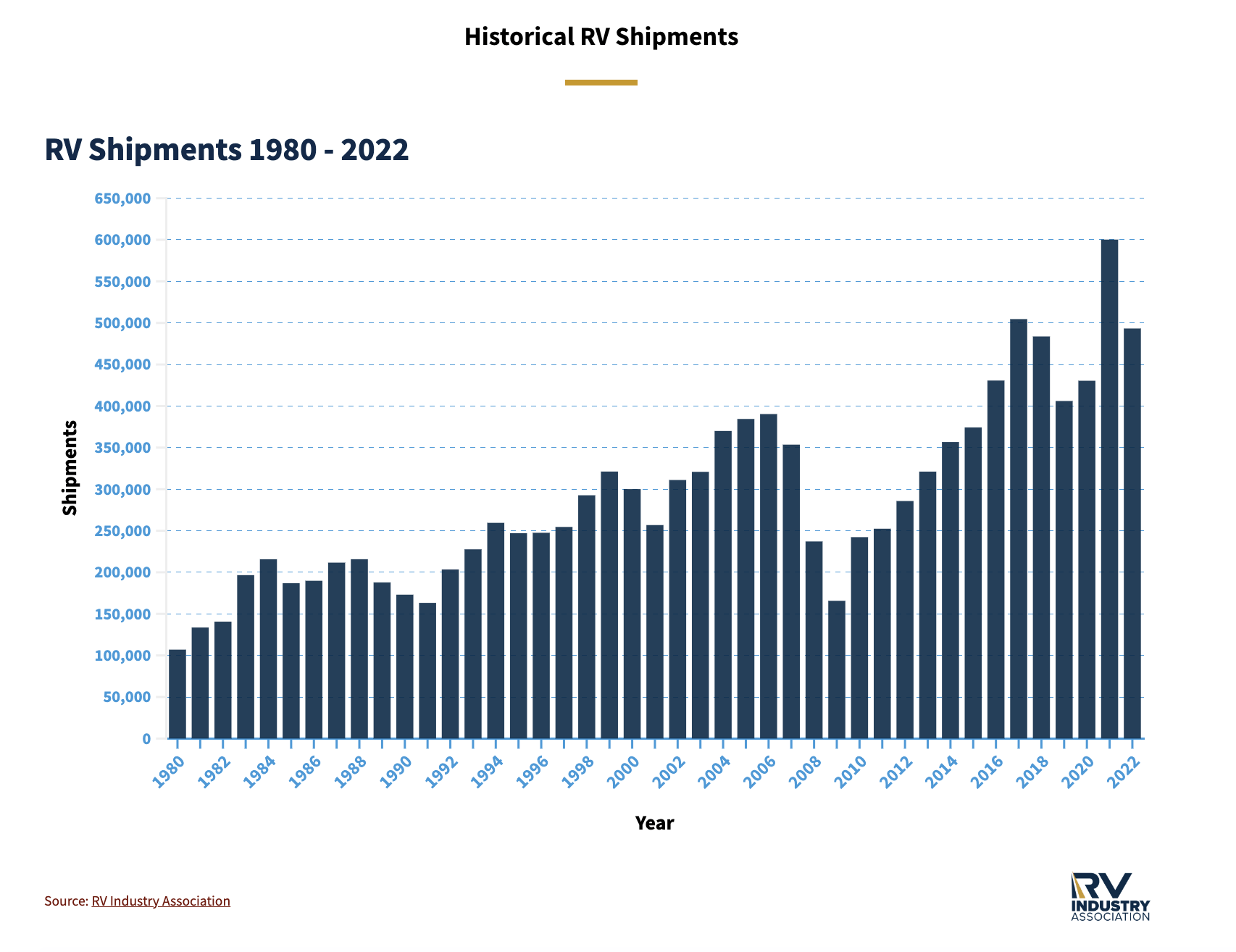

The RV market has also been stubborn. During the pandemic, years worth of additional demand was pulled to what was then the present day. This was caused by a greater desire to engage in social distancing, combined with economic stimulus that made purchasing an RV easier. Low interest rates at the time also helped in this regard. As you can see in the chart above, there was a spike in shipments to 600,240 in 2021. That's significantly higher than the 451,089 shipments that were averaged per year in the five years leading up to that point.

Although official data is not out yet for 2023, the RV Industry Association estimated last year that total shipments for 2023 would come in at a midpoint of 307,700 units. Naturally, this would hurt any firm in this space. The good news is that a recovery is forecasted to already be in the works. The current expectation is for us to see around 350,000 units this year.

{kind=link}

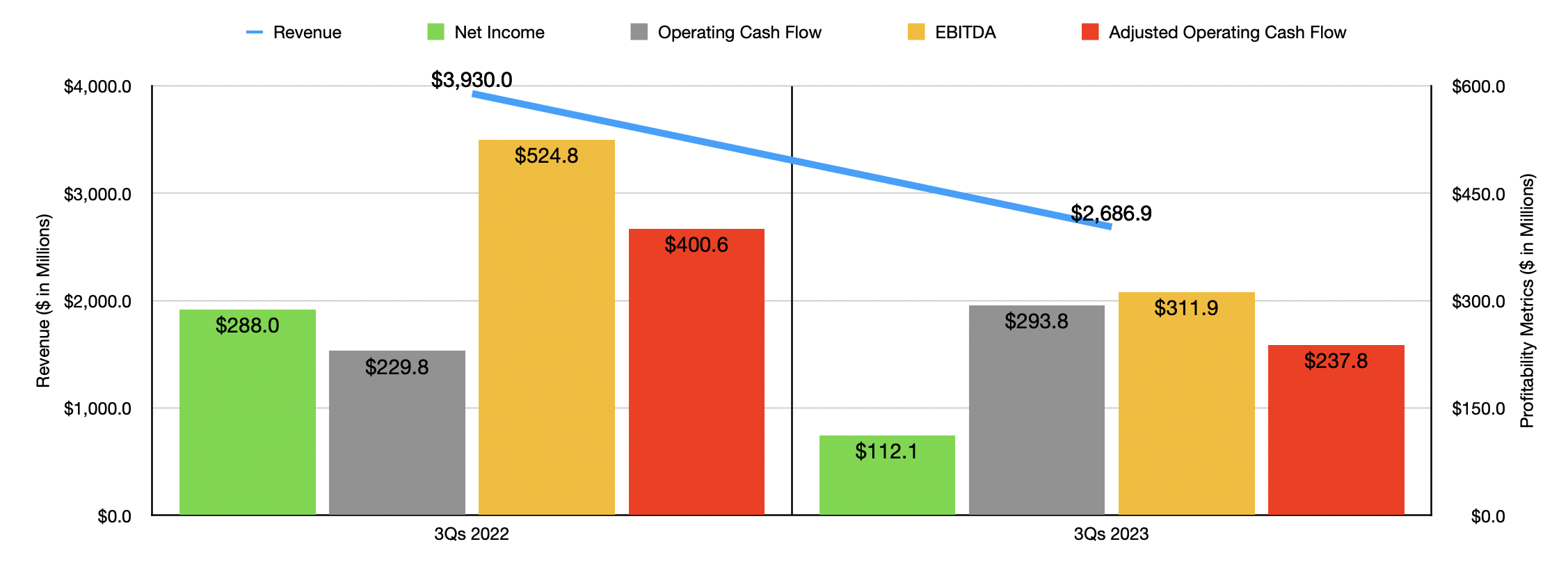

It is this optimism regarding 2024, and likely what should be an even better year in 2025, that has caused shares of Patrick Industries to rise nicely in recent months. Because, as you can see in the chart above, financial performance for the first nine months of 2023 was substantially worse than what it was during the same time in 2022, indicating that the third quarter on its own was not just a blip on the radar.

Unfortunately, management has not provided a real forecast as to what financial performance should look like for 2023 in its entirety. But based on my own estimates, net profits should be around $127.7 million, while adjusted operating cash flow should be $280.4 million. Meanwhile, EBITDA should come in somewhere around $382.2 million.

{kind=link}

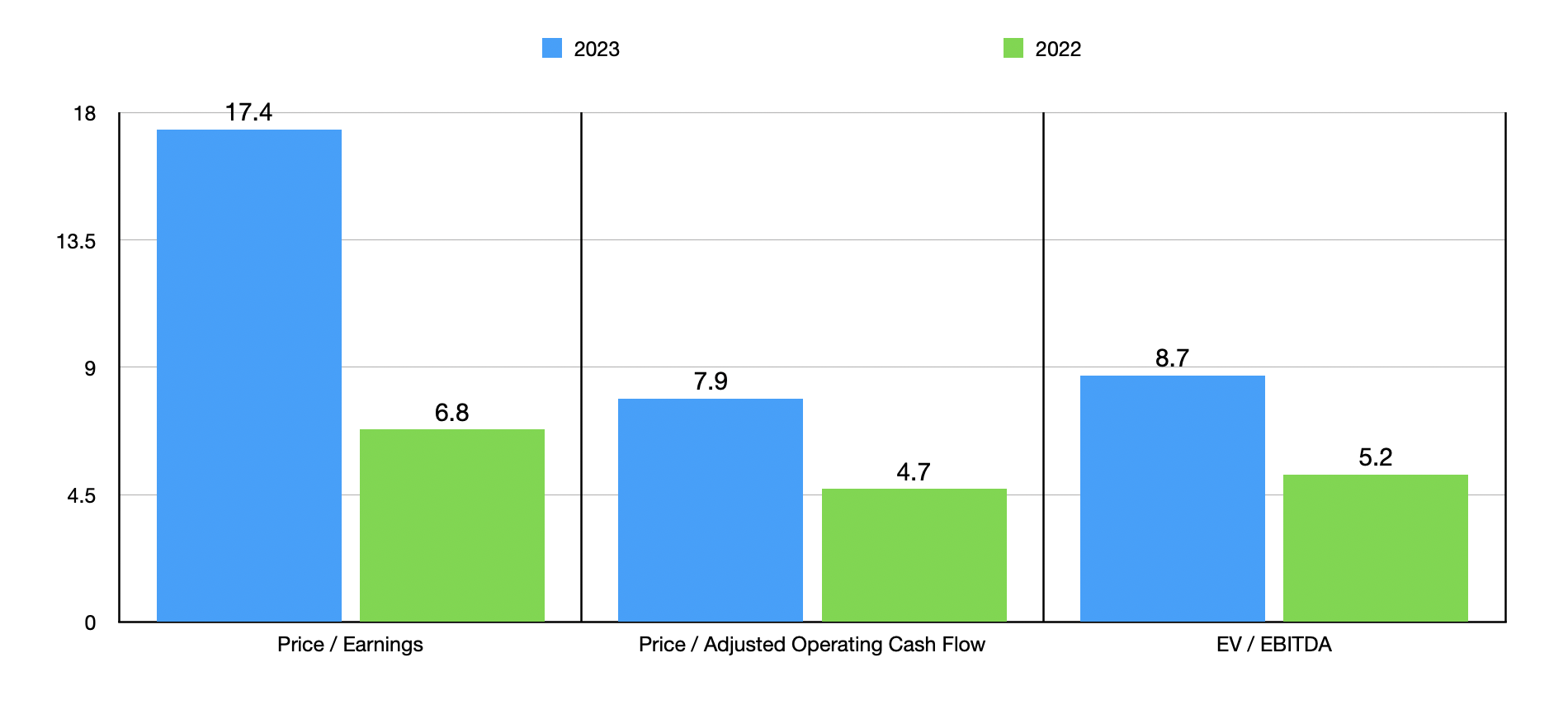

Using these figures, I was able to value the company as shown in the chart above. This shows data for about 2022 and 2023. Even if the 2023 estimates come to fruition, I would argue that, relative to cash flow at least, shares of Patrick Industries are incredibly cheap. Clearly, they aren't as attractive as they were before the rise. But they are attractive enough to warrant a good degree of optimism.

I then decided, as shown in the table below, to compare the company to five similar firms. What I found is that, using the price to earnings approach and the EV to EBITDA approach, one of the five companies was cheaper than Patrick Industries. Meanwhile, using the price to operating cash flow approach, only two of the five firms ended up being cheaper.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Patrick Industries |

| 17.4 |

| 7.9 |

| 8.7 |

| LCI Industries ( LCII ) |

| 64.8 |

| 6.3 |

| 17.7 |

| Modine Manufacturing ( MOD ) |

| 15.5 |

| 19.7 |

| 12.2 |

| American Axle & Manufacturing ( AXL ) |

| 20.2 |

| 2.1 |

| 4.7 |

| Gentherm ( THRM ) |

| 96.5 |

| 21.2 |

| 18.5 |

| XPEL Inc. ( XPEL ) |

| 30.4 |

| 36.4 |

| 20.4 |

Takeaway

As things stand, I can understand why some investors might be concerned about putting their money into Patrick Industries. Fundamental performance continues to worsen. In addition to this, shares are more expensive than they were last year. Even with that being the case, however, the stock is incredibly cheap and we are in the early stages of a turnaround for at least two of the three markets in which it operates. Combined, these two markets comprise 72% of the company's revenue. The other 28% of market exposure has been hit as well, but overall shipments aren't nearly as bad as what the RV and housing spaces happen.

At the end of the day, when you understand just how cheap shares are and the direction that we are moving for the most affected markets, it's difficult, at least for me, to be anything other than bullish regarding Patrick Industries.

For further details see:

Patrick Industries: The Ride Higher Isn't Over