PATI - Patriot Transportation: Fleet Renewal And Driver Turnover Reduction Is Paying Off

2023-08-07 14:12:48 ET

Summary

- The company is hiking driver pay and investing $12 million in the renewal of its fleet in FY23.

- It seems that this strategy is working well as revenues rose by 3.2% year on year in Q3 FY23 while operating income soared by 64.2% to $1.5 million.

- In my view, Patriot Transportation has a lot of momentum and EPS for Q4 FY23 could surpass $0.20.

- I think the stock should be valued at above 1.2x P/B, which translates into $11.49 per share.

Investment thesis

In March, I wrote an article on SA about US tank truck hauler Patriot Transportation ( PATI ) in which I said that the $12 million in planned CAPEX for FY23 could deplete its cash reserves and that its financials could be under pressure in the second part of the fiscal year if the US enters a recession.

Well, the company posted its results for Q3 FY23 on August 3, and I think they were solid as operating income soared by 64.2% to $1.5 million. The US economy has been faring better than many experts expected, and the strategy of Patriot Transportation of focusing on driver retention and renewal of its truck fleet seems to be paying off, as it has been able to add new business over the past few months. In addition, cash and cash equivalents decreased by just $0.88 million during the first nine months of FY23 thanks to strong operating cash flow. Overall, it seems that I was too pessimistic about the financial performance of Patriot Transportation in FY23. In my view, the company could finish the fiscal year with earnings per share ("EPS") of over $0.80, and I’m upgrading my rating on the stock to buy. Let’s review.

Overview of the Q3 FY23 financial results

In case you're not familiar with Patriot Transportation or my earlier coverage, here's a brief description of the business. In 2015, the firm got spun off from FRP Holdings ( FRPH ) and is the owner of Florida Rock & Tank Lines, which is a premier bulk tank carrier focused on the southeastern USA - Florida, Georgia, Alabama, and Tennessee. The latter is involved in the transportation of petroleum and other liquid and dry bulk commodities and some 85% of its revenues come from the hauling of gas and diesel fuel from storage facilities to convenience stores, truck stops, and fuel depots. As of June 2023, Patriot Transportation had a network of 17 terminals and six satellite locations and its fleet included 253 company-owned tractors, 52 owner operators, and 402 trailers (see page 8 here ).

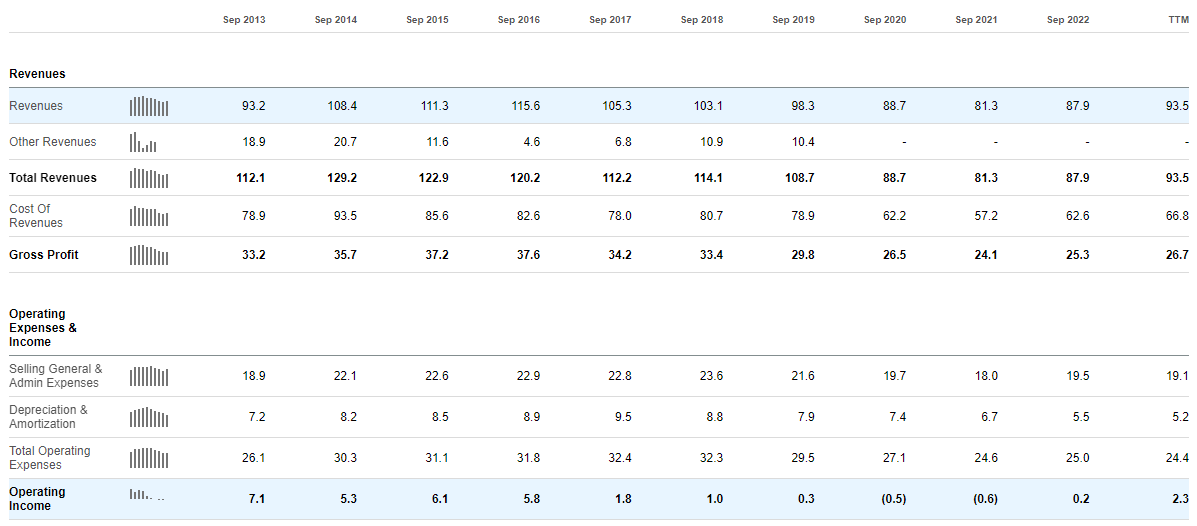

Now, I don’t like the trucking industry as it’s characterized by low operating margins, high driver turnover rates, and strong cyclicity due to low barriers to entry. It’s difficult to build a moat, and it doesn’t seem like Patriot Transportation has one as its revenues declined from $115.6 million in FY16 to $81.3 million in FY21 and the company struggled to remain in the black.

{kind=link}

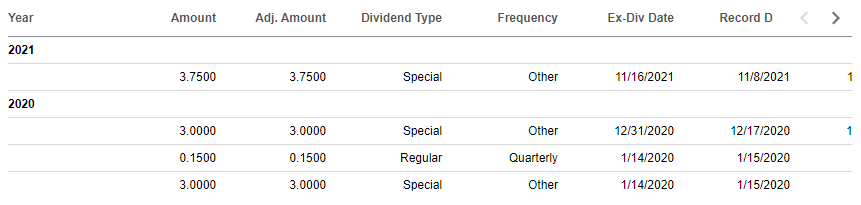

Yet, the shrinking revenues put this stock on my radar as Patriot Transportation started selling terminals in 2019 and distributing the proceeds as dividends instead of investing them in renewing its fleet. With no debt on the balance sheet, the company paid out a total of four dividends totaling $9.90 in 2020 and 2021, which is higher than its current share price.

{kind=link}

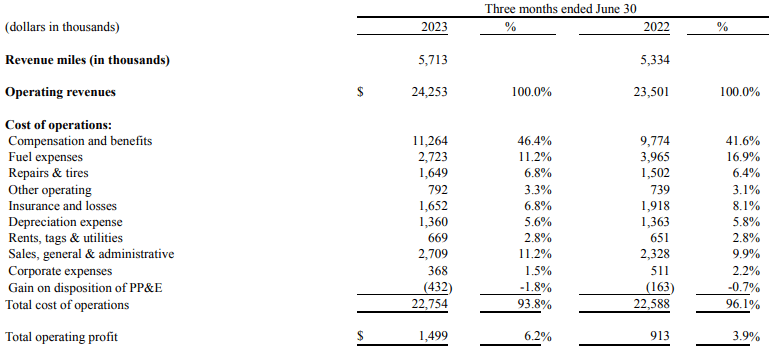

I was expecting the asset sales and high dividends to keep coming, but then Patriot Transportation revealed in its FY22 financial report that it expected to spend about $12 million on CAPEX in FY23 (Page 30 here ) in a bid to renew its fleet. In addition, the company started boosting the remuneration of its drivers with the aim of reducing their turnover rate and I thought that these measures were coming at the wrong time considering many financial experts were expecting the US economy to enter a recession in 2023. Yet, the economy has been holding up better than many analysts forecast, and it seems that the strategy of Patriot Transportation is paying off well so far. Increased pay enabled the company to decrease the driver turnover rate to 73.4% for the first nine months of FY23 from 77% over the same period of FY22, as well as boost the number of drivers by 3.5% (42 more drivers). This allowed it to add new business with both existing and new customers (see page 2 here) and this boosted revenue miles. Looking at the Q3 FY23 results, operating revenues rose by 3.2% year-on-year to $24.25 million thanks to higher rates, increased miles, and an improved business mix. The increase is significant when you take into account that revenue per mile declined by 3.6% year-on-year due to lower fuel surcharges as diesel prices decreased. Looking at the cost structure, fuel expenses slumped by over 32% thanks to lower diesel prices as well as improved fuel efficiency thanks to investment in new tractors. The modernization of the fleet also helped drive down insurance costs as risk insurance claims decreased. In addition, Patriot Transportation booked a decent $0.43 million gain on the sale of equipment, and I expect this to continue to take place over the coming months as the company revealed in its Q3 FY23 earnings call that petroleum trailer prices are some $30,000 higher compared to the time before the COVID-19 pandemic.

{kind=link}

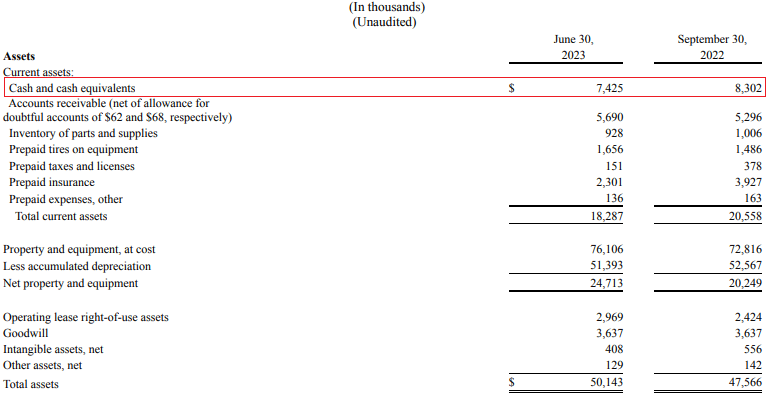

Over the first nine months of FY23, Patriot Transportation bought 52 new tractors and plans to replace another 21 tractors in the fourth quarter of the fiscal year (see page 17 here). Investment in the purchase of property and equipment totaled $8.82 million, but the $6.92 million cash flow from operations and $0.91 million proceeds from the sale of property and equipment led to a decrease in cash and cash equivalents of less than $1 million over the first nine months of FY23. Patriot Transportation had no debts at the end of June.

{kind=link}

The company still expects CAPEX for the fiscal year to stand at around $12 million, and this means that the sum for the current quarter should come in at just over $3 million. In my view, Patriot Transportation has a lot of momentum going into Q4 FY23 and EPS is likely to remain above $0.20 while cash could be above $6 million at the end of September thanks to strong operating cash flow. I think that the company is starting to look undervalued, and I expect the market capitalization to gradually increase to above some 1.2x book value over the coming months. This translates into $11.49 per share, or an upside potential of 30.1% as of the time of writing.

Turning our attention to the downside risks, I think that the major one is that I could be over-optimistic about the company’s financial performance in Q4 FY23. It’s possible that compensation expenses will start eating into margins significantly in the near future, or that gains on the sale of old equipment will decrease as petroleum trailer prices return to pre-pandemic levels. In addition, a potential slowdown in the US GDP growth could put the whole sector under pressure. Investors should also keep in mind that this is a thinly traded microcap stock whose daily volume is seldom above 2,000 shares. This means that there could be significant share price volatility here and that it could be challenging to close a large position.

Investor takeaway

Patriot Transportation’s financial performance so far in FY23 has been much better than I expected, and it seems that the company’s strategy of reducing driver turnover and renewing its fleet has been a major factor in this. I think that Patriot Transportation is likely to book decent results in Q4 F23 as well and that the share price could be in the double digits soon. In my view, there is a decent margin of safety here, but considering this is a thinly traded microcap stock, it could be best for risk-averse investors to avoid Patriot Transportation.

For further details see:

Patriot Transportation: Fleet Renewal And Driver Turnover Reduction Is Paying Off