PAXS - PAXS: The Best PIMCO Taxable Bond CEF To Buy Now

2023-10-09 11:08:46 ET

Summary

- Traditional retirement portfolio strategies of a 60/40 mix of stocks and bonds are being challenged due to poor bond market performance.

- Bond funds are on track for a third consecutive year of losses, which has not happened since the 1970s.

- PIMCO Access Income Fund is recommended as a good investment option due to its high UNII coverage, discount to NAV, and attractive yield.

Traditional investing strategies over the past 50 or more years have recommended a mixed allocation to stocks and bonds in most retirement portfolios. Generally speaking, the advice has been to hold more stocks in your younger years during the accumulation phase, shifting to more conservative bonds and fixed income holdings in later years to preserve capital and increase the amount of income generated. The 60/40 mix (60% stocks and 40% bonds) is often discussed as a target retirement allocation and in fact, many “ target date funds ” apply that strategy, or something like it, to manage the portfolio holdings for those who do not want to worry about managing their own investment portfolios.

In an article published in 2015 by CNN Money, that target allocation is described in this way:

One method many retirees employ is what's known as a "static" asset allocation. You settle on a mix that offers a reasonable tradeoff between risk and return -- likely in a range between 40% stocks-60% bonds and 60% stocks-40% bonds for most retirees -- and you then largely maintain that blend throughout retirement by periodically rebalancing , or selling some stocks and plowing the proceeds into bonds if stocks have been on a roll or doing the reverse if stocks have lagged. A balanced fund -- a type of mutual fund that generally keeps 60% of its assets in stocks and 40% in bonds -- is a classic example of static asset allocation.

But the past 3 to 5 years have changed that thinking for many investors, as the Covid-19 pandemic and the resulting post-pandemic impact have changed how bond markets have performed due to rising interest rates and high inflation. In fact, during 2022 both stocks and bonds had one of the worst performing years in recent history. And although it started to appear that in 2023 things would improve for the bond market during the first half of the year as the bond market started to rebound by July, now in October it looks like the bond market is likely to have a third year in a row of underperformance.

Due to the Federal Reserve’s “higher for longer” message, the largest bond funds have posted both short-term and long-term losses as of Q323. In this article from Morningstar, it appears that bond funds are on track to suffer losses for the third year in a row, something that has not happened since the 1970s.

A negative third quarter has put investors in many of the largest bond funds on track for a nearly unheard-of third consecutive year of losses. In the background, even though the Federal Reserve held interest rates steady at its September meeting, its “higher for longer” messaging sent waves through the bond market. In response, yields on intermediate and long-term bonds rose sharply, and bond funds focused on those maturities suffered.

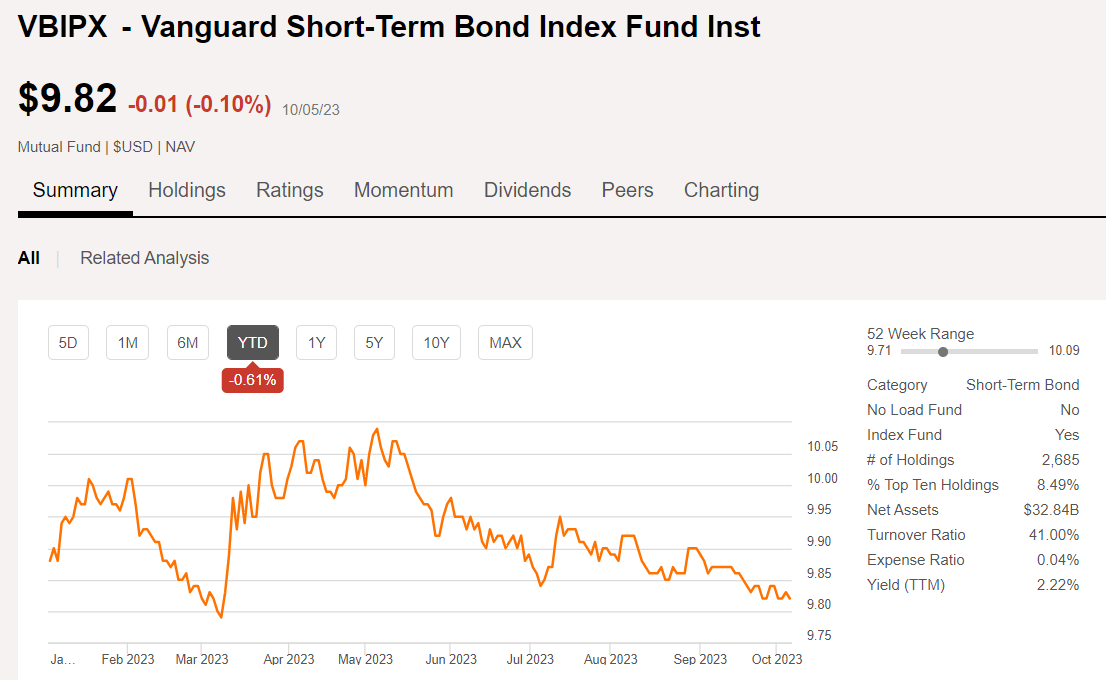

Among the largest bond funds, only the ones with short-term and ultra-short-term bond holdings made gains in the third quarter. The Vanguard Short-Term Bond Index ( VBIPX ) gained 0.2% during the quarter but is now down -0.6% YTD.

{kind=link}

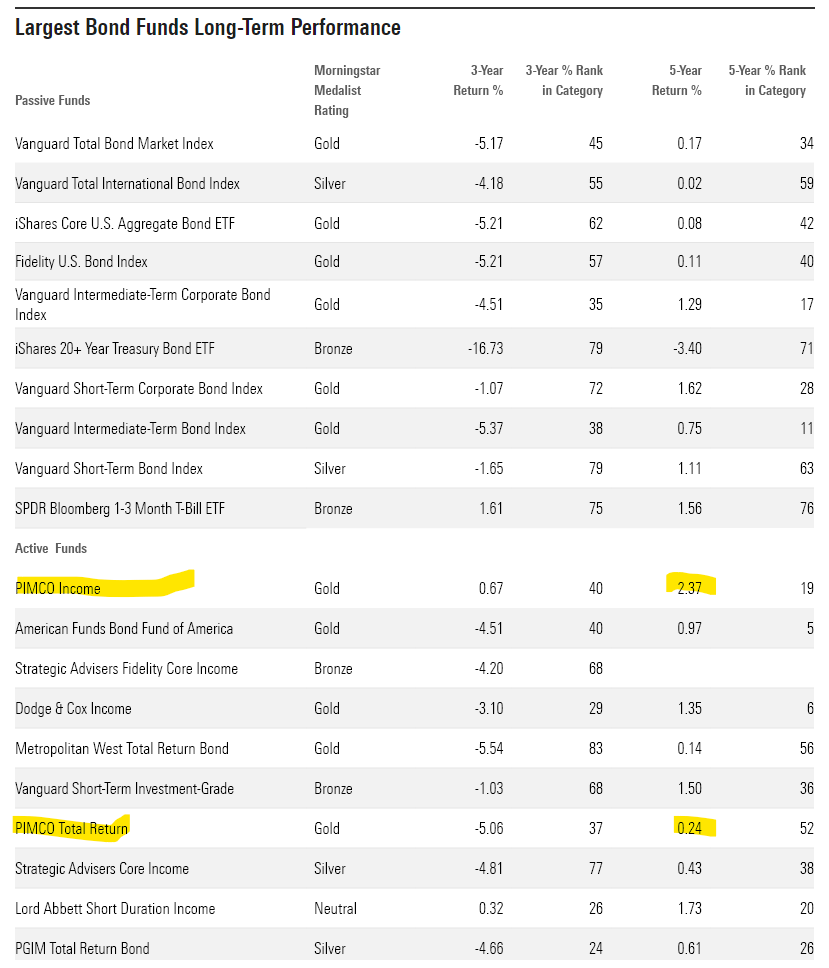

Even long-term performance as measured over the past 3 and 5 years have eked out only small gains for the best actively managed bond funds such as those from PIMCO as illustrated in this table from Morningstar.

{kind=link}

PIMCO Bond CEFs

For many fixed income investors that follow recommendations on Seeking Alpha, there is a lot of discussion surrounding the closed-end funds ("CEFs") that PIMCO offers. Generally, the PIMCO taxable bond funds that are offered as CEFs offer a high yield and may trade at a discount to NAV. Those CEFs from PIMCO that trade at a premium are also appealing to many fixed income investors due to the long track record of outperformance, as well as the added benefit that all the Pimco CEFs allow for reinvestment at a discount (up to -5%) to NAV.

In this article, I intend to review the PIMCO Access Income fund ( PAXS ) and suggest that now may be a good time to start a long position in the fund or add to it if you already hold some shares. Other PIMCO CEFs that are also worth considering now include PIMCO High Income (PHK), which is currently trading at a slight discount for the first time in a year and yields 13%, PIMCO Dynamic Income Opportunities (PDO), which is trading at a slight discount and yields 13%, and PIMCO Dynamic Income fund (PDI), which is currently trading at a slight premium and offers a yield exceeding 15%.

My reasons for recommending PAXS include the fact that it has the best UNII (Undistributed Net Investment Income) coverage of all the taxable CEFs from PIMCO as of August 31, currently trades at a discount to NAV of about -4%, yields about 13% on an annual basis with monthly dividends, and holds the best mix of fixed income assets (in my opinion) for the current environment.

UNII Coverage

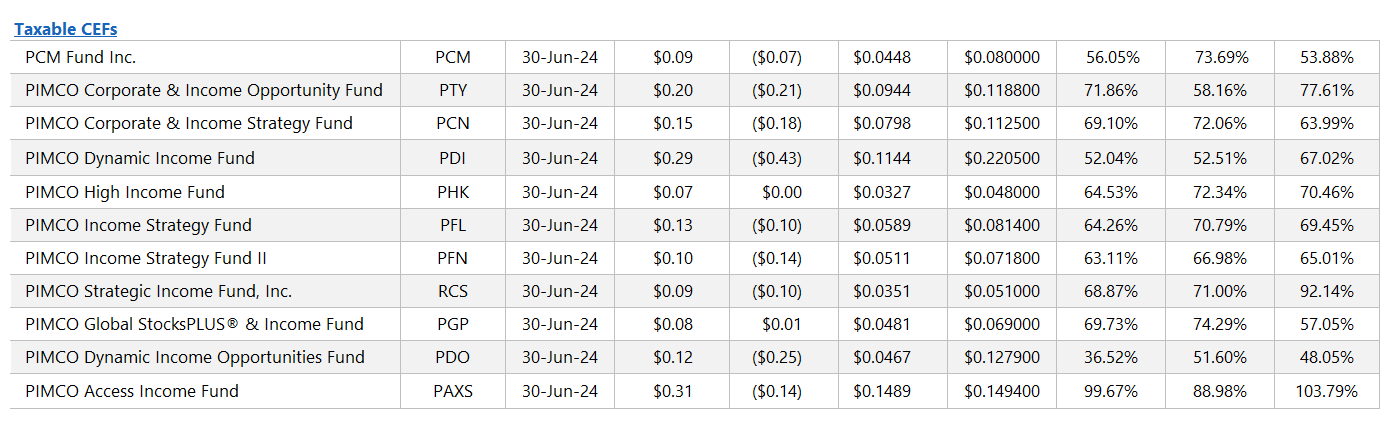

Each month, PIMCO posts an updated table with UNII coverage for all of the CEFs they offer. The latest available as of the date that I am writing this article, October 8, is the one for the period ending August 31, 2023. A snippet of that spreadsheet is included here so that you can see for yourself what the latest coverage shows, keeping in mind that this only represents 2 months’ worth of current fiscal year coverage with the fiscal year ending June 30 for the taxable funds.

{kind=link}

{kind=link}

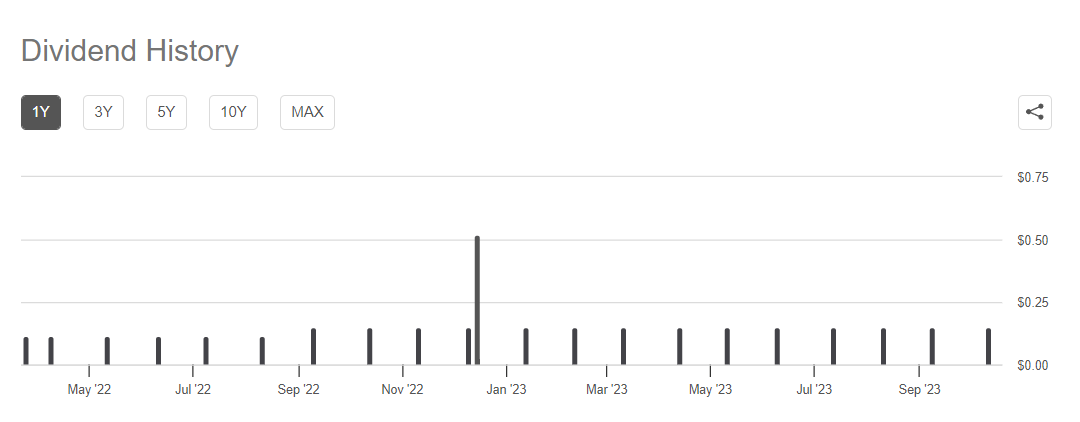

As you can see in the table above, PAXS is the only taxable CEF that has more than adequate distribution coverage for the current fiscal year, and nearly 100% coverage for the rolling 3-month period. This tells me that not only is coverage improving, but it also means that they may pay a special dividend at the end of the year like the one in 2022 when a special dividend of $0.52 was paid in December.

PAXS Overview

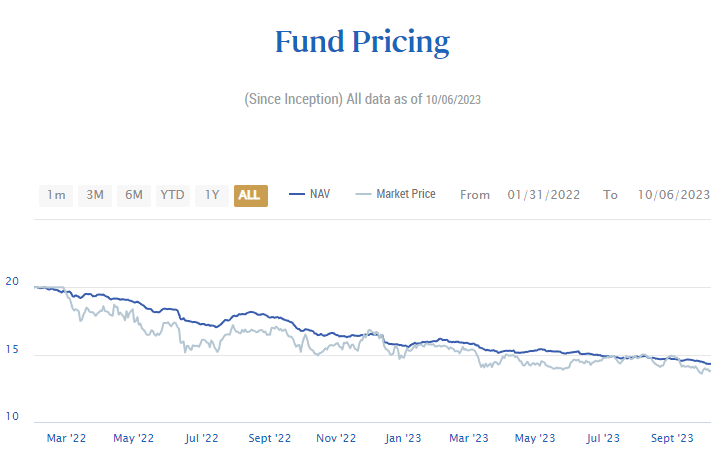

The PAXS fund was launched in January 2022, the worst possible timing for a fixed income fund. Looking at the fund pricing since inception, it is apparent that the fund has nearly always traded at a slight discount to NAV and that the fund NAV and price has been in a steady decline since its inception.

{kind=link}

This is not surprising given the bond market rout that occurred in 2022 and the ongoing underperformance of bonds in general in 2023. It is quite possible that the price could fall even further from here, however, I have to believe that at some point in the next few months, the Fed will stop raising rates and bonds will begin to rise in value as yields start to come down.

It is not a good idea to try to time the market, but then again if you are not invested you cannot realize the gains from the monthly dividends and that is my goal for investing in a fixed income fund. And if the price does continue to decrease, that just means that investors in PAXS will realize an even higher yield on cost as long as the distribution continues to be paid out at the same $0.1494 that it has been paying for the past year, since the dividend was raised from $0.1167 back in September 2022.

{kind=link}

Portfolio Composition

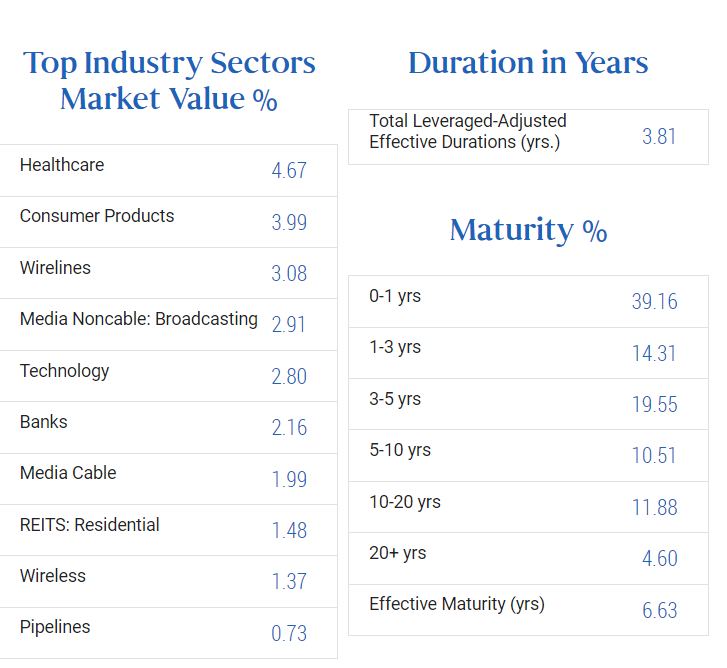

PAXS is heavily weighted toward shorter maturity holdings with nearly 40% in less than 1-year maturities as shown in this snippet from the fund’s website .

{kind=link}

The fund is well diversified across sectors as of August 31, with only a small allocation to government bonds and not too large of an investment in mortgage securities relative to other PIMCO funds.

Pimco

I believe that the current mix of shorter duration holdings and less reliance on government bonds and mortgage related securities has helped them maintain distribution coverage over the past few months. The fund employs a multi-sector approach including private credit and some foreign issues as well, when appropriate, as explained in the fund overview.

The Fund seeks to achieve its investment objectives by utilizing a dynamic asset allocation strategy among multiple sectors in the global public and private credit markets, including corporate debt, mortgage-related and other asset-backed instruments, government and sovereign debt, taxable municipal bonds and other fixed-, variable- and floating-rate income-producing securities of U.S. and foreign issuers, including emerging market issuers and real estate-related investments (“real estate investments”).The Fund may invest without limitation in investment grade debt securities and below investment grade debt securities (commonly referred to as “high yield” securities or “junk bonds”), including securities of stressed, distressed or defaulted issuers.

Assets, Leverage, And Where Do We Go From Here

The PAXS fund currently has about $646 million in common net assets as of August 31, and employees leverage of about 44% using reverse repurchase agreements. There are currently no preferred shares, credit default swaps, or floating rate notes issued.

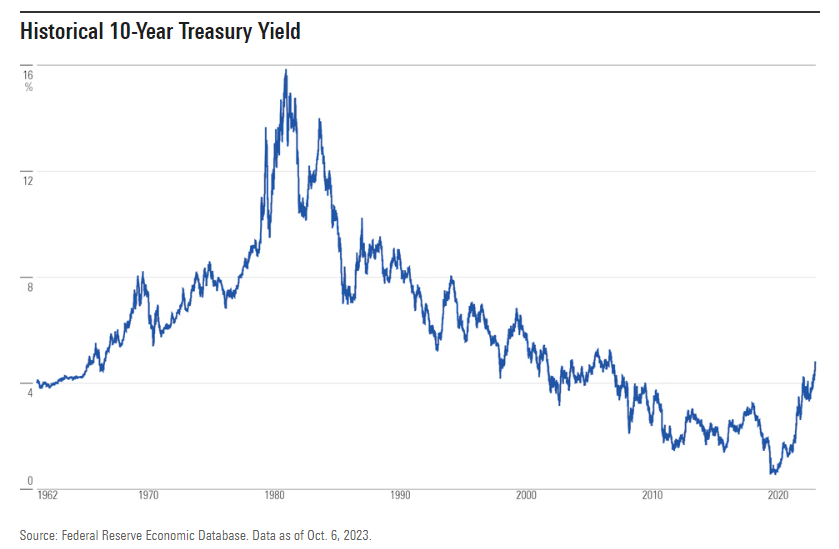

With some market prognosticators predicting the 10-year yield will exceed 5% next year, things could still get worse before it gets better for bonds. If we continue to see rising inflation that mirrors what happened in the 1970s, we could still have a long way to go before interest rates start coming down.

{kind=link}

The shocking jobs report from last week caused yields to rise again, nearly approaching the 5% level.

Before Friday, the yield on the U.S. Treasury 10-year note had already risen to 4.70% from 3.97% at the end of July. Following the release of the jobs data, the 10-year yield briefly jumped to around 4.85% before settling to end the day at 4.78%. These are the highest yields since June 2007.

On the other hand, there are some who believe that the economy is slowing and that the 5% yield could mark the top in the short term, with rate cuts on the table for next year. If that happens, the bond markets could reverse quickly, and it would represent a good opportunity to buy bonds now while prices are still low. From another recent Morningstar article , this comment from Tony Rodriquez with Nuveen summarizes this thinking:

“If we’re right about this moderation of growth as a result of the lagged effect of this much higher rate environment that we’re in, we think that you will see lower rates by the middle of next year,” he says. “Now, whether the 10-year hits 5% here is anybody’s guess. Certainly, the momentum is in that direction. And if you get a surprisingly high inflation print next week, it wouldn’t surprise us at all to see us get another 10-basis-point day—which seems to be routine nowadays—and all of a sudden, you’re knocking on the door of 5%.”

That said, Rodriguez adds, “We would say that we think bonds are attractive here and that over a six-to-12-month horizon … you will also end up seeing some price appreciation from a decline in yields.”

Summary

With the recent downturn in the markets since the end of July and bonds underperforming over the past 2 plus years, it is hard to invest in something that looks like a falling knife. But as many have suggested , the time to buy is when there is “Blood in the streets.” The recent news, Israel battles Hamas militants as country's death toll from mass incursion reaches 600 of the attack by Hamas on Israel and declaration of war is literally causing blood in the streets and may have a “black swan” effect on the markets. I would not be surprised to see yet another decline in market prices for both stocks and bonds in the coming days and weeks. Despite that warning and even with the uncertainty around yields and inflation, I do believe that now is a good time to add shares of PAXS to your income portfolio.

The markets tend to be forward looking, and if bond yields and interest rates start to decline by the middle of next year, now would be a good time to load up on the PAXS fund to add the 13% yielding monthly dividend payer to your portfolio. I am long PAXS and PDO in my Income Compounder portfolio and intend to add more to my PAXS holding if the prices drop further to increase my future income stream even more.

For further details see:

PAXS: The Best PIMCO Taxable Bond CEF To Buy Now