HQI - Paylocity: Favorable Risk-Reward Despite Potential Economic Weakness

2023-06-29 15:49:24 ET

Summary

- I have covered Paylocity twice before and assigned it a "Hold" rating both times.

- I am now upgrading my rating to a "Buy" as Paylocity's earnings have grown substantially over the past few years with little dilution.

- If Paylocity meets its long-term financial targets, I think the stock could grow at a 20-25% CAGR due to earnings growth and multiple expansion.

- Economic risk is the biggest concern, but I think the upside in my bull case provides enough compensation for the downside a recession could cause.

Paylocity Holding Corporation ( PCTY ) financial results have improved substantially over the past few years. Since 2019, revenue has grown 20%+ per year and adjusted EBITDA margin has remained relatively flat, moving from 28.7% to 27.9%. The stock, however, has not followed this growth in earnings. This type of discrepancy between earnings and the stock price is often caused by dilution, especially with software companies, but Paylocity’s diluted shares outstanding went from 55.4m to 56.5m. This modest increase has also occurred with no cash spent on repurchasing shares which is refreshing to see when many software companies boast large stock repurchase plans just to offset dilution from stock based comp.

I’ve written about Paylocity twice before and I continue to revisit the stock because I believe the company will be a long term winner in the human capital management software industry. I wrote about why I think this will be the case in a previous article and my thoughts on the matter have not changed. Paylocity is offering a much more modern and complete product when compared to the larger incumbents in the industry and I think this gap in product quality will continue to increase as new technologies arise such as AI, and as the modern workplace continues to modernize. Paylocity will keep up with these changes better than its industry peers in my view.

Despite this, I’ve been cautious on stock due to valuation concerns. I feel this trepidation was correct as the stock is up only 10% since I first wrote about it 2 years ago in June 2021. Improving fundamentals with a lower stock price means that there has been multiple compression which makes now a better time to invest, if the investor thinks the fundamentals will continue to improve as they have. In the case of Paylocity, I think this question comes down to maintaining 20%+ revenue growth.

At this point, with revenue almost double what it was in 2019, higher margins, a flat share count, and an EV/Sales ratio that is almost half of what it was in 2019, I am rating Paylocity as a buy. I think the trends of the past few years will continue far into the future and for a longer time than analysts are currently expecting.

Research and Development

Most modern software businesses operate in industries whose seeds were planted during the tech boom in the late 90s. On the other hand, the HCM industry is an old one with incumbents such as Automatic Data Processing, Inc. ( ADP ) and Paychex, Inc. ( PAYX ) founded in the 1940s and 1970s, respectively. Of course, the industry has changed in that time but those companies have maintained and increased their market share.

Paylocity was founded in the late 1990s and I think this gives it a different DNA than the incumbent industry players. There is a much larger focus on research and development as it works to build out the best HCM solution on the market. They break out R&D spending in their annual report and in 2022 it was 12% of total revenue. ADP and Paychex don’t break this out and I think that speaks to the emphasis that Paylocity places on the importance of developing innovative tools for their product.

In fact, a search for the term “research and development” in Paylocity’s most recent annual report returned 30 different instances of the phrase being used. Paychex had 4 instances and ADP had 1. This isn’t a very scientific way of analyzing the businesses, but I think it does speak to where priorities lie.

Anecdotally, I also know how difficult it is to change and update software once it has been developed and deployed. Given ADP and Paychex’s much larger size and customer base, and the fact that they’ve been around much longer I would bet it is much more difficult to make quality changes to its software in a timely manner.

Valuation and Comparison to ADP

Valuing growth businesses like Paylocity requires making estimates for results many years into the future, so I like to keep my forecasts for them as simple as possible. Errors with assumptions are magnified each year that goes by, so I like to do this to reduce the number of potential errors.

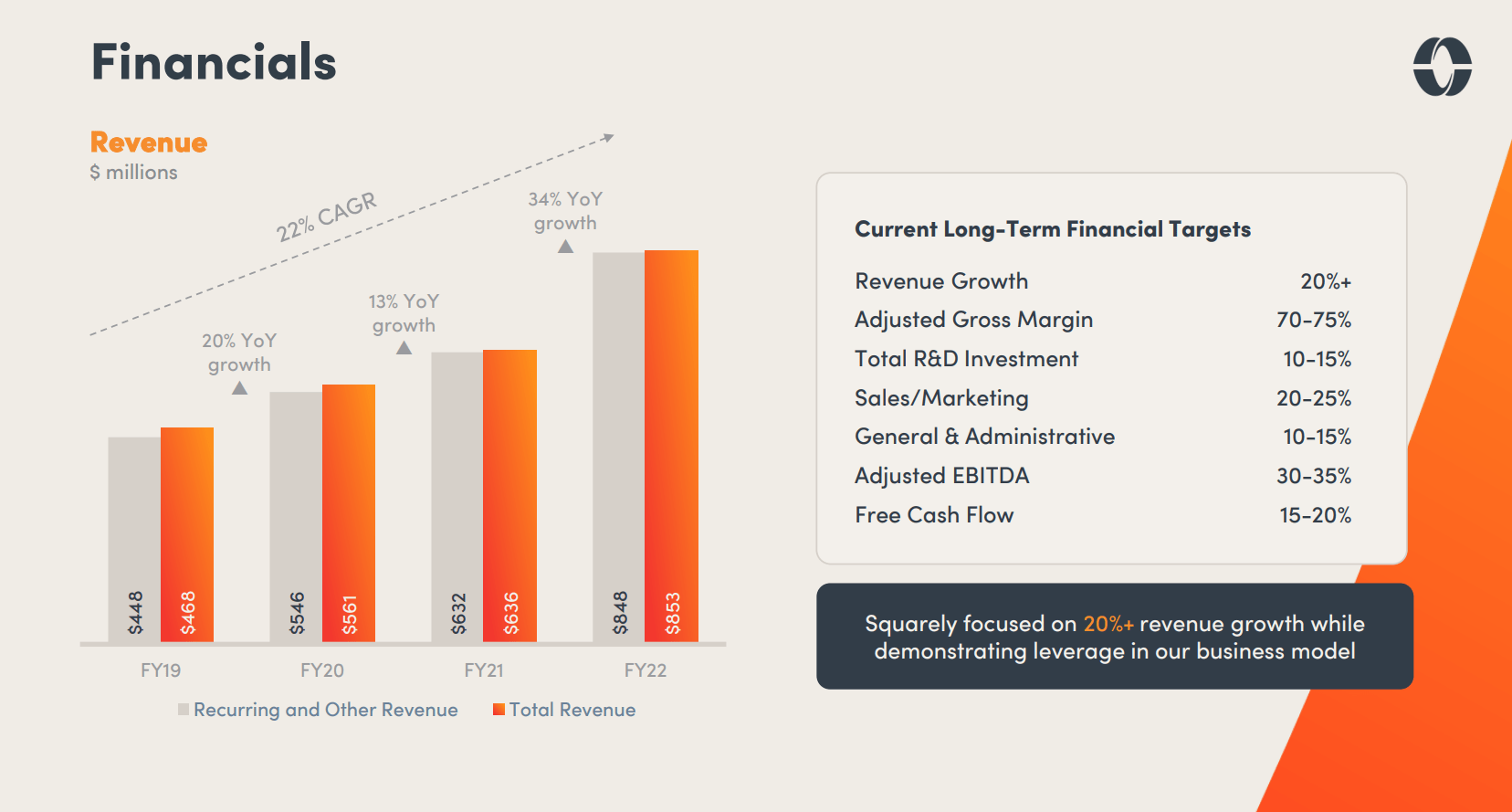

Paylocity Long Term Financial Targets (Paylocity Investor Presentation)

{kind=link}

Guidance for 2023 is about $1.16 billion in revenue with $370 million in adjusted EBITDA. I will assume they hit these numbers and I will use them as a base to build from.

Analysts are projecting a 16.8% CAGR in revenue from 2024 to 2027, and a 33.8% EBITDA margin in 2027. This means they are betting against Paylocity’s long term revenue growth guidance. Given my thoughts on Paylocity’s product being higher quality, I will take the other side of that bet.

If revenue grows 20% for the next 5 years and the adjusted EBITDA margin grows to 34%, revenue in 2028 would be $2.89 billion and adjusted EBITDA would be $981 million. This implies adjusted EBITDA CAGR of 21.5% through 2028.

The current EV/EBITDA multiple based on fiscal year 2023 adjusted EBITDA guidance is 26.2. ADP’s trailing twelve month EBITDA multiple (I’ve added back stock based comp to this adjusted EBITDA figure to more align with how Paylocity calculates it) is 17.7. ADP is guiding for 10-12% growth EBIT over the next few years so if Paylocity meets its long term revenue growth and EBITDA margin guidance, EBITDA growth rate will be about twice as high as ADP's. I think this higher growth should command a premium multiple, somewhere in the range of 25-30 times EBITDA. This would give an enterprise value target range of $24.5b-$29.4b or a CAGR for the stock of 20-24.5%.

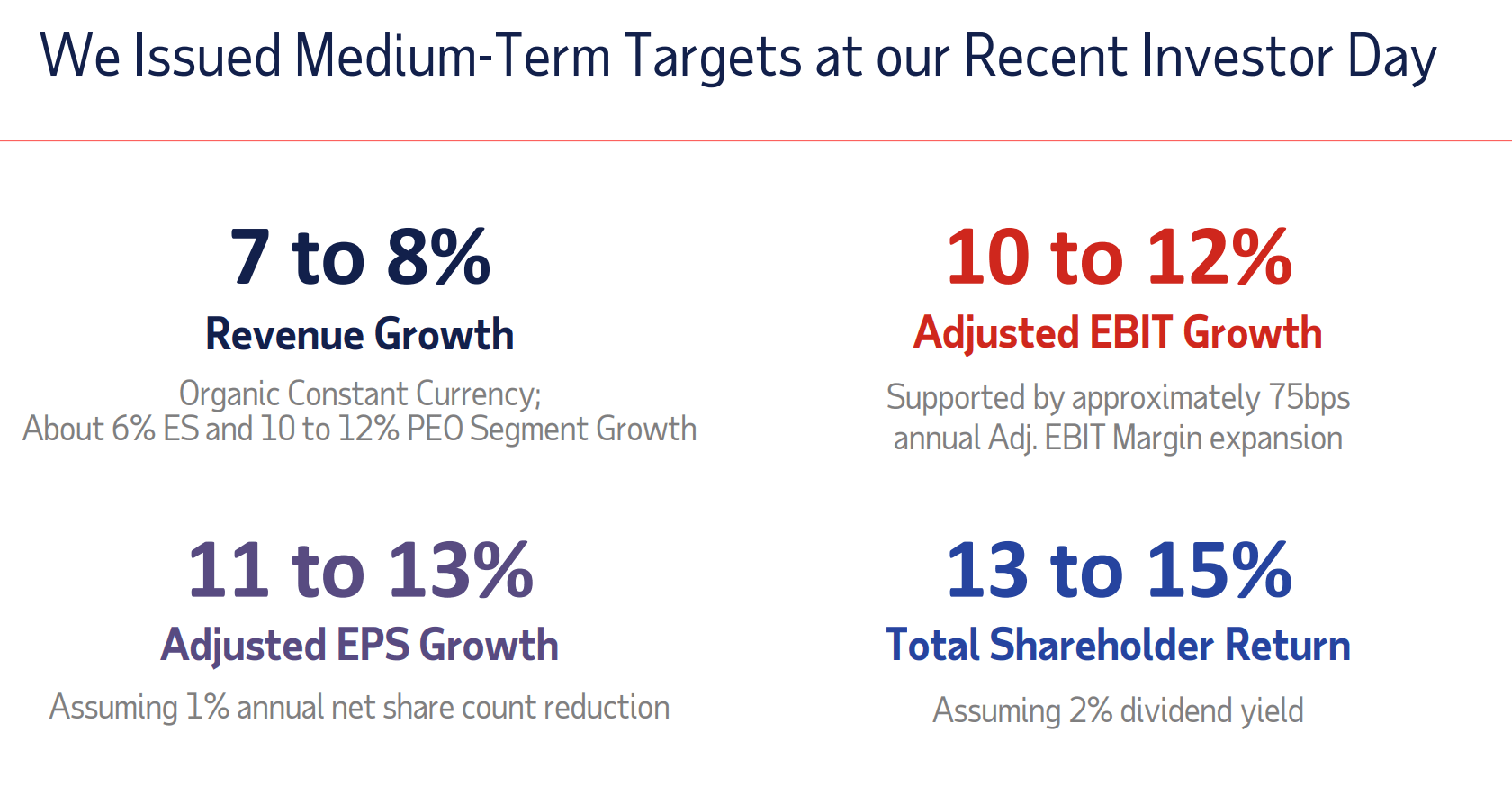

ADP Financial Targets (ADP Investor Presentation)

{kind=link}

Risks

The biggest near term risk I see is a recession that leads to a rise in unemployment. I recently wrote about HireQuest, Inc. ( HQI ) which is a staffing company. It is a high quality business with a long runway for growth, consistently high ROIC and good capital allocation, but I am cautious due to its high valuation going into potential economic weakness. In general, I do not think the current valuation provides enough of a margin of safety given the near-term risks.

I mention HireQuest because it also operates in an industry that is strongly tied to the unemployment rate. Both HireQuest’s and Paylocity’s business fundamentals have improved over the past few years, but the difference is that Paylocity’s stock has undergone significant multiple compression while HireQuest’s multiple has expanded.

This relative underperformance by Paylocity's stock, along with analysts’ long term growth expectations being below Paylocity’s long term guidance leads me to believe that the economic weakness risk is more priced into Paylocity’s stock as it trades at an EV/Sales ratio of 9. For reference, the lowest its trailing EV/Sales ratio has been as a public company was around 6.5 in February 2017.

In hindsight, February 2017 was a great time to invest as fundamentals improved and the multiple expanded. Unless a very bad recession hits causing investor sentiment to drop significantly, I don’t see the EV/Sales multiple dropping much farther below the previous low of 6.5 as they are a much more proven company at this point. Paylocity’s adjusted EBITDA margin in fiscal year 2017 was 18.7% compared to 27.8% in fiscal year 2022. These higher margins and improved scale should cause the stock to command a higher multiple.

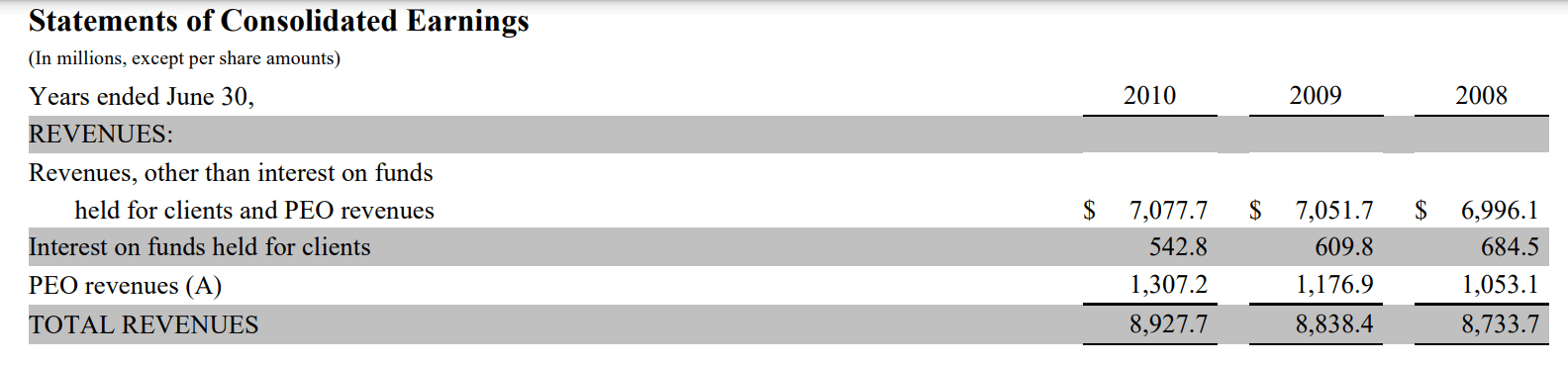

To better understand what could happen in a recession, I checked ADP’s financial results during the 2008-2009 financial crisis. I was surprised to see that from fiscal year 2008 to fiscal year 2009, which included the worst of the crisis, revenue was flat. This didn’t stop the stock from dropping 25% as the multiple compressed, but considering the severity of the crisis and the 50% drop in the S&P, this was not a terrible outcome.

ADP 2009 Income Statement (ADP 2009 Annual Report)

{kind=link}

If there was a bad recession which caused Paylocity’s revenue to be flat year over year at $1.16b, and investor sentiment caused the EV/Sales multiple to drop to 6.5, the enterprise value would drop to $7.5b or about 25% below what it is now.

Final Thoughts

I have covered Paylocity twice before and gave “Hold” ratings both times due to valuation concerns. This time around, I think the current multiple compensates investors well for the risk of a recession, given my forecast of a 20-25% CAGR for the stock over the next 5 years compared to my estimate of a 25% drop in the enterprise value in a worst case scenario.

Despite changing my rating from “Hold” to “Buy”, my thoughts on the quality of the business have not changed. They are growing and taking market share by offering a superior product when compared to its competitors and adding to that product with its focus on R&D.

The HCM software industry is large and provides a long runway for growth. If Paylocity maintains this R&D advantage over time, I believe earnings will rise in the long run regardless of what happens to the economy in the next 1-2 years.

For further details see:

Paylocity: Favorable Risk-Reward Despite Potential Economic Weakness