PAY - Paymentus: Beneficial Guidance And More Partnership Agreements Imply Undervaluation

2023-05-21 06:31:08 ET

Summary

- Paymentus serves billers of all sizes in different industry verticals, such as utilities, financial services, insurance, government, and telecommunications.

- Paymentus didn't only report an increase in the revenue guidance, management also reported an increase in the number of transactions processed and a new relationship agreement with Oracle.

- I believe that Paymentus will successfully gain new billers, financial institutions, and partners, which may enhance future revenue growth and FCF generation.

Paymentus Holdings, Inc. (PAY) reported an increase in the 2023 revenue guidance as well as the 2023 EBITDA guidance. Management successfully signed a new partnership agreement with a large corporation, and continues to report transactions processed growth. I believe that international expansion, new products and functionalities, and headcount growth will most likely bring free cash flow generation in the coming years. Even considering the risks from relationships with large partners and new regulations, I believe that the stock could be trading higher.

Paymentus Reports A Growing Number Of Clients From Different Sectors

Paymentus offers a next-generation suite of products through a modern technology stack. As of December 2022, its platform was used by approximately 27 million consumers and businesses in North America to pay bills, move money, and engage with customers.

The business model is well diversified. It serves billers of all sizes in different industry verticals, such as utilities, financial services, insurance, government, telecommunications, and healthcare. Additionally, it provides financial institutions with a modern platform for bill payment, account-to-account transfers, and person-to-person transfers.

It offers easy-to-use, flexible, and secure experiences for paying electronic bills through an omnichannel payment infrastructure. Its platform is built on a single code base, and leverages a software-as-a-service infrastructure, allowing the company to rapidly deploy new features and tools.

Among the key performance indicators reported by Paymentus, I believe that the most relevant is the number of transactions processed. In 2020, the number of transactions was 195 million, and this number increased to 366.8 million in 2022. In my opinion, further increase in the number of transactions might not only bring economies of scale, but also significant revenue growth and free cash flow growth.

{kind=link}

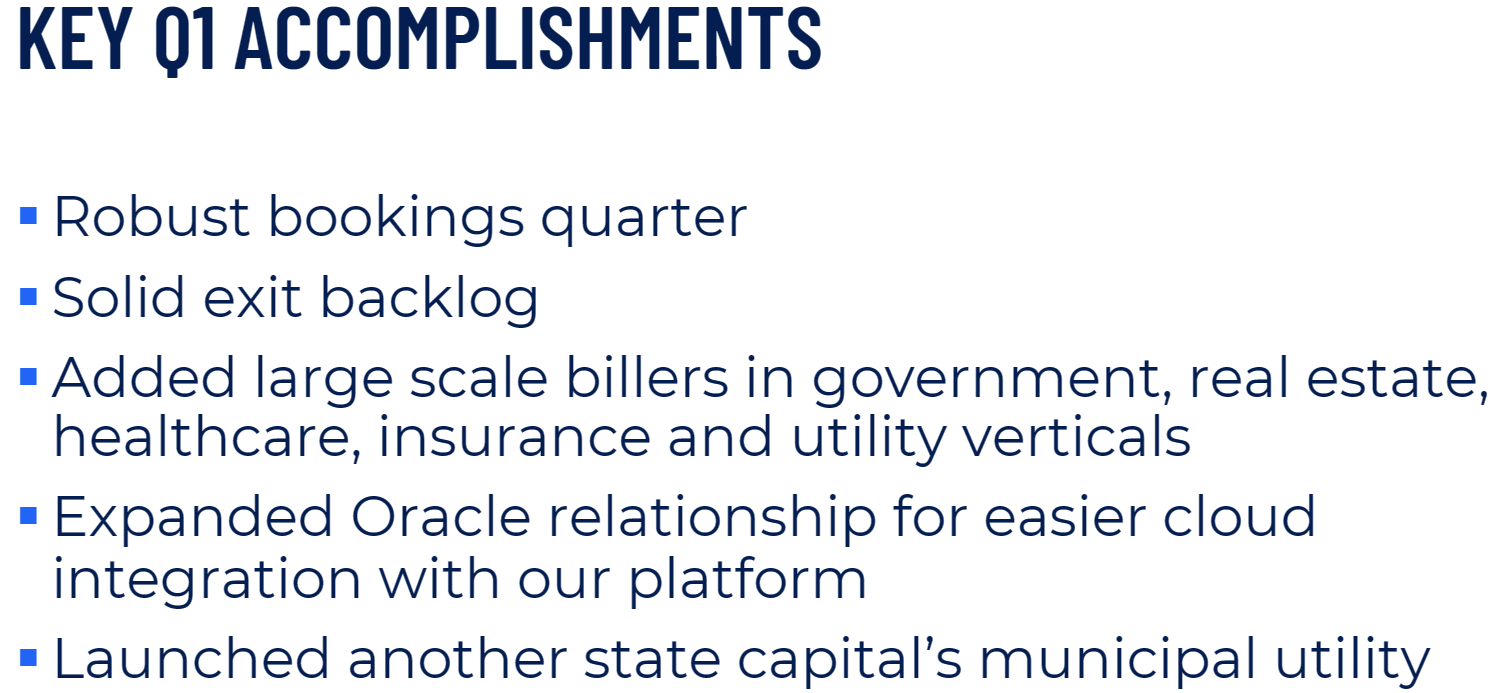

Among the new information that we received in the first quarter of 2023, the most relevant factors appear to be an increase in bookings, the solid exit backlog, and the fact that Paymentus added large scale builders and the new relationship with Oracle (ORCL).

{kind=link}

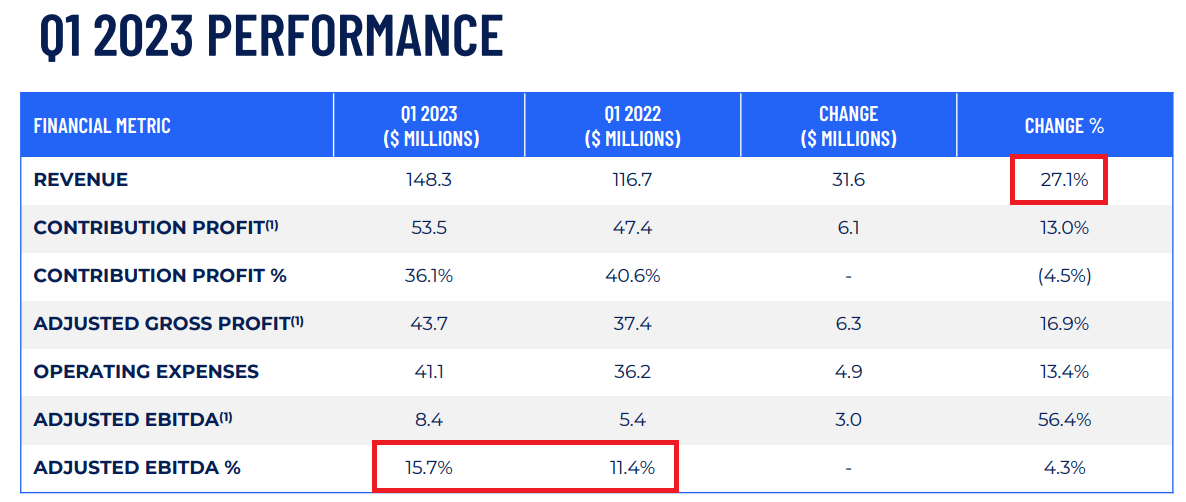

The new financial figures reported in the first quarter of 2023 were also impressive. The company reported revenue growth quarter on quarter of 27% as well as a significant increase in the Adjusted EBITDA and the Adjusted EBITDA margin.

{kind=link}

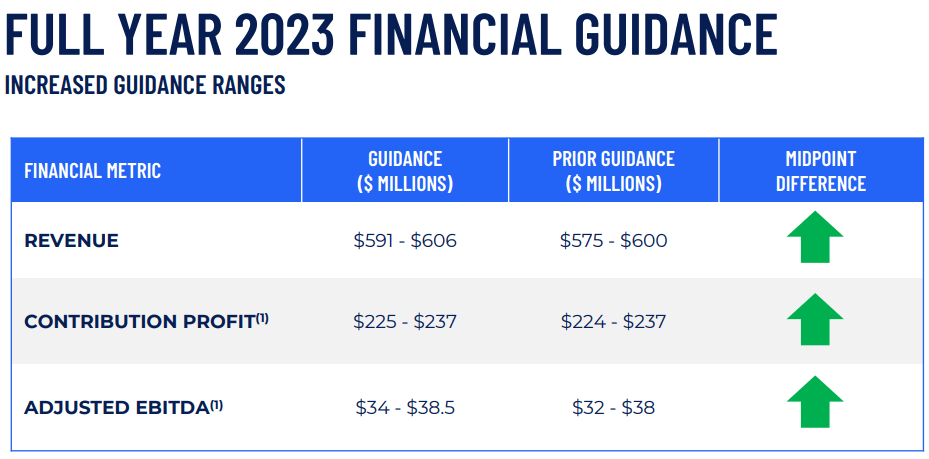

With that about what happened in the past, the most interesting in the quarterly report was the full year 2023 financial guidance. The company now expects more revenue for 2023, more contribution profit, and more Adjusted EBITDA. In particular, Paymentus now expects revenue close to $606 million and Adjusted EBITDA of close to $38.5 million.

{kind=link}

Market Expectations Include Free Cash flow Growth, Net Income Growth, And Sales Growth.

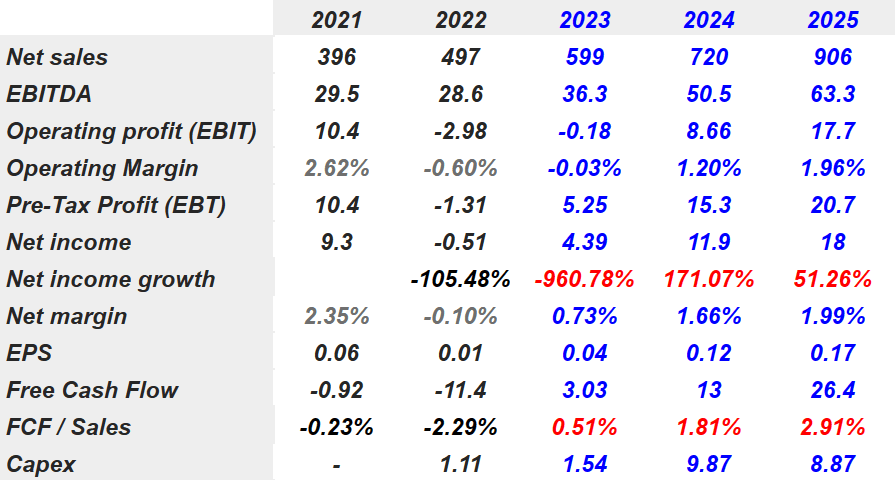

I believe that the expectations of other financial analysts are worth considering. They expect sales growth in 2024 and 2025 accompanied by EBITDA growth. The operating margin is expected to go from 1.2% in 2024 to 1.96% in 2025. Also, with increases in the earnings per share, I believe that the most relevant is the increase in free cash flow. Financial analysts expect free cash flow of $13 million and $26.4 million in 2024 and 2025 respectively. Finally, capital expenditures would stay at close to $9 million in 2024 and close to $8.87 million in 2025.

{kind=link}

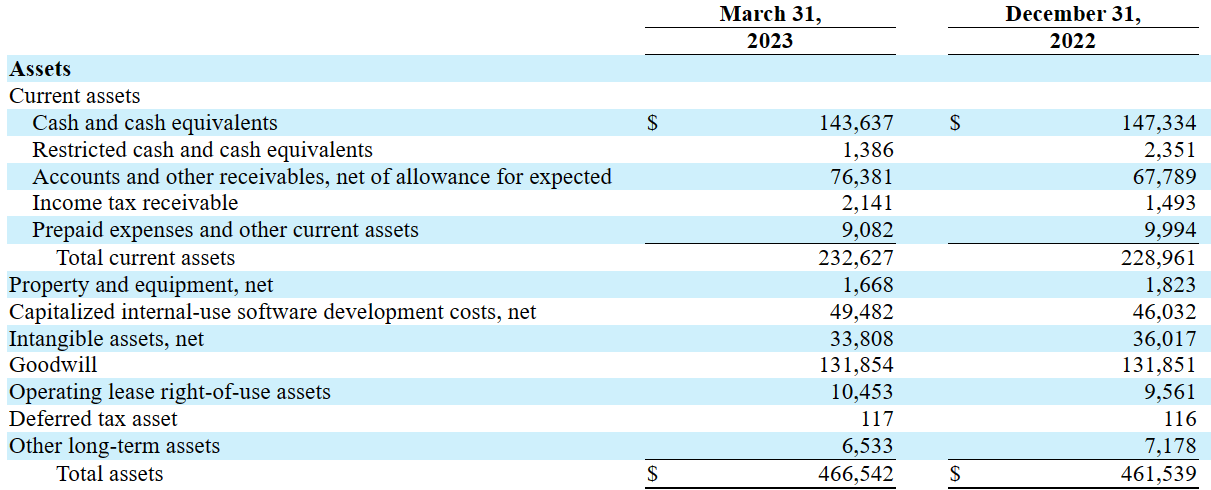

Solid Balance Sheet

I believe that most investors will appreciate the balance sheet reported in March 2023. It includes a considerable amount of cash and cash equivalents, restricted cash, a large amount of total assets, and very little liabilities. The company also reported a significant amount of intangible assets and goodwill from previous acquisitions. With an assets/liability ratio close to seven times, I believe that the balance sheet stands at a very good position.

{kind=link}

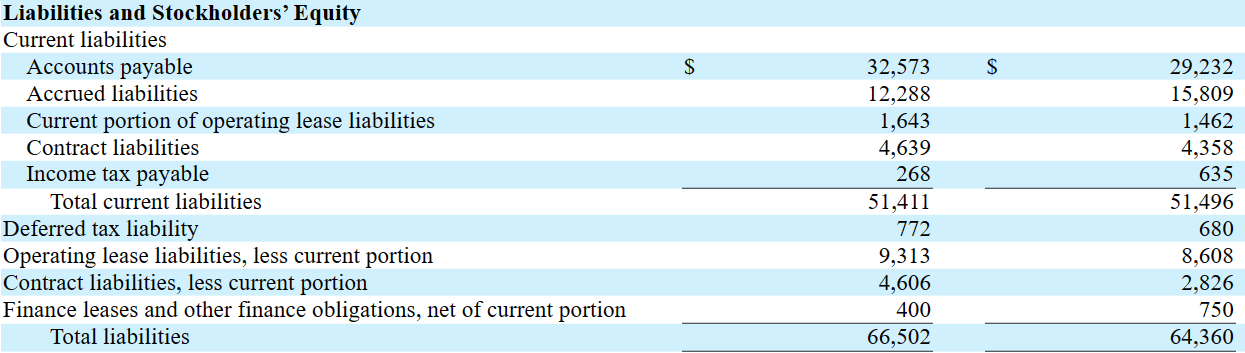

With regards to the list of liabilities, the most relevant are the accounts payable worth $32 million, followed by accrued liabilities of $12 million, total current liabilities of $51 million, and total liabilities of $66 million. Let's note that the company doesn't report financial debt.

{kind=link}

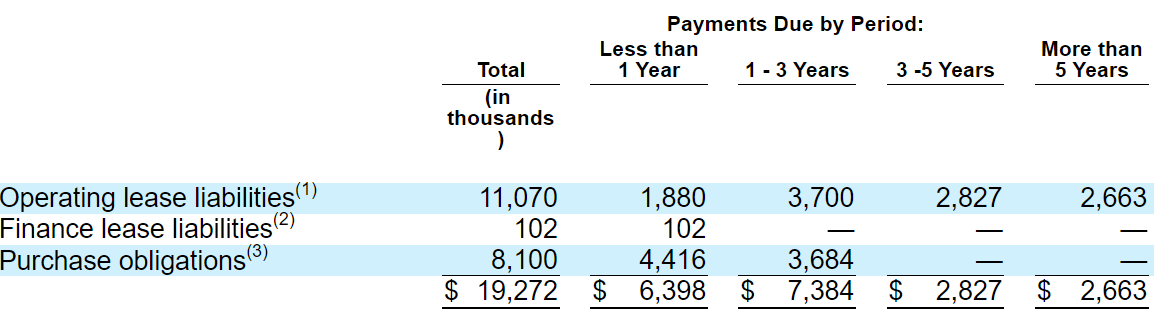

With regards to the contractual obligations, I'm really not worried. Considering the cash on hand and future generation of free cash flow, the total amount of control obligations doesn't look very significant. Paymentus reported operating lease liabilities, finance lease liabilities, and purchase obligations, totaling close to $19 million.

{kind=link}

My Financial Model Implied A Valuation Of $11.63 Per Share

Under normal conditions, I believe that Paymentus will successfully gain new billers, financial institutions, and partners, which may enhance future revenue growth and FCF generation. Considering the number of clients that trust Paymentus, many other potential clients will most likely be interested in the company.

We intend to continue investing in our efficient go-to-market strategies, increasing brand awareness and driving adoption of our platform and products. Our ability to attract new, and maintain existing, billers and financial institutions and drive adoption of our platform will depend on a number of factors, including the effectiveness and pricing of our products, offerings of our competitors and the effectiveness of our marketing efforts. Source: 10-Q

The company uses a diversified go-to-market strategy that includes direct sales, strategic partnerships, resellers, and integrated payment network. In addition, it collaborates with strategic and software partners to expand their reach and enhance their bill payment capabilities.

We believe there is a significant opportunity to increase the transactions on our platform through expanding our base of software, strategic and IPN partners. While revenue derived from or through our IPN partnerships has not been significant historically, we expect that the revenue contribution from our IPN will grow over time. Source: 10-Q

I would also expect that additional features and functionalities may be added to capture more electronic bill payments as well as to expand into new channels and industry verticals. In addition, new products and international expansion may even bring more revenue growth and value creation.

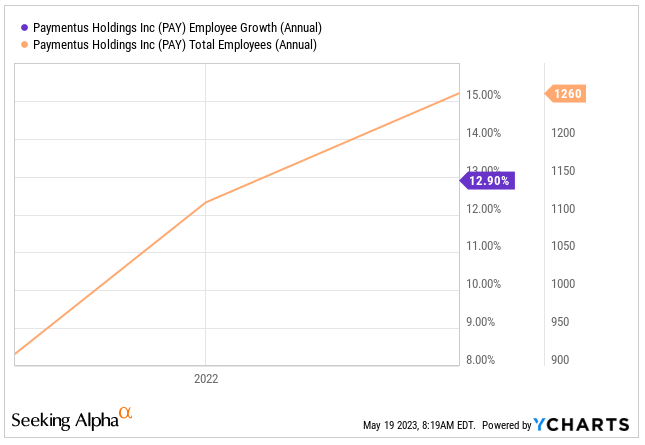

Besides, considering the state of the balance sheet and the total amount of cash on hand, I expect employee growth in the coming years, which most likely will lead to free cash flow growth and sales growth. Let's keep in mind that in the past the company reported employee growth close to 13% year on year.

{kind=link}

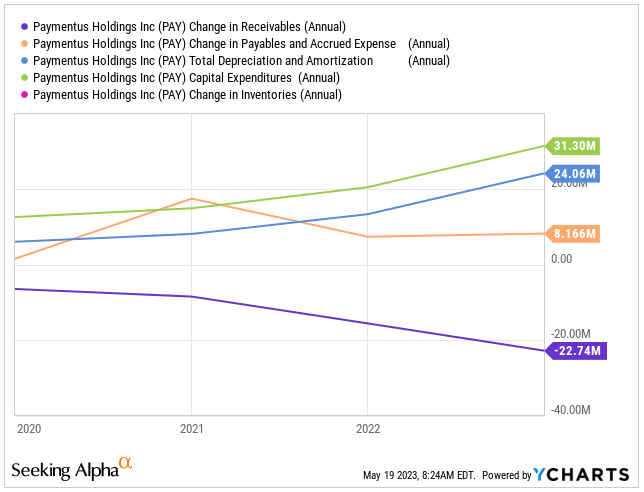

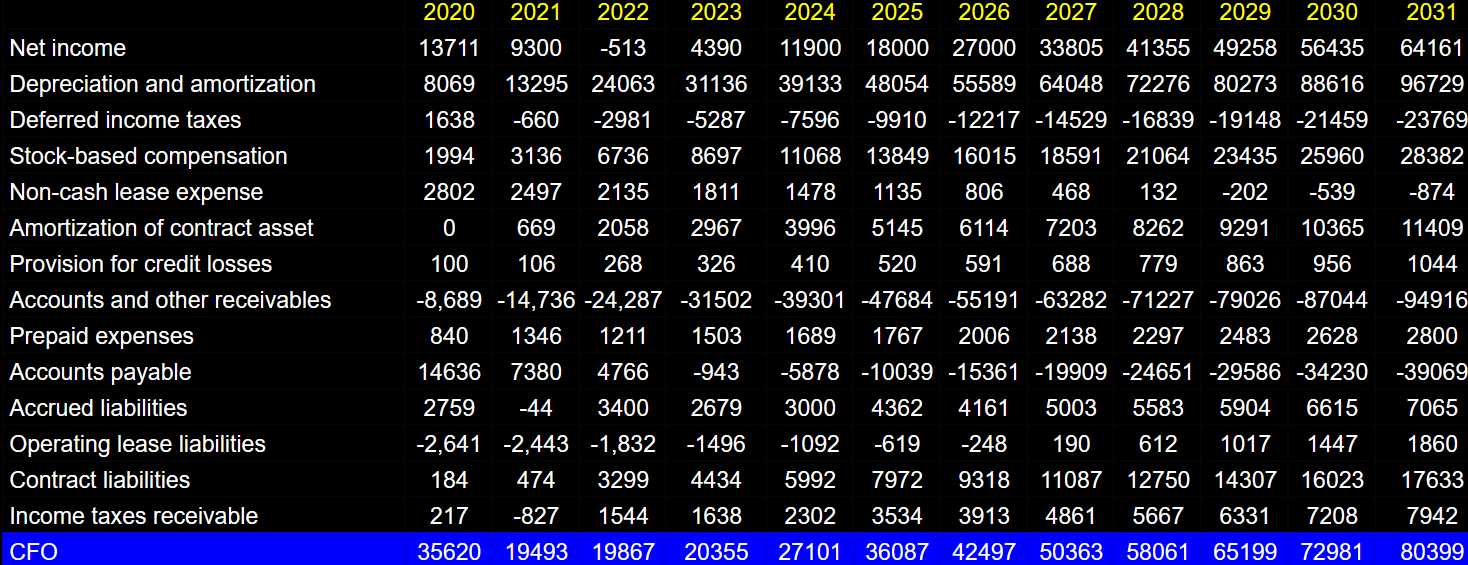

For the design of my free cash flow model, I used figures seen in the past regarding changes in receivables, changes in accounts payables, accrued expenses, depreciation and amortization, capital expenditures, and changes in inventories. I think I am quite conservative.

{kind=link}

My financial model included 2031 net income worth $64 million, 2031 depreciation and amortization of $96 million, and deferred income taxes of -$24 million. Also, taking into consideration stock-based compensation of $28 million, non-cash lease expenses worth -$1 million, and amortization of contract assets close to $11 million, I included changes in accounts and other receivables of -$95 million and changes due to prepaid expenses worth $2 million. Finally, with changes due to accounts payable of -$40 million and accrued liabilities worth $7 million, I obtained 2031 CFO of $80 million.

{kind=link}

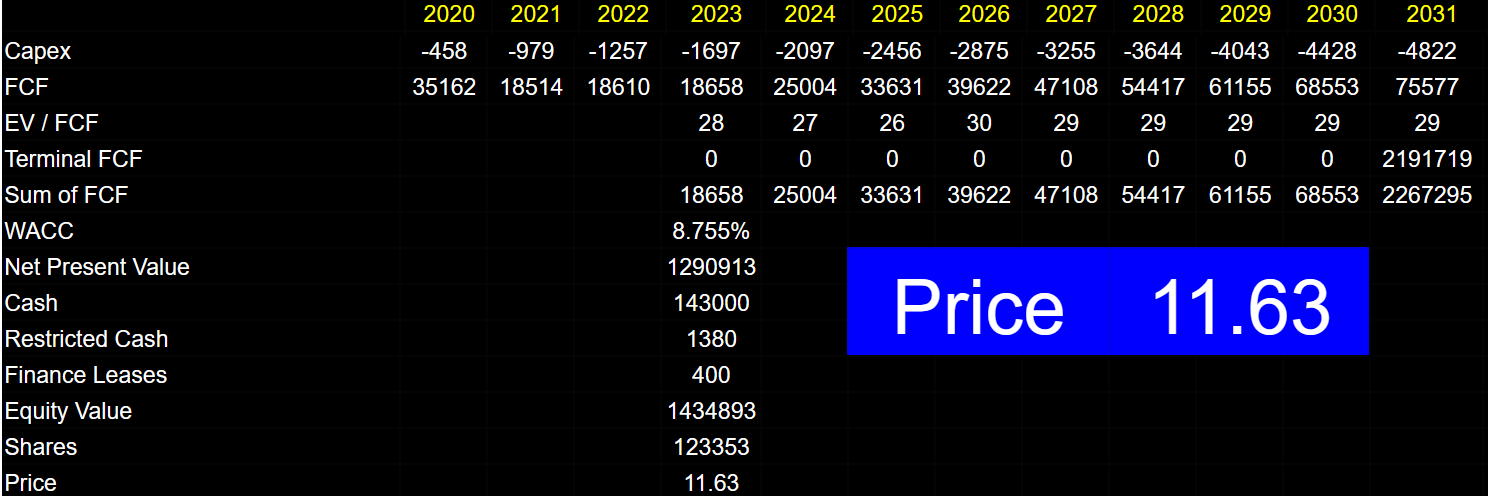

I also included 2031 capex of -$5 million, which implied 2031 FCF close to $75 million. Now, if we include an EV/FCF ratio of 29x, which I believe is a conservative valuation, and a WACC of 8.755%, the implied enterprise value would be close to $1.29 billion.

If we also sum cash of $143 million, restricted cash of $1.38 million, and subtract finance leases worth $0.4 million, the equity valuation would be $1.468 billion. Finally, the fair price would stand at close to $11.63 per share.

{kind=link}

Risks

Paymentus faces numerous risks and uncertainties, which include the sustainability of growth, the ability to establish and maintain partnerships, and an increase in revenue. In my view, we can't expect the company to deliver the same sales growth in the future as compared to the growth in the last four years. Besides, I believe that lower sales growth expectations may lead to lower demand for the stock and stock price declines.

It is also worth noting that partners are large banks and payroll solutions providers. Paymentus may not be able to renegotiate conditions with these large partners. In addition, it may also happen that new partners are not willing to accept new products or new developments offered by Paymentus. As a result, I believe that free cash flow margins might be lower than expected.

We also rely on strategic partners, such as U.S. Bank, JPMorgan Chase ( JPM ) and a major payroll solutions provider, and industry-expert partners to refer new billers to our platform. Additionally, the IPN is our patented and proprietary network that enables partners, such as PayPal (PYPL), Walmart (WMT), Green Dot (GDOT), a leading global ecommerce retailer and banks, to embed our end-to-end electronic bill payment solution into their ecosystems through a single point of access. Source: 10-K

If we are unable to increase adoption of our platform by partners and manage the costs associated with marketing our platform to potential partners and integrating with their systems, our business, operating results and financial condition may be adversely affected. Source: 10-K

Paymentus may also suffer from an eventual economic recession in 2023, inflationary pressures, and a decrease in consumption. As a result, we might see net income declines and free cash flow declines, which might lead to stock price depreciation. In this regard, management made a comment in the last annual report.

We expect economic uncertainty and inflationary conditions to continue to impact our 2023 performance. For example, some of our clients deferred anticipated 2022 implementations into 2023 or are reevaluating the development of technology resources, which will delay expected revenue recognition. Furthermore, inflationary pressure resulted in higher average bills, particularly in the utility sector, and increased interchange fees. Source: 10-K

Competitors

The company's main competition comes from providers of legacy solutions and systems developed internally by financial institutions. These solutions are often limited in terms of integration, payment methods, and analytics capabilities. The company excels by offering a modern and agile platform that provides an omnichannel eBill payment experience enhanced by AI, ML, and contextualized data. Key competitive factors include security, functionality, rapid deployment, total cost of ownership, customer satisfaction, partnerships, and ability to provide contextual insights.

My Opinion

Paymentus didn't only report an increase in the revenue guidance, management also reported an increase in the number of transactions processed and a new relationship agreement with Oracle. In my view, the company has a solid business model supported by a modern and agile platform as well as a large network of partners. Assuming international expansion, new products and functionalities, and headcount increase, I believe that the company is positioned to capture more electronic bill payments as well as to expand its presence in different industry verticals. Even taking into account risks from relationships with large partners, new regulations, and a potential economic recession in 2023, in my view, the stock is undervalued.

For further details see:

Paymentus: Beneficial Guidance And More Partnership Agreements Imply Undervaluation