PAY - Paymentus: Stock Remains A Long As It Continues To Perform

2023-06-16 10:59:39 ET

Summary

- Paymentus' recent management comments on growth visibility and backlog expansion have strengthened my conviction that FY23 guidance is achievable.

- The next catalyst to stock performance should be PAY regaining its rule of 40 status.

- At the current valuation, PAY is trading at a discount to peers, which makes my modelled upside look conservative as I assume no change in multiples.

Thesis update

My thesis remains largely the same for Paymentus (PAY) with a few key highlights recently that improved my conviction on the name. First of all, it's management comments on growth visibility which gave me comfort knowing that FY23 guidance is achievable. Management stressed that the company's highly recurring business model continues to provide a high degree of revenue visibility in the near future. The company's backlog commentary also gave me hope, as it indicated that the pipeline was expanding healthily, which bodes well for the possibility of a revenue reacceleration in 2024. I believe the repricing of customer contracts by PAY (inflation also driving price up in this case) in 2024 is likely to be a major factor in the near-term growth. Nonetheless, I would stress once again the importance of being wary, as the development of the macro environment does affect the course of business. Therefore, it is prudent to leave some wiggle room in the portfolio so that stock holdings can be increased in size if the price drops further or if other opportunities present themselves.

Growth visibility

I believe investors are waiting to see signs of a re-acceleration in revenue growth, as I mentioned before. I believe the revenue growth spurt in 1Q23 is a primary factor in the stock price increase. Accelerating from 22.2% growth in 4Q22 and 26% growth in 3Q22, 1Q revenue grew by 27%. With this increase, PAY 1Q23 revenue has reached $148.1 million, or $593.2 million on an annualized basis (already within the low end of FY23 guidance). In FY23, I anticipate PAY revenue to be at the upper end of the guidance range because the company is continuing to see healthy demand and bookings conversion. In addition, management has confirmed a sizable backlog caused by larger deals and decisions that were put on hold because of the pandemic. IPN would also be a driver of growth which has the potential to be the game-changer that allows PAY to exceed revenue guidance. Despite only accounting for about 10% of revenue, IPN is expanding rapidly and assisting in the rollout of their bill pay service to more financial institutions. In my opinion, IPN has the capacity to help PAY expand its customer base through the inclusion of billers who are currently not part of their network. This expansion is made possible by considering the bank's payees who are not yet part of the network as potential leads for generating sales. Moreover, management also stressed the importance of noting that they have not factored in any substantial revenue from new wins to the guide. All in all, with 1Q23 annualized revenue already within he guided range, I now see potential for PAY to do much better than expected in FY23, which will lead to a high base for consensus FY24/25 numbers.

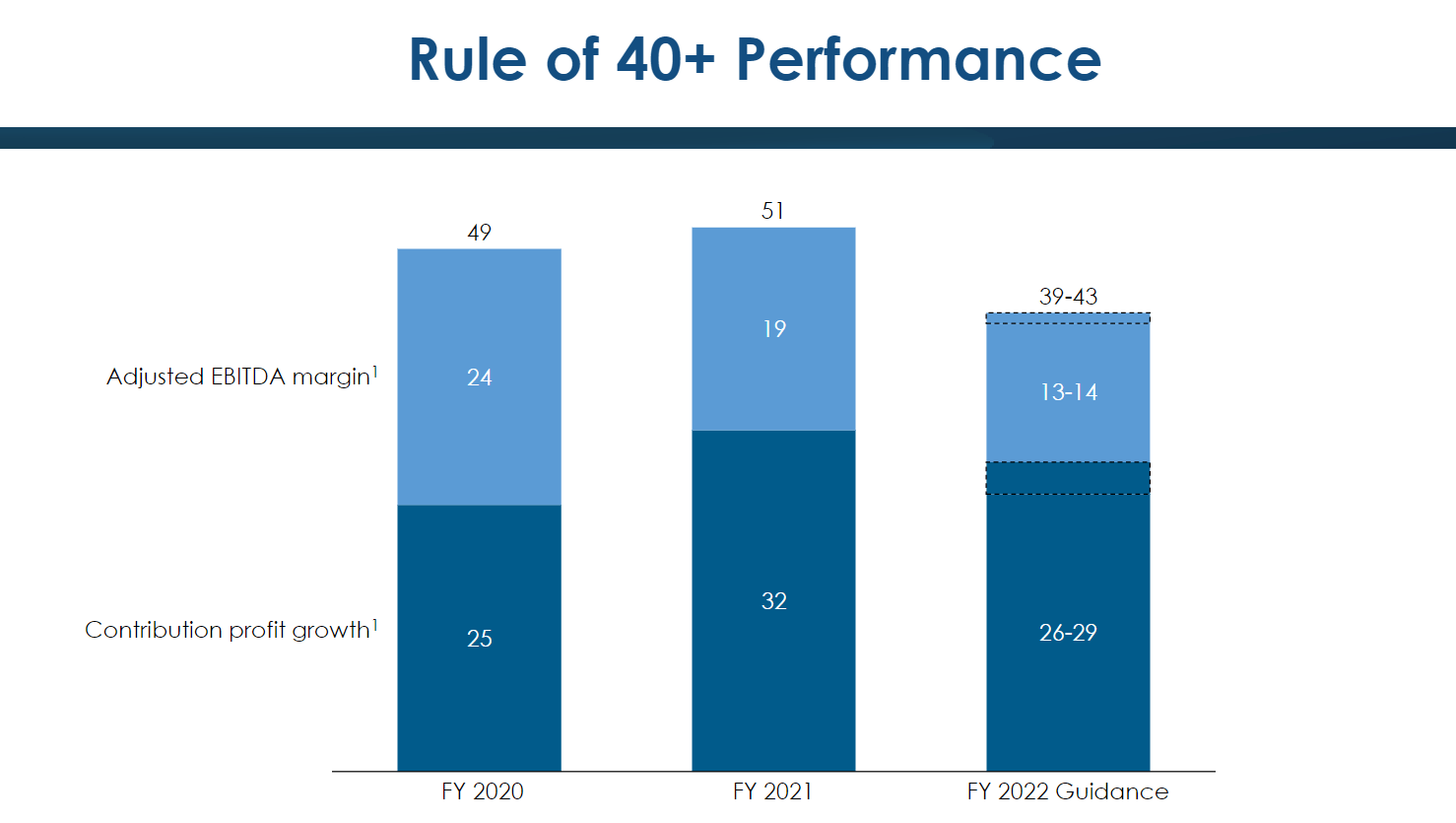

Profitability is the upcoming catalyst

The next catalyst for the stock to rise, in my opinion, will be when PAY regains its rule of 40 status (contribution profit + adj. EBITDA margin). Management has been vocal about this, and the company was in this position prior to the current inflation/interest rate crisis. Both components of the equation have cracked in the last year, with growth slowing to 19% and margins falling to 10%. Now that one part of the equation (growth) has returned to normal (accelerating), the focus has shifted to adj. EBITDA margins (15.7% in 1Q23). I anticipate PAY to begin printing accelerating improvements in adj. EBITDA margins in the coming quarters, as management is now focused on maximizing near-term profitability and is confident that PAY will regain its rule of 40 status in the coming years. I believe PAY can achieve this because as it grows in size due to its scale (note that 1Q23 revenue is the highest quarter revenue ever), economies of scale should benefit contribution margins.

{kind=link}

Valuation

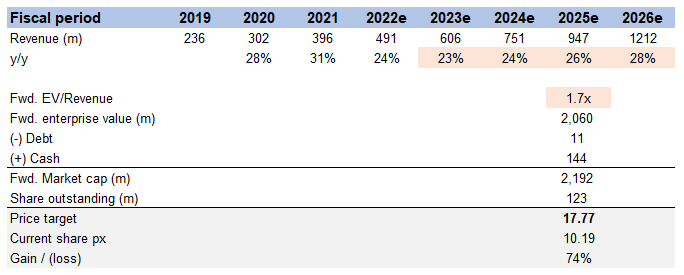

The beauty of long-term investing is that one can take advantage of significant market mispricing. PAY is trading at 1.7x forward revenue, a discount to its historical average, as investors await more evidence of growth and profits. When the macroeconomic environment improves, I believe PAY will continue to accelerate its growth back to previous levels of 20%+. When compared to other similar payment stocks such as Bill.com (BILL), ACI Worldwide (ACIW), Paycor (PYCR), and others, PAY trades at a discount. Taking this into account, my valuation of 1.7x forward revenue may be too conservative.

{kind=link}

Conclusion

My investment thesis for PAY remains largely unchanged, with recent developments strengthening my conviction in the company. Management's comments on growth visibility and the expansion of the company's backlog have provided reassurance that the FY23 guidance is achievable. The growth visibility is further supported by the company's solid performance in 1Q23, with revenue growth reaching 27% and already within the low end of the FY23 guidance range. In addition, I anticipate a potential revenue reacceleration in 2024, driven by the repricing of customer contracts and the growing demand for PAY's services. Looking ahead, I believe profitability will be a catalyst for the stock as the company aims to regain its rule of 40 status by improving adj. EBITDA margins. With PAY trading at a discount compared to similar payment stocks and the potential for accelerated growth, I believe the current valuation may be conservative. Overall, I remain optimistic about PAY's prospects and will closely monitor its performance while being mindful of the macroeconomic environment.

For further details see:

Paymentus: Stock Remains A Long As It Continues To Perform