PAY - Paymentus: Transaction Growth Beneficial Guidance And Cheap

2024-01-17 08:20:46 ET

Summary

- Paymentus delivered better-than-expected EPS and revenue growth, with significant transaction count growth.

- The company's business model focuses on online payment platforms and has partnerships with major banking entities and PayPal.

- Paymentus has a stable balance sheet with a decent amount of liquidity and is experiencing an increase in the number of transactions processed.

Paymentus Holdings, Inc. ( PAY ) recently delivered better-than-expected EPS and revenue growth. It also appears to experience significant transaction count growth. Besides, recent inflation appears to increase the amount of fees obtained from new transactions. In my view, given the recent increase in research and development expenses, headcount growth, and sales and marketing expenses, I think that we may see new innovations in the coming years. There are some risks from changes in the regulation and losses of partnerships with financial institutions. However, I think that PAY could be a bit more expensive.

Paymentus' Business Model And Links With PayPal

Paymentus offers platforms for online payments and related solutions. The main clients of this company are medical, telecommunications, and insurance coverage institutions, which receive payments from their clients through Paymentus.

The operations are divided into three segments according to the geographical operation of the activities: United States, India, and Canada. As mentioned previously, at present, the bulk of the transactions is made from the United States, and the other two segments do not contribute significant income but are affected by different regional legislation that changes the way of business within that market.

The Payments platform works as a SaaS, which allows changes to be made quickly and efficiently based on user trends and demand. Another interesting point that Paymentus has achieved in its insertion within the markets for electronic payment solutions is that it maintains agreements with the largest banking entities in the country to make payments from checking accounts within the platform. It allows payment from PayPal ( PYPL ), one of the pioneers and historical references of this type of business.

Although the company receives income from paying for the subscription to the platform, the percentage of this income has not exceeded 3% in recent years, and the bulk of the income comes from the commission it charges on each transaction made regardless of the type of payment.

Paymentus' Expectations For Q4 2023 Were Beneficial

Recent earnings included better-than-expected quarterly revenue and better-than-expected EPS GAAP Actual earnings. EPS stood at close to $0.05, and quarterly revenue was close to $152 million. Given these figures and the beneficial reaction of the market, I believe that having a look at the recent financials may be beneficial.

Seeking Alpha Source: SA

There is another meaningful piece of information that investors may appreciate. In the last 90 days, out of five EPS revisions, five revisions included an increase in earnings. There is definitely a certain level of optimism in the market.

Seeking Alpha

I also believe that the Q4 2023 guidance given recently is quite beneficial. Paymentus expected revenue close to $155-$159 million, with an adjusted EBITDA of about $12-$14 million .

{kind=link}

Stable Balance Sheet, With A Decent Amount Of Liquidity

Paymentus' balance sheet includes a considerable amount of cash in hand, some accounts receivable, accounts payable, and accrued liabilities. The working capital is not negative. However, given the total amount of cash and little debt, Paymentus does not seem to have problems to finance its operations.

In particular, the company reported cash and cash equivalents worth $162 million, restricted cash and cash equivalents of about $4 million, and accounts and other receivables close to $74 million. Additionally, with prepaid expenses and other current assets of $11 million, total current assets stand at $255 million, and the current ratio is larger than 4x. I do not see liquidity issues here.

The list of assets includes property and equipment worth $1 million, with capitalized internal-use software development costs of $56 million, intangible assets close to $29 million, and goodwill of about $131 million. Total assets are about $489 million, a bit more than that in 2022 .

10-Q

The list of liabilities does not seem worrying, and the lack of financial debt is ideal. Providers offer some financing, so Paymentus does not need to talk to banks. Accounts payable stands at close to $33 million, with accrued liabilities worth $18 million and total current liabilities of about $59 million. Besides, with contract liabilities of about $2 million, total liabilities stand at close to $71 million.

10-Q

Number Of Transactions Processed Increased As New Billers And Financial Institutions Use Paymentus

With a more than 25% increase in the number of transactions reported by Paymentus in the last quarters, I believe that transaction count momentum could continue in the near future. In my view, given the growth in the number of billers and new financial institutions willing to use Paymentus, both economies of scale and network effects could bring FCF margin growth.

The number of transactions processed during the three and nine months ended September 30, 2023 increased approximately 25.2% and 23.7%, respectively, as compared to the same periods in 2022. The increase was primarily driven by the addition of new billers and financial institutions and increased transactions from our existing billers and financial institutions. Source: 10-Q

{kind=link}

Inflationary Pressure And Increased Interchange Fees May Not Be Detrimental For Paymentus' Cash Flow Statement

With the recent increase in inflation, Paymentus reported an increase in the average bills, which may have a beneficial impact on the amount of money collected. In my view, if management successfully negotiates with clients' price adjustments, we may see an increase in profitability and FCF margin growth. In this regard, Paymentus noted the following in the last quarter.

Inflationary pressure is resulting in higher average bills, particularly in the utility sector, and increased interchange fees. While we are seeking to adjust our prices to address the inflationary pressures, our ability to do so typically lags behind the impact of inflation on our clients, the increase in average bill amounts and increased interchange fees. We intend to continue to manage through this uncertain economic environment by working closely with clients on implementations and price adjustments. Source: 10-Q

Paymentus' Headcount Increase And Sales And Marketing Increase Will Most Likely Lead To Net Sales Growth And Client Count Growth

In the last two years, the number of employees increased substantially, driven by increases in sales and marketing. It appears clear that management is expecting further clients and demand for its systems. It would not hire that much if it was not the case. In my opinion, a further increase in the headcount will most likely lead to net sales growth and FCF growth.

The increase in sales and marketing expenses was primarily due to an increase in employee-related costs, including benefits, as we continued to expand our sales and marketing efforts with additional headcount in order to continue to drive our growth. Source: 10-Q

YCharts

Research And Development May Lead To Better User Experience And More Products

With institutions from different sectors through a unified platform mediated by AI algorithms, I believe that Paymentus will be successful because of the different sources of business development, offering solutions direct to customers, and improving user experience. In this regard, I believe that increases in research and development may lead to better product design and usability.

10-Q

I think that R&D expense increases may also lead to expansion in the product offering through new launches, besides seeking to position itself in an industry where it has not yet participated. In addition, achieving expansion into international markets could also bring significant net sales growth. Once payments of its clients within the United States are done successfully, and Paymentus acquires a lot of know-how in the country, management may be successful elsewhere.

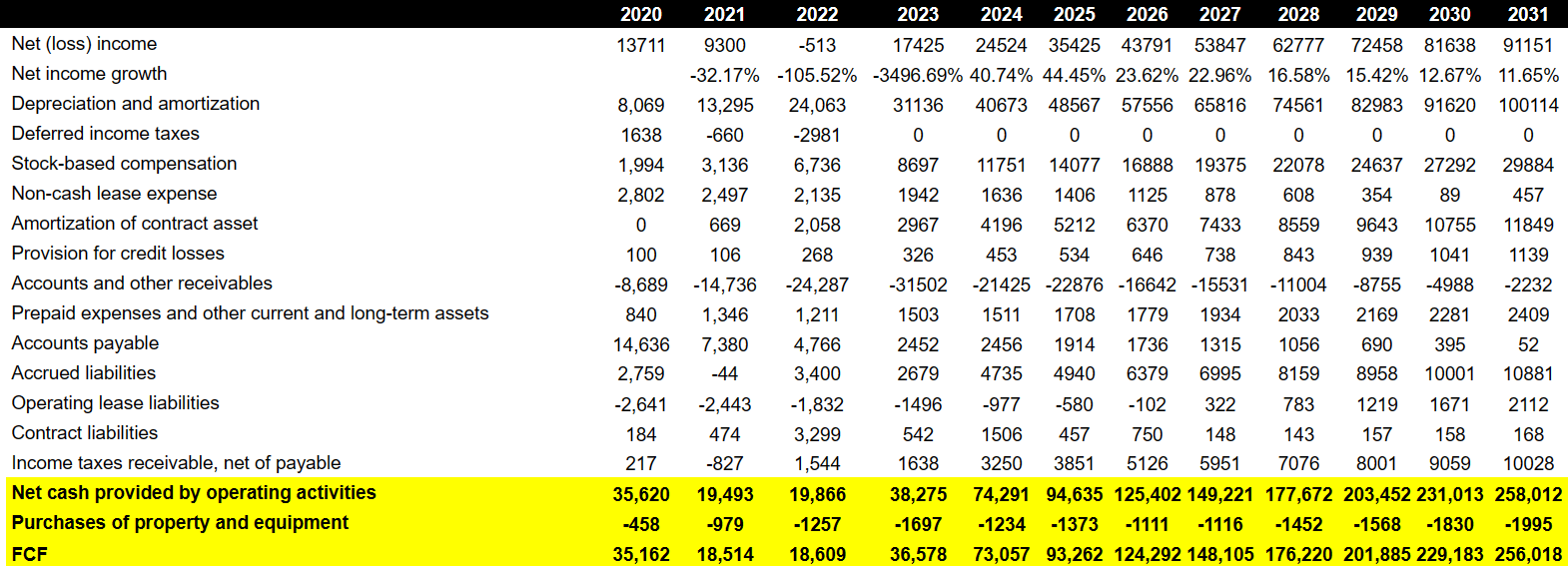

My Financial Model

My expectations include 2031 net income of close to $91 million, with net income growth between 40% and 11% from 2024 to 2031. Also taking into account depreciation and amortization worth $100 million and stock-based compensation of $29 million, I included changes in accounts and other receivables worth -$3 million. Finally, with prepaid expenses and other current and long-term assets worth $2 million, I obtained net cash provided by operating activities worth $258 million, and 2031 FCF would be $256 million. I believe that my figures are quite conservative.

{kind=link}

With other peers reporting a WACC between 6.2% and 10.1% and a median WACC of 9.92%, I assumed a cost of capital of 9.9%. The EV/EBITDA of competitors stands at close to 16x-23x, so I believe that exit multiples may not be far from these figures .

GuruFocus YCharts

With FCF ranging from $73 million to $256 million and a WACC of 9.9%, the net present value would be close to $802 million. With an exit of EV/FCF of 19x, the NPV of future FCF would be close to $2.2 billion. In sum, the implied enterprise value would be close to $3.089 billion. Additionally, with cash, the implied equity value would be $3.2 billion. Finally, the implied price would be $26 per share, and the IRR would stand at 7%.

DCF Model

Competitors

Competition for Paymentus includes financial institutions' development of their own brands for payment solutions. This includes traditional ATM payment methods such as home banking options. In this sense, I believe that these options have become outdated with respect to the dynamics currently demanded by the market. The company's platform valued by technology, together with the adaptability it offers, means a competitive differential compared to the other offers that exist at the moment.

Risks

Within the high economic pressures that the global industry is currently experiencing, part of the risks for Paymentus involves managing its growth as well as having the capacity to set up an international payment network of large companies. In the same sense, the risks inherent to this market force the company to be in a position to develop products and succeed in launching them in the face of innovations from the competition.

In addition, the company's growth may require unavailable amounts of capital to be sustained, and the ability to establish pricing strategies that are attractive to customers will most likely play a fundamental role. I also believe that this type of business is subject to a series of risks associated with legislation, and at this point, it may affect future international expansion or its activity outside the United States.

Conclusion

Given recent headcount growth, double-digit sales and marketing expense growth, and R&D increases, I would expect further business growth in the coming years. Also taking into account the recent increase in the number of transactions, beneficial guidance, and EPS momentum, Paymentus may see further momentum growth in 2024. There are some risks from changes in international legislation with regard to payments or loss of links with large and established financial partners. However, I believe that Paymentus could trade at higher price marks.

For further details see:

Paymentus: Transaction Growth, Beneficial Guidance, And Cheap