FDN - PayPal: Mid-Teens Underlying Growth In Q2 Margin Expansion Guided Ahead

- PayPal stock rose 11% in aftermarket trading on Tuesday (August 2), after the company released Q2 2022 results.

- The confirmation of Elliott Management's $2bn stake was a big positive, but PayPal's operating performance was also reassuring.

- Despite rising macro headwinds, PayPal is continuing a roughly mid-teens underlying growth, excluding eBay and currency.

- Cost savings are in full swing, headcount is already lower than the start of 2022, and EBIT margin is expected to expand 5 ppt in 2023.

- At $99.75, shares are at a 21x P/E (27.5x on GAAP EPS) and expected to return 121% (26.7% annualized) by 2025 year-end. Buy.

Introduction: Why is PYPL Stock Up?

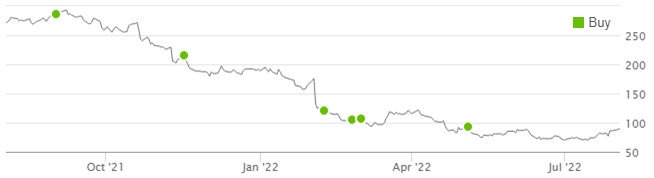

PayPal Holdings, Inc. ( PYPL ) stock rose 11% in aftermarket trading on Tuesday (August 2), after the company released Q2 2022 results . Despite this, PYPL stock remained more than two thirds down from its peak last July:

| Librarian Capital PayPal Rating History vs. Share Price (Last 1 Year) |

{kind=link}

Compared to when we upgraded our rating on PYPL to Buy in May 2020, shares are down 28%, entirely due to the P/E multiple shrinking from 45x (2019 Non-GAAP EPS) at our upgrade to 22x (2021 Non-GAAP EPS) now.

We significantly reduced our forecasts in May, but still expected a mid-teens EPS CAGR, and reiterated our Buy rating. Q2 results support this updated investment case. Excluding losses from the final stages of the eBay ( EBAY ) out-migration, underlying growth was 15% (excluding currency) in Total Payment Volume and 14% in revenues. Non-GAAP EBIT margin fell 7.4 ppt, but cost growth has slowed and PayPal now targets at least 5 ppt of margin expansion in 2023. Management is working with activist investor Elliott Management and added $15bn to its share repurchase program. Our forecasts indicate a total return of 121% (26.7% annualized) by 2025 year-end. Buy.

PayPal Buy Case Recap

Our investment case consists of the following:

- Payment networks are great businesses, thanks to their mission-critical nature, network effect, recurring revenues, natural pricing power, and operational leverage; there is a structural shift to electronic payments

- As a two-sided payment platform with visibility over both parties in every transaction, PayPal has key advantages in data, speed, security, etc.

- PayPal also has a long-term vision of building an integrated payments ecosystem that includes both online and in-store purchases, payments (including P2P and B2C), consumer rewards, Buy Now Pay Later ("BNPL"), etc.

| PayPal Example Innovations in 2020 Source: PayPal results presentation (Q4 2020). |

- There is significant potential in new geographies, beyond the U.S. and the U.K., which were historically 65% of revenues (in 2019)

- PayPal's margin expansion potential in future years is not fully appreciated by investors, as management chose to rapidly increase investments

At its February 2021 investor day, PayPal released targets that included a 2020-25 EPS CAGR of 22% and a 2025 Free Cash Flow ("FCF") of $10bn+, but these were withdrawn in May due to a slowdown in e-commerce penetration growth and macroeconomic headwinds. Management also admitted they had over-expanded and needed to refocus the company on fewer things. We cut our forecasts correspondingly but saw a mid-teens EPS CAGR to be still reasonable.

Our updated investment case has been borne out by Q2 2022 results and new management actions.

PayPal Q2 2022 Results

PayPal's key volume and financial figures for Q2 2022 are as follows:

| PayPal Key Financials (Q 2 2022 vs. Prior Periods) Source: PayPal company filings. NB. All figures are GAAP unless otherwise stated. |

Active Accounts were up 0.4m (less than 1%) sequentially from Q1, in line with management's stated goal of focusing on increasing engagement among existing accounts and letting low-return accounts churn. Active Accounts were still up 6.5% year-on-year, thanks to Net New Accounts in prior quarters.

Number of Payment Transactions grew 16.5% sequentially and 6.8% year-on-year, faster than the growth in accounts, as Transaction Per Account continued to grow. 80% of PayPal's volume was driven by 30% of its active accounts.

Total Payment Volume ("TPV") grew 9.3% year-on-year (13% excluding currency) and 5.3% sequentially, despite the drag from the final stages of the eBay outmigration. Excluding eBay, TPV grew 11% (15% excluding currency). TPV growth was driven by merchants, especially with Braintree; P2P TPV grew just 3% and Venmo TPV grew just 6%.

Transaction Revenues grew 8.2% year-on-year and 4.6% sequentially, slightly less than TPV. Transaction Take Rate was 1.85% for Q2, slightly below the 1.86% in both the prior-year quarter and Q1. Transaction revenue growth was mainly driven by Braintree and Venmo (Venmo revenues grew 50% in Q2 and exceeded $100m in June); it was also helped by gains in currency hedges that were recorded as Transaction Revenues.

Other Value-Added Services revenue rose 21.1% year-on-year and 10.1% sequentially, much more than TPV, a s result of growth in credit products as well as in interest income on customer stored balances.

Total Net Revenues was up 9.1% year-on-year (10% excluding currency) and 5.0% sequentially. Excluding eBay revenues, which fell 60% year-on-year to just $166m, revenues grew 14% year-on-year (including currency).

Transaction Expense grew 20.6% year-on-year and 8.1% sequentially, faster than volume "largely" due to the mix shift to Braintree, which is "predominantly" card-funded and involved PayPal paying for funding fees.

Transaction & Loan Losses comparisons are distorted by one-off credit reserve releases of $156m in the prior-year quarter and $104m in Q1.

Other Operating Losses rose 5.5% year-on-year but fell 1.4% sequentially, both less than revenues, as management actions to reduce costs started to produce an impact. Sales & marketing spend was down 7% year-on-year, and PayPal's headcount is now lower than at the start of the year. Management aims to make non-transaction-related expenses "roughly flat" as it exits 2022.

GAAP EBIT was $764m. The $538m gap between GAAP and Non-GAAP EBIT was largely due to $329m of stock-based compensation costs and $119m of amortization of acquired intangible assets.

Non-GAAP EBIT declined 21.3% year-on-year and 3.1% sequentially, as a result of costs growing faster than revenues. The year-on-year decline was similar to that in Q1 (19.7%). Non-GAAP EBIT margin fell 7.4 ppt year-in-year.

GAAP Net Income was negative in Q2 due to $715m of "Other Expense," likely mark-to-market losses on equity investments and debt securities (as rates rose), and an atypically high $390m tax expense.

Still Growing at Mid-Teens ex-eBay

Excluding eBay, underlying growth has continued at mid-teens despite larger macro headwinds - a key positive.

Q2 year-on-year TPV growth was 13% excluding currency, but 15% if also excluding eBay. This was a strong performance after last year's TPV growth of 36% excluding currency and 43% also excluding eBay:

| PayPal TPV Growth ( S ince Q4 2019 ) Source: PayPal company filings. |

Similarly, excluding eBay, year-on-year revenue growth was a relatively consistent 15% in Q1 and 14% in Q2 (including larger currency headwinds in Q2). With eBay volumes becoming smaller, year-on-year revenue growth (excluding currency) accelerated from 8% in Q1 to 10% in Q2:

| PayPal R evenue Growth ( S ince Q4 2019 ) Source: PayPal company filings. |

Similarly, as eBay volumes became smaller, year-on-year revenue growth (excluding currency) also accelerated within Q2, from 7% in April to 10% in May, 12% in June, and 14% in July month-to-date.

New FY22 Outlook

Broadly mid-teens underlying growth (excluding eBay and currency) is also expected for full-year 2022, despite growing macro headwinds.

Due to macro headwinds, PayPal has reduced its 2022 outlook slightly to:

- TPV growth of 16% excluding currency (was 15-17%)

- TPV growth of 12% including currency (was 13-15%)

- Revenue growth of 11% excluding currency (was 11-13%)

- Revenue growth of 10% including currency (was 11-13%)

| PayPal 2022 Outlook Headlines Source: PayPal results presentation (Q1 2022). |

The outlook includes a further $125m decline in eBay revenues in H2, after $625m in H1. Revenue growth is expected to accelerate each quarter, from 10% in Q2 to 12% in Q3 and 14% in Q4 (excluding currency). The outlook for Q3 year-on-year revenue growth includes a 150 bps headwind from Paycheck Protection Program revenues last year.

2022 revenue growth excluding eBay is expected to be 13.5%, or 14.5% excluding currency.

2022 Non-GAAP EPS is now expected to be $3.87-3.97 (was $3.81-3.93), and GAAP EPS is expected to be $1.52-1.62 (was $2.19-2.34), though EPS is a less meaningful metric due to credit reserve builds/releases and mark-to-market investment losses. 2022 FCF is still expected to exceed $5bn.

Importantly, the outlook now also includes significant cost savings and margin expansion.

Significant Benefits from Cost Actions

Cost savings at PayPal are generating significant benefits and will likely result in margin expansion in 2023.

PayPal is targeting $900m of cost savings in 2022, and these are expected to produce a benefit of $1.3bn in 2023. Management described these as "identified" savings, with "nearly 50%" coming from transaction-related expenses. Management also stated they have "renegotiated contracts across many of (their) suppliers." CEO Dan Schulman stated that cost actions taken will help PayPal "exit the year with operating margin leverage that will continue to grow in 2023."

While management is not providing explicit 2023 guidance, and budgets are actually still being prepared, interim CFO Gabrielle Rabinovitch stated management are "targeting at least 50 bps of operating margin expansion," which would reverse most of the approximately 7 ppt decline seen in H1 2022 so far.

The overall driver for these is PayPal's scale and ecosystem, in line with our thesis about the PayPal platform's natural advantages.

Sizing Up Share Buybacks

PayPal is also sizing up share buybacks, partly to take advantage of the deflated share price.

The Board has authorized a new $15bn buyback program, adding to the approximately $3bn already authorized. Management expects 2022 buybacks to be approximately $4bn, equivalent to 3.5% of the current market capitalization. CEO Dan Schulman stated on the call that:

We expect the pace of our share repurchases to remain aggressive as we believe there's currently a unique and attractive opportunity to return capital to our shareholders."

Buybacks already totaled $2.25bn year-to-date, including $750m in Q2, and PayPal's average share count was 2.4% lower year-on-year in Q2 2022.

In addition, management is also exploring other capital options, including another potential "credit externalization event" similar to the sale of PayPal's $6.8bn U.S. consumer card receivables to Synchrony Financial ( SYF ) in 2018. PayPal's gross receivables stood at $6.2bn at the end of Q2 and, while not all of this will be suitable for disposal, an "externalization" could help reduce the cashflows needed to fund future credit product growth.

Elliott Involvement

PayPal confirmed that activist investor Elliott Management has become involved with the company.

First reported by the Wall Street Journal in July (subscription required) , Elliott's stake was confirmed to be approximately $2bn in PayPal's earnings release, implying an approximately 2% ownership of PayPal shares.

Management confirmed that Elliott has signed an information sharing agreement to facilitate collaboration, and CEO Dan Schulman described the two sides as "substantially aligned on the areas of focus for achieving our objectives."

Elliott's involvement is a positive, both in signaling the attractiveness of PayPal shares and in helping management focus on efficient and shareholder-friendly capital allocation.

Valuation: Is PayPal Stock Expensive?

PayPal's valuation is attractive for a company we believe can achieve mid-teens EPS CAGR.

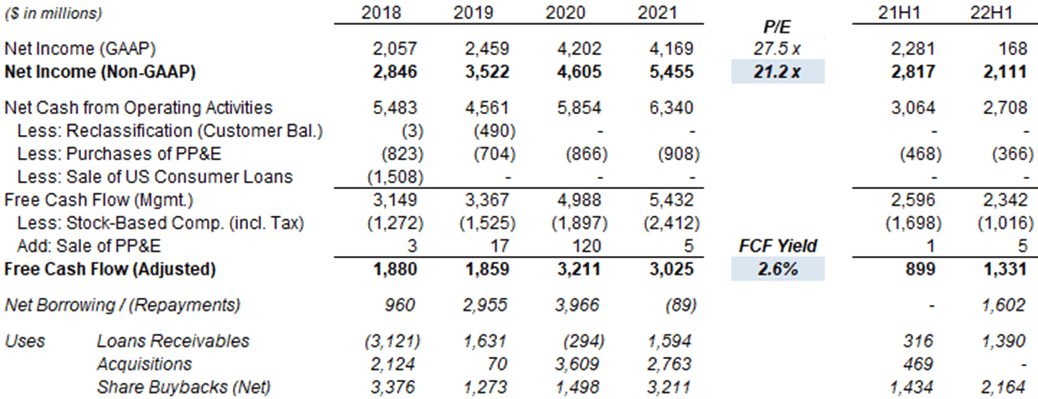

At the aftermarket price of $99.75, relative to 2021 financials, PYPL stock is trading at a 21.2x P/E on Non-GAAP EPS and a 27.5x P/E on GAAP EPS; FCF Yield, after deducting share-based compensation, is 2.6%:

{kind=link}

Relative to the mid-point of the latest 2022 outlook, PYPL stock is trading at 25.4x Non-GAAP EPS and 63.5x GAAP EPS. Management guided to FCF exceeding $5bn (on their definition) in 2022, broadly consistent with 2022.

PayPal Stock Forecasts

We update our 2022 EPS forecast in line with guidance, but keep other assumptions unchanged:

- 2022 EPS to be $3.92 (was $3.87)

- Thereafter EPS growth to be 15%

- No dividends

- Share count to fall by 1.0% annually

- P/E to be at 37.5x at 2025 year-end

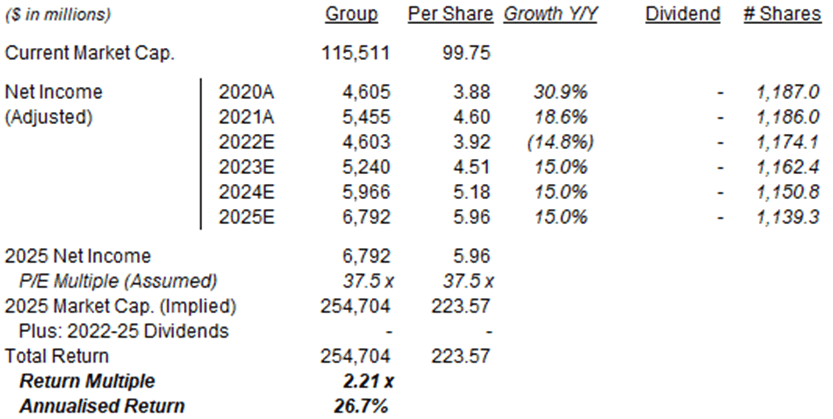

Our new 2025 EPS forecast is 1% higher than before ($5.89):

{kind=link}

With shares, we expect an exit price of $224 and a total return of 121% (26.7% annualized) by 2025 year-end. The exit price is 28% lower than PYPL's peak of around $310 in July 2021.

Conclusion: Is PYPL Stock a Buy?

We reiterate our Buy rating on PYPL stock.

For further details see:

PayPal: Mid-Teens Underlying Growth In Q2, Margin Expansion Guided Ahead