PYPL - PayPal Q2: A Brilliant Outlook And A Discounted Share Price (Rating Upgrade)

2023-08-03 09:00:08 ET

Summary

- PayPal Holdings, Inc. Q2 results were in line with expectations, but the stock fell 8% premarket nevertheless.

- The company's long-term potential remains strong, with expected double-digit growth in TPV through 2026.

- PayPal's position as a leading payment solution, partnerships with tech giants, and focus on new payment solutions contribute to its growth potential and should drive double-digit EPS growth through FY26.

- I remain bullish on PayPal and its long-term prospects. The company is given no credit by the market at all despite its strong performances and criminally low valuation, creating an opportunity for investors.

Investment thesis

I upgrade my rating on PayPal Holdings, Inc. ( PYPL ) to a strong buy and update my revenue and EPS estimates following the company’s Q2 results . PayPal reported financial results in line with the consensus but fell 8% premarket. Meanwhile, I remain bullish on the company’s long-term potential and believe it should continue to grow its TPV by double digits through 2026.

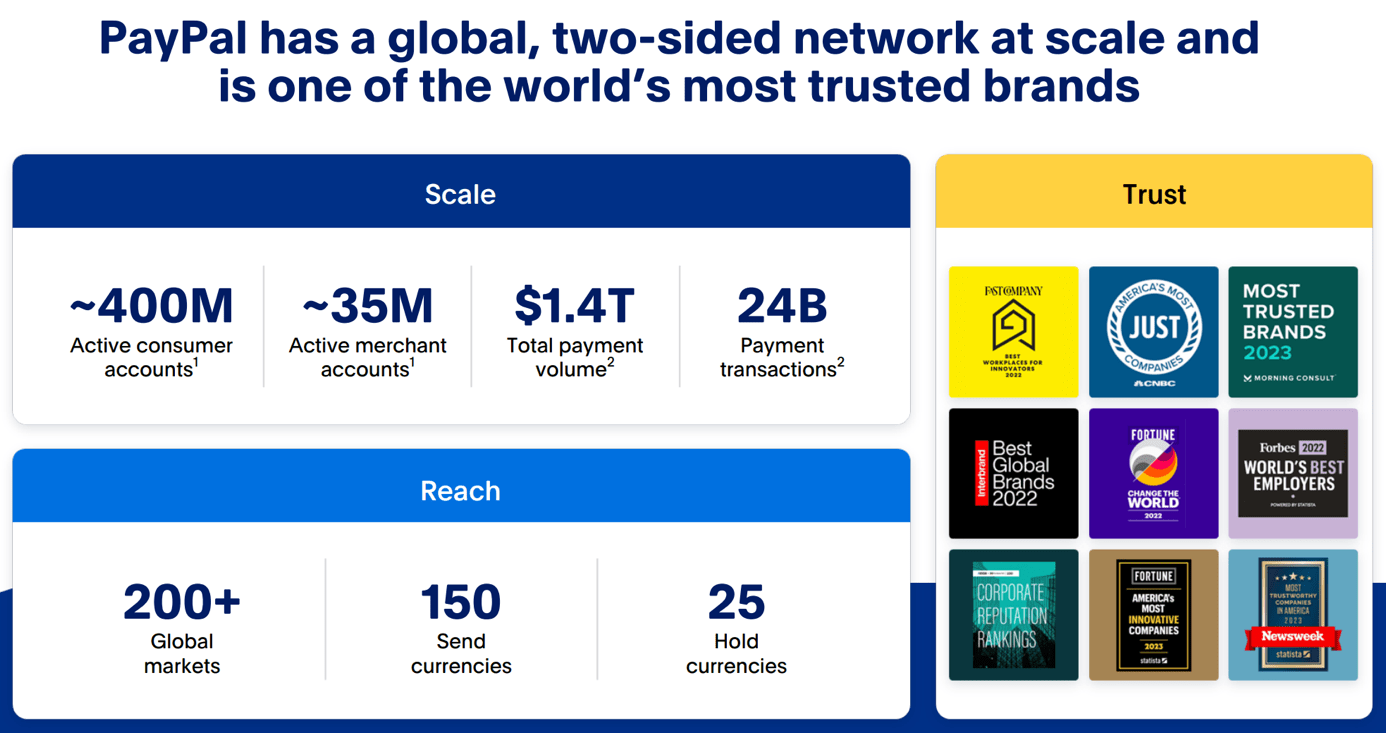

The company's continued solid growth across the board and positive signs of a faster-than-expected recovery in digital payments should drive a solid FY23 result and strong momentum going into FY24. One key factor driving growth is the increase in transactions per account. As PayPal's customer base is already substantial at 431 million active accounts, future growth is expected to be primarily fueled by TPA growth, driven by new payment solutions and improved customer experience, enhancing customer engagement.

Looking ahead, PayPal's long-term outlook appears incredibly promising. The company's position as a leading payment solution on e-commerce platforms, its efforts to expand partnerships with tech giants, and its focus on new payment solutions like BNPL contribute to its growth potential. PayPal's global moat and strong market share in the online payment processing industry are additional strengths.

In this article, I will take you through the latest developments and financial results and update my estimates and view on the company accordingly.

A very decent quarter for PayPal

PayPal reported its Q2 results yesterday, August 2, and reported revenue and EPS in line with the consensus. The company continues to see solid growth across the board and positive signs of a faster-than-expected recovery in digital payments, which could boost the company’s H2 result. Yet, despite this solid performance, shares are down quite significantly premarket, falling over 8% at the time of writing. And while not everything in the earnings report was positive, I remain bullish on the company’s long-term prospects, especially as the company seems to be hated by the market at the moment, creating attractive long-term opportunities for investors.

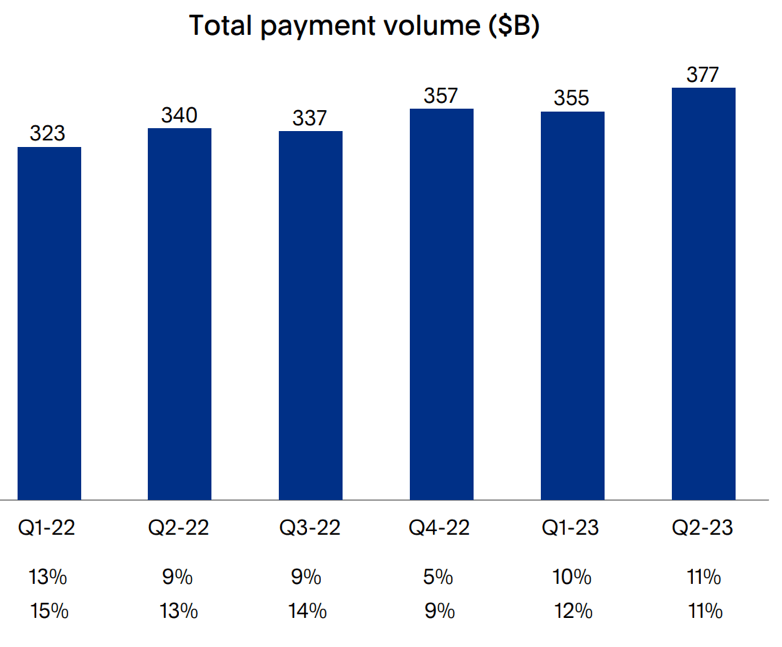

Looking at the Q2 results , TPV (total payment volume) grew by 11% in Q2 to $376.5 billion, driven by a 10% increase in transactions and a 12% increase in transactions per account. Especially the fast-growing number of transactions per account ((TPA)) is something that excites me. As it will become harder and harder for PayPal to meaningfully grow its customer base due to the large existing base of 431 million active accounts, I believe future growth should primarily be fueled by TPA growth, which should be boosted by the introduction of new payment solutions and an improved customer experience, causing a higher customer engagement.

This is why it is especially important to keep a close eye on this metric to monitor how the company is doing in increasing customer engagement, which has been positive so far. That it is indeed hard to grow the user base is highlighted by the fact that PayPal was only able to grow active accounts by 0.4% YoY in Q2, which is somewhat disappointing still. Yet, we can expect this to accelerate again once the macroeconomic environment improves and digital payments growth accelerates. Though, I expect this to remain relatively low in the low to mid-single digits in the long run.

{kind=link}

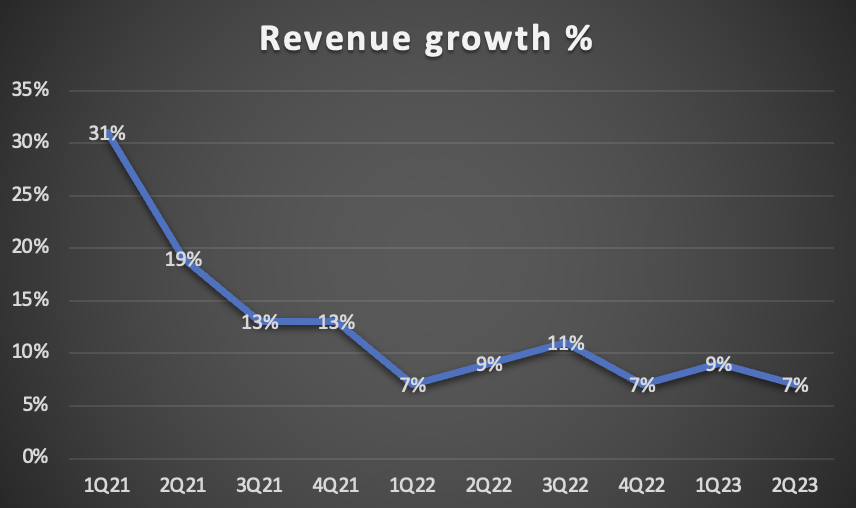

Driven by this increase in TPV, PayPal reported revenue of $7.3 billion, up 7.1% YoY as growth is slowing down from a 9% reported growth in Q1 but has been stable in the high single digits as visualized below. The difference in revenue and TPV growth was caused by a hard YoY revenue comparison due to some positive one-offs last year. Excluding this, revenue growth would have come in at 9% to 10%. Also, the take rates showed a minor YoY decline, but this was largely driven by FX changes.

{kind=link}

Crucial to the Q2 performance was a stabilization in the very important e-commerce industry, as also highlighted by the Deutsche Post ( DHLGY ) quarterly results from earlier this week, which pointed to a 4% increase in e-commerce volumes YoY. This stabilization has come a lot earlier than anticipated by management, which should be positive for PayPal’s payment volume. The stabilization has already become visible in PayPal’s monthly data as branded checkout growth is increasing again, from 6.5% in June to 8% in July. This should improve further as e-commerce growth picks up.

Looking at the regions, the U.S. was the largest driver of growth as it saw growth of 9% against 5% growth in international markets. Transaction revenue grew by 5% to $6.6 billion, driven by a strong performance in Braintree and branded checkout. Value-added services grew at a much quicker 37% but from a lower revenue base to $731 million.

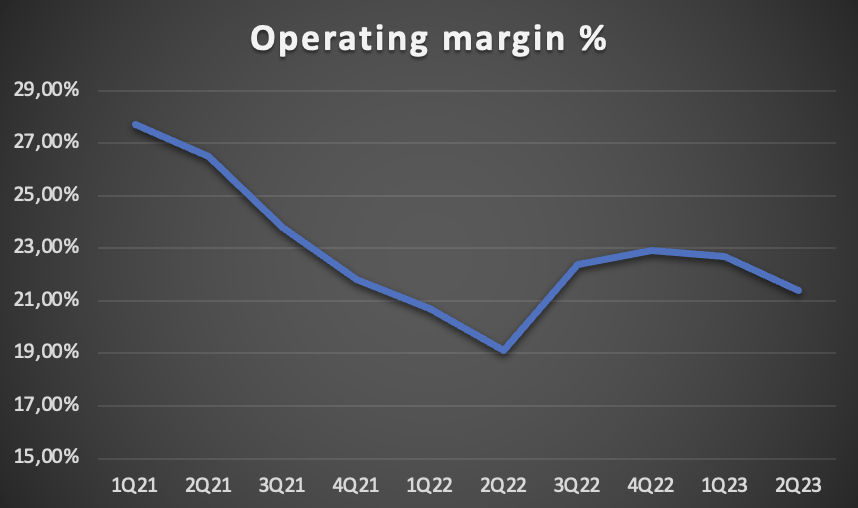

In Q2, management continued to execute its cost-saving strategies and, through solid cost discipline, was able to lower its (non-transaction-related) operating expenses by 11% YoY, which allowed for an operating margin expansion of 230 basis points YoY to 21.4% or $1.6 billion, up 20% YoY. As highlighted in the graph below, the slower reported growth rates heavily impacted the margins throughout FY21 and the first half of FY22 as these dropped rapidly. Now, since management acknowledged that its growth expectations were too rosy and its investments and costs too high, it has been able to boost margins again, perfectly illustrated in its latest quarter. For FY23, the operating margin should expand by 100 basis points YoY. Meanwhile, EPS was $1.16, up 24% YoY, again due to margin improvements.

{kind=link}

PayPal ended the quarter with a total cash balance of $14.4 billion against $10.5 billion of debt. Its balance sheet remains in excellent health and provides the company with enough room for significant further investments and, of course, share buybacks. In Q2, the company repurchased $1.5 billion worth of shares and expects this to amount to $5 billion for the full year, which is well covered by the $5 billion expected free cash flow ("FCF"). The company has once more confirmed its desire to return capital to shareholders and has taken an aggressive approach by returning 100% of its FCF this year. Since 2021, this has resulted in a 6% reduction in its share count. I expect this to remain a focus point for management and believe we might start to see a dividend paid by PayPal in the next couple of years as the business stabilizes further and growth remains stable.

The long-term outlook for PayPal remains incredibly promising, making its current valuation quite ridiculous

In part due to the better-than-expected performance in e-commerce payments, management believes the second half of the year could come in better than the first half of the year, but for now, sticks to its overall expectation of a relatively comparable second half with growth in the high single digits, although likely to come in around 10-11% when looking at the slight macroeconomic improvements. This includes a slightly lower Q3 expectation due to a tough comparable with Q3 last year due to positive one-offs, resulting in Q3 guidance of $7.4 billion, up 8% YoY, and the expectation of a return to double-digit growth by Q4.

Driven by the expected 100 basis points of operating margin expansion, EPS growth should remain in the mid-double digits range in the second half of the year, which is why management sticks to its EPS guidance of approximately $4.95, representing 20% growth YoY. Q3 EPS is projected to come in at $1.22-$1.24, up 13% to 14%. Management also leaves the FCF expectation for FY23 unchanged and continues to expect $5 billion in FCF.

Diving a bit deeper into its long-term outlook, we can comfortably say that e-commerce will remain a strong tailwind for the company with the industry projected to keep growing at a CAGR of 15.2% , according to Mordor Intelligence. PayPal will benefit from this growth as a leading payment solution on e-commerce platforms like Amazon. In fact, e-commerce is one of the leading drivers of growth in digital payments, which as a whole are expected to keep growing at a CAGR of close to 12% through 2027. This means that PayPal, as one of the industry leaders, should continue to see strong growth in its payment volumes, even if it would lose market share to the increasing competition in the industry.

And as PayPal remains committed to growing the reach of its platform, which is highlighted by the announcement by Microsoft ( MSFT ) about last quarter, it should be able to fully benefit from these growth drivers. The company will be integrating more PayPal payment solutions on Microsoft platforms, including pay-later options. This deal should work for PayPal as it makes its platform even more useful for Microsoft customers and gives it more payment volume growth potential.

Of course, this deal in itself is not going to move the needle very meaningfully, but I do appreciate PayPal’s efforts to extend and deepen partnerships with these big tech giants with millions of paying customers. Late last year, the company announced the integration of Venmo into Amazon ( AMZN ) and a deeper partnership with Apple ( AAPL ) to integrate more PayPal solutions into Apple Pay, which most definitely could be a needle mover if the company starts benefitting more from Apple Pay users, of which there are many.

{kind=link}

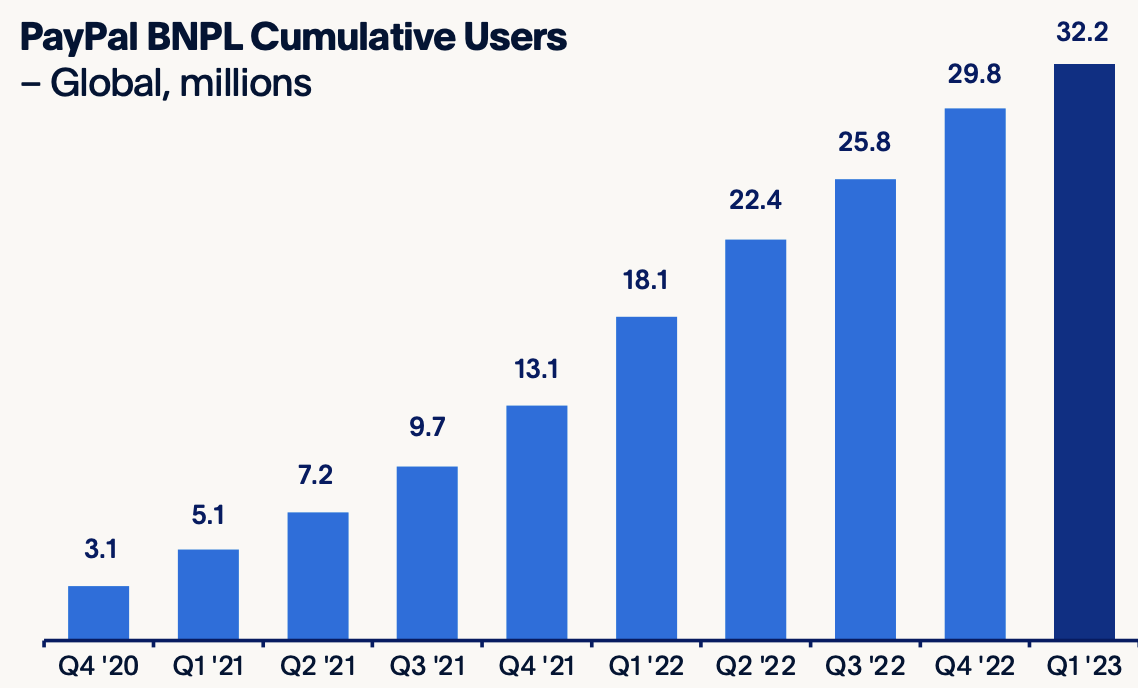

These partnerships are crucial to extend the company’s product reach and increase its user numbers and payment volume. Ultimately, the payment solution that can be used in most places has the strongest moat. Also, the company remains committed to further developing its transaction solutions to improve the customer experience, creating higher customer engagement. For example, the company has been working on simplifying its branded payout and has rolled out the ability to log in without a password globally. The introduction of new payment solutions like BNPL in more regions should also boost PayPal's usefulness to both consumers and merchants and drive growth in numbers for both, as highlighted by the rapid growth PayPal has seen in the adoption of this new payment method.

{kind=link}

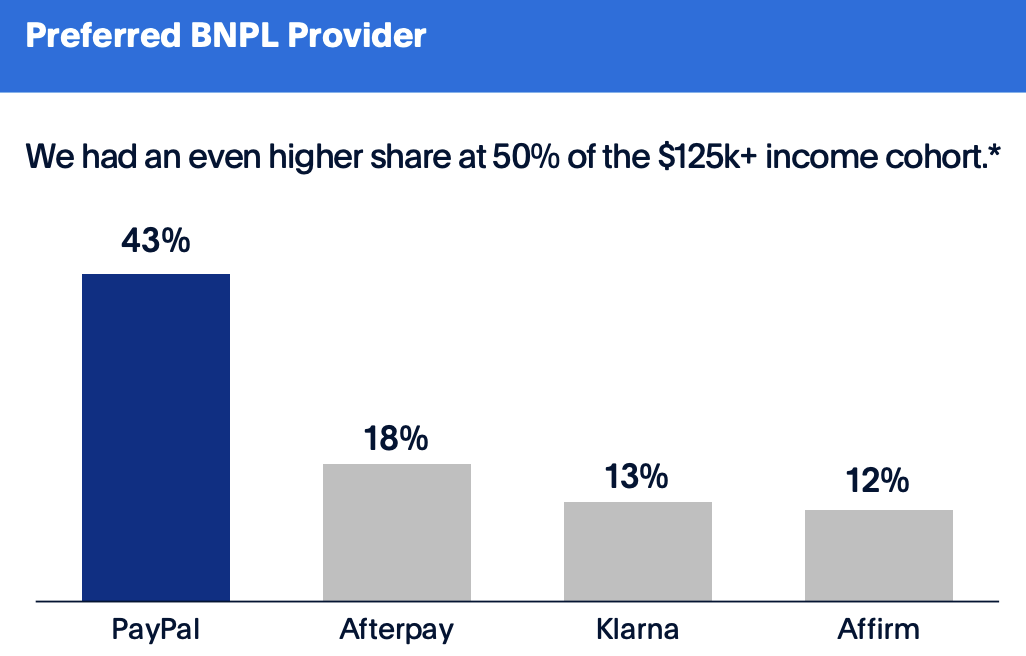

Furthermore, according to PayPal, the platform is the preferred buy now, pay later ("BNPL") platform among consumers with 43% of BNPL users leveraging the PayPal platform. Among the high-income cohort, PayPal even reaches a share of above 50%, according to a survey performed by JPMorgan . This positions PayPal extremely favorably to benefit from the future growth in BNPL adoption, driving the industry to grow at a CAGR of 22% through 2030. I believe BNPL could become an even more meaningful growth driver for the company in future years.

{kind=link}

Also, with the fintech market projected to grow at a CAGR of 19% through 2028, driven by new payment solutions and higher adoption of these new ways of payment, PayPal’s commitment to expanding its number of solutions and improving its customer experience is crucial to maintaining its lead.

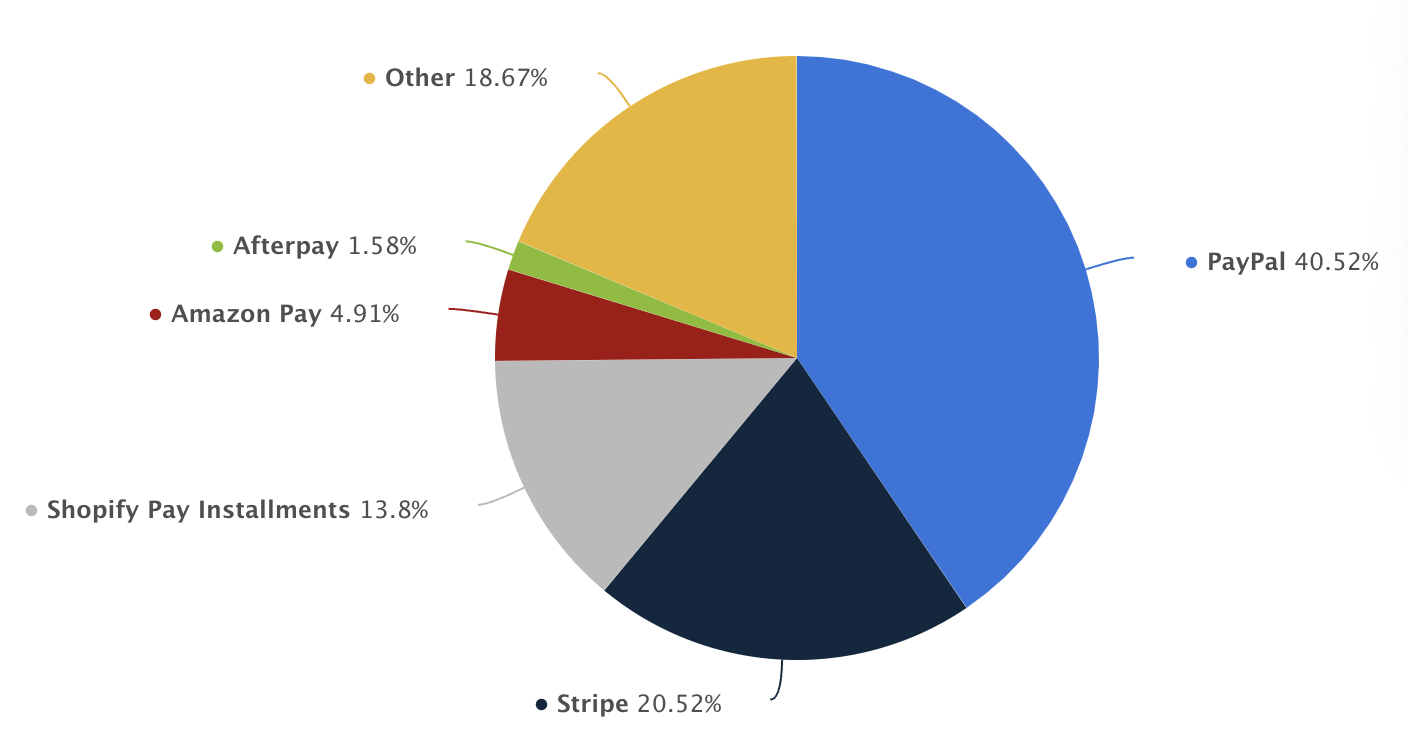

As of July 2023, the company is said to hold a very strong 40.52% market share globally in the online payment processing market, down 135 basis points from when I last covered the company in May. Though, it should be noted that these percentages can fluctuate. Still, this gives it significant size advantages to outpace competitors in technological development, especially in its global moat, as highlighted by its excellent availability. Finding a digital store where PayPal is not a payment option is hard. And in the end, for PayPal, a strong global presence will result in increasing user numbers, which causes higher merchant adoption, creating a strong vicious cycle. With global availability being the strongest moat in the payment industry, PayPal holds the best cards today. This is why I remain bullish on PayPal’s growth and believe it should be able to keep its market share in the payments industry relatively stable. Overall, I project its market share to remain above 34% by 2028.

market share globally in the online payment processing market (Statista)

{kind=link}

Going by everything discussed above and the expected industry growth, PayPal should be able to keep its payment volume growth in the low-double digits for the foreseeable future. I see revenue fluctuating in the same range as payment volume, although I do expect the take rate to drop slightly further as PayPal will need to keep its pricing competitive as the industry becomes more competitive. Meanwhile, EPS growth will remain in the low to mid-double digits as the company sees a lot of room for margin expansion in the coming years as new advancements like AI allow it to do things smarter and cheaper. This should result in further margin expansion, while share buybacks will also have a positive impact on EPS growth.

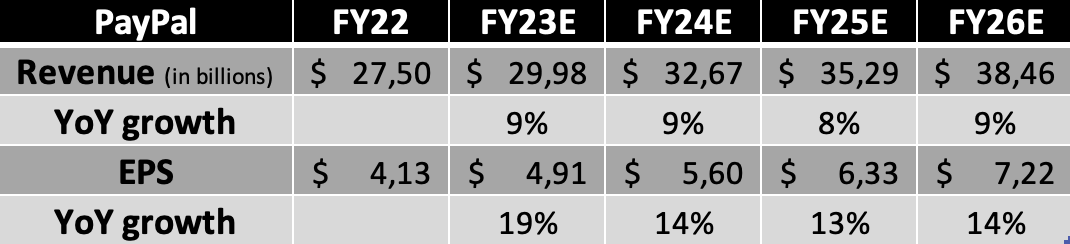

Following this analysis, the company’s Q2 results, and the Q3 and FY23 guidance, I now project the following financial results through FY26.

{kind=link}

(This includes a Q3 revenue of $7.47 billion and EPS of $1.23.)

Shortly explaining my FY23 estimates (as my long-term outlook has largely been explained above), I now expect PayPal to report revenue of $29.98 billion in FY23, fueled by a slightly stronger H2 compared to H1. This is also up slightly from my previous revenue estimate. I believe this will be driven by a slight recovery in the e-commerce market and an improving macroeconomic outlook which should boost consumer spending, also fueled by lower inflation levels. Meanwhile, I have slightly lowered my EPS outlook for FY23 as I expect PayPal to report EPS that sits slightly below its current estimate due to somewhat higher costs.

In addition, I have increased my long-term EPS and revenue estimates as I continue to see incredible long-term potential for PayPal and the high probability of it holding on to its strong payment processing market share, driven by strength in BNPL and a focus on introducing new payment solutions and improving the customer experience.

As a result of my higher estimates, the current valuation looks even more ridiculous. PayPal is currently trading at a forward P/E of 13.7x based on my (below average) FY23 EPS estimate and its current pre-market share price of $67.50. This means it is trading at a 60% discount to its 5-year average valuation. And while I would agree that its growth outlook is not as strong as it was perceived to be for the majority of the last 5 years and a P/E of 36x is far from justified, a 13.7x P/E for a company with a 40% market share in the digital payment processing industry and projected to grow its P/E at mid double digits for the foreseeable future is simply ridiculous.

Considering everything discussed throughout this article and in my initial coverage of the company back in May, I believe a P/E of 18x is fully justified. This is up from my previous fair value P/E of 15x as my outlook for the company and its risk profile have improved. Based on this belief and my FY24 EPS estimate, I calculate a target price of $101 per share, leaving an upside of 50% from its pre-market share price. (Please note, this target price is solely based on its forward P/E and is only for indicative purposes.)

Going with an annual return of slightly over 11% to assure a solid risk-reward profile, a current fair value share price sits around $87 per share.

Conclusion

Similar to when I covered the company in May , PayPal Holdings, Inc. shares are trading at a massive discount to fair value as the market seems unwilling to give the company any credit right now. This is probably still the result of the company’s massive downfall over recent years as a result of COVID-19 tailwinds disappearing and management overestimating its growth potential. So yes, I can see where it is coming from but that still does not justify the current valuation.

The company continues to report excellent financial results and remains focused on strengthening its market share through new product releases and an improved customer experience. I remain very bullish on PayPal’s long-term outlook and believe the company remains perfectly positioned to benefit from growth in the fintech, e-commerce, and digital payments industry. Its moat is sticky, and it should be able to hold onto it relatively well despite increasing competition.

With shares still undervalued, I upgrade my rating on the company to a rare strong buy. I see an upside of 50% over the next 1.5 years and believe PayPal Holdings, Inc. stock is a no-brainer at any price below $85 per share.

For further details see:

PayPal Q2: A Brilliant Outlook And A Discounted Share Price (Rating Upgrade)