PSFE - Paysafe: Has The Selloff Gone Too Far?

2023-05-23 04:59:00 ET

Summary

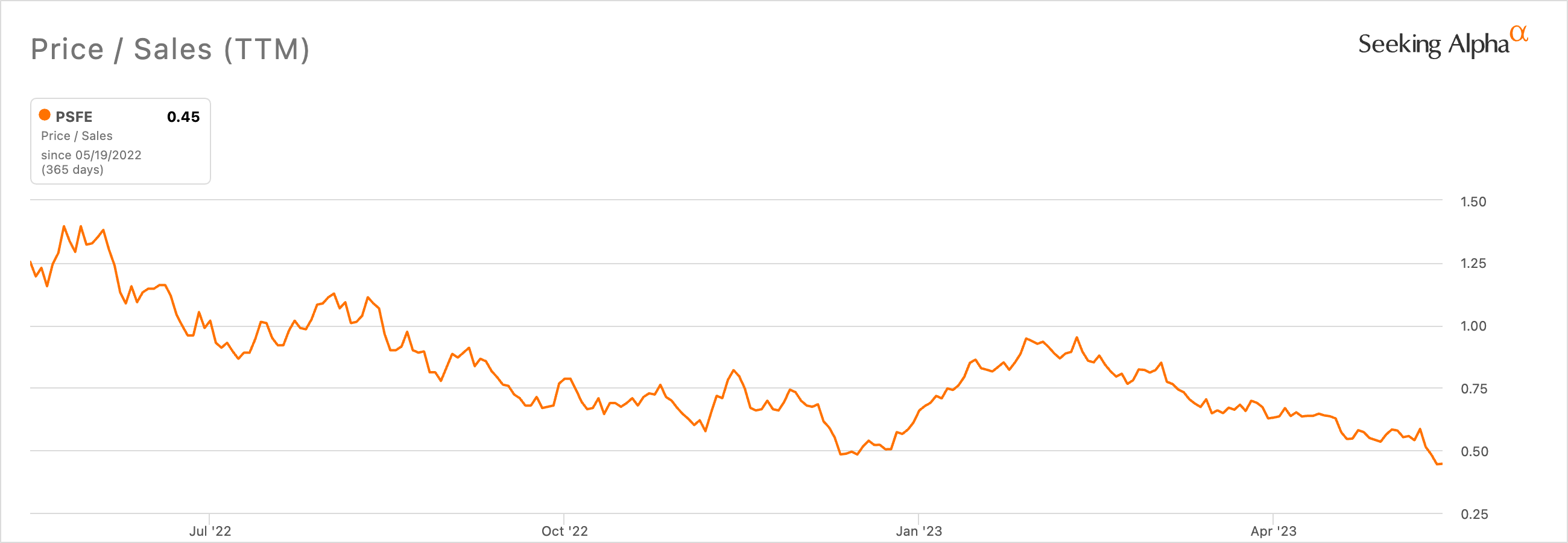

- Paysafe's selloff deepened this year with the stock down 22% to trade on a 0.45x multiple to trailing 12-month revenue.

- This is less than half the multiple in the same period last year despite revenue being much higher.

- 2023 will likely see the stock continue to experience headwinds to an expansion of its multiple. This might start to change once the Fed starts cutting interest rates.

Is Paysafe ( PSFE ) now a buy after a 22% decline since the start of the year? At some point a selloff becomes overextended and PSFE stock now trades at 0.45x its trailing 12-month revenue as of the end of its fiscal 2023 first quarter. This is 80% lower than its sector median and comes at a time when broader macroeconomic concerns continue to weigh down on the valuation of growth-orientated stocks. Paysafe's investment pitch has always been built on its strong position in the fast-growing iGaming space. This was meant to be a secular growth story as more US states liberalized their gambling laws to allow for online gambling.

Paysafe is one of the most widely used payment providers for the online gambling industry with its payment solution used by PokerStars, DraftKings, and Golden Nugget Online Casino among other gambling firms. Online sports betting is only legal in around 37 states with Kentucky's HB 551 legalizing sports betting signed into law at the end of March this year. This all comes five years after the supreme court struck down a federal law that barred gambling on football, basketball, baseball, and other sports in most states.

{kind=link}

The market sentiment towards Paysafe is getting worse. Indeed, its price-to-sales multiple has been cut in more than half over the last 12 months alone. It's also down from an 8x sales multiple from when the company went public via a blank check company in the spring of 2021. To be clear, Paysafe has to earn around twice the revenue it did exactly a year ago to trade on the same market cap. Bears, who form the 4.75% short interest, would be right to state that the company's current market cap at $676 million is set against slow and almost anemic revenue growth and net losses. The latter factor of unprofitability in a broadly risk-off environment has rendered stocks like Paysafe to be difficult investments for most investors.

The Fiscal 2023 First Quarter Earnings

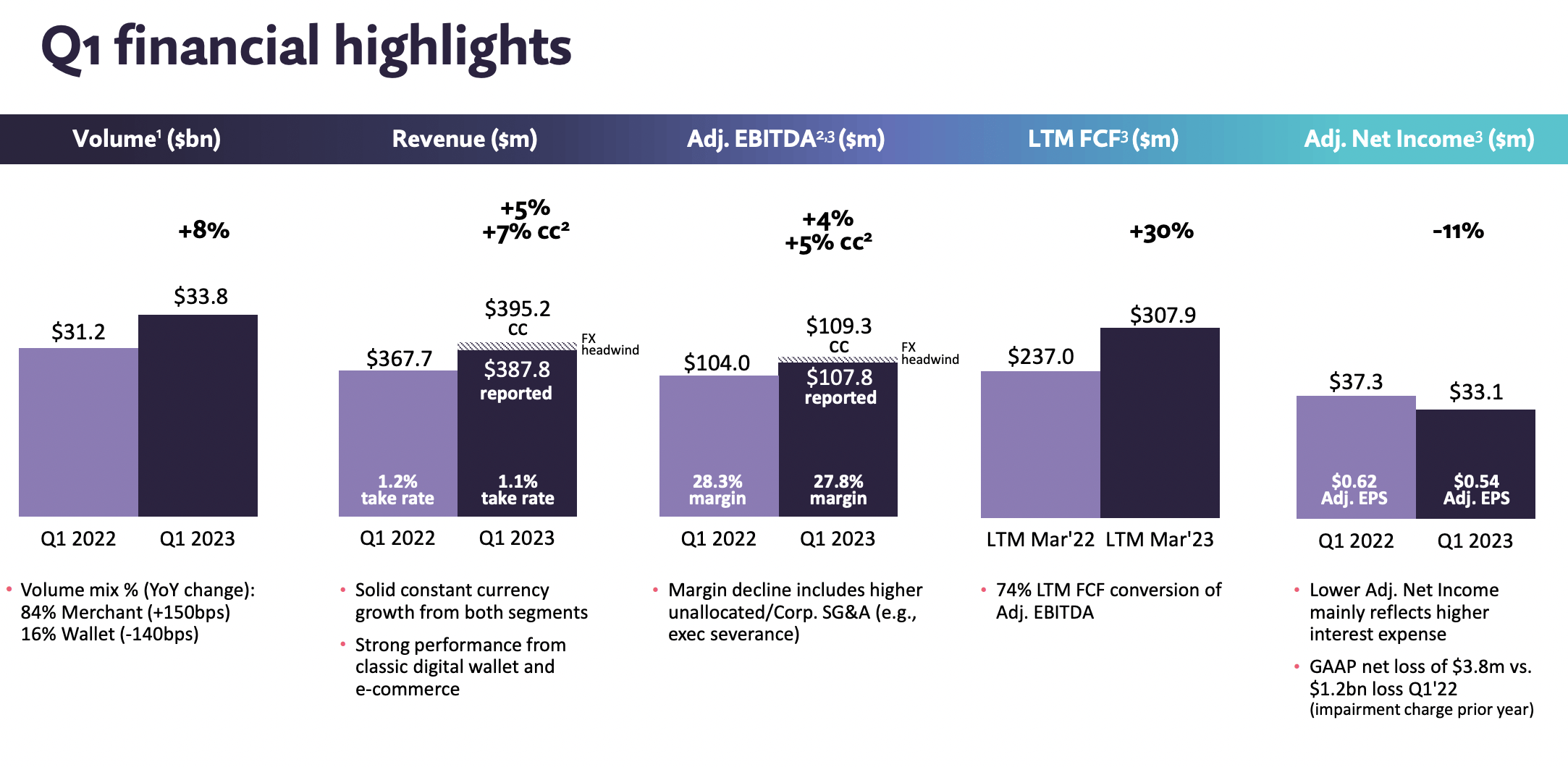

Paysafe recently reported fiscal 2023 first-quarter earnings which saw revenue come in at $387.8 million , a 5.5% increase over the year-ago comp and a beat by $10.2 million on consensus estimates. Growth was 7% on a constant currency basis and was boosted by total payment volume that grew by 8% over its year-ago quarter to $33.8 billion. This was also a sequential growth of 2.1% over the fourth quarter. Digital Wallets saw revenue increase by 6% year-over-year on a constant currency basis.

{kind=link}

This was a broadly normal quarter with adjusted EBITDA up around 4% year-over-year to $107.8 million . Adjusted net income at $33.1 million, declined 11% over its year-ago comp. This is a non-GAAP measure that excludes certain non-operational and non-cash items including impairment expense on goodwill and intangible assets. Bears would right to flag that Paysafe's cash flow from operations during the first quarter was negative at $119 million , a marked deterioration versus an inflow of $503.8 million in the year-ago comp. However, this difference was caused by the timing of the settlement of funds payable and amounts due to customers.

Is The Stock Market Overreacting?

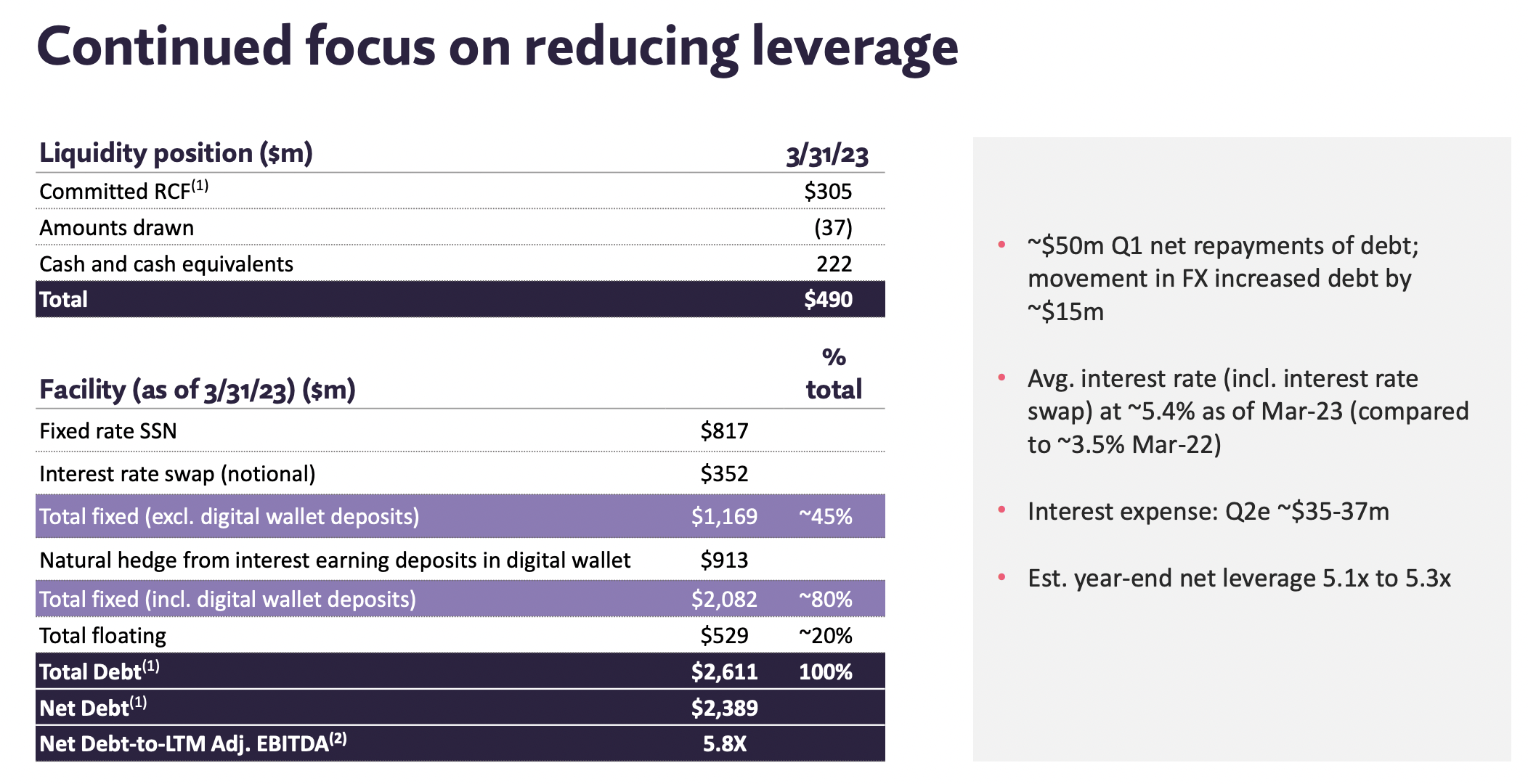

Paysafe's debt balance continues to form the core headwind to its performance. Total debt as of the end of the first quarter stood at $2.6 billion, roughly unchanged sequentially versus the fourth quarter but with the company making $50 million in net repayments of debt. Cash and cash equivalents as of the end of the quarter stood at $222 million, down from $260 million in the prior fourth quarter.

{kind=link}

Interest expense for the first quarter came in at $37.5 million, down from $55.8 million in the prior fourth quarter but a jump of 44.3% year-over-year. This was as the company's average interest rate jumped 190 basis points to 5.4%. Critically, from a profitability perspective, the first quarter earnings were lackluster. Revenue growth was of course welcomed by bulls but the overall health of the business model is less obvious to deduce due to the use of non-GAAP figures, the mismatch between cashflows year-over-year, and the large debt burden.

Whilst Paysafe's current sales multiple is a product of a number of abnormal macroeconomic factors from a Fed funds rate at its highest level since 2008 to a regional banking crisis that caused a broad stock market selloff, its core profitability as measured by GAAP is poor. That its total debt amounts to 384% of its market cap has not helped its investment case. Paysafe will likely continue to trade sideways for much of 2023 with this trend only likely to reverse from 2024 once the Fed starts to cut rates. I'm not a fan of the company here but the current low valuation against a still-growing business makes it hard to rate this as a sell.

For further details see:

Paysafe: Has The Selloff Gone Too Far?