PSFE - Paysafe: Moderate Risk But Rebound Is In Sight

2023-05-24 12:14:58 ET

Summary

- Despite challenges, Paysafe is well-positioned for a rebound in FY 2023.

- Merchant solutions and US SMB growth provide potential catalysts, but caution needed due to high debt level and forex and interest rate risks.

- Paysafe is trading at an attractive discount to my modelled target price, presenting a buy opportunity.

Founded in 1996, Paysafe (PSFE) is a global payment platform. Through its well-known services, Skrill and Neteller, it enables individuals to do secure money transfers and online purchases through various payment methods. It also provides PCI-compliant payment processing tools for merchants across different sizes. Paysafe has processed transactions across different verticals, such as online betting, e-commerce, gaming, and financial services.

It went public on NYSE in 2021 and since then, shares performance has been underwhelming. Since the middle of last year, the stock has lost almost a third of its value, and YTD, is down by +24% and trading at ~$11 per share. Though Paysafe has been a relatively mature and cash-rich business, top-line growth has been stagnant while earnings have been in the negatives as the business was facing various macro headwinds.

There seems to be a potential rebound in FY 2023, especially as Paysafe achieved strong Q1 results and guided to a 6% - 7% YoY growth for the full year, the best outlook since IPO. My model suggests that Paysafe is currently trading a significant discount to the target price.

In this first coverage, I give Paysafe an overweight rating. I anticipate a few catalysts in play that may deliver outperformance, while also being slightly cautious about the development of several risk factors.

Catalyst

I anticipate some catalysts that may potentially drive outperformance for Paysafe into the next quarter and beyond.

Firstly, with the management’s relatively stronger guidance for FY 2023 with a 6% to 7% YoY growth outlook, the business also seems to anticipate a softened forex headwind. Revenue grew by 5% YoY in Q1, and when excluding the forex headwind, it grew by 7%. This was already a significant improvement from what we see in FY 2022, where the reported and constant currency growth differed more significantly. In FY 2022, Paysafe grew flat (0.61% YoY) on reported revenue, but grew 5% based on the constant currency basis.

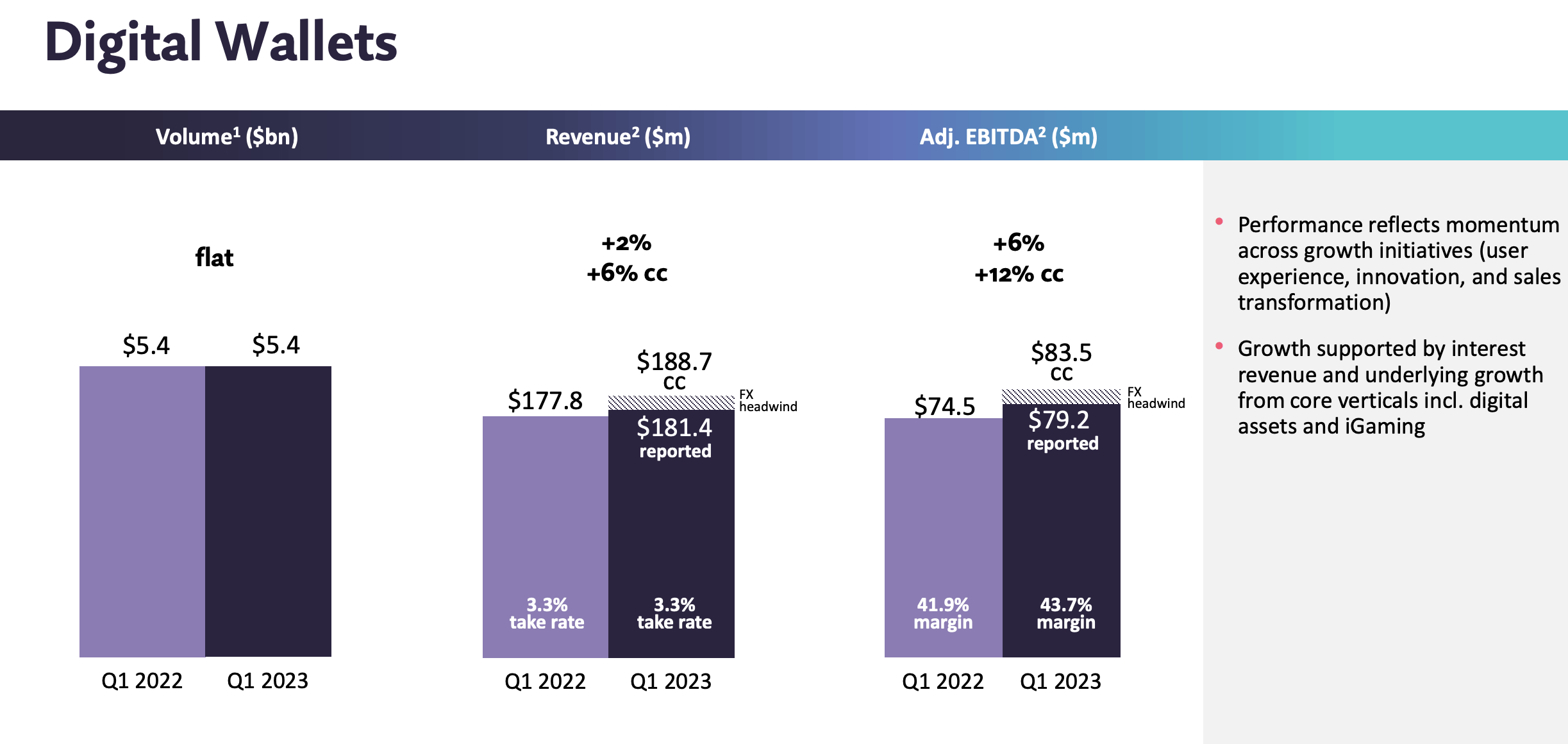

In addition, while Paysafe may potentially see less forex headwind, it may also benefit from another macro catalyst, which is the continuing resilience of the US SMBs and e-commerce sector. Paysafe’s merchant solutions business, which generates ~54% of Paysafe revenue today, already experienced an improvement in the e-commerce vertical in Q4, followed by double-digit growth in Q1. With double-digit growth, the e-commerce vertical grew faster than the overall Q1 revenue growth of 5% YoY / 7% in constant currency.

{kind=link}

The continuing resilience of US e-commerce demonstrates a surprisingly countercyclical trend despite the ongoing macro slowdown. The data published by the Department of Commerce indicates that the US e-commerce industry grew by ~8% YoY in Q1 2023, even as total retail sales only grew by 3.6%. The situation was a bit different in Q1 2022, where we saw e-commerce and retail sales growing at a more similar magnitude. Since PaySafe has also seen an uptrend in e-commerce vertical over the last two quarters, the momentum may last for a bit longer. I have also observed a similar trend in the performance of SMB-focused e-commerce platforms like Squarespace (SQSP), which witnessed significant growth in trial conversions .

Merchant solution business may even strengthen further in Q2 and beyond. In Q1, the management also pointed to the enterprise sales transformation initiative to drive more cross-selling and upselling opportunities across its existing client base as well as new merchant acquisitions. With the success seen in Q1, where Paysafe landed 30 enterprise deals with 20 of them including multiple products, Paysafe has planned to double its sales headcount in FY 2023 .

However, as I will discuss later in the risk section, the initiative could be a little risky. Aside from the additional sales expense incurred when the business is in need to prioritize debt servicing, the initiative will depend largely on Paysafe’s ability to quickly ramp up sales productivity with the new hires. I believe that it is important for investors to closely monitor this catalyst in Q2 to determine whether the positive impact is sustainable.

Risk

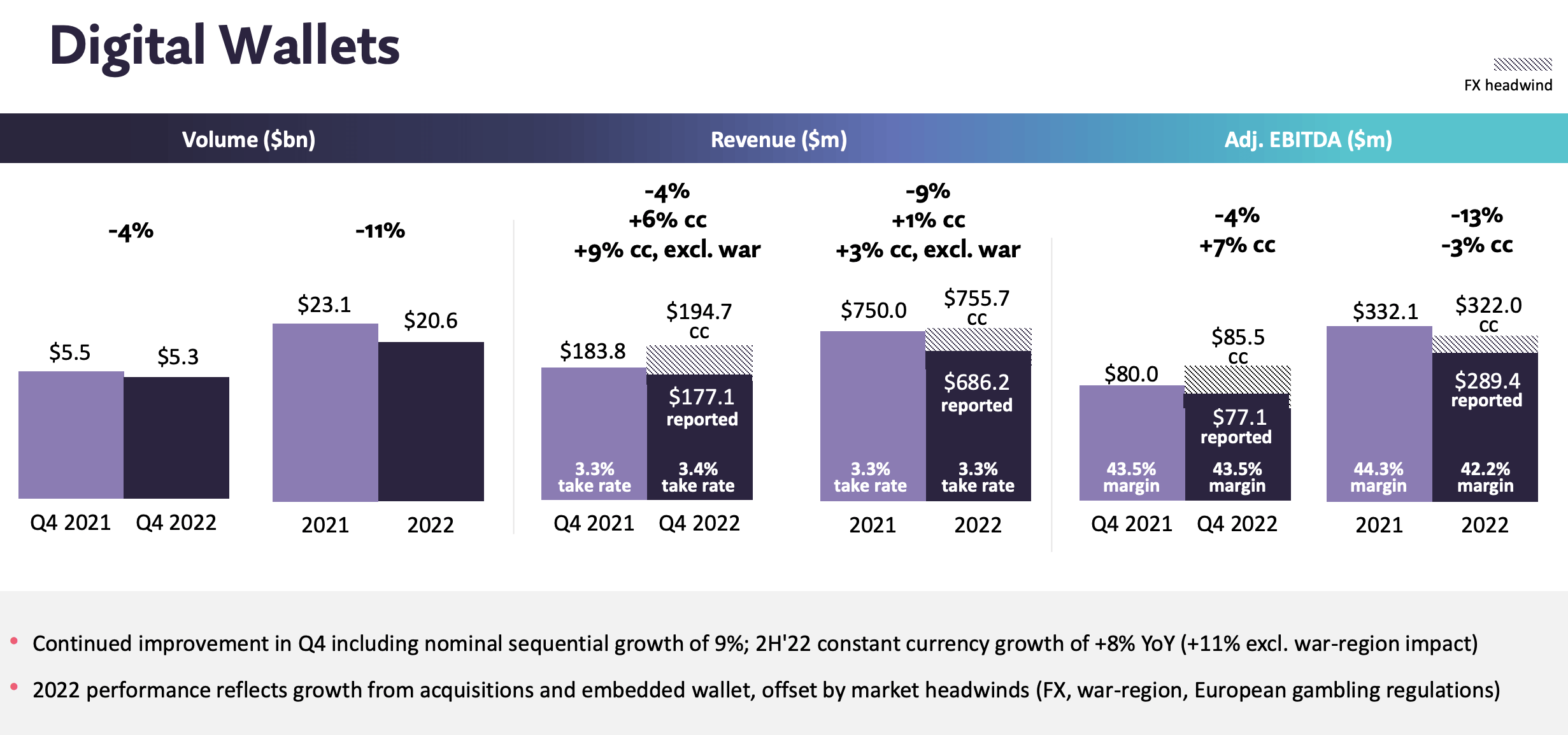

While merchant solution business is primarily US-focused, forex fluctuations have posed difficulties for Paysafe's more global digital wallet business.

{kind=link}

Though Paysafe's operations in Russia and Ukraine only represent ~1% of the total revenue, it appears that the impact towards the digital wallet business was quite severe due to the war in 2022, as highlighted by the management:

Adjusting for the impact of Russia-Ukraine war, constant currency revenue would have increased approximately 9% and 3% for the fourth quarter and the full year, respectively. Adjusted EBITDA in Digital Wallet segment was $77.1 million in the quarter, with margins consistent with prior year at 43.5%. Full year adjusted EBITDA was $289.4 million and margin decreased 210 basis points, reflecting investments and headwinds from Russia-Ukraine and European gambling operations.

{kind=link}

The forex impact seems to have softened in Q1. In Q1, forex impact on the digital wallet was offset by overall growth in the digital assets and iGaming verticals, which the management credited to the momentum across growth initiatives. Given the seemingly structural shift, it is possible that the growth momentum continues in Q2 to again offset the forex headwind. However, given Paysafe’s global activities and the ongoing macro uncertainty, I would still be cautious of the impact of forex fluctuations.

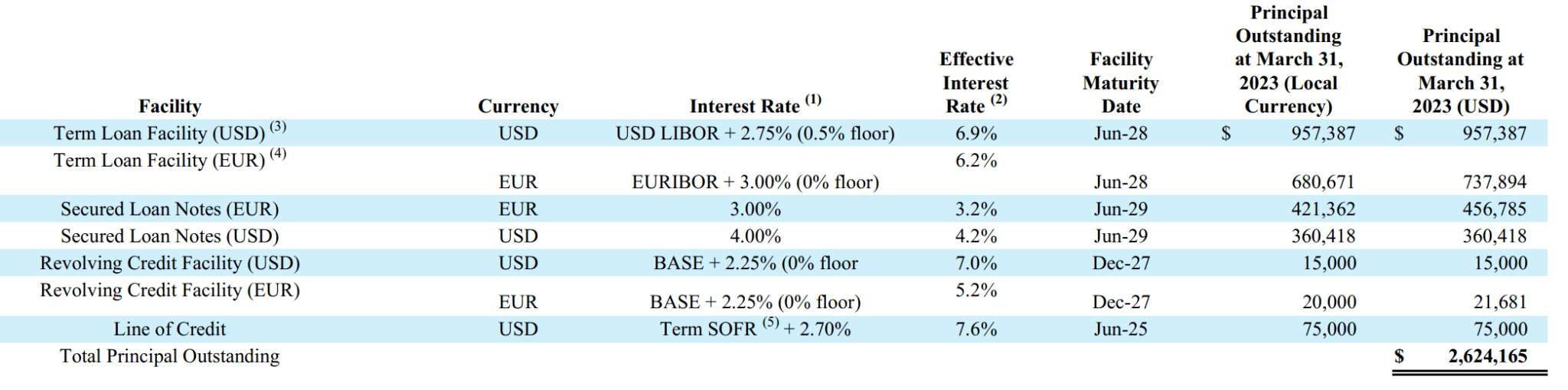

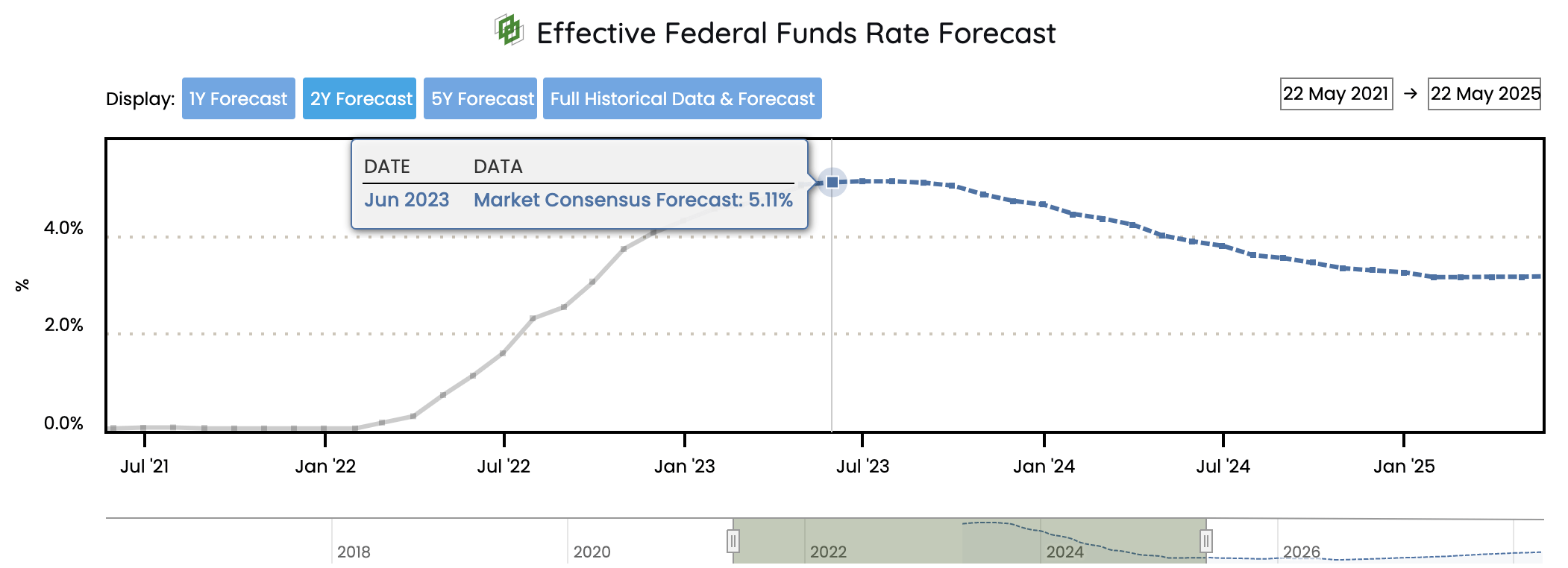

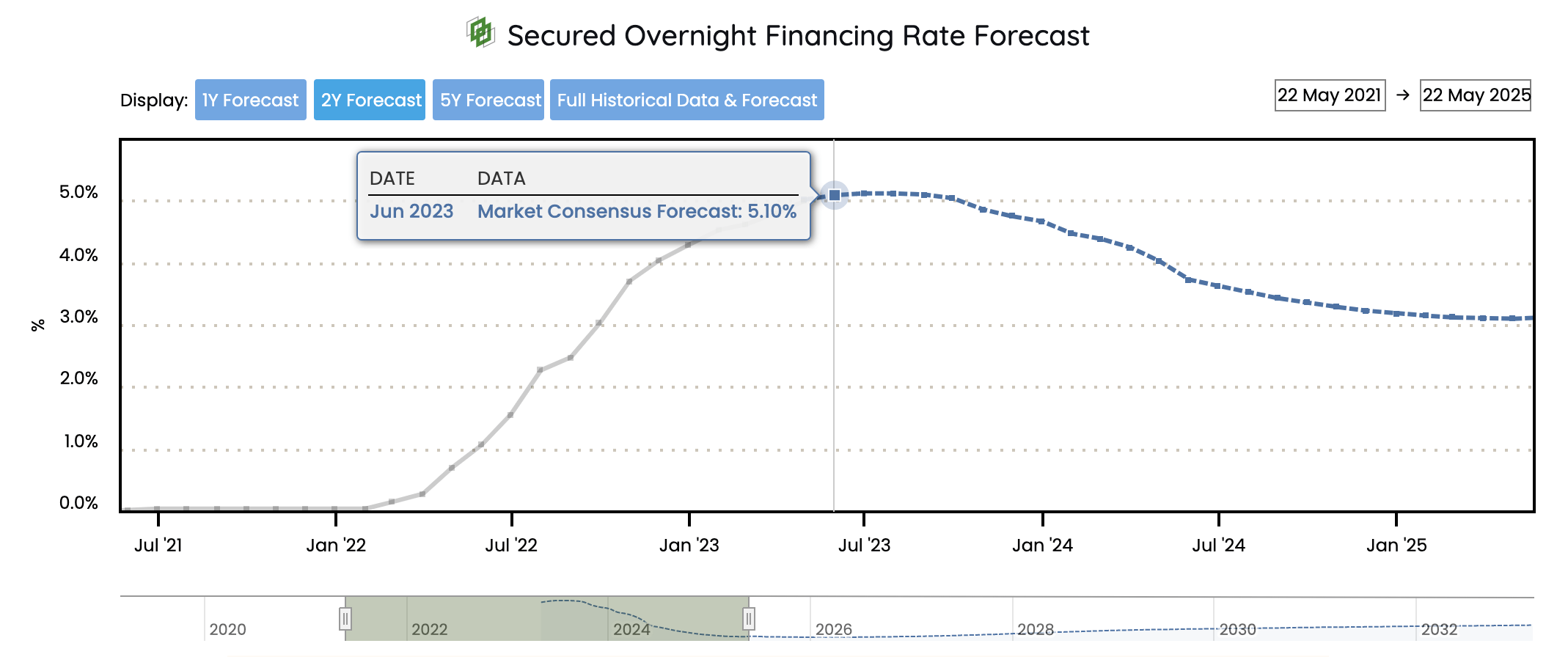

Another key risk factor for Paysafe today would be its high debt level. The net debt-to-LTM adjusted EBITDA ratio of 5.8 times in Q1 indicates a substantial debt burden. Combined with the high-interest rate environment we are in today, the risk level has only become greater for Paysafe.

{kind=link}

The total outstanding debt principal was ~$2.6 billion as of Q1, and the largest portions have floating rates. With rising interest rates, the cost of servicing these debts would increase, impacting the company's goal to maintain profitability and cash flow generation.

econforecasting.com econforecasting.com

{kind=link}

{kind=link}

Based on a recent forecast , it seems that we will still be in a relatively high-interest rate environment for sometime. It is expected that effective borrowing rates may increase slightly in Q2, before reaching the peak and seeing a gradual decline in Q4 onwards, though the outlook will still depend on inflation.

{kind=link}

At such rate, interest expense may still potentially pose a challenge for profitability in Q2. As it stands, Paysafe may continue to incur at least +$37 million of interest expense in Q2. Coming off Q4 2022, interest expense rose by +44% to +$37 million in Q1 to drive a net loss of $3.8 million, even after SG&A expense, one of the top two key operating cost items, already managed to decline by 1.7%.

Meanwhile, there is a possibility of increased SG&A expenses as the company plans to double its headcount to drive enterprise sales efforts in FY 2023. While the management expresses confidence in achieving enough sales growth to counterbalance the pressure on sales and marketing, execution risk remains since Paysafe has a relatively new executive team.

The new CEO and the digital wallet product leader joined in May 2022, while the Chief Revenue Officer / CRO, who is responsible for the sales growth, joined later in July 2022. The effectiveness of this new team in executing strategic decisions and overcoming industry challenges is yet to be fully observed.

Valuation / Pricing

My target price for Paysafe is driven by the following assumptions for the bull vs bear scenarios of the FY 2023 projection:

- Bull scenario (70% probability) assumptions:

- Paysafe to see a 7% growth at the end of FY 2023, in line with the company's guidance as of Q1 .

- The e-commerce and US SMB trends continue to drive the growth of the merchant solutions business. Paysafe’s success with its enterprise sales transformation will not only benefit the merchant solutions but also the digital wallet business, given the cross-selling strategy.

- Borrowing rates to see a slight increase in Q2, and to start declining in Q3. Adjusted EBITDA margin, which accounts for interest expenses, to expand to 29% at year end from 27.8% today.

- Paysafe to have a Net-Debt-to-adjusted EBITDA ratio of 5.1x, in line with the company's high-end projection in Q1

- Bear scenario (30% probability) assumptions:

- Paysafe to see a 6% growth rate at the end of FY 2023, in line with the company's low-end guidance in Q1.

- Paysafe to face some sales capacity challenges in its sales transformation initiatives.

- Borrowing rates to see a slight increase in Q2, but then will stay flat throughout the rest of the year. adjusted EBITDA margin, which accounts for interest expenses, to drop slightly to 27% at year end from 27.8% today.

- Paysafe to have a Net-Debt-to-adjusted EBITDA ratio of 5.3x, in line with the company's low-end projection in Q1

I assign Paysafe an EV/adjusted EBITDA of 7.3x across both scenarios. I think it is a fair figure, considering that it is based on the latest FY outlook in 2022, where YoY growth was flat with a relatively similar level of adjusted EBITDA margin to that of the bear scenario. In addition, I expect Paysafe to see an adjusted EBITDA margin expansion under the bull scenario.

{kind=link}

Consolidating all the information above into my model, I arrived at an FY 2023 weighted target price of +$16 per share. Discounting that target price with a 20% discount rate, I reached a Present Value/PV weighted target price of +$13 per share. The 20% discount rate represents the expected annual return for holding Paysafe. I think that it is a fair figure, considering that Paysafe still presents a bit of risk despite its size.

In summary, +$13 per share is the highest price point at which investors can purchase the stock to realize a projected 20% annual return should my FY 2023 target price of +$16 be achieved. At ~$11.6 per share today, the stock trades at a ~10% discount to my target price, indicating that it is undervalued.

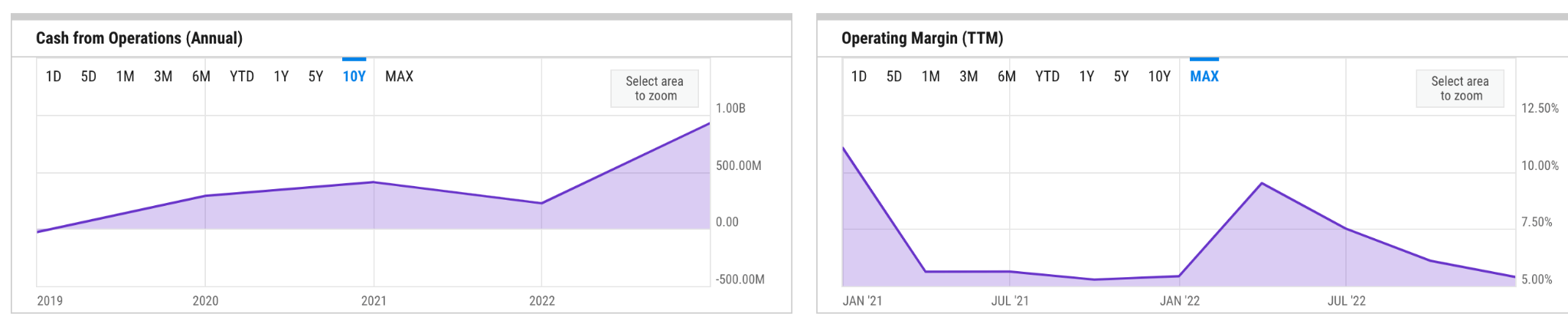

There appears to be an interesting buying opportunity - even under a relatively conservative bull scenario, the stock still appears undervalued. As a side note, I would highlight the fact that Paysafe remains a relatively cash-rich business today.

YChart - OCF and operating margin

{kind=link}

Though operating margin has been on a downtrend in recent times, OCF has seen a significant improvement. However, I foresee a potential downside risk to the shares price if the risk factors I highlighted earlier intensify, putting noticeable pressure on both OCF and profitabilities.

Conclusion

Paysafe, despite being a relatively mature and cash-rich business, has faced stagnant top-line growth and negative earnings due to macroeconomic challenges. However, there are indications of a potential rebound in FY 2023. The company delivered strong Q1 results and guided a 6% - 7% year-on-year growth, presenting the most positive outlook since its IPO.

Several catalysts may deliver outperformance. One of those is the continuing strength in merchant solutions, driven by the e-commerce and SMB growth in the US market. However, downside risk remains. Investors would need to be cautious of the impact that forex and interest rate have on Paysafe’s ability to service its high debt level.

Based on my analysis, Paysafe appears to be trading at a discount compared to the target price, presenting a buying opportunity. As such, in my initial coverage, I assign an overweight rating to Paysafe.

For further details see:

Paysafe: Moderate Risk, But Rebound Is In Sight