BIZD - PBDC: 'Keeping It Simple' With Our BDC Investments

2024-01-06 06:04:26 ET

Summary

- BDCs are one of our favorite vehicles for investing in the credit asset class.

- But there are so many good ones to choose from; takes a lot of monitoring and due diligence.

- Glad to see the still relatively new, actively-managed Putnam BDC ETF doing well; beating the much larger ETF BIZD, which is more or an index approach.

- I like them both, and expect to utilize both of them in an effort to simplify and streamline my BDC investing.

Keeping It Simple..........With BDCs

One of our favorite asset classes over the past year or so has been, and continues to be, credit . Lots of reasons for this, as discussed here and also here.

Most investors are taught to think of two primary asset classes: stocks (i.e. equities) and bonds (or actually, "fixed income", which includes more than just bonds.)

"Fixed income" means that the amount an investor receives at maturity is, well, "fixed." No surprises there. That differentiates it from equity, where your return is essentially unlimited, at least in theory. But fixed income can mean a lot of different things: loans, bonds, preferred stock, etc.

What mostly differentiates various types of fixed income is what sort of risk you are taking (interest rate risk, credit risk, etc.) and how much you get paid to take that risk.

Many of the best known, mainstream "fixed income" assets are long-term bonds issued by the US Treasury and large corporations with high credit ratings (i.e. "investment grade" credit ratings of AAA through BBB). These bonds have no or virtually no credit risk, because the government and highly rated corporations never or hardly ever default. So the only real risk you are taking (and it is a very real risk) when you buy these long-term highly rated bonds is interest rate risk , the risk that you will commit your money for 10-20-30 years at a low rate of interest; and that rates will rise and new bonds from the same issuers will carry higher interest rates, so your "old" bond will be marked down to a lower price, so its yield will match the higher yield that the newer bonds carry. We saw that happen in recent years when the Federal Reserve raised interest rates and existing long-term Treasury and corporate bonds saw their prices drop to reflect the new interest rate levels.

Personally, I'm not interested in making interest rate bets and buying traditional long-term Treasury or corporate bonds.

What I am interested in is making "credit bets," which involve buying bonds and loans issued by companies with lower credit ratings; where (1) there is some real (but predictable, and capable of being modeled) credit risk, (2) interest rate risk is minimal because the interest rate is reset regularly (i.e. "floating" rate loans) or relatively short term (high yield bonds, typically 5 years or so), and (3) interest rates are considerably higher than Treasury and highly rated corporate bonds, to compensate investors for the higher credit risk.

Business Development Companies ("BDCs") have been one of my favorite vehicles for investing in credit, and we own 8 of them in our Inside the Income Factory® "Core" model portfolio, and I own a number of additional ones in my personal portfolio. In addition to the ones we own, some members own others, and we see frequent articles on Seeking Alpha about various BDCs.

What I like about BDCs in general is that most of them are essentially mini-banks, that specialize in making secured, senior loans at floating rates to established middle market companies. Many of them have first-class parent organizations with good reputations in the corporate credit arena, including: Ares, Apollo, Carlyle, Goldman Sachs, Barings/Mass Mutual, KKR, Blackstone, Oaktree, Blue Owl, Bain Capital, BlackRock, etc. Many have close relationships to private equity firms, who are both (1) a source of client contact for new business opportunities, and (2) incentivized with their own "skin in the game" to help support client borrowers if and when they encounter financial difficulties.

BDCs have an advantage over banks in that they are much less leveraged; generally less than 2 to 1, as opposed to a typical bank that is leveraged close to 10 to 1. And instead of bank deposits that can walk out the door en masse at any time, as we saw earlier this year when several medium-sized banks suffered "runs," most BDCs fund themselves through bond and note issues, or formal bank lines of credit. So they know exactly when their liabilities come due and can plan ahead how to refinance them.

Lots of Good BDC Choices

The challenge with BDCs is that there are so many of them that it is difficult to do all the due diligence necessary to pick the best ones and/or to limit the choice to a number that provides adequate diversification without holding more than is necessary or convenient. One simplified approach I am considering is utilizing one or another (or both) of the exchange traded funds ("ETFs") that are available to us. We have the VanEck BDC Income ETF ( BIZD ) already in our Core Model (and in my personal account as well). It is essentially an index fund, based on the MVIS®US Business Development Companies Index that tracks the overall performance of publicly traded BDCs. BIZD has a pretty good record ( described here ) and does what it is supposed to, most recently tracking the exceptionally good record of BDCs over the past year while paying a distribution yield of 10.5%.

Given that there is a certain level of mediocrity built into any index strategy, I have also bought a number of individual BDCs (probably too many, 12 in my personal holdings), in an effort to do better than just meet the index average. The downside is having to monitor and manage so many individual BDCs.

So I was pleased when Putnam Management announced the launch of Putnam BDC ETF ( PBDC ) just over a year ago. PBDC is an actively-managed ETF, so it offers the possibility of doing better than merely meeting the BDC industry average performance, which, admittedly has been pretty good lately.

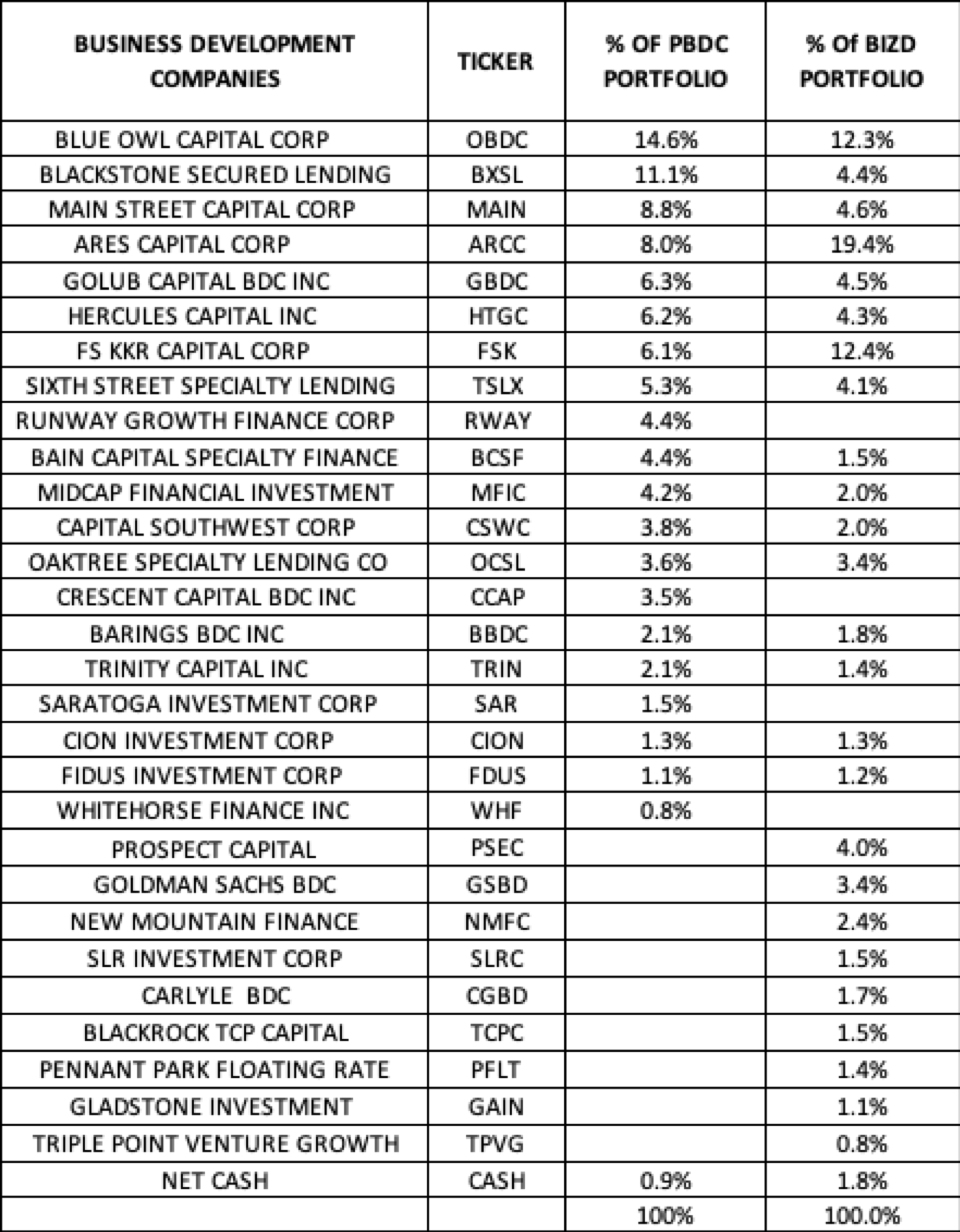

Here is a comparison of the two ETF's current portfolios

{kind=link}

As you can see, there is a fair amount of overlap, although as we might expect, the PBDC portfolio being actively managed, is focused on a somewhat smaller set of holdings. It's that selectivity that we are paying for in an actively managed fund, and judging by the first year's results, it's paying off so far.

{kind=link}

At this point, PBDC is still a new and quite small fund, only about $50 million in assets versus BIZD's $770 million. But the difference in performance, if it continues, will make a big difference over the long run.

Although the fund is young, here's what we know so far:

PBDC's Objective: "To invest in companies offering attractive income to public investors through private market exposure." In other words, Putnam saw that "private credit" is becoming a popular asset class, and has become the first investment firm to offer an actively managed ETF to make private credit available to retail investors. I think this is smart on Putnam's part, and demonstrating in its very first year that it can generate a higher return than an index fund, like BIZD, delivers a very positive message to potential investors.

Total Return History: PBDC's history is short, but its first year's total return of 30% is pretty impressive. (The chart above only shows price performance for both PBDC and BIZD.) On a total return basis (i.e. price performance with distributions added in) PBDC beat BIZD by 30% to 27% for the year (per Fidelity). Obviously we don't expect returns like that to continue but it's a great way to start out. BIZD and S&P's BDC Index have both had annual total returns of about 7% for the past 10 years. Most of that time was a zero-interest rate environment, which is unlikely to repeat. So even if rates do decline somewhat in the years ahead, I think it is reasonable to expect BDCs, overall, to return in the high single-digits. If PBDC, through active professional management, can do somewhat better than that, then investors (myself included) will be happy.

How does PBDC earn its total return? PBDC earns most of its total return through dividends from the BDCs that PBDC owns. The BDCs themselves are like commercial banks, but tend to be safer because they have negotiated lines of credit rather than deposits (i.e. no "runs"), and they are only leveraged about 2 to 1 (or less) rather than 10 to 1 like banks.

Distribution Coverage? During its first reporting period, that ended April 30, 2023, PBDC covered its cash distribution 100% with its Net Investment Income ("NII"). We are currently awaiting the fund's report of its next six months ending in October. I expect the fund, which has been adding assets under management and increasing its quarterly dividend, will show steady or increased profits in its next report.

Coverage of 100% or more by NII is ideal, because it means the distribution can depend on what I call "business as usual income" (regular cash flow from loans to BDC customers), and not be dependent on more "heroic" income like capital gains, which can dry up in periods like we've had in recent years. Even when the price of a company's equity is down and its stockholders are losing money, it still has to continue making its loan payments. So BDCs, just like commercial banks or funds that hold loans and bonds, continue to collect regular interest payments with which they can fund their distributions to their own investors, regardless of what stock or bond markets may be doing.

Fund Management: Putnam Investments, based in Boston, has a long history as a money manager, dating back to 1937. Just this past week, Putnam was acquired by Franklin Templeton, one of the top 10 global asset managers. PBDC's portfolio manager is Michael Petro, who has been at Putnam for 22 years as an analyst and portfolio manager. Besides managing PBDC, he also manages Putnam's Small-Cap Value Fund, and prior to that spent many years as an analyst in the corporate small-cap sector. That seems like the perfect background for evaluating BDCs, whose primary business is lending to small-cap corporates.

Fund Expenses: There have been many comments and questions about PBDC's expenses, which at first glance seem quite high, at 6.8%. But it's important to read the "fine print" which explains how an ETF like PBDC is required to "roll up" the operating expenses of the BDCs it holds and report them with its own expenses, as a separate item. Those are called "acquired fund expenses," but do not represent costs incurred by PBDC.

PBDC's own real management fees are only 0.75%. The other reported expenses are the same operating expenses the BDCs have in carrying out their business and earning the profits and ultimately the dividends that they pay to all of their shareholders, including PBDC. So if you choose to buy the BDCs individually (which is a good alternative strategy) rather than through PBDC, the only fee you save is the 0.75%. The other "acquired fund expenses" have already been incurred back in the BDCs themselves, as their ordinary day-to-day operating costs.

Conclusions: BDC's have really proven themselves as an asset class over the past year. Seeking Alpha is awash with hundreds of articles about various BDCs, and most of them are good investments. That's the challenge for many of us investors: how to track so many possible investment candidates, choose the ones we want, and then monitor and review them regularly. Whew, it's a lot of work!

PBDC offers us a potential solution. I expect to monitor PBDC carefully and move more of my BDC investments into it over time, if its performance justifies it (as it seems to have done so far). My ultimate goal would be to own fewer individual BDC stocks and utilize PBDC (and BIZD too) more and more for my exposure in this important asset class.

Another way that more active investors could piggy-back on professional management like Putnam in the BDC realm, would be to monitor PBDC and use its BDC stock selections as "candidates" for our own due diligence, and then buy those we like directly into our own portfolios.

For further details see:

PBDC: 'Keeping It Simple' With Our BDC Investments