PBF - PBF Energy: A Deeply Undervalued Top-Rated Energy Play For 2024 And Beyond

2023-12-13 07:30:43 ET

Summary

- Energy stocks have underperformed the S&P 500 this year due to investor bets on lower inflation and rate cuts.

- PBF Energy, a major independent petroleum refiner, is an under-the-radar gem with strong fundamentals and an attractive valuation.

- PBF has a diverse product range, strategic refinery locations, and promising growth potential, along with initiatives in renewable diesel and hydrogen production.

Introduction

In my recently released 2024 outlook , I highlighted a number of areas that I expect to do well in 2024 (and beyond). One of these sectors is energy.

I'm buying energy companies, which I expect to protect me against sticky inflation. I also believe that in the event of improving economic growth, we could see a rapid oil price uptrend to triple digits in dollars. I like energy companies with low breakeven prices, healthy balance sheets, and a willingness to distribute most of their free cash flow to shareholders.

Year-to-date, energy stocks have performed poorly, underperforming the S&P 500 by more than 25 points. Even worse, in recent months, we have witnessed a divergence between the two, caused by investors betting on much lower inflation and aggressive rate cuts in 2024.

In such a situation, investors want to own growth stocks instead of energy and related value investments.

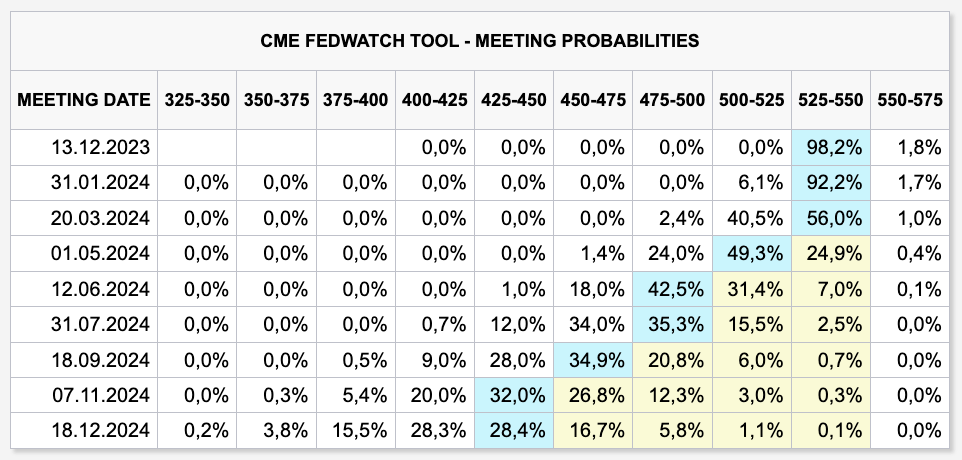

The problem is that investors have gone completely overboard, expecting no less than four rate cuts in 2024.

{kind=link}

Unfortunately, the Fed has never regularly cut rates outside of a recession.

It usually cuts rates more rapidly once economic conditions are so poor that it is forced to give up on tightening.

So, on top of the high likelihood that the market may have to price in more inflation, I believe that a recession isn't unlikely, especially because I expect the Fed to overtighten.

To use another quote from my 2024 outlook:

I like beaten-down cyclical stocks. This includes railroads, machinery companies, and certain consumer stocks with proven track records, which I'm buying on weakness. This is based on the aforementioned phenomenon where cyclical stocks price in a recession well before it happens. I'm not going all in, but I'm gradually buying these stocks when the valuation offers a significant margin of safety.

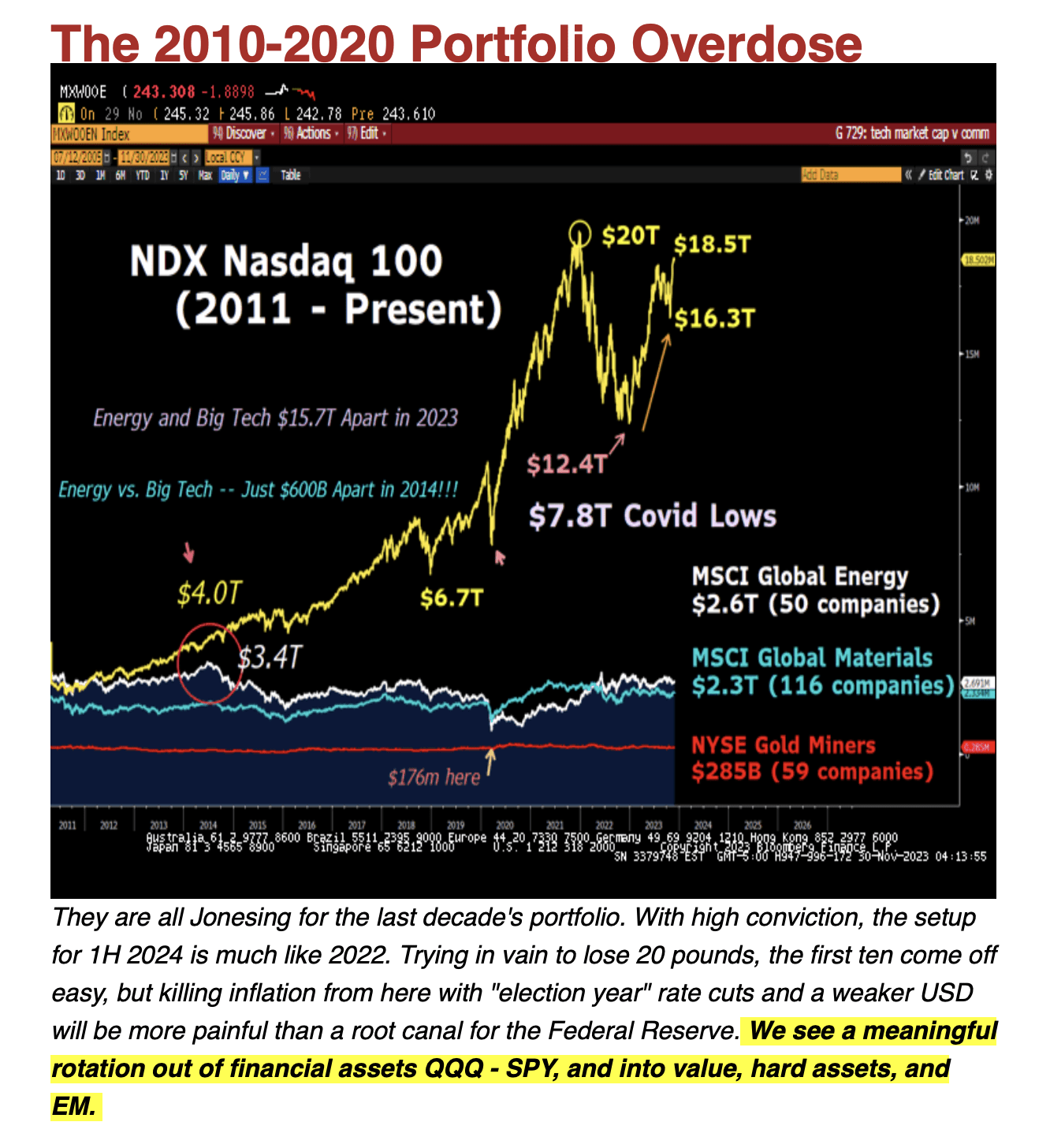

This is what the Bear Traps Report recently wrote when it made the case for a significant rotation into value stocks:

{kind=link}

Hence, in this article, I'll discuss a fascinating energy play. Although the company we're about to discuss does not produce oil and gas, it turns feedstock into valuable refined products.

That company is PBF Energy ( PBF ) , one of America's largest refiners.

However, as it is much smaller than its peers Valero Energy ( VLO ), Marathon Petroleum ( MPC ), and Phillips 66 ( PSX ), it is flying under the radar, which comes with opportunities.

Not only does this company have some of the best Seeking Alpha quant ratings on the market, but it is fully backed by strong fundamentals, an attractive valuation, and a LOT of room for accelerating shareholder distributions.

So, without further ado, let's discuss a stock I have never discussed before!

A Top-Rated Refinery Play

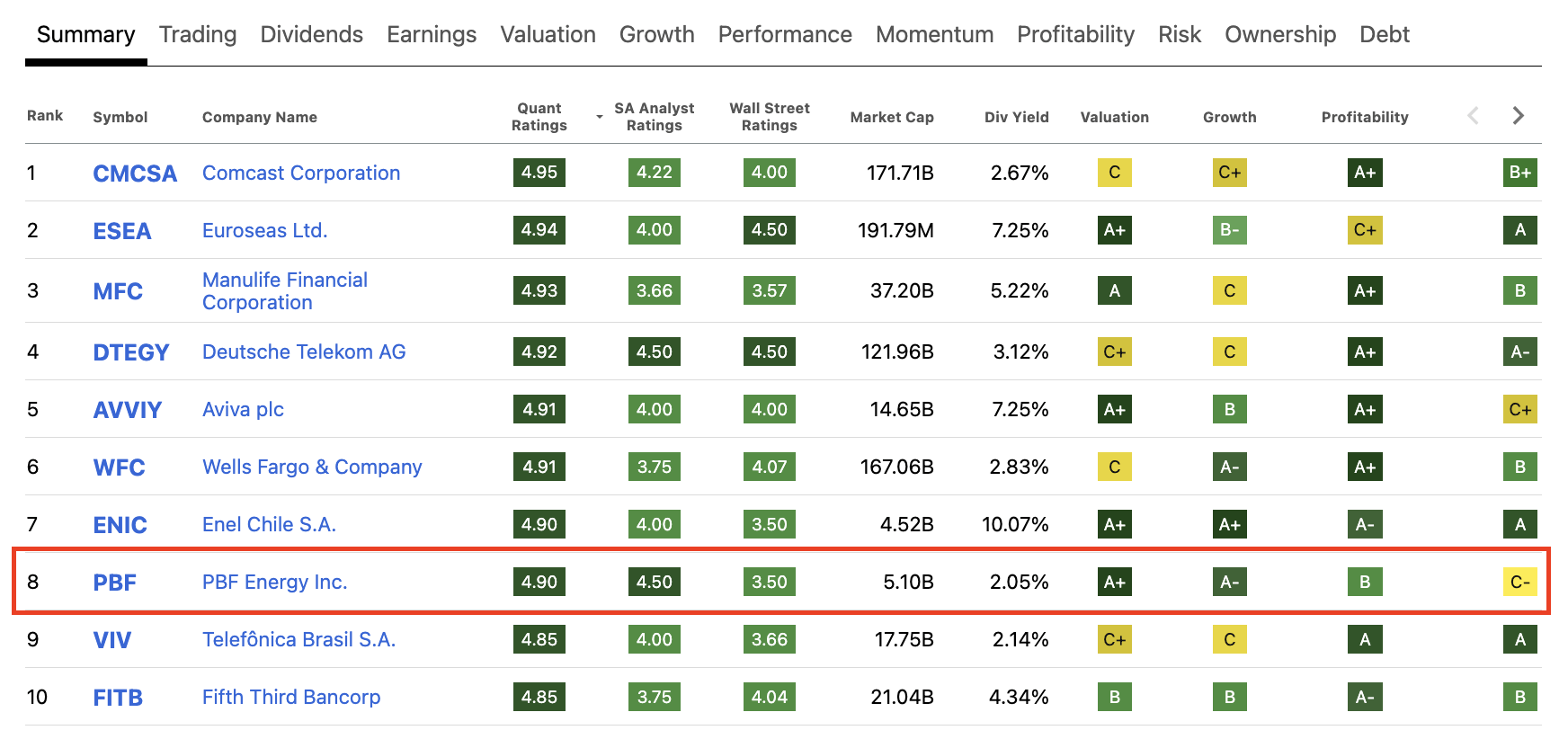

Before I started diving into PBF Energy, I ran a screener to see which dividend stocks the market and fellow Seeking Analysts liked.

I used the following filters:

- Quant rating: Buy to Strong Buy.

- SA analyst rating: Buy to Strong Buy.

- Wall Street analyst rating: Buy to Strong Buy

- Dividend Yield ((TTM)): 2.0% to >8.0%

Here are the results:

{kind=link}

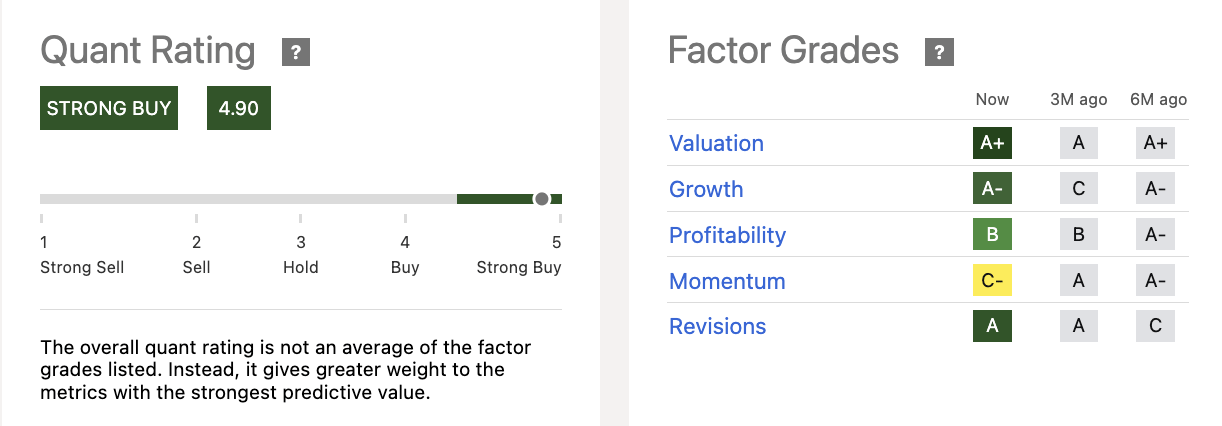

As we can see on the right side of the overview above, the quant rating is backed by strong quant scores. These ratings can also be seen below.

PBF Energy scores very high on its valuation. It has high scores for growth and revisions, a decent profitability score, and a somewhat poor momentum score.

{kind=link}

Nonetheless, the momentum score isn't poor enough to ruin the total score, which is 4.9, indicating Strong Buy.

I agree with the momentum score. Three months ago, it scored an A for momentum. That has changed.

As we can see below, the stock has lost momentum. Over the past three months, shares are down 25%, bringing the year-to-date performance to -1%.

The good news is that momentum doesn't say a lot about the company. If anything, we want to buy great companies after they have lost momentum. Everything else would mean we're chasing hot stocks.

This brings me to the core part of this article.

What's PBF Energy?

With a $4.9 billion market cap, PBF Energy is a major independent petroleum refiner in the United States, with a focus on supplying unbranded transportation fuels, heating oil, petrochemical feedstocks, lubricants, and other petroleum products.

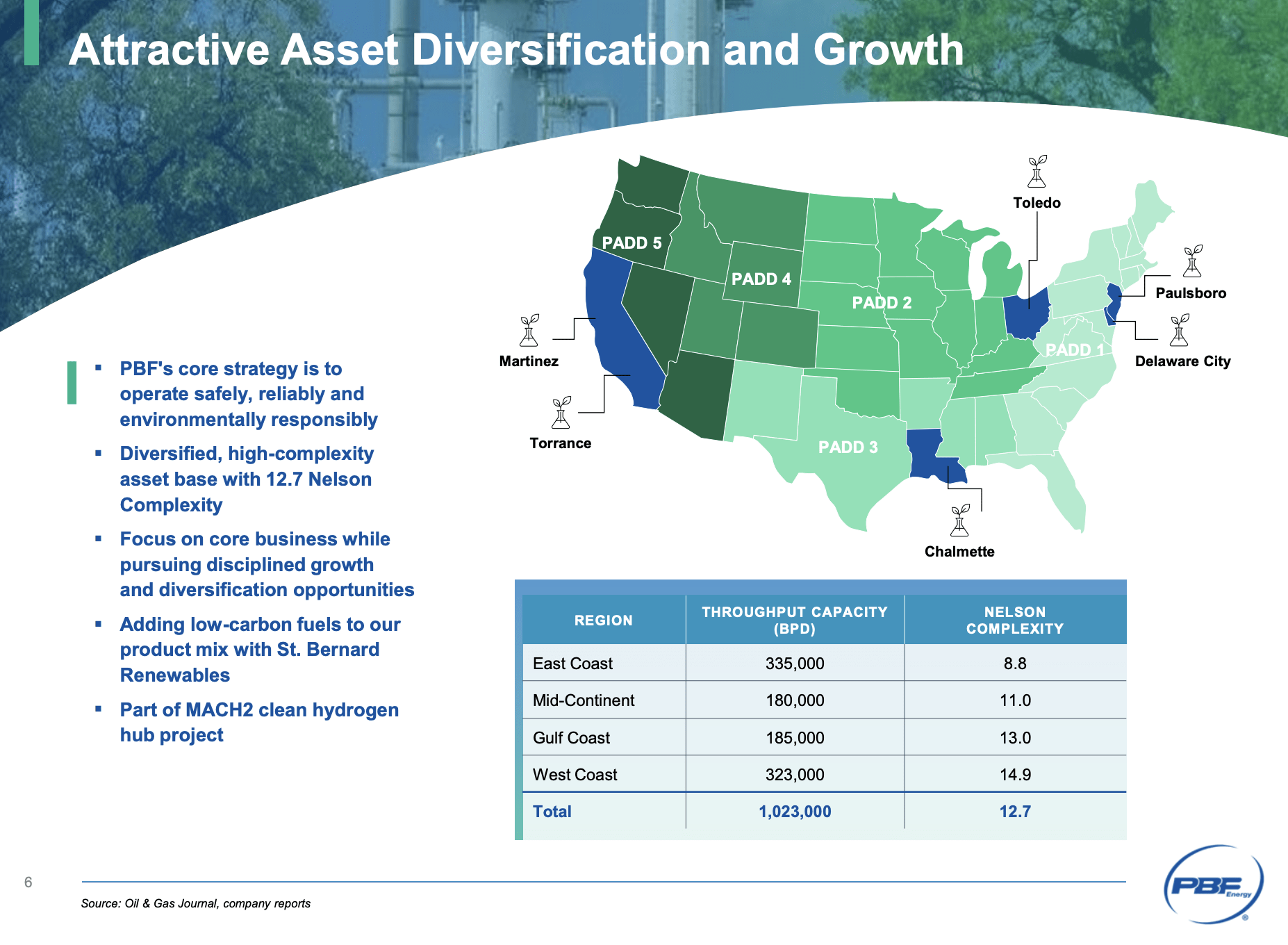

Operating in the Northeast, Midwest, Gulf Coast, West Coast, and international markets, the company owns and manages six domestic oil refineries with a total processing capacity of approximately 1 million barrels per day.

This is slightly more than one-third of the nation's largest pure-play refinery company in the United States, Marathon Petroleum, which processes roughly 2.9 million barrels per day.

{kind=link}

The business operates in two segments: Refining and Logistics, with refining accounting for 99.9% of 2022 revenues.

As we can see above, the company's six refineries are strategically located in Delaware, New Jersey, Ohio, Louisiana, and California.

Each refinery possesses distinctive characteristics, including the Nelson Complexity Index, throughput capacity, and crude processing capabilities.

For example, the Delaware City refinery, located on a 5,000-acre site, is fully integrated and capable of processing a variety of crudes. The Paulsboro refinery, located on the Delaware River, plays a vital role in the East Coast Refining System.

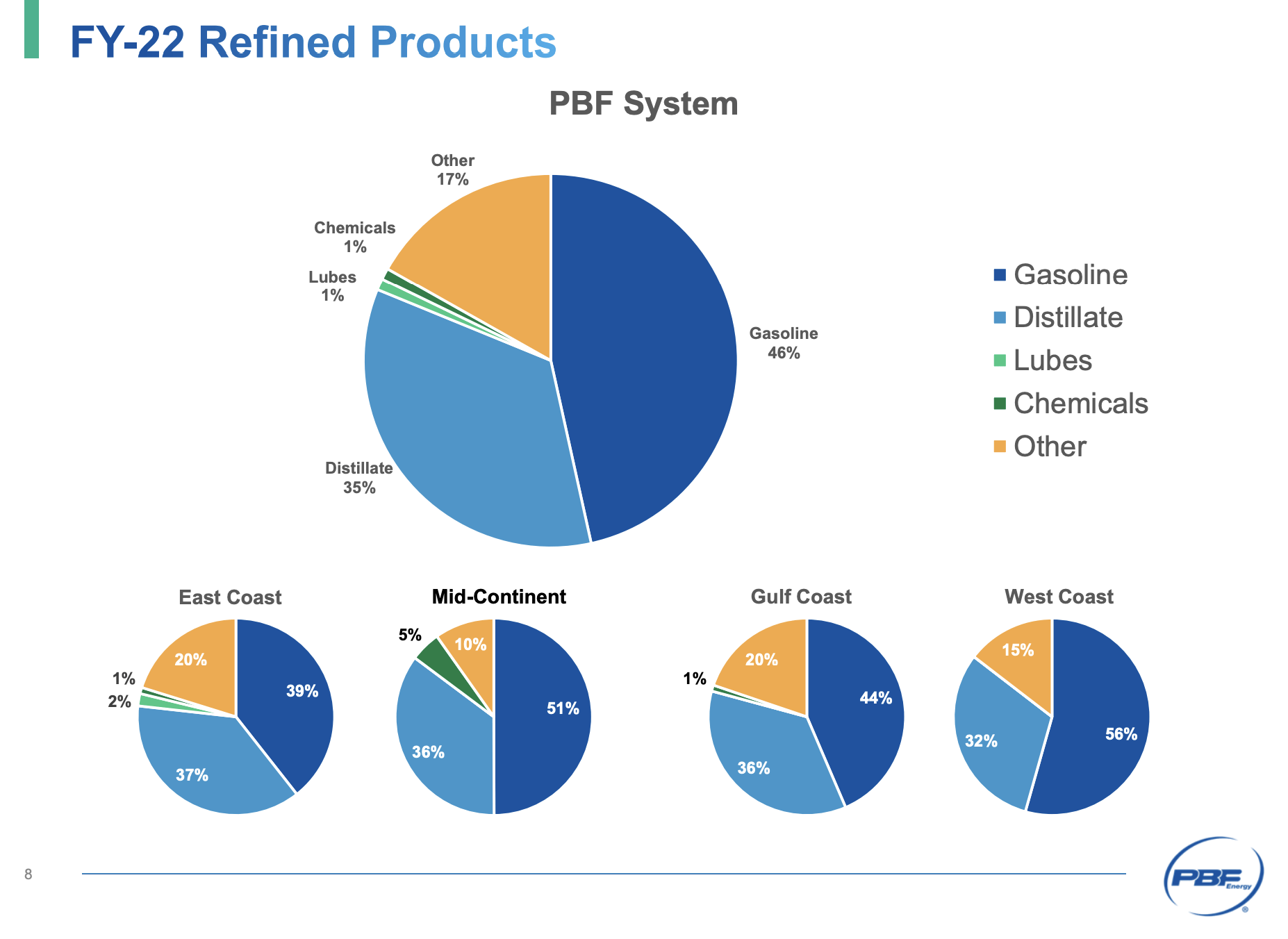

As we can see below, the refineries produce a diverse range of products, including gasoline, ULSD, heating oil, jet fuel, lubricants, petrochemicals, and asphalt.

These products are distributed through pipelines, barges, and truck racks, catering to customers across various regions in the United States, Canada, Mexico, and international markets.

{kind=link}

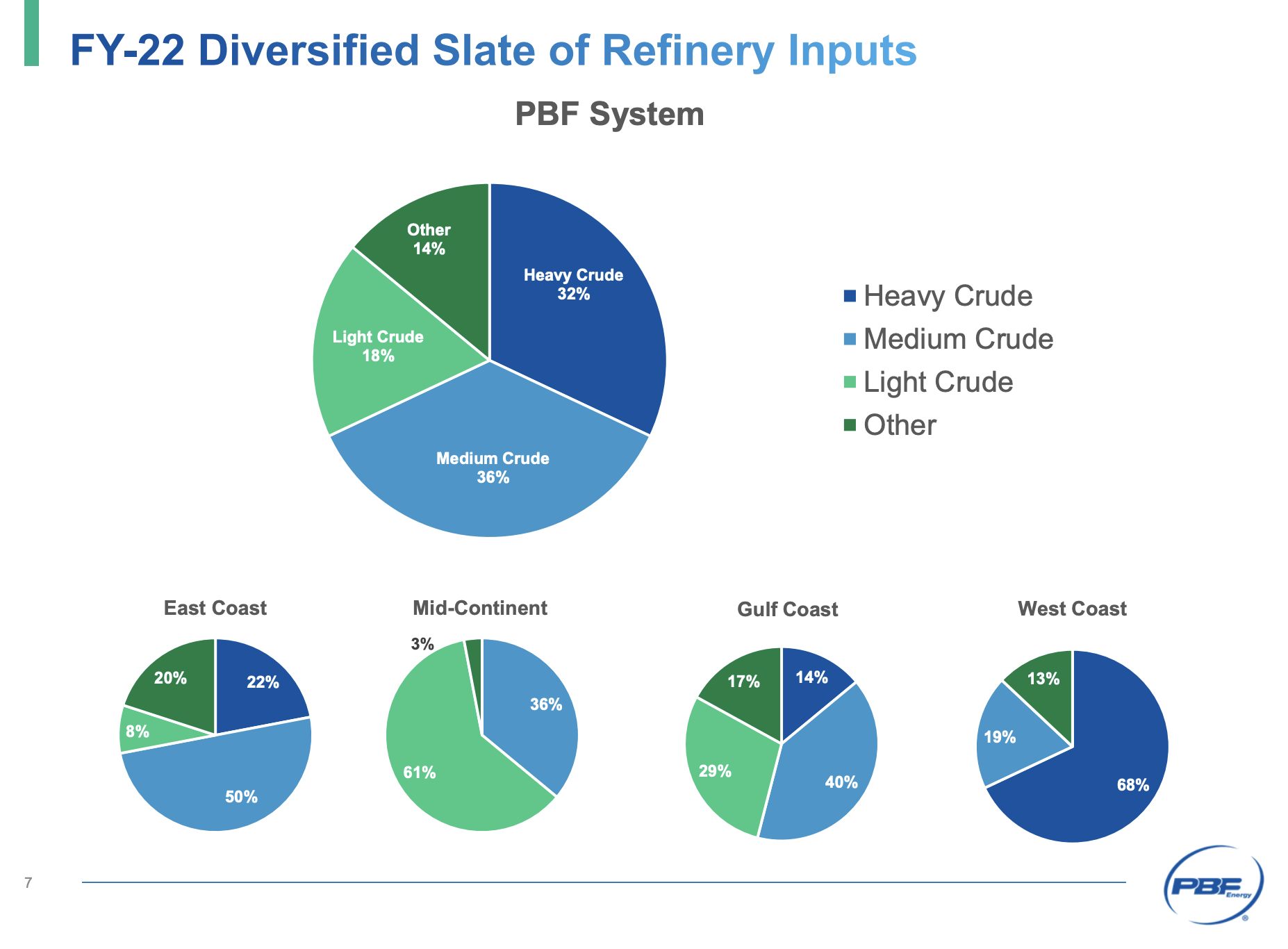

Furthermore, PBF Energy strategically sources crude oil through short-term and spot market agreements, ensuring flexibility in responding to market dynamics.

The company has a significant contract with Saudi Aramco, purchasing up to 100,000 barrels per day of crude oil processed at the Paulsboro refinery.

{kind=link}

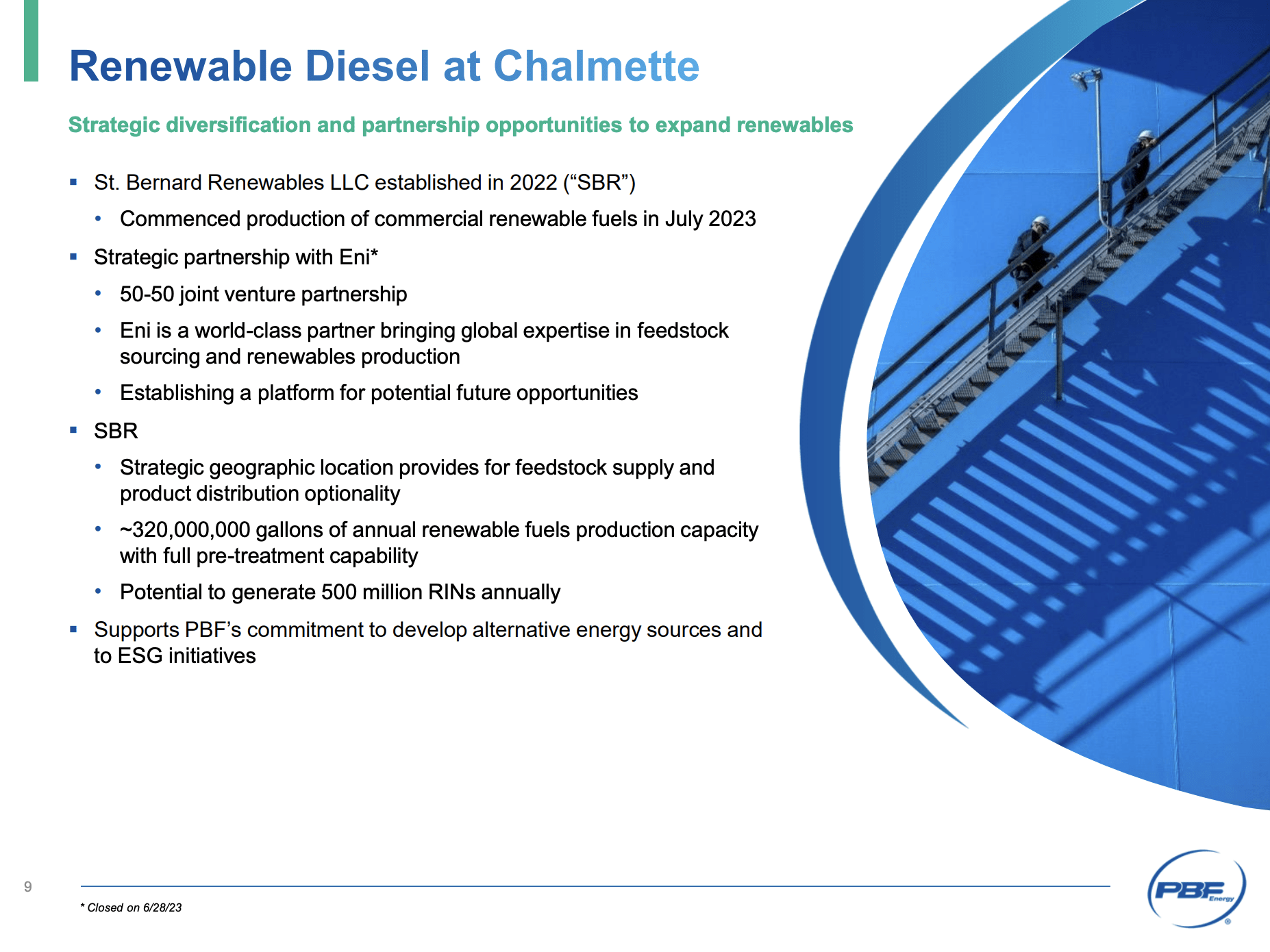

On top of that, PBF Energy is actively progressing on a significant renewable diesel project located at its Chalmette refinery.

This innovative initiative involves incorporating existing idled assets, including a hydrocracker, along with the construction of a new pre-treatment unit.

The goal is to establish a state-of-the-art 20,000 barrels per day renewable diesel production facility.

To get this done, the company has entered into a 50-50 joint venture named St. Bernard Renewables LLC ("SBR") with Eni Sustainable Mobility, a subsidiary of Eni SpA.

Eni will contribute capital and expertise in renewable diesel operations, supply, and marketing, while PBF Energy will continue to manage project execution and serve as the facility's operator upon completion.

{kind=link}

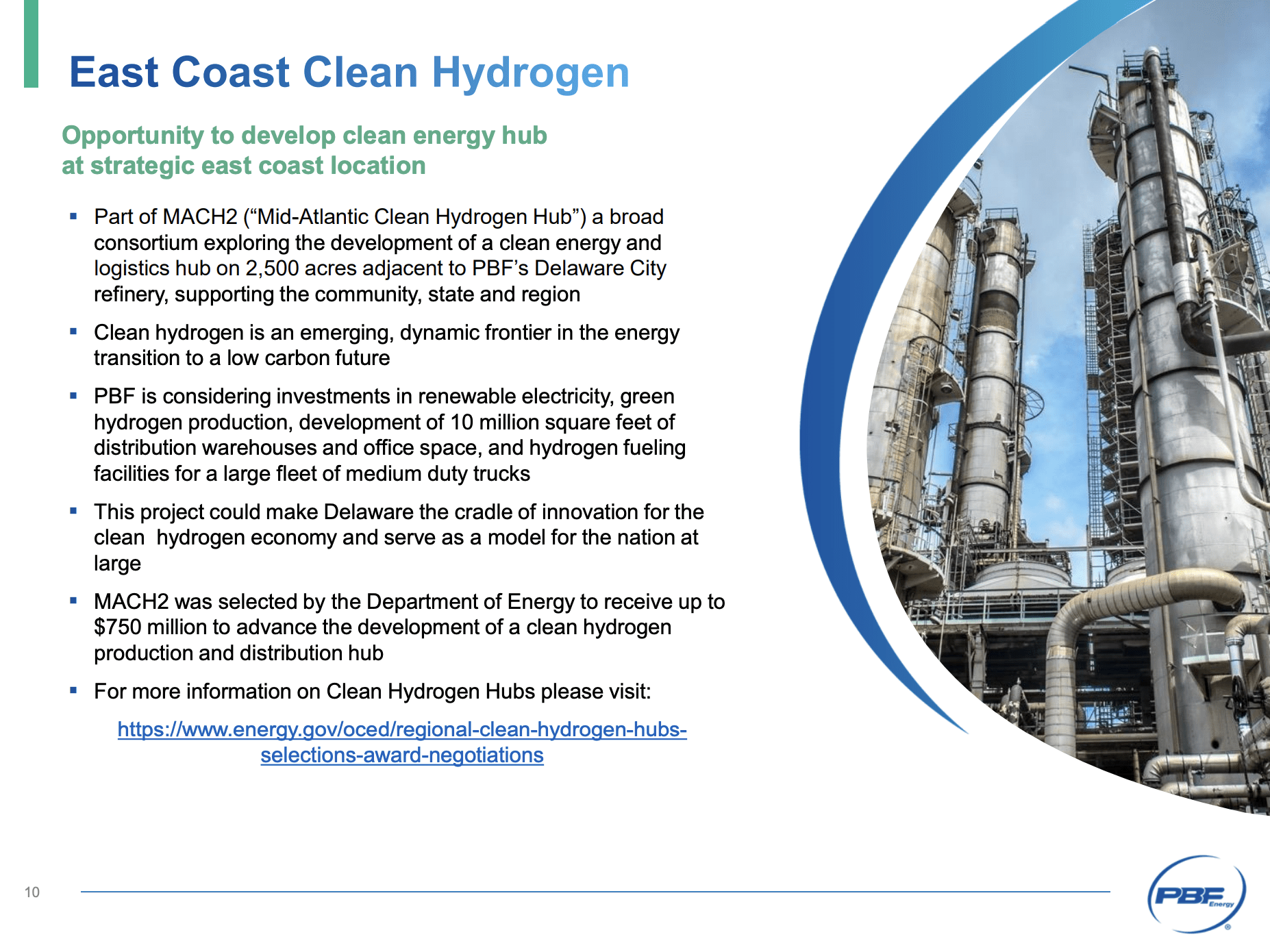

Additionally, PBF is increasingly focused on hydrogen production.

As reported by the Delaware Business Times (emphasis added):

The Delaware City Refinery owned and operated by New Jersey-based PBF Energy will figure prominently into the MACH2 plans. The company aims to create a plant in Delaware City capable of producing upward of 137 megatons of clean hydrogen a day , according to the MACH2 concept proposal.

Initial projections are that 85 tons of clean hydrogen could be produced and used by companies and entities in the mid-Atlantic region in the early stage of development , which can replace an equivalent amount of daily natural gas combustion. It could reach over 600 tons per day once fully scaled up.

Some of that production would likely go to help support the adoption of hydrogen fuel by long-haul truckers, an industry that could benefit from the fast-fueling, long-lasting energy . Air Liquide, a French chemical company that has its U.S. Innovation Center in Glasgow, is exploring the buildout of eight fueling stations along the Interstate 95 corridor that could help create an environment here that currently only exists in California.

{kind=link}

With that said, let's take a closer look at the business and its ability to generate shareholder value.

Where's The Shareholder Value?

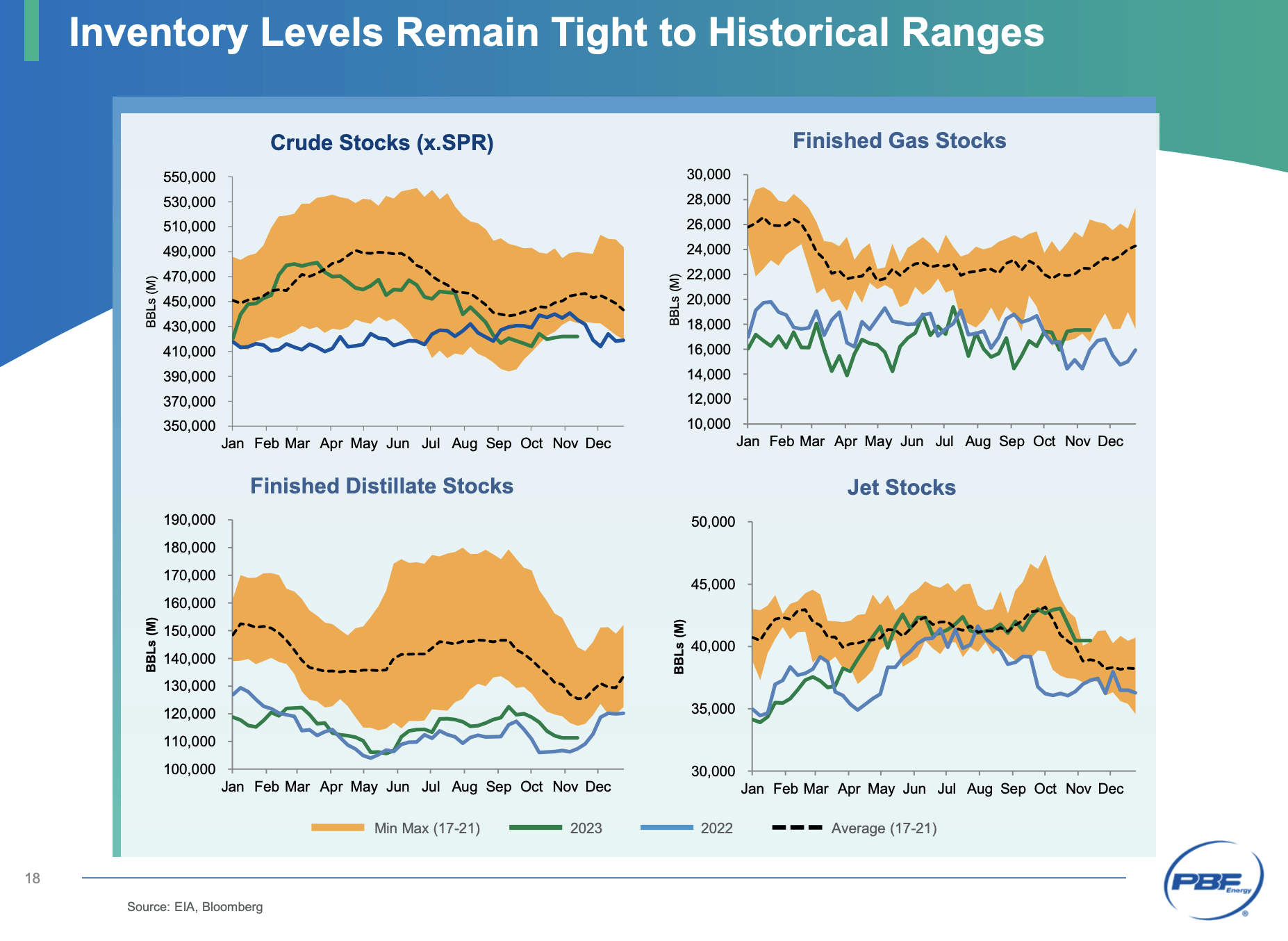

Despite economic weakness, PBF is doing well.

In its third quarter, its refineries ran well with no major planned outages, contributing to a strong performance.

While gasoline cracks decreased in the shoulder season, diesel margins remained robust due to tight inventories.

{kind=link}

Cracks, or crack spreads, are margins for refined products. As the company is buying feedstock to turn this into value-added products, it is dependent on both input and output prices.

However, despite the gasoline price pullback, the company expects prices to stabilize, and compound cracks will likely stay above previous mid-cycle levels.

I agree with this. While we won't see the fantastic numbers we saw last year, I expect refiners to keep benefitting from tight inventories and pricing advantages.

In light of these developments, in the third quarter, the company reported adjusted net income of $6.61 per share and adjusted EBITDA of $1.3 billion.

This includes contributions from the equity interest in SBR and a $100 million benefit from the market decline in the price of renewable energy credits, captured in gross margin.

Net income was down from $7.96 per share in the prior-year quarter.

Cash flow from operations for the quarter was $1.15 billion, excluding working capital changes. Working capital was a $618 million headwind, primarily due to efforts to strengthen and simplify the balance sheet.

This brings me to, you guessed it, the balance sheet.

During the third quarter, the balance sheet was strengthened by reducing gross debt by approximately $170 million. The company issued $500 million in 2030 notes and called the remaining balance of 2025 notes, eliminating near-term debt maturities.

The undrawn ABL facilities were increased to $3.5 billion, with an extended maturity to 2028.

On top of plenty of liquidity, the company is expected to end this year with $460 million in net cash, which means more cash than gross debt. In 2020, the company had more than $3 billion in net debt, which was the result of the pandemic.

In 2019, the company had $1.3 billion in net debt, which was roughly 1.6x EBITDA.

Thanks to a strong balance sheet, the Board approved a $0.05 per share increase in the quarterly dividend to $0.25 per share.

After a tough pandemic period, PBF shares currently yield 2.5%.

Going forward, the company will evaluate potential dividend hikes on an annual basis.

It is also using buybacks to distribute excess free cash.

In the fourth quarter of 2022, PBF announced a $500 million share buyback program, later increased to $1 billion in May .

The company has actively deployed $590 million in cash, repurchasing 14 million shares or 11% of the shares outstanding.

Year-to-date, PBF has bought back roughly 6% of its shares.

Going forward, PBF expects to remain active in buying back shares. The level of buyback activity will be determined by excess cash generation and an evaluation of reinvestment opportunities relative to share buyback economics.

What About PBF Stock's Valuation?

Essentially, this part is a continuation of the prior part.

Looking at the Seeking Alpha quant scores, we see that PBF scores very high on its valuation.

I agree with that (objective) rating.

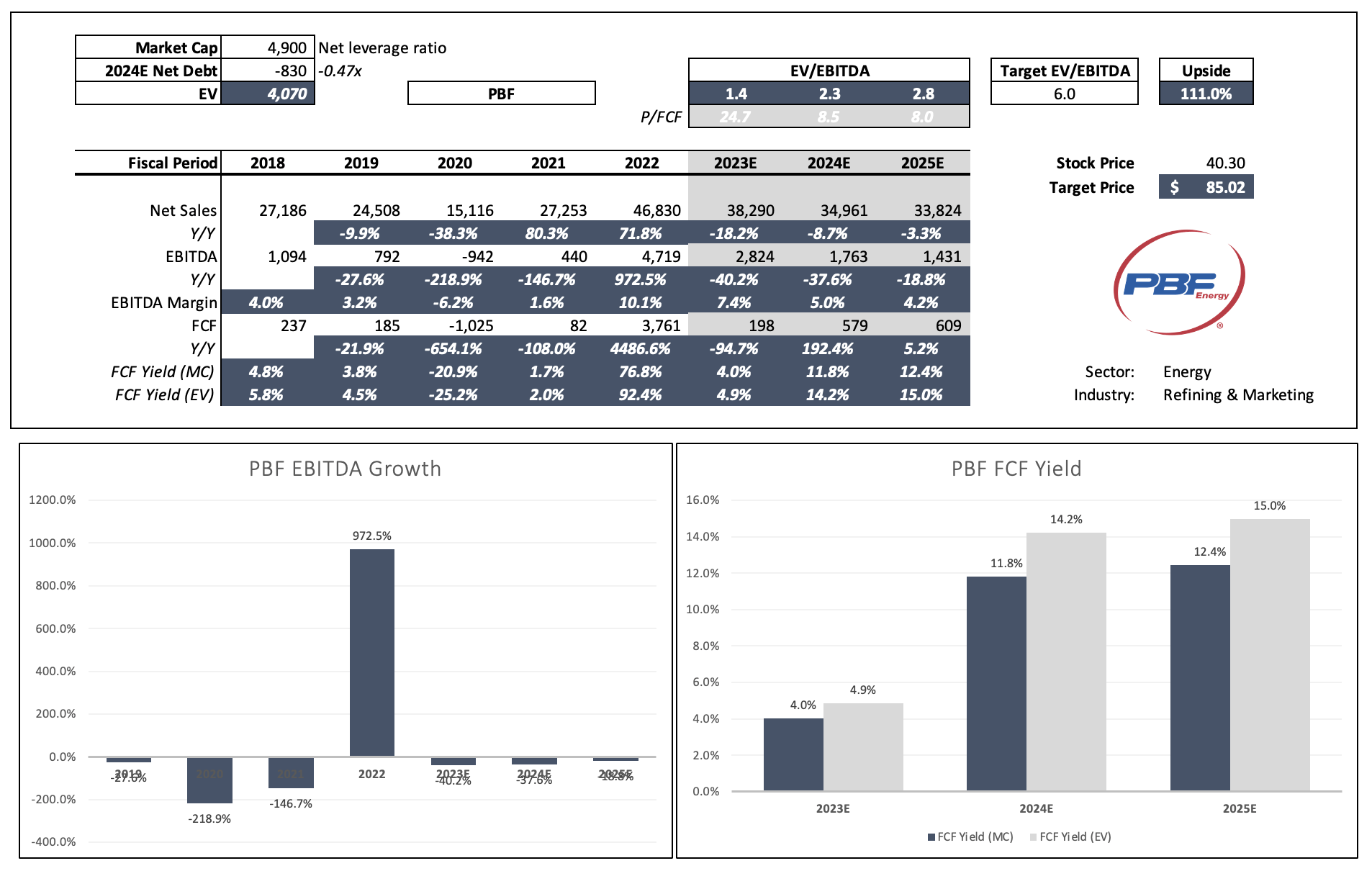

PBF, which currently has a $4.9 billion market cap, has a 2024E enterprise value of roughly $4.1 billion, based on an expected surge in net cash to more than $800 million.

This year, the company is expected to generate $2.8 billion in EBITDA. That number is expected to gradually decline to $1.4 billion in 2025. These expectations are common in its industry, as analysts price in normalization in volumes and prices.

Although I expect the actual numbers to be much stronger than expected, even these numbers are bullish, as the company is expected to generate more than $600 million in free cash flow in 2025.

This implies a free cash flow yield of more than 10%. It could even hit 15% of its enterprise value. This means that there is a lot of room to increase the current dividend and buy back a ton of stock.

Leo Nelissen (Based on analyst estimates)

{kind=link}

It also means that PBF is attractively valued.

Applying a 6x EBITDA multiple indicates a $85 fair stock price target. That's more than 100% above the current price.

We find similar numbers when applying a 9% to 10% free cash flow yield to its free cash flow expectations. This would give the stock a fair market cap of $6.1 and $6.8 billion, respectively. That's between 50% and 70% above the current price.

Although I expect a potential recession to be able to do more damage to PBF's stock price, I am very bullish about its future and believe it is a great investment on weakness.

I put the stock on my watchlist and hope to add a few shares if it drops another 10% to 15%, which would fit my view on the economy.

Given its long-term performance and attractive value, I will give the stock a Strong Buy rating. Nonetheless, please be aware of potential economic risks.

Takeaway

Going into 2024, my focus on energy investments includes PBF Energy, an under-the-radar gem in the refining sector.

Despite recent market fluctuations, PBF stands out with strong fundamentals, an attractive valuation, and promising growth potential.

With a diverse product range and strategic refinery locations, the company navigates market dynamics very efficiently.

Meanwhile, PBF's forward-thinking initiatives, like the renewable diesel project and emphasis on hydrogen production, position it for sustainable success.

Financially robust, PBF boasts a strengthened balance sheet, the potential for massive dividend increases, and an active share buyback program.

As the market reacts to macroeconomic uncertainties, I see PBF as a resilient and promising investment opportunity.

For further details see:

PBF Energy: A Deeply Undervalued Top-Rated Energy Play For 2024 And Beyond