VLO - PBF Energy Could Be A Huge Winner In 2023

Summary

- PBF enters 2023 at just 1.89x 2022 estimated earnings and near tangible book value.

- Despite being up a whopping 176% over the last year, Enterprise Value is roughly flat as PBF used the enormous cash flow to retire debt.

- Crack spreads could stay high this year due to a combination of low product supplies, increased demand, and the Russian product ban.

- Lower natural gas prices, lower interest expense, and the PBFX acquisition should provide a major tailwind to PBF's 2023 results.

- The low valuation and net debt-free position may allow PBF to repurchase a significant amount of shares.

PBF Energy ( PBF ) is a $6.1 billion oil refiner that owns six modern refineries and associated logistics in the United States. Like most refiners, last year's record crack spreads provided an incredible windfall with PBF generating $3.3 billion in operating cash flow in just Q2 and Q3 alone. Upcoming Q4 results could produce another billion in OCF.

Predictably, the share price did well. But I believe the company has just gone from "insanely cheap" to "very cheap" and there is still significant upside ahead.

Valuation

Some investors initial reaction when looking at PBF may be that this is "last year's trade." All the refiners did well last year, and PBF did really well. I'll admit, whenever I see a chart like this, it screams mean reversion coming - avoid to me, too. But I don't think that is the case.

PBF is set to earn roughly $24/share for 2022, on a $44 stock price, for a trailing P/E of 1.89x. Most refiners have done well this year (trailing P/E for Marathon Petroleum ( MPC ) is 5.1x, Phillips 66 ( PSX ) is 5.43x, and Valero ( VLO ) is 5.14x) but nothing is as cheap as PBF.

While other refiners have shifted focus to dividends and buybacks, PBF has used almost all of the cash flow to pay off debt, like the early call of $1.25B in 9.25% Senior Notes in July. Looking at Enterprise Value, rather than just price, tells a different story.

Note that this chart above only captures cash flow through Q3 and doesn't include what is projected to be a very good Q4. With Q4 included, Enterprise Value will be nearly flat after a record year when the company went net debt free!

PBF will also be near tangible book value after Q4 is added in, the only refiner in this set that's close by that measure. The replacement cost of these assets are far higher than their book values. The Cenovus ( CVE ) Superior refinery rebuild cost is approaching $1.2 billion. While brand new and state of the art, this refinery only has 49 Mbbls/day of capacity, less than a third than most of PBF's.

I believe PBF is just too cheap. All refiners will do well if the strong crack spread environment persists, but PBF is the only one that could cash flow 50-75% of its market cap in the next year and materially de-risk in just a few quarters of strong crack spreads.

Comparisons to other refiners - how much of the discount is merited?

PBF looks so cheap it almost seems too good to be true. Why is PBF so cheap compared to other US refiners? I believe there are some valid reasons, but not anywhere enough to justify such a massive discount.

1. Diversification and refinery location

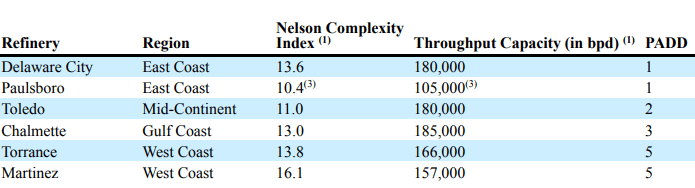

With only six refineries, it's not as large and diverse as some larger refiners. 2/3rds of their refineries are in PADD1 and PADD5 where operating conditions can be challenging.

{kind=link}

Five of the six refineries are coastal, which does not provide the advantages it once did when the US imported a much higher percentage of our crude. In-land refineries like Toledo can take advantage of the discount in Canadian heavy oil; other inland refineries can take advantage of shale oil.

Additionally, with the exception of the two East Coast refineries, PBF's refineries operate independently with little integration with each other.

This could explain some of the value discrepancy with the larger refiners.

2. Complexity

The Nelson Complexity Index is a measure of the sophistication of an oil refinery. Refineries that are higher on the Nelson Complexity Index are able to handle lower quality crude or produce more value-added products, increasing margins.

US based refiners average 11.6 and are typically more complex than Europe (9.3) and Asian (9.8) counterparts. Of these, PBF is among the highest. (Note that Paulsboro is typically a 13.1 on this scale, but based on its current configuration, it scores lower.)

It is open for debate and difficult to quantify how much of an advantage this is for PBF. To be conservative, I simply view this as non-inferiority versus the other major US refineries.

If there is a reason for a discount versus other refiners, it isn't because PBF's refineries lack capability.

3. California

PBF has a 1/3 of its refineries located in California, a locale that is increasingly difficult to do business in and is openly hostile to the oil and gas industry. Governor Gavin Newsom recently proposed legislation to limit oil and gas profits. (Whether this would hold up to legal challenges is highly questionable, but it is certainly not a positive in any case.) MPC, PSX, and VLO all have some California exposure to their operations (between 10-15%) but none to the extent PBF does.

The exposure to California is a double edged sword. While it's difficult to do business there, it's a large market with minimal excess capacity, which leaves it prone to price spikes that can benefit the remaining refiners.

In summary, I do believe there are reasons why PBF should trade at a small discount to the larger peers, but the current discount is far too extreme.

2023 Crack Spreads

Future crack spreads are the gigantic elephant in the room. No one knows what crack spreads will look like over the course of 2023 and beyond, which will determine how much PBF and other refiners earn.

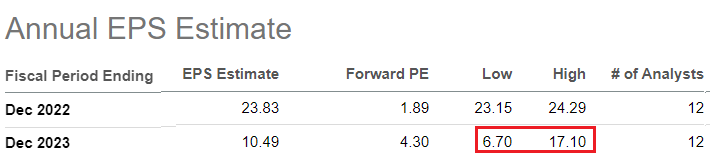

PBF EPS Estimates (SeekingAlpha 1-25-23)

{kind=link}

The spread in 2023 analyst estimates is big enough to drive a truck through (and for whatever analyst has $6.70, I'll take the over. PBF may do that in Q1 alone.)

Last year's record crack spreads were a result of demand rebounding quickly after nearly 4+ mbpd of global refining capacity closed permanently during the pandemic. The Russia/Ukraine conflict further complicated the energy trade.

Gulf Coast Crack Spreads ( EIA )

No one expects crack spreads to stay this wide indefinitely. There are new refining projects opening in Asia and the Middle East, with 1.6 mbpd coming online in 2023, and many refiners, flush with cash from last year, will spend smartly to debottleneck and increase capacity.

But 2023 could be another very good year for refining generally and for PBF specifically. From the chart above, we see that we're already starting 2023 at a much higher level than 2022. The 3-2-1 crack spread right now is near $40, which is historically very high, and unheard of for this time of year.

Refined Product Days Supply ((EIA))

Product stocks start the year still below 5-year averages and are building slowly. China is reopening, and the EU's ban of Russian refined products starts February 5th. I still expect Russian products to get to market, but the ban will likely complicate international product trade flows further.

Global Liquid Consumption Estimates (IEA)

With crack spreads so high in 2022, many refiners chose to defer as much maintenance as possible. But turnarounds can't be deferred forever, so the next few months will feature higher refinery capacity offline than normal. Right around when the Russian product ban starts, the US is expected to lose a significant amount of capacity through the end of the first quarter. After that, the EIA expects demand to accelerate after the normal seasonal Q1 dip.

US Projected Offline Refining Capacity (Reuters)

Add to this general activity levels that continue to increase, with business and airline travel returning, along with more workers being called back to offices. Why couldn't 2023 be as good of a year as 2022 for US refiners?

2023 Tailwinds

In 2022, PBF reinvested the majority of its free cash flow back into the business, mostly by reducing debt, but also by acquiring the portion of PBFX it did not already own, and progressing on a renewable diesel project.

All other things (read: crack spreads) being equal, 2023 results should show significant improvement over last year.

Natural Gas Prices

In 2022, the wholesale U.S. natural gas spot price at Henry Hub averaged $6.45/MMBtu. Thanks to a warm winter, ample supply, Freeport LNG being offline, and various other reasons, natural gas prices are much lower now than last year. I see little that is going to move them significantly higher, because supply - often associated gas from oil drilling - keeps increasing.

Refiners use a lot of energy, and a lower natural gas price helps them.

From PBF's 2021 10-K :

Our predominant variable operating cost is energy, which is comprised primarily of natural gas and electricity. We are therefore sensitive to movements in natural gas prices. Assuming normal operating conditions, we annually consume a total of between 75 million and 95 million MMBTUs of natural gas amongst our six refineries as of December 31, 2021. Accordingly, a $1.00 per MMBTU change in natural gas prices would increase or decrease our natural gas costs by approximately $75.0 million to $95.0 million.

Using the midpoint of this guidance, and a $3.50 natural gas price (the current price as of this writing is $3.07) amounts to a $255 million tailwind versus 2022.

PBFX Rollup

Last year, PBF announced a merger where it would acquire the remaining 52.3% of PBFX that it did not already own. This merger closed in November.

Under the merger agreement, each common unit of PBF Logistics was converted into 0.270 shares of PBF Energy common stock and $9.25 in cash. This cost $306 million + 8.9 million shares (~$390 million at today's closing price.)

PBFX had a steady operating history, with $147 million in net income in 2020, $153 million in 2021, and on track to do roughly the same this year.

PBF discussed cost savings from removing the overhead of running two companies, but without any consideration of that, just from a financial rollup perspective, acquiring the remaining 52.3% of PBFX should result in a ~$79 million tailwind over 2022.

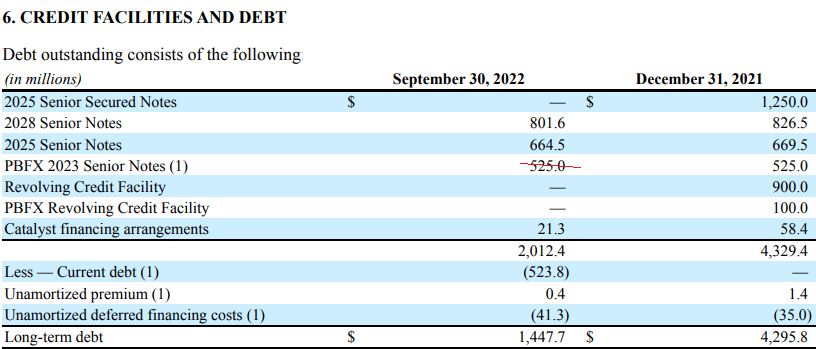

Debt (or lack thereof)

PBF entered 2022 with $1.3 billion in cash and $4.2 billion in debt. As of Q3, PBF had $1.9 billion in cash and $2 billion in debt - effectively net debt free. They will likely generate another $800 million+ in Q4 (my estimate.)

{kind=link}

PBF just announced the redemption of the $525 million in 6.875% PBFX Senior Notes.

In 2021, PBF paid $327.8 in interest expense.

In 2022, PBF has paid $216.6 in interest through Q3. Q4 will come in around $35 million, for a total of $251.6 million.

In 2023, PBF will carry $664.5 million of 7.25% 2025 Senior Notes and $801.6 million of 6.0% 2028 Senior Notes. Total interest expense from these notes is roughly $96 million/year. Additionally, short term interest rates are 4.5% and PBF is still sitting on around $2 billion in cash. This should almost net out and leave net interest at a de minimis level, maybe $10 million/quarter. $200+ million tailwind over 2022.

Maintenance CapEx above normal in 2022

2022 featured a heavier than normal turnaround cycle, as some assets were brought back from being shut during the pandemic, and other maintenance was deferred.

Then-CFO Erik Young:

Our annual maintenance CapEx has averaged between $150 million and $200 million a year, regardless of whether it's pre, during or post pandemic. We anticipate that will continue to come on. So when we think through the turnaround cycle and we're back to a regular way turnaround, the safe assumption for this year is we're going to be spending $325 million to $350 million on turnarounds

I'll assume 2023 is also a bit heavier and they do $225 in maintenance capital this year. This would be a $100+ million tailwind over 2022.

Renewable Diesel Project

PBF is adding capacity into its Chalmette (Gulf Coast) refinery to produce renewable diesel. The estimated project spend is ~$600 million, and as of the end of Q3, half of the capital spend was completed. The cost of this project was lower than a complete greenfield development because it makes use of an idled hydrocracker, and because many of the components were ordered before the recent burst of inflation.

The project is expected to start producing RD by mid-year 2023, and at recent RIN pricing, it is expected to produce over $400 million in EBITDA a year.

Then CFO Eric Young on the Q3-22 Conference Call

To Matt's point, this thing is essentially halfway there. So we've got another, call it, $300 million to $350 million of CapEx that I think we're comfortable overall investing to get that project up and running because that kind of current market environment or current market prices with 300 million gallons a year of production on an annualized basis, that should generate $400 million a year in EBITDA.

Whether RIN pricing drops or not, this will be a big win compared to 2022.

To be conservative, I'll assume this project is half as good as they project it to be, which I think is fair until proven otherwise since PBF has little experience with RD projects.

Operating at half a year, and using half their company's estimates makes this a $100 million tailwind over 2022 , which hopefully will increase significantly in future years.

Adding this all up , it moves the 2023 starting line-up $700 million over 2022 results.

What will they do with all the cash?

Last year, PBF used almost all of its cash flow to deleverage. I think they'll continue down this path and repay the $664.5 million of 7.25% 2025 Senior Notes in June, when they become callable at par. The few hundred million in remaining spend for the RD project will wrap up around the same timeframe.

After that, I think the majority of cash flow will be directed towards increased shareholder returns, hopefully upsizing the already announced repurchase authorization.

Conclusion

Like any energy investment, PBF will be at the mercy of commodities markets, but I think the current low valuation creates an asymmetric risk/reward setup.

This investment doesn't need a repeat of last year's crack spreads to be a winner, but if we get a repeat, it will be a massive winner and could double from here. Fundamentally speaking, I don't see much different in the environment between last year and this year. I could even argue this year's setup looks better.

I believe domestic refining will see a higher level of mid cycle earnings for at least the next few years as a result of structural supply tightness, and I think PBF has significant upside from it.

For further details see:

PBF Energy Could Be A Huge Winner In 2023