PBF - PBF Energy Is Incredibly Undervalued But Is 'Stuck' At Its Current Valuation

2024-01-16 21:30:19 ET

Summary

- PBF Energy continues to generate tons of cash but still has not experienced any multiple expansion to reward its efforts.

- The company has paid down debt, bought back shares, and increased the dividend. Management doesn't have many other tools at its disposal to drive multiple expansion.

- While an investment in PBF may look appealing due to its low valuation, I see no catalysts to drive the stock price meaningfully higher.

- The main investment thesis for PBF is a value play. If management cannot find a way to sell PBF's performance to the investment community, PBF may become a value trap.

The last time I covered PBF was nine months ago in April of 2023. In that article, I argued that shareholders of PBF should sell to harvest what amounted to nearly 500% gains over the prior two years. My main reason for this was because refining crack spreads had significant potential to decrease following 2022 which they hit decade highs. I also stated I was in favor of larger peers Phillips 66 ( PSX ) and Marathon Petroleum ( MPC ) due to their diversification in midstream assets and higher yields. I got a lot of pushback because PBF was significantly discounted compared to these large-cap refiners and represented a deep discount to NAV play.

Today, PBF is still severely undervalued. After another solid year in the refining space, and one that saw PBF return $372 million in share buybacks and increase the dividend from $0.05/share to $0.25/share since my last article, PBF still has not experienced any multiple expansion. In fact, PBF now trades near the levels when my first article was published ($42.86/share vs $42.21/share on April 6th, 2023) with a trailing P/E ratio of 2.67x.

Since then, PBF's performance as a company has only gotten better. Unfortunately, the stock has not followed suit. This article will dive into why I expect PBF to continue performing well but I do not expect any multiple expansion to lift the stock price. PBF is a clear value play. However, to experience true appreciation, it must transition from undervalued to fairly or overvalued. Otherwise, PBF is just stuck in the mud.

Absurdly Low Valuations

PBF is a conundrum to me. With an EV to EBITDA of essentially 1 and a trailing PE ratio of 2.67x, there is nothing to conclude other than PBF is extremely undervalued. This conclusion has been detailed in several articles on Seeking Alpha over the last two months.

1. PBF Energy: A Deeply Undervalued Top-Rated Energy Play for 2024 and Beyond. Published 12/13/23

2. The Bottom Fishing Club: PBF Energy. Published 11/4/23

The deep value investment is a powerful investment thesis. This thesis, however, hinges on the fact that one day it will be fairly or overvalued. That is the only tangible way to realize capital appreciation.

This thesis has not played out well over the last 18 months. PBF's PE ratio has actually contracted not expanded, despite recording higher earnings, improving its balance sheet, and increasing the dividend. This brings me to my contrarian viewpoint. What else can PBF realistically do to attract investors and drive up what people are willing to pay for this company?

The company has not committed to any large-scale future project to drive future growth. The only thing advertised at the moment is a loosely framed hydrogen hub project with no projections on potential earnings or capital requirements. PBF needs to start putting the pedal to the metal and provide clear direction on how it plans to spend its excess cash. Otherwise, PBF isn't a value play, it's a value trap .

Earnings Potential

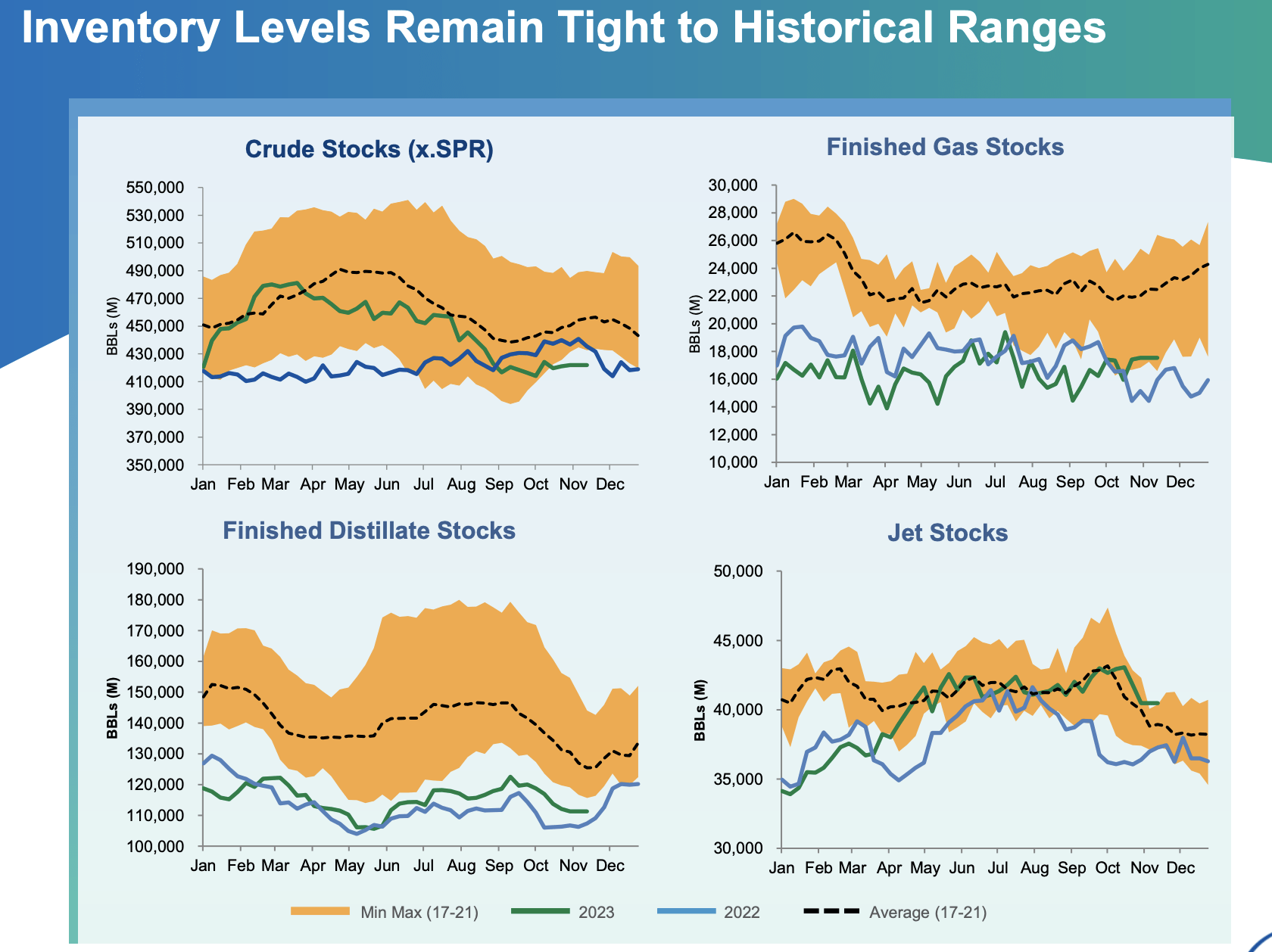

While crack spreads have dropped off recently , this follows typical seasonality that the industry has not seen in a few years. Despite this near-term pressure, the fundamentals for gasoline and distillate still support robust crack spreads going forward.

The inventory levels of both of these products are well below the 5-year average, leaving little storage to compensate for high demand periods. The winter and early spring months are generally periods of high consumption of distillate due to heating and the beginning of farming season while the summer driving season drives the crack spread for gasoline.

As I write this, much of the United States is at the beginning of the first deep freeze of the winter season. A prolonged cold spell could be the start of a distillate tailwind to kick off 2024. Gasoline and distillate equate to just over 80% of PBF's production and as a result, the company will be well positioned when seasonal demand signals begin driving crack spreads higher.

{kind=link}

To put some meat behind this thesis, executives from Phillips 66 and Valero ( VLO ) have similar viewpoints on how the distillate market is shaping up for the near term.

Phillips 66 ((PSX)), January 4th, 2024 - The crack spreads have seasonally tightened up a bit, but distillate is still strong. Gasoline is, of course, seasonally impaired a little bit, but we see strength going into next year. Barring any major recessionary activity, we think we're going to continue on a good constructive path.

Gary Simmons, Valero COO weighed in during the Q3 earnings call to give his viewpoint on future crack margins.

In terms of the outlook going forward, we'd expect gasoline to kind of follow typical seasonal patterns, weaker cracks, kind of the fourth quarter and first quarter.

The thing we're really looking at, as you know, the fundamental that looks good to us is the market structure still doesn't really support storing summer-grade gasoline, putting gasoline in New York Harbor for driving season next year. So as long as that's the case, our view would be that when you get to driving season next year, demand picks back up, you'll see cracks respond.

So diesel demand remains very strong. Our view of the broader markets is that diesel demand in the U.S. is probably down about 1% year-to-date from where it was last year, and that's mainly due to the warmer winter we had last year. Our guys' estimate, we lost about 125,000 barrels a day of diesel demand due to the warmer weather. So inventories remain below the 5-year average level, demand remains good. So you're heading into winter with low inventories, and we would expect strong diesel cracks through the winter and could get very strong if we have a colder winter.

Overall it looks as if PBF is positioned to continue its stretch of strong profitability in 2024. The refining market continues to be generally under-supplied, and inventories continue to remain near decade lows. Barring any recessionary event that largely affects consumer demand, crack spreads should continue to remain robust.

Management is Giving Everything It Has...Even the Kitchen Sink

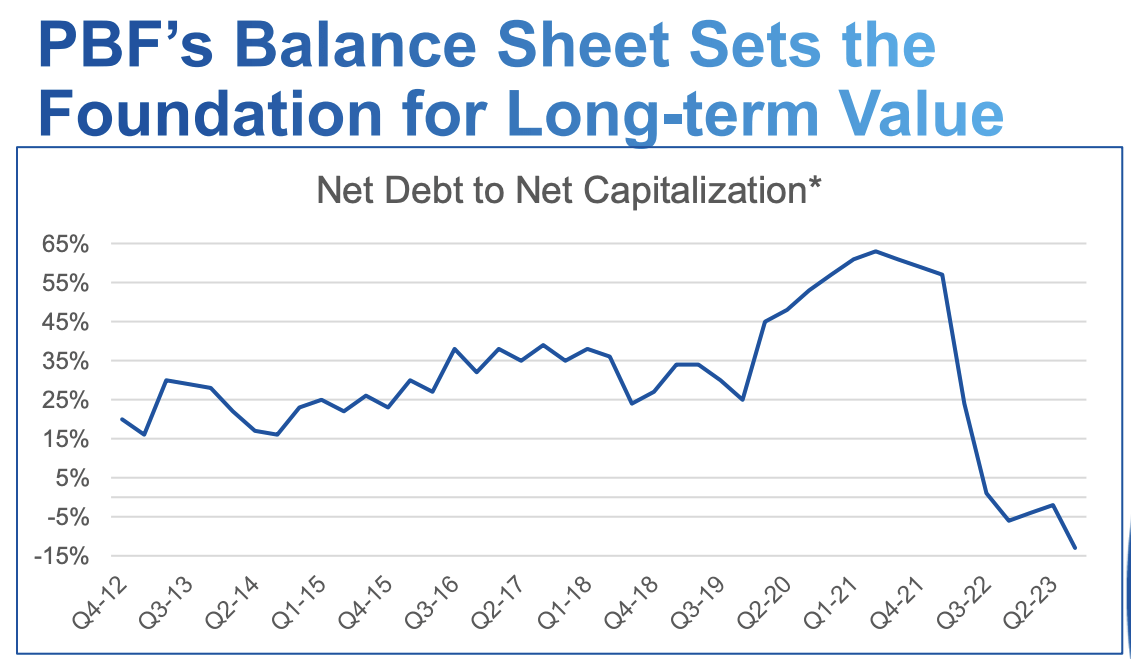

One area that PBF continues to do well is its cash management. PBF as a company has dramatically improved. In fact, PBF has gone from a company with $3 billion in debt to a net positive cash position in just two years' time.

{kind=link}

PBF has done far more than just buyback debt. Matthew Lucey perfectly detailed PBF's accomplishments during the Q2 conference call.

We have repaid over $3 billion in debt, repurchased PBF Logistics and PBF Inventory Intermediation Agreements, reduced our environmental credit payables by about 40% since the beginning of the year, and to the renewable fuels business with a world-class partner in Eni, restart paying a dividend and commenced in executing a share buyback program where we bought about 8% of the shares.

To build on that resume, Q3 was another strong quarter. The company increased the dividend from $0.20/share to $0.25/share, and repurchased $113 million of company stock, while also retiring $170 million debt. The company also commenced operations at its renewable diesel refinery, St. Bernards Renewables. SBR was able to produce 17,000 barrels per day of renewable diesel profitably right out of the gate.

The question I am faced with now is, what is the path forward? How can I logically explain a path toward multiple expansion? The refinery business is cyclical like many other energy-related industries. Even though I believe 2024 will be a solid year for PBF, it would be foolish to assume this level of profitability is sustainable forever. It would also be foolish to expect a "super-cycle" like that which occurred in 2022. If investors haven't valued PBF at this point, will they ever?

There is a lot to like about PBF, and it has done a lot for its shareholders. At this point, I can't see anything that PBF can achieve in the near term that would exceed what it already has done. As a result, I believe PBF is stuck at its current valuation with limited upside from here.

Get Your Pitchforks

Before the PBF loyalists get ready to take me out behind the woodshed, let me propose one more piece of data that would explain why PBF is "stuck" in this low multiple conundrum.

The ownership profile of PBF is notably different than its peers. PBF is almost entirely owned by institutions and corporations with only roughly 5% of its stock owned by the 'average Joe'. The table below summarizes the ownership profile of a group of peers. All data was obtained from the Seeking Alpha page for each stock.

| PBF |

| PSX |

| VLO |

| MPC |

| DINO |

| Institutions |

| 82.8% |

| 73.6% |

| 80.1% |

| 77.3% |

| 71.6% |

| Corporations |

| 10.3% |

| 0% |

| 0% |

| 0% |

| 13.8% |

| Insiders |

| 1.6% |

| 0.2% |

| 0.5% |

| 0.2% |

| 0.3% |

| Public |

| 5.4% |

| 26.2% |

| 19.4% |

| 22.5% |

| 14.2% |

To get multiple expansion, there needs to be a liquid source of stock that can be bought. New buyers need to be introduced that are willing to pay a premium. Large chunks of stock typically get bought up by a large investor or institution. A prime example is the $1 billion stake Elliott Management bought in Phillips 66 in November. As the fund acquired shares and eventually announced its stake and intentions, the stock experienced tremendous gains, largely unrelated to any immediate change in earning potential.

The trouble I see with PBF at the moment is there just isn't that much stock held in the public's hands. This makes it difficult for an investment firm to come in and drive multiple growth.

Risks

We've discussed how PBF is largely undervalued by multiple different metrics. This gives a strong price floor to provide downside protection should crack spreads drop off. The combination of this, with low inventory levels, provides reasonable assurance that in the near and medium terms, there is low downside risk to the company's profitability.

As I have discussed so far in this piece, PBF the company, and PBF the stock performs differently. Despite the promising outlook, the near-term price action of the stock appears bearish. The 50-day moving average is approaching the 200-day moving average in a downward pattern. If the 50-day were to breach the 200-day, this could indicate near-term weakness for the stock.

Summary

Since my last article on PBF, the company has performed well. The company has continued to buy back stock, retire debt, and increase the dividend. With inventories in distillate and gasoline well below 5-year averages, there is strong fundamental support for crack spreads over the medium term.

The company continues to be severely undervalued, trading at a P/E of less than 3 and EV/EBITDA of roughly 1. This can be seen as a positive by many. I am however worried that the market just refuses to recognize the performance of PBF and that multiple expansion will be difficult in the future. The company has solid prospects to continue rewarding shareholders as distillate and gasoline inventories remain very low. Even if the company significantly ramps up shareholder returns, will this be enough for Wall Street to start paying a premium? If not, PBF appears to be stuck.

In April 2023, I previously rated PBF as sell. Given the progress PBF has made since then, I now upgrade it to a HOLD.

It is hard to deny the value prospects of PBF. If the stock displayed some evidence of multiple expansion (or if the management team provided firm details on how it intended to do so), PBF would certainly be a buy or possibly a strong buy recommendation.

For further details see:

PBF Energy Is Incredibly Undervalued, But Is 'Stuck' At Its Current Valuation