XYLD - PCEF: A High-Yield Alternative Poised To Rally Into 2024

2023-11-16 13:05:53 ET

Summary

- Invesco CEF Income Composite ETF is an "ETF of CEFs" that tracks a basket of income-focused closed-end funds.

- The fund offers a 10% yield through a monthly distribution.

- We see the macro backdrop as positive for this unique market segment going forward.

The Invesco CEF Income Composite ETF ( PCEF ) can be described as a fund of funds, or an "ETF of CEFs," tracking a basket of income-focused closed-end funds.

The attraction here is the opportunity to capture diversified exposure to this unique segment of the market. Closed-end funds, or CEFs, are recognized as actively managed investment vehicles that represent alternative strategies and often employ leverage or options writing to generate high levels of income.

This is a fund we previously covered back in 2019 with an article concluding with a hold rating at the time. While a lot has changed in the period since, including significant macro headwinds pressuring fixed-income returns and overall more volatile equity conditions in recent years, PCEF has favorably outperformed several key benchmarks.

Fast forward, the update here is that we see room to turn more positive with an expectation for stronger returns going forward. An environment of more stable interest rates alongside a resilient economy through 2024 should be positive for PCEF, and supportive of its 10% yield distributed monthly.

What is the PCEF ETF?

PCEF tracks the "S-Network Composite Closed-End Fund Index" targeting income-focused CEFs specifically. According to the methodology , the strategy includes funds across three sectors:

- Investment Grade Fixed Income Closed-End Funds

- High-Yield Fixed Income Closed-End Funds

- Option Income Closed-End Funds.

The allocations include bonds, credit, loans, convertibles, preferred shares, and derivatives with a significant portion being long-equity options-based strategies. The other takeaway here is that while the underlying CEFs are actively managed, PCEF itself is a passive instrument .

In terms of the CEFs selected, there is a minimum asset under management threshold of $100 million along with average daily trading liquidity. The weighting adds a factor adjustment to favor funds trading at a discount to NAV while single holding is capped at 8% of the fund's total investment.

The result is a distinct vehicle that combines the advantages of an exchange-traded-fund ("ETF") structure which are liquidity and asset transparency, with the allure of CEFs which is the high income and potential for excess returns.

PCEF Portfolio

With a portfolio of 112 funds, PCEF essentially covers the universe of income CEFs. The largest current position is in the Eaton Vance Tax-Managed Global Diversified Equity Income Fund ( EXG ), which is a buy-write equity CEF with $1.5 billion in AUM. EXG as an example of this type of strategy, essentially holds a portfolio of globally diversified stocks while the portfolio management team sells call options on those positions to generate income.

Going down the list, approximately 42% of the exposure is classified as similar option income CEFs, followed by 26% in high-yield bond or credit strategies, 11% in taxable bond funds, and a smaller position in municipal bond funds along with cash.

The understanding here is that the breadth of the fund is extensive enough that the performance of the CEF sector takes precedence over any individual holding.

Seeking Alpha

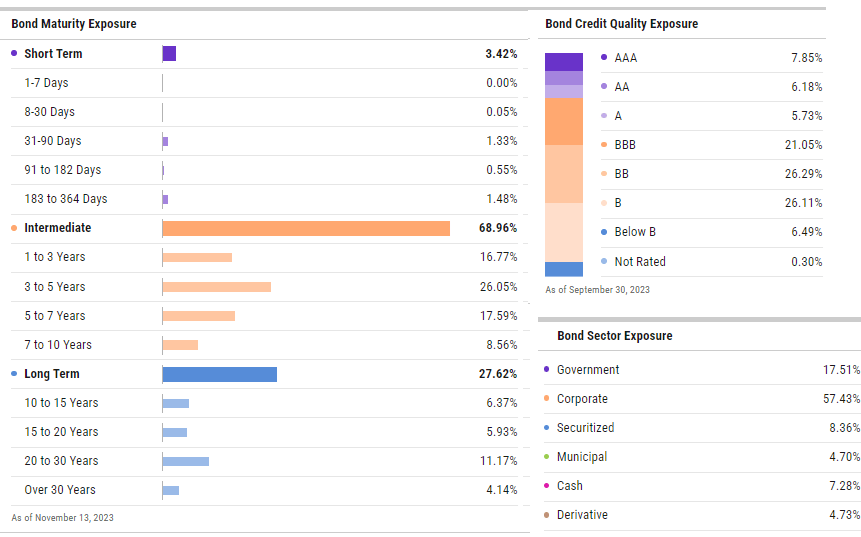

What we want to bring attention to is the fixed income exposure which represents more than half of the entire fund strategy. Here we note that PCEF carries what can be described as an intermediate-maturity portfolio where the average duration is listed at 4 years.

This means that PCEF is moderately sensitive to changes in market interest rates, but far from the type of volatility observed in long-term bond funds. Separately, the credit profile is more than half in "junk bonds," although nearly 40% is investment-grade also reflecting a balanced profile.

{kind=link}

PCEF Performance

We mentioned that PCEF has outperformed benchmarks in recent years. Specifically, the data we have is that PCEF with a 20% cumulative total return in the past 5 years is ahead of the overall "bond" market, which we proxy through the iShares Core U.S. Aggregate Bond ETF ( AGG ) with a 2% return over the period.

PCEF also beats out the iShares iBoxx $ High Yield Corp Bond ETF ( HYG ) with a 15% return, as well as the Invesco S&P 500 BuyWrite ETF ( PBP ) as an options strategy benchmark which returned 19.5% in the last 5 years.

At the same time, it's evident from the chart below that PCEF has been more volatile, underperforming more recently from the highs in late 2021.

The caveat here is that it's hard to find a direct benchmark for PCEF considering its combination of both equity option income strategies and fixed-income funds.

We can say that the allocation worked well during a period when bonds were under pressure with rising interest rates since last year because of its equity positions, but also underperformed more vanilla equity funds over the same period.

Simply put, PCEF sits between the two asset classes, meaning its performance should be a mix of stocks and bonds. Indeed, that dynamic is more visible over the last 3 years where PCEF has returned 4.4%, which is an improvement compared to the -14% loss from AGG, but well below the 18% return in the PBP buy-write fund.

We can also bring in a separate Global X S&P 500 Covered Call ETF ( XYLD ) with a similar return to PBP over the period, with the difference being that XYLD has a higher income component comparable to PCEF.

Our point here is not to say that PCEF is "better" or is always to outperform a different strategy, but simply that it needs to be viewed for its own merits. The various factors driving both the return history and forward outlook, along with the risk profile, should be considered.

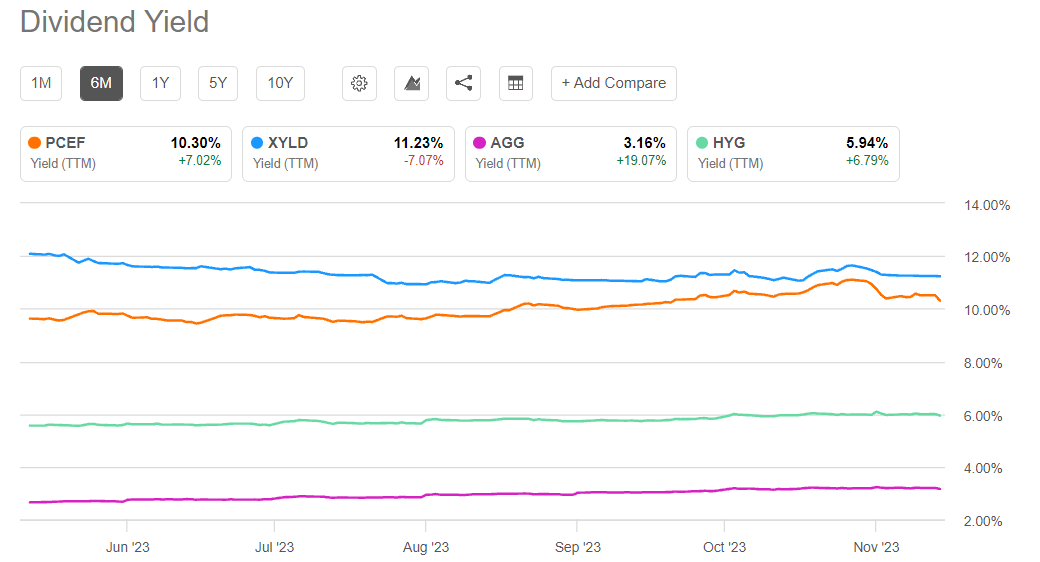

The current listed 10% dividend yield as an aggregate of the underlying funds' distributions is slightly lower the 11% offered by XYLD, but well above unleveraged high-yield bonds like the 6% from HYG.

While PCEF's listed expense ratio at 1.99% is elevated, keep in mind that this includes 1.49% from fees of the underlying funds, while Invesco's management fee' is a more reasonable 0.50% and similar to the 0.6% from XYLD. Still, that higher cost can be justified by the potential that the fund can outperform to the upside.

{kind=link}

What's Next For PCEF?

Notably, PCEF has rallied nearly 10% in recent weeks amid a broader burst of momentum in the market. Compared to the backdrop of rising interest rates and concerns the Fed would need to keep hiking over the past year, the latest macro development has been favorable inflation data with the October CPI coming in below expectations reaching an annual rate of 3.2%.

Our take is that with building confidence that inflation will continue to trend towards the 2% target, a 5.5% Fed Funds rate becomes unnecessary, and opens the door for rate cuts down the line in 2024.

The setup has driven a sharp pullback in long-term bond yields through the repricing. For context, the 10-year Treasury yield (US10Y) current at 4.5% is down from a cycle high above 5.0% last month.

Naturally, the scenario where bond yields have potentially seen their highs for the cycle can be very bullish for the bond market including the underlying exposure of the PCEF portfolio.

{kind=link}

When thinking about CEFs as a sector, the outlook for lower interest rates offers a separate tailwind considering many of the funds utilize leverage and are thus impacted by the cost of debt. This means that the strategies become relatively more attractive, all else equal, which can be translated through a shifting spread to each fund's net asset value.

While the trend of rising interest rates over the past year generally resulted in a widening discount between the CEFs' prices and their NAV (or at least a lower premium) a reversal from here means that there is room for spreads to narrow (or see the premium climb).

This adds an incremental layer of return to the upside as PCEF rallies higher. Even as PCEF itself as an ETF does not trade at a spread to NAV, that factor is carried through its underlying exposure.

On the equity side, we believe stocks and option-income strategies should also perform well. A continuation of a resilient U.S. economy, while interest rates stabilize, is supportive of the corporate earnings environment as well as valuation multiples.

Final Thoughts

We like PCEF as a portfolio diversifier and income vehicle. The bullish case for the fund is based on the view that CEFs should once again outperform to the upside as the strategies benefit from an improving macro backdrop.

On the other hand, we can consider the possibility of a deteriorating economic outlook as a risk to consider. A scenario where inflation re-accelerates and interest rates make a new cycle high would likely drive a new round of market volatility.

For further details see:

PCEF: A High-Yield Alternative Poised To Rally Into 2024