CION - PCF: A Good Diversifier For An Income Portfolio But Distribution Appears Strained

2023-10-04 13:54:55 ET

Summary

- High Income Securities Fund offers a remarkable 12.04% yield, but this high yield may indicate an expectation of future reduction.

- The fund's portfolio consists of common equity securities issued by business development companies, which are quite rare to find in any closed-end fund.

- The fund's distribution has been inconsistent in the past, and its ability to sustain its current distribution is uncertain.

- Interest rates in the United States may stay high for longer than expected, which will limit the fund's potential to earn capital gains.

- The fund is currently trading at a discount to NAV, but its lack of regular updates makes an exact valuation difficult.

High Income Securities Fund ( PCF ) is a closed-end fund, or CEF, that has long been a fairly popular way for investors who desire income to obtain it. This is evidenced by the fund’s remarkable 12.04% yield at the current price. However, as I have pointed out numerous times in the past, any time a fund manages to obtain a yield that is this high, it is a sign that the market expects that it will be reduced in the near future. As such, we want to investigate this situation in order to see exactly how sustainable the distribution is likely to be.

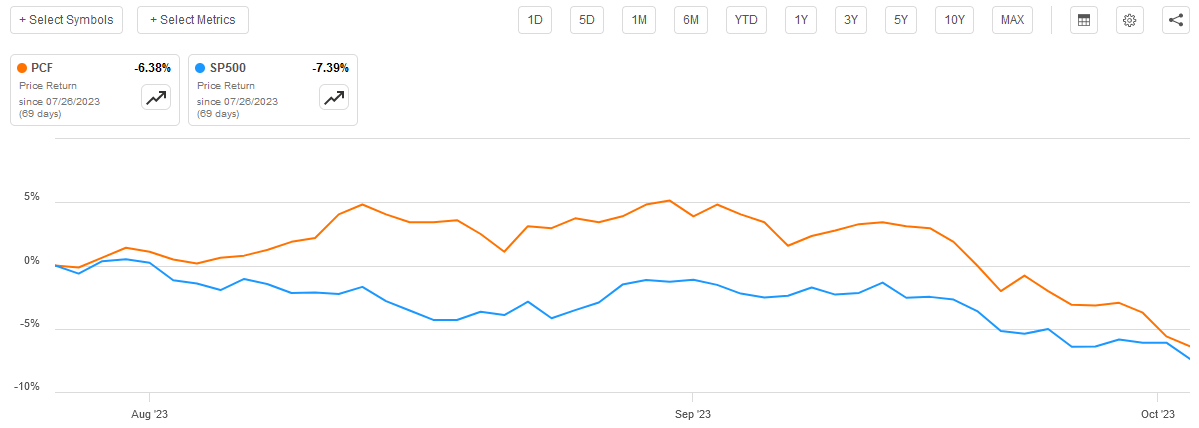

As regular readers will likely recall, we last discussed this fund around the end of July. At the time, I had some concerns about it due to the difficulty of finding information about it as well as the multiple distribution cuts over the past three years. The market has been more optimistic about the fund, at least since the time that the article was published. As we can see here, shares of the fund have only declined by 6.38% since the date of publication, beating the S&P 500 Index ( SP500 ):

{kind=link}

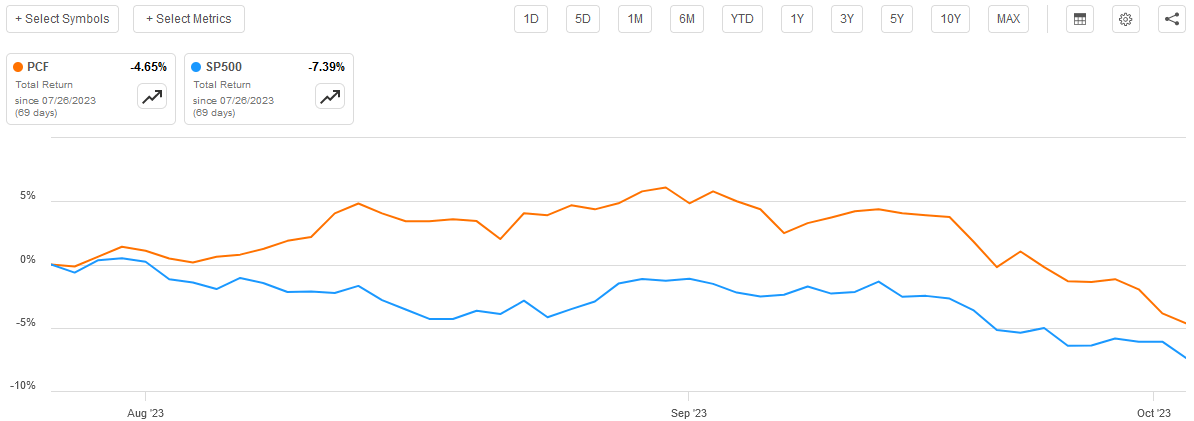

The difference is even more stark when we include the distribution in the fund’s returns. This is something that we really should do with closed-end funds considering that the distribution accounts for the vast majority of the total investment return that the fund provides to its shareholders. In this case, shareholders in this fund would have only lost 4.65% since the time that my previous article was published, which was clearly a far better choice than parking money into the S&P 500 Index:

{kind=link}

As the prior article was published several months ago, there have been some changes to the fund’s portfolio. Perhaps more importantly, the market has changed dramatically as investors are finally waking out to the very real probability that there will not be any near-term interest rate cuts, inflation has gotten worse, and yields across the market are rapidly increasing. These all have a significant impact on this fund, as it bills itself as a solution for the generation of income. As such, we should revisit the fund and our general thesis and see if purchasing it today makes any sense.

About The Fund

As I pointed out in my previous article, the webpage for the High Income Securities Fund is extremely spartan and does not include a description of the fund’s objectives or strategy. In fact, it does not even include a fact sheet, which makes this the only closed-end fund that I have ever seen that does not include such rudimentary information on its webpage. The fund does include information about the strategy and objectives in its semi-annual report , but it is necessary to dig through the document to find it. For reference, shareholders can find this information on page 20 of the 52-page document. Here is how the semi-annual report describes the fund:

The goal of the Fund continues to be to provide high current income as a primary objective and capital appreciation as a secondary objective. The Fund pursues its objective primarily by investing, under normal circumstances, at least 80% of its net assets in discounted securities of income-oriented closed-end investment companies, business development companies, fixed income securities, including debt instruments, convertible securities, preferred stocks and special purpose acquisition companies. The Fund also invests in high-yielding non-convertible securities with the potential for capital appreciation.

This is probably what most people expect when picturing a high-income fund. The ordinary assumption is that the fund will be investing in fixed-income securities such as preferred stocks and bonds, perhaps with special attention paid to junk bonds. However, 54.84% of this fund’s portfolio is invested in common equity:

CEF Connect

With that said, this common stock allocation consists mostly of the common equity securities issued by business development companies. These are a type of company that we do not hear very much about in the news media or even across the online investment community. A business development company is a specialized form of closed-end fund that invests primarily in debt securities issued by private companies. They may also take common equity positions in these companies, although common equity positions are more often obtained by purchasing things such as convertible preferred stock or convertible bonds in private companies. An ex-business partner of mine once described these as “publicly-traded private equity funds,” which actually describes them very well. We do not see them very often as an investment in a closed-end fund, but there are a few such as this one and the Saba Capital Income & Opportunities Fund ( BRW ) that include positions in them.

One of the nicest things about business development companies is that they tend to have very high yields. We can see this quite clearly by looking at the current yields of the largest positions in the High Income Securities Fund. Here they are:

CEF Connect

Here are the yields possessed by these companies:

| Company |

| Type |

| Current Yield |

| FS KKR Capital Corp ( FSK ) |

| Business Development Company |

| 13.49% |

| First Trust Dynamic Europe Equity Income ( FDEU ) |

| Closed-End Fund |

| 6.97% |

| CION Investment Corp. ( CION ) |

| Business Development Company |

| 13.32% |

| Suro Capital Corp. ( SSSS ) |

| Business Development Company |

| N/A |

| BlackRock ESG Capital Allocation Term Trust ( ECAT ) |

| Closed-End Fund |

| 9.70% |

| Saba Capital Income & Opportunities Fund |

| Closed-End Fund |

| 13.82% |

| Highland Opportunities and Income ( HFRO ) |

| Closed-End Fund |

| 11.91% |

| Neuberger Berman Next Generation Connectivity ( NBXG ) |

| Closed-End Fund |

| 11.88% |

| Portman Ridge Finance Corp. ( PTMN ) |

| Business Development Company |

| 14.96% |

| Nuveen Short Duration Credit Opportunities |

| Closed-End Fund/Defunct |

| N/A |

The Nuveen Short Duration Credit Opportunities Fund was formerly traded under the symbol JSD, but it is no longer available. This is, unfortunately, one of the problems with the High Income Fund’s lack of transparency and communication that I pointed out in my previous article on this fund. For some reason, the fund’s most recent holdings report on its website is actually the semi-annual report dated February 28, 2023. There is a holdings report available from the Securities and Exchange Commission dated May 31, 2023, if you dig through the database available on EDGAR, which is where the above information comes from, but it should not be that difficult to obtain recent copies of the fund’s documents.

It is uncertain what the Nuveen Short Duration Credit Opportunities Fund was replaced with, as the fund has not yet made that information publicly available anywhere.

We can still clearly see though that the fund is taking some unorthodox attempts to achieve a high level of income from the assets in its portfolio. After all, it is one of only a few closed-end funds that actively invests in either other closed-end funds or business development companies. This could have two very positive effects from an investment perspective, however. The first of these is that it can allow an investor to add an asset class to their portfolio that they would otherwise have limited exposure to. As such, it works quite well from a diversification perspective.

In addition, it could make the distribution more sustainable than we would otherwise expect. After all, the yields shown in the chart above are all fairly comparable to the yield that the fund itself pays out. The fact that the fund is collecting such yields from the assets in its portfolio makes it quite easy to accept that it could pay out a similar amount of money. We will naturally investigate this more later, but it is not inconceivable the fund’s income is a lot higher than might be expected.

Current Market Trends

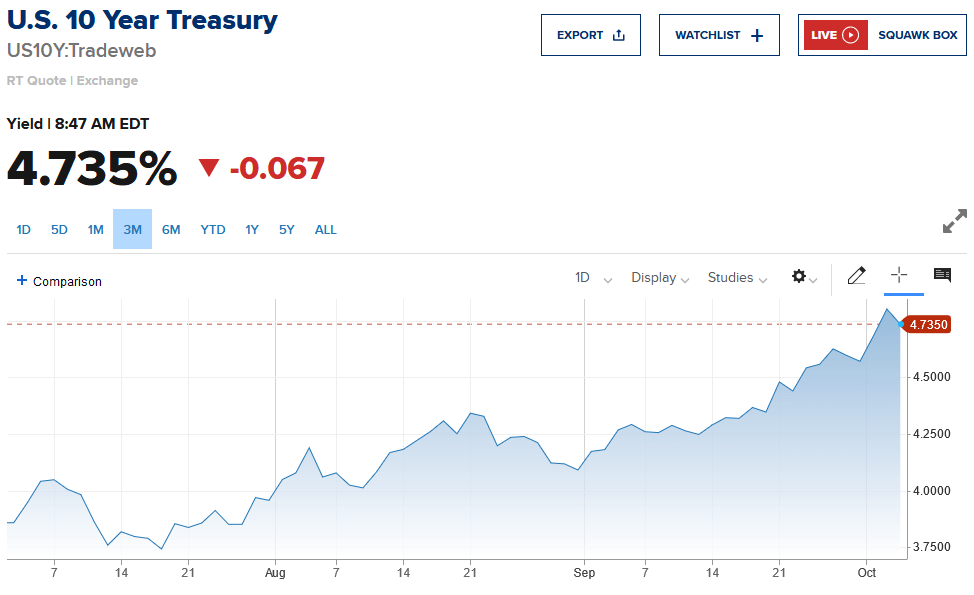

It is difficult to deny that the market has re-entered a bear phase. As mentioned in the introduction, the S&P 500 Index is down 7.39% since the late July publication date of my previous article on the High Income Securities Fund. Interest rates are also up, by quite a lot. The ten-year U.S. Treasury, which is widely considered to be the de facto “risk-free” benchmark, had a yield of 3.85% three months ago. Today, the bond is yielding 4.735%:

{kind=link}

This has had an impact on all assets and caused a wave of repricing across the market. This is because most assets are priced in some way off of the risk-free rate. Thus, as the ten-year Treasury yield increases, the price of pretty much everything else will decline because these alternatives have to offer a much higher return in order to attract investor dollars. This makes sense since nobody will buy a ten-year investment-grade corporate bond with a 4.7% yield when they could buy a ten-year Treasury instead. That is the biggest reason why we have been seeing such steep sell-offs in both the stock and bond markets.

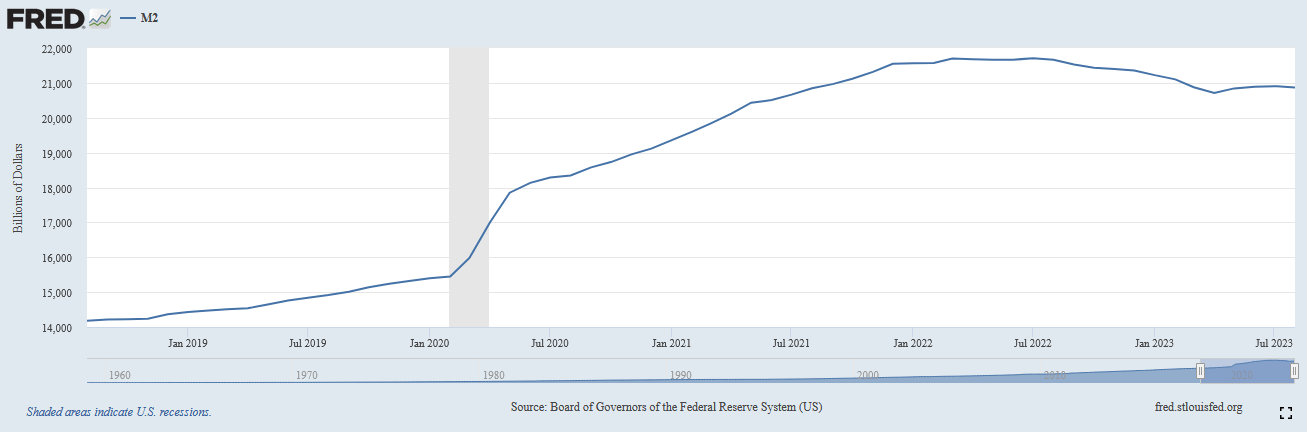

Thus, it is important to have some idea as to the direction of interest rates going forward. This is difficult to predict, as the Federal Reserve’s monetary policy is only one factor. The other factor is the demand for money against the supply of it. As a few commentators and analysts have mentioned over the past several months, during the second half of last year, the M2 money supply started declining. This has continued through to the present day, although the situation has moderated somewhat:

{kind=link}

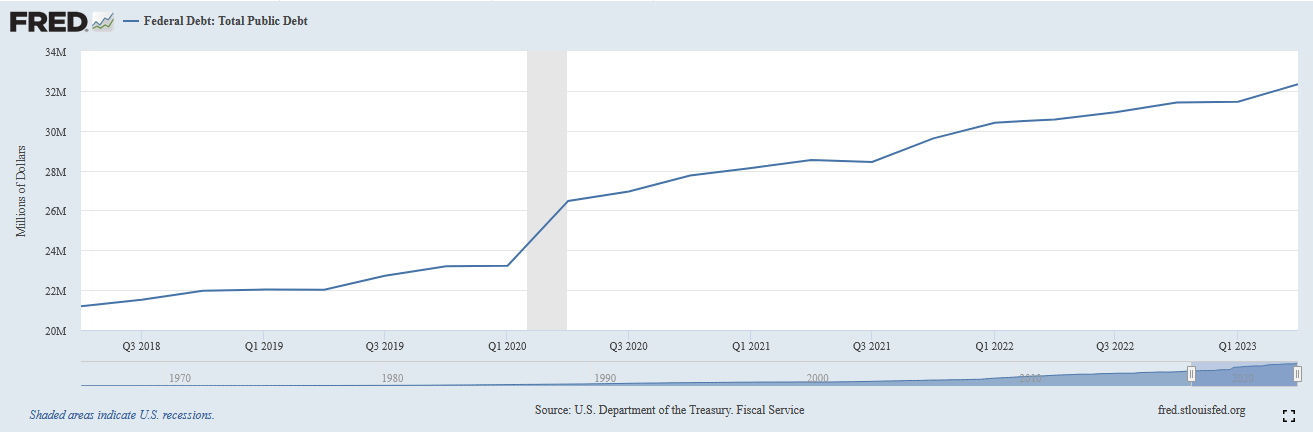

As we can see, the M2 money supply actually increased in May, although since then it has largely been bouncing around between $20.800 trillion and $20.900 trillion. This is important because the U.S. national debt keeps increasing. We can see that here:

{kind=link}

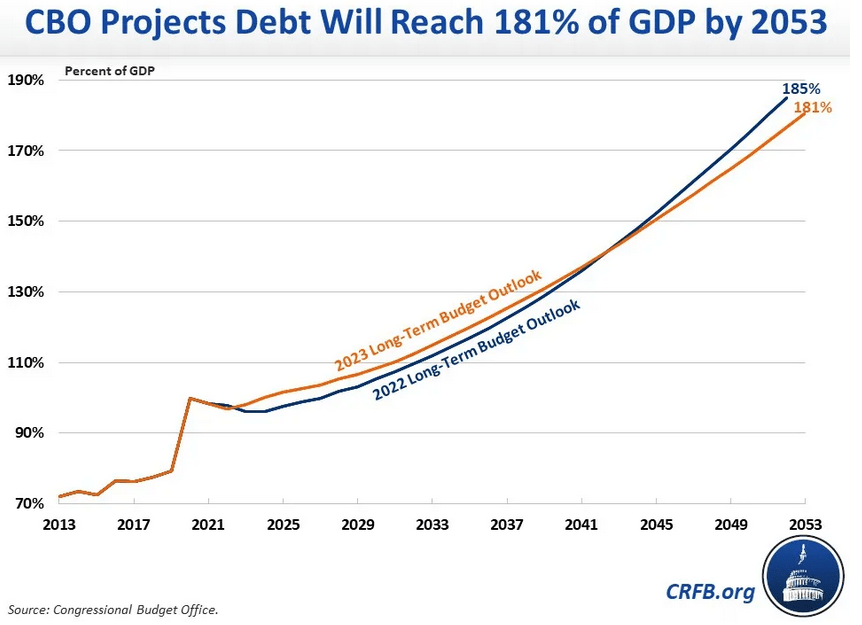

Thus, the Federal government is demanding greater sums of money to fund its operations, but the money supply is not growing. Thus, the demand for money is increasing due to the government but the supply of it is not increasing. That pushes up interest rates because governments and institutions that need money have to compete against each other to obtain it. It seems highly unlikely that this government demand will go away anytime soon. The Congressional Budget Office projects that the Federal deficit will increase from $1.5 trillion today to $2.5 trillion by 2033 if no changes are made to current law:

{kind=link}

Thus, the long-term trajectory for interest rates points higher in the absence of massive growth in the private sector. That is, to put it mildly, unlikely considering the aging population, the fact that energy supplies are likely to be much more constrained over the next decade than they were over the last five, declining worker productivity, and other factors. Thus, private wealth will probably not grow rapidly enough to absorb the government’s demand for money, and this will push up interest rates. Mainstream media sources have even started to take notice of this, as a recent guest on CNBC suggested that ten-year rates may hit 13% within seven years and, while that may seem impossible, others have stated that rates will not come down much within the next seven years.

If rates remain significantly higher than the market expects, as the above analysis suggests, then it could exert considerable downward pressure on the price of this fund’s shares. However, the majority of loans made by business development companies tend to be floating-rate loans. These companies should thus be much more resistant to the effects of rising interest rates than companies in most other sectors. That should extend to the fund considering that a high proportion of its portfolio is in these companies. As such, this fund should be somewhat more resistant to rising interest rates than a fund that invests primarily in fixed-rate corporate securities or junk bonds.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the High Income Fund is to provide its shareholders with a very high level of current income. In order to accomplish this task, the fund invests primarily in business development companies, closed-end funds, and other assets that have enormous yields. It collects the payments that it receives from these securities along with any capital gains that it manages to realize and pays them out to its shareholders, net of the fund’s own expenses. As many of the securities in the portfolio boast double-digit yields, we can expect that it will have a tremendously high yield itself.

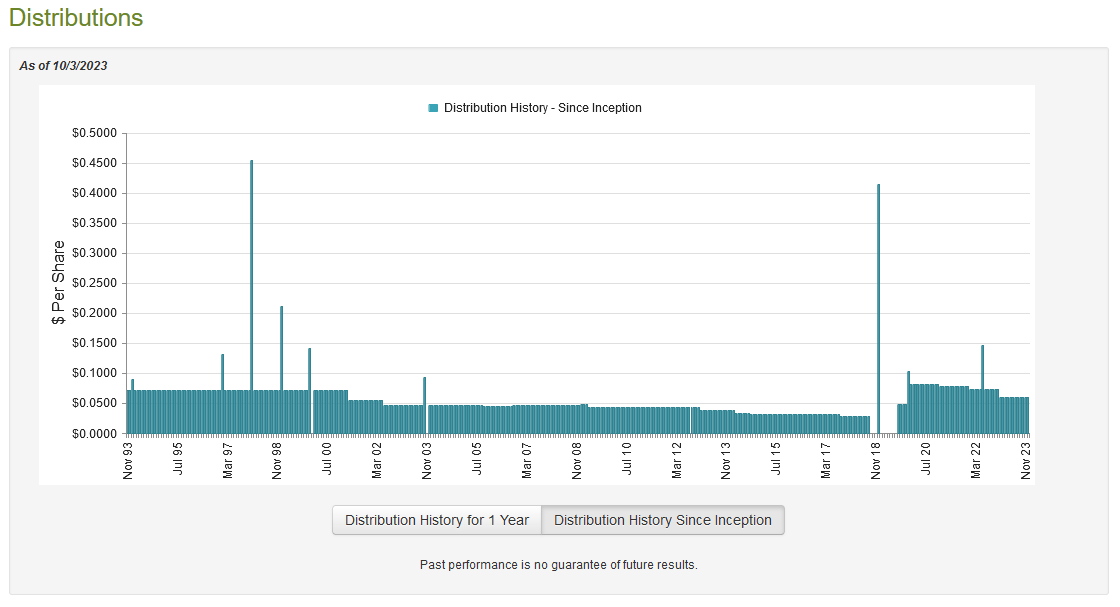

This is indeed the case as the High Income Securities Fund pays a monthly distribution of $0.0604 per share ($0.7248 per share annually), which gives it an enormous 12.04% yield at the current price. Unfortunately, the fund has not been especially consistent with respect to its yield over the years, as it has both raised and cut it numerous times:

{kind=link}

This history is likely to be a turn-off for anyone who is seeking a safe and secure distribution to use to pay their bills or finance their lifestyles. In particular, the fact that the fund has cut its payout three times since 2020 will certainly prove concerning. However, the current distribution is still higher than the fund’s distribution at any time prior to January 2020 so it is not necessarily the end of the world. The big concern here is how well the fund can sustain its current distribution going forward. After all, anyone who buys the fund today will receive the current distribution at the current yield and will not be negatively impacted by the events of the past. Let us investigate this.

Unfortunately, we do not have a particularly recent document that we can consult for the purpose of our analysis. The fund’s most recent financial report is the aforementioned semi-annual report that corresponds to the six-month period that ended on February 28, 2023. As such, it will not include any information about the fund’s performance over the past seven months. That is quite disappointing as quite a lot has happened during that period that could have a significant impact on the fund’s financial condition. After all, there was a fairly powerful bear market bounce in the first half of this year that was driven by optimism about rate cuts and the potential of artificial intelligence. I have also heard that some of it was driven by young traders who have never known an environment in which money is not freely obtainable. This strong market could have provided the potential for capital gains, although that optimism appears to have died off now and the new mantra needs to be about minimizing losses.

During the six-month period, the High Income Securities Fund received $4,571,493 in dividends and $234,492 in interest from the assets in its portfolio. This gives the fund a total investment income of $4,805,985 during the period. It paid its expenses out of this amount, which left it with $4,184,430 available to shareholders. This was, unfortunately, nowhere close to enough to cover the $7,236,575 that the fund actually paid out during the period. At first glance, this is quite concerning as the fund was not able to cover its distributions solely out of net investment income. The securities that this fund invests in primarily deliver their returns through direct payments to the shareholders, so this full coverage is something that we would certainly like to see.

With that said, there are some other ways through which the fund can obtain the money that it needs to cover its distributions. For example, it might have been able to sell some appreciated securities and realize capital gains that could be paid out. In addition, some closed-end funds make return of capital distributions that would not be considered part of net investment income but still represent money coming into the fund.

Unfortunately, the fund generally failed at that task during the period. During the six-month period, it reported net realized losses of $1,828,955 accompanied by $794,109 net unrealized losses. Overall, the fund’s net assets declined by $5,675,209 during the period. This certainly explains the distribution cut at the start of this year, as the fund also failed to cover its distribution during the preceding full-year period. It remains to be seen how sustainable the fund’s current distribution will be, as that information will not be available to us until the fund releases its annual report sometime in the next four weeks or so.

Valuation

As of September 29, 2023 (the most recent date for which data is currently available), the High Income Securities Fund has a net asset value of $7.26 per share but the shares trade for $6.04 each. That gives the shares a whopping 16.80% discount on net asset value at the current price. This is a very attractive discount that greatly surpasses the 9.02% average discount that the shares have had over the past month. As such, the price appears to be quite reasonable right now.

With that said, it is important to note that the fund does not report its net asset value daily. It is perhaps the only closed-end fund on the market that does not provide daily updates. The market in general has fallen quite a bit since September 29, so it is uncertain what exactly the fund’s discount is at the moment. It is probably less than the 16.80% implied above, but it is probably still trading at a discount on net asset value.

Conclusion

In conclusion, the High Income Securities Fund is one of the few closed-end funds that seek to provide a high level of income to its investors without investing in the traditional portfolio of bonds or preferred stock. It actually does fairly well at this task, as most of the assets in its portfolio have far higher yields than even junk bonds. This provides the fund itself with a high level of income, but it still pays out more than its net investment income, which presents problems in a market in which capital gains may be difficult to come by.

For further details see:

PCF: A Good Diversifier For An Income Portfolio, But Distribution Appears Strained