PCK - PCK: The Discount To NAV Is Not Enough To Remain Bullish (Rating Downgrade)

2023-08-17 02:50:52 ET

Summary

- PIMCO California Municipal Income Fund II has struggled throughout 2023 despite a widened discount to NAV.

- The fund's inability to attract buyers at its discounted price is a cause for concern.

- Income metrics from PCK are alarming, raising doubts about the sustainability of its income stream.

Main Thesis & Background

The purpose of this article is to evaluate the PIMCO California Municipal Income Fund II ( PCK ) as an investment option at its current market price. The PCK CEF invests primarily in California municipal bonds, and therefore "seeks to provide current income, which is exempt from federal and California income tax, as well as the alternative minimum tax."

Back in January the fund was coming off a bad stretch. It had been seeing a negative return anyway and then got hammered by a distribution cut. While painful for current investors, I saw it as an opportunity . I thought the sell-off was getting a bit overblown and investors would rotate back in for value. In short, I was wrong, and PCK has continued to struggle throughout 2023:

Fund Performance (Seeking Alpha)

After taking another look at PCK, it would be easy to remain bullish. The fund's discount to NAV has expanded and I generally have a positive outlook for fixed-income as a whole under current market conditions. However, I remain concerned about the sustainability of the income stream, especially after the most recent UNII report from PIMCO this month. The fund's extensive use of leverage is also a problem while the yield curve stays inverted. Because of these headwinds (and others) I think a downgrade to "neutral" makes sense.

Discount Has Not Brought In Buyers, Only Widened

Much of the rationale for downgrading my outlook here has to do with the fund's inability to use its valuation to draw in prospective buyers. Back in January I saw a sell-off occurring that looked a bit too steep. The fund still had an attractive yield at current valuations - especially for highly taxed California residents. With a discount near 5%, I saw a strong case for buying in.

However, the market did not agree with me. Rather than use that discount gap as a reason to buy, investors simply widened to the level of almost 10% that we see today:

Current Valuation (PIMCO)

Now this is an important metric because it is hard for me to be "bearish" with such a steep discount. This is especially true when its sister funds (PCQ and PZC) have valuations of a 3% discount and 3% premium, respectively.

This is not meant to be double-speak but simply to manage expectations. I am not trying to be almost here. A discount this wide very well could attract attention. It may also cause some investors in PCQ or PZC to rotate given the relative value. But I am no longer bullish here because it has been clear in 2023 that PCK's discount is not enough to really get momentum going. That could change, but I am not willing to bank on it anytime soon.

Income Metrics Quite Alarming

The next topic is income - which is of course of critical importance for PCK investors. Sadly, the distribution cut back in January may not have been enough to solve the fund's problems. Today (8/16), PIMCO released the most updated UNII figures and it shows PCK is struggling in a big way:

{kind=link}

The fund has rough 3 months of income in arrears and its coverage ratios suggest improvement is a long way off. This makes it difficult for me to stay bullish because another cut remains in the cards.

The problem is we are in the same old situation with the same old story unfolding. PCK simply uses too much leverage and it has not delevered in 2023 as it should have. At 44% leverage, this puts the fund in a very difficult spot. Short-term borrowing costs have continued to rise this calendar year, meaning PCK has had to shell out more money to continue borrowing at this level. Yet, the yield curve remains steeply inverted, limiting the opportunity for PIMCO managers to earn higher income at the longer end of the curve:

Yield Curve Inversion Very Steep (St. Louis Fed)

My followers know I am very reluctant to add a lot of leverage to my portfolio as long as this backstory continues. With the Fed looking to maintain rates at current levels in the short-term, it is difficult to forecast PCK improving its income production. While the current yield looks attractive on the surface, we have to consider how attractive it will be if it gets cut:

Latest Distribution (PCK) (Seeking Alpha)

Ultimately I can't get behind this income story at the moment. There are other reasons to like PCK - such as the discount and broader optimism around California's muni bonds. But when it comes to the income stream, the leverage and yield curve inversion are going to continue to pressure it. That is a difficult hurdle to overcome and probably explains why investors have not bid this fund up out of discount territory yet.

Holdings Are High Quality

Of course, the story behind PCK is not all bad. One of the positives is the credit quality of the underlying holdings. Aside from that, it is quite diversified. While the largest sector is state and local GO (general obligation) bonds, PCK holds exposure across a variety of areas:

Sector Breakdown (PIMCO)

California has been making news recently because of its budget deficit - a far cry from the surplus it enjoyed in very recent memory. But the state still has a strong credit rating and a history of making good on its obligations. And I like that PCK holds a lot of GO bonds, as opposed to revenue bonds, because the state's finances will likely recover this year as income tax collections remain high along with rising equity markets.

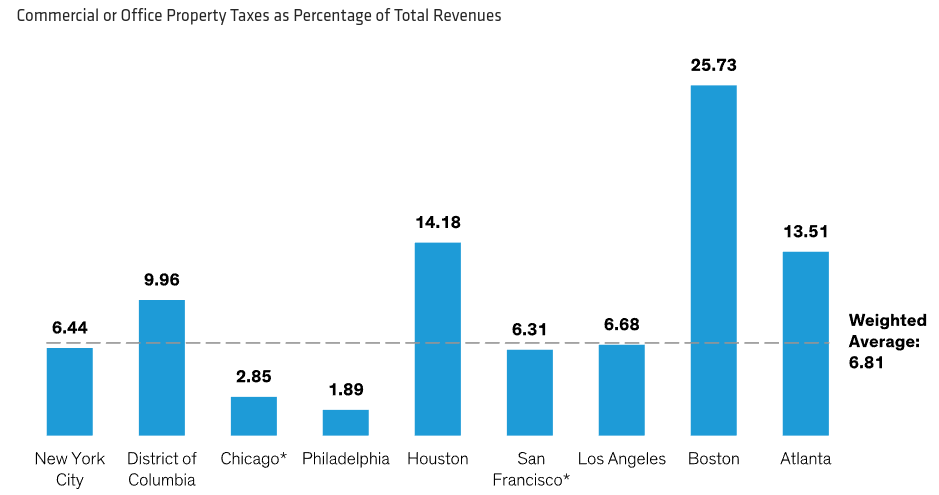

Another headline item beyond the deficit is one that is impacting a lot of different states and cities around the country. This is declining office occupancy, which has certainly become the norm in many cities that rely on white-collar workers. The fear (for muni investors) is that a decline in office occupancy could result in lower property values and, as a result, lower tax revenue streams. While office vacancies are certainly something to monitor, the truth is that California as a whole is not overly reliant on commercial office buildings for their coffers.

Bear in mind, I am not suggesting this theme is not something to monitor. It is for California and for any state in the US that is seeing an uptick in remote work. But this ties back to PCK because California's largest cities actually rely less on this revenue stream than the national average:

Property Taxes As Percent Of Total Revenue (Commercial/Office space only) (AllianceBernstein)

{kind=link}

As the graphic clearly shows, neither San Francisco or Los Angeles are any more at-risk of this trend than the average US city. In fact, their reliance on office space taxes is actually slightly less than your average US city.

My takeaway here is not to suggest this isn't going to pose any sort of problem down the line. But rather it is to keep things in perspective. California is not going to see a sudden depletion in revenue if more workers continue to work remote. The state's reliance (and individual city's) on this source of revenue is very moderate and is not something to get alarmed about - yet. This tells me PCK is not at risk of a big drop going forward.

Being Selective Is Important

My final point relates back to the leverage discussion I had earlier. I want to emphasize this point because there is more to just out-sized swings in share price when a leveraged play doesn't work out. As short-term rates have spiked, borrowing costs have simultaneously risen. This is a problem not for management in truth - but rather for the owners/investors of this fund and others like it.

What I mean by this is that fund managers get paid for assets under management. They do not (generally) make a lot more just because a fund does well and certainly don't make less because a fund does poorly. The caveat is that if assets drop (or rise) because of poor performance (strong performance) that could meander its way in to compensation.

But the on-the-surface, upfront costs of leverage are borne by you and I in the form of expenses. When short-term borrowing costs rise, fund managers do not eat this expense - they pass it on to you! The net result is this is a very expensive way to access the muni market right now:

Expense Ratios (PCK) (PIMCO)

{kind=link}

What I draw from this is that PCK is going to have to really deliver to make it worth this expense and so far in 2023 that has not been happening. I don't see a lot changing on a macro-level to really want to remain bullish on this fund given the recent losses. This in a nutshell is central to why a downgrade is the right move at this time in my opinion.

Bottom-line

PCK has not drawn in many buyers despite a healthy discount to NAV. The net result of poor income metrics, heavy use of leverage, and negative headlines about California's budget situation are all pressuring the fund. While some of these claims - especially those tied to California's credit quality - are a bit overblown in my view that is not enough to get me excited about this muni CEF. Therefore, I am not "neutral" on this fund and encourage readers to approach any new positions very selectively.

For further details see:

PCK: The Discount To NAV Is Not Enough To Remain Bullish (Rating Downgrade)