PCM - PCM: Small CEF Trading At Wide Premium To NAV

2023-08-12 03:57:47 ET

Summary

- PCM Fund Inc. is a small closed-end fund from Pimco that aims to deliver high current income from a portfolio of credit instruments like MBS and high yield bonds.

- PCM Fund has delivered modest returns in recent years due to a poor 2022 performance.

- My main concern with the PCM fund is its 14.3% of NAV distribution yield, which appears far too high relative to the fund's earnings power.

- Furthermore, the fund is trading at an unsustainable ~50% premium to NAV. While the premium may not collapse overnight, long-term investors could be at risk.

Recently, while screening for high yielding fixed income funds, I came across the PCM Fund Inc. (PCM). PCM is an under-the-radar credit fund offered by Pimco that pays an attractive 9.7% distribution yield.

However, upon further review of the fund, I am concerned that fund's distribution yield is actually 14.3% on NAV, which appears far too high compared to what the fund has earned historically. Furthermore, the PCM fund is trading at a steep 47.5% premium to NAV, which makes the unit price of the fund vulnerable. I would personally avoid the PCM fund.

Fund Overview

The PCM Fund Inc. is a small closed-end fund ("CEF") from Pimco that aims to deliver high current income from a portfolio of various credit instruments including agency guaranteed mortgage-backed securities ("MBS"), private label MBS, investment grade corporate bonds, high yield corporate bonds, and commercial MBS.

As of June 30, 2023, the PCM fund had $81 million in net assets and 45% effective leverage. The PCM fund charges a 2.3% total expense ratio.

Portfolio Holdings

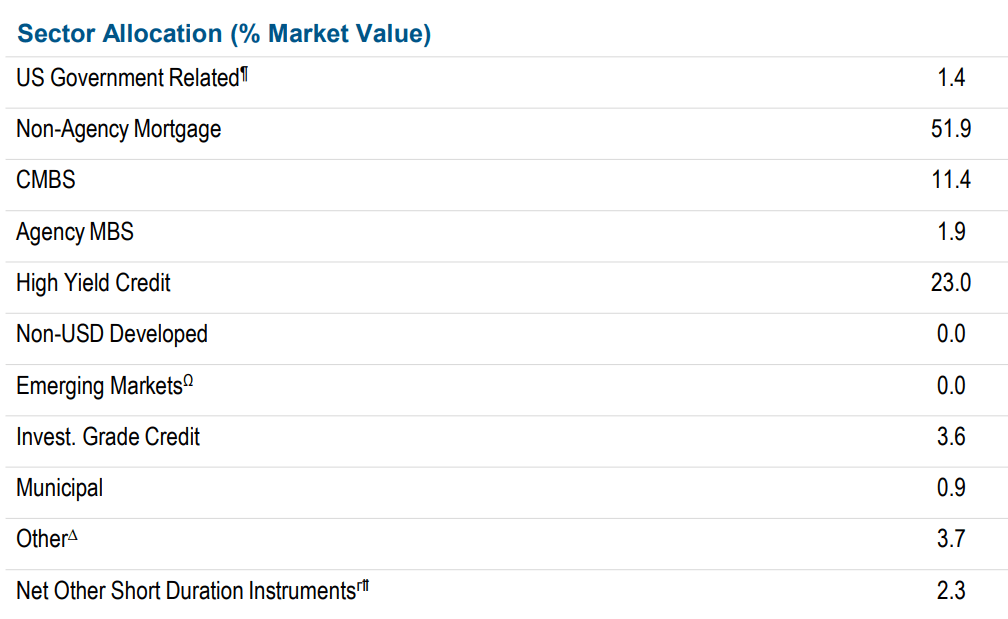

Figure 1 shows the sector allocation of the PCM fund. The PCM fund's largest sector allocations are non-agency MBS (51.9%), high yield bonds (23.0%), and commercial MBS (11.4%).

{kind=link}

Figure 2 shows the maturity allocation of the PCM fund. The vast majority of PCM's investments are shorter duration, with a total leverage adjusted duration of 3.9 years for the portfolio.

{kind=link}

Unfortunately, the PCM fund does not show a breakdown of the fund's credit quality allocation, so it is difficult to fully analyze the risks to the fund.

Returns

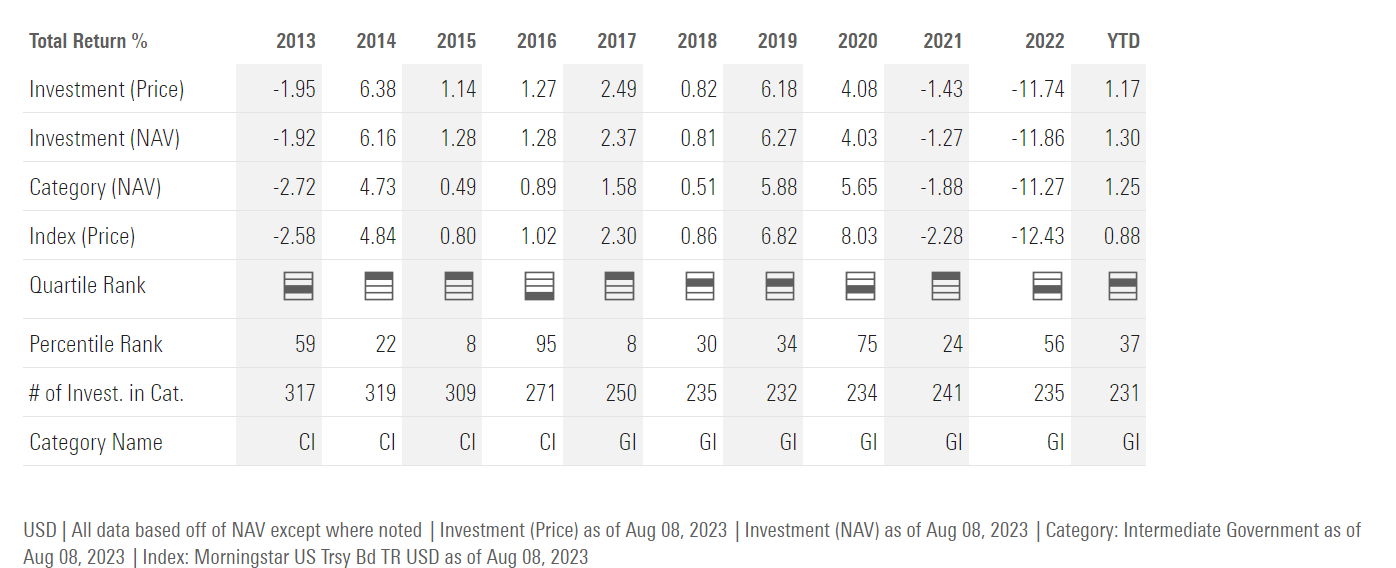

Figure 3 shows the historical returns of the PCM fund. The PCM fund has delivered modest returns in the past few years with 3 and 5Yr average annual returns of only 3.4% and 2.5% respectively to July 31, 2023. However, PCM's long-term returns have been better, with 10 and 15Yr average annual returns of 5.7% and 9.5%.

{kind=link}

The main issue with PCM's historical returns appear to be 2022, when the fund lost 16.5% of NAV as the Federal Reserve raised interest rates to combat inflation, leading to mark to market losses for many fixed income securities. Excluding 2022, the average annual return for the PCM fund from 2013 to 2021 was a solid 8.7%.

Although PCM's losses in 2022 appear large in isolation, they are roughly inline with other credit investments. For example, the iShares MBS ETF (MBS) lost 11.9% in 2022 (Figure 4).

{kind=link}

Similar, the iShares iBoxx $ High Yield Corporate Bond ETF (HYG) lost 11.4% in 2022 (Figure 5).

{kind=link}

Given the levered nature of PCM's portfolio, it is not too surprising that PCM's losses in 2022 surpassed those of the individual unlevered sectors.

Distribution & Yield

The PCF fund pays an attractive monthly distribution, currently set at $0.08 / month or a forward yield of 9.7% on market price.

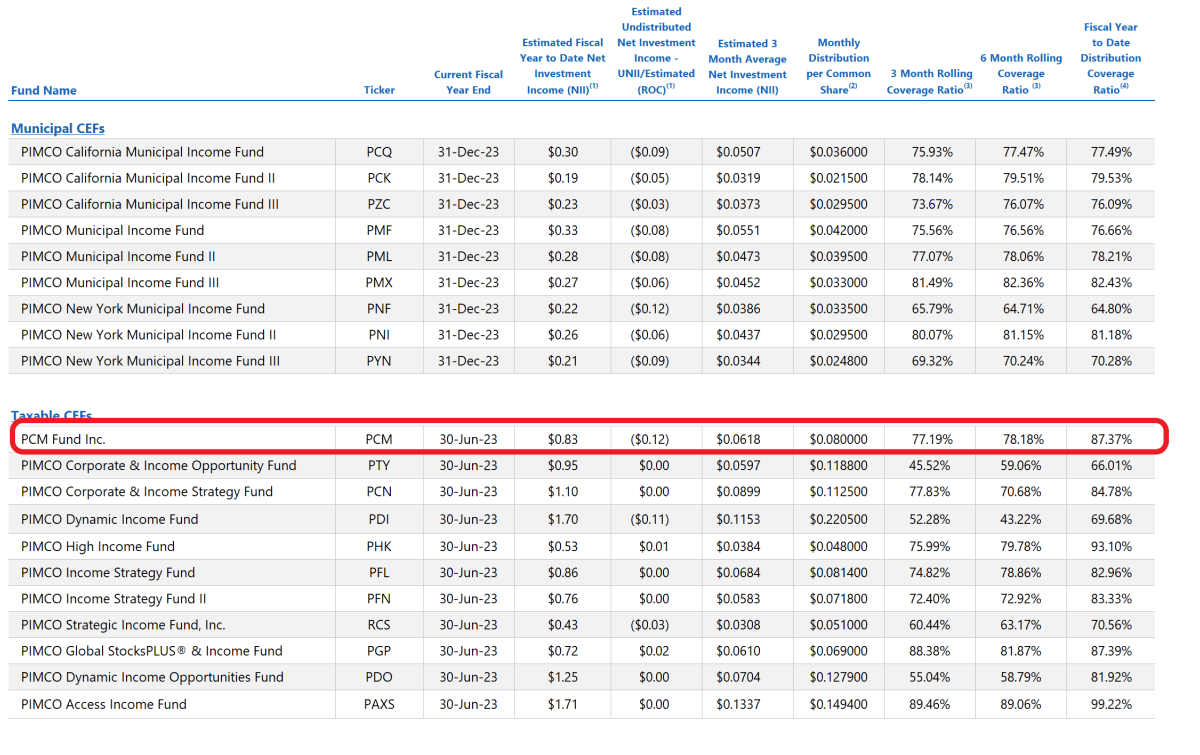

However, there are potential issues I have with the PCM fund's distribution. First, if we look at the fund's most recent 'UNII report' , we can see that the PCM fund's distribution is not fully covered by its net investment income ("NII") (Figure 6). The 3-month rolling coverage is 77.2% and the fiscal YTD coverage is 87.4% as of June 1, 2023.

Figure 6 - PCM's distribution is not covered by NII (pimco.com)

{kind=link}

Large Premium To NAV Warrants Caution

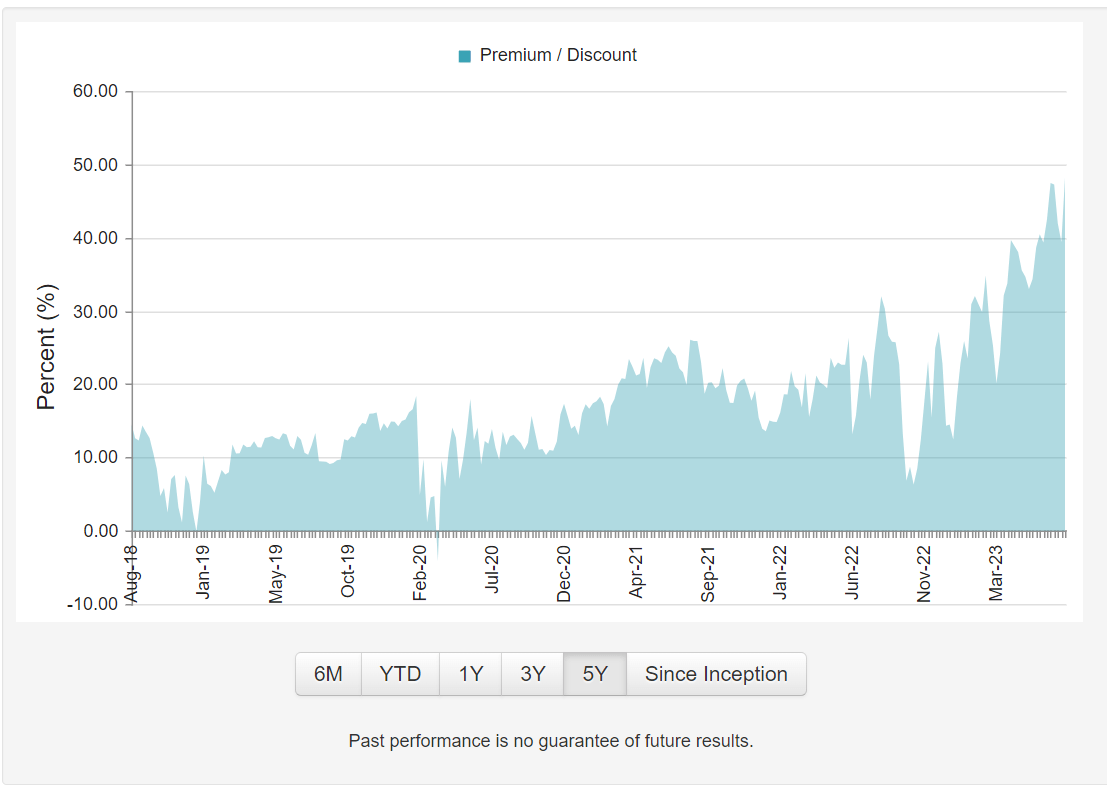

More importantly, the PCM fund trades at a steep 47.5% premium to NAV, so on a NAV basis, the PCM fund is actually paying a forward distribution yield of 14.3% (Figure 7).

Figure 7 - PCM is trading at a large premium to NAV (cefconnect.com)

{kind=link}

Comparing PCM's distribution yield on NAV to the fund's historical returns of 5.7% over 10 years, we can see a large gap between earnings and yield. This suggests the PCM fund is an amortizing 'return of principal' fund does not earn its distribution.

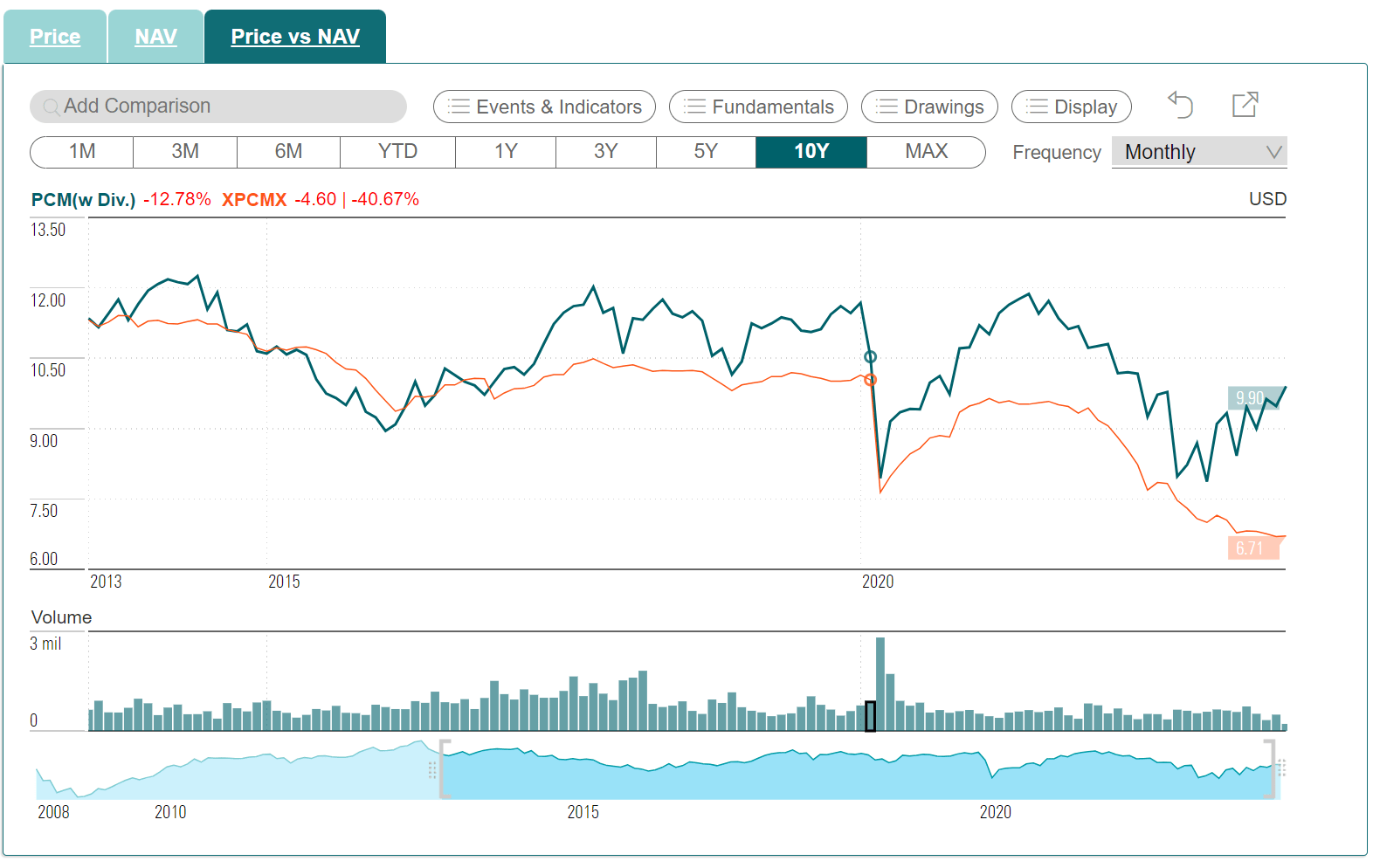

My thesis is confirmed by an analysis of PCM's long-term NAV performance, which shows the fund's NAV has shrunk from over $11 / share in 2013 to $6.71 today (Figure 8).

Figure 8 - PCM has a shrinking historical NAV, characteristic of return of principal funds (cefconnect.com)

{kind=link}

Although the fund's market price has declined less than its NAV, this is purely a function of the premium to NAV increasing, from basically trading at NAV in 2013 to ~50% premium to NAV today.

While investment funds can maintain a large premium to NAV for a long time so long as unitholders do not sell their shares en masse, the situation is ultimately untenable.

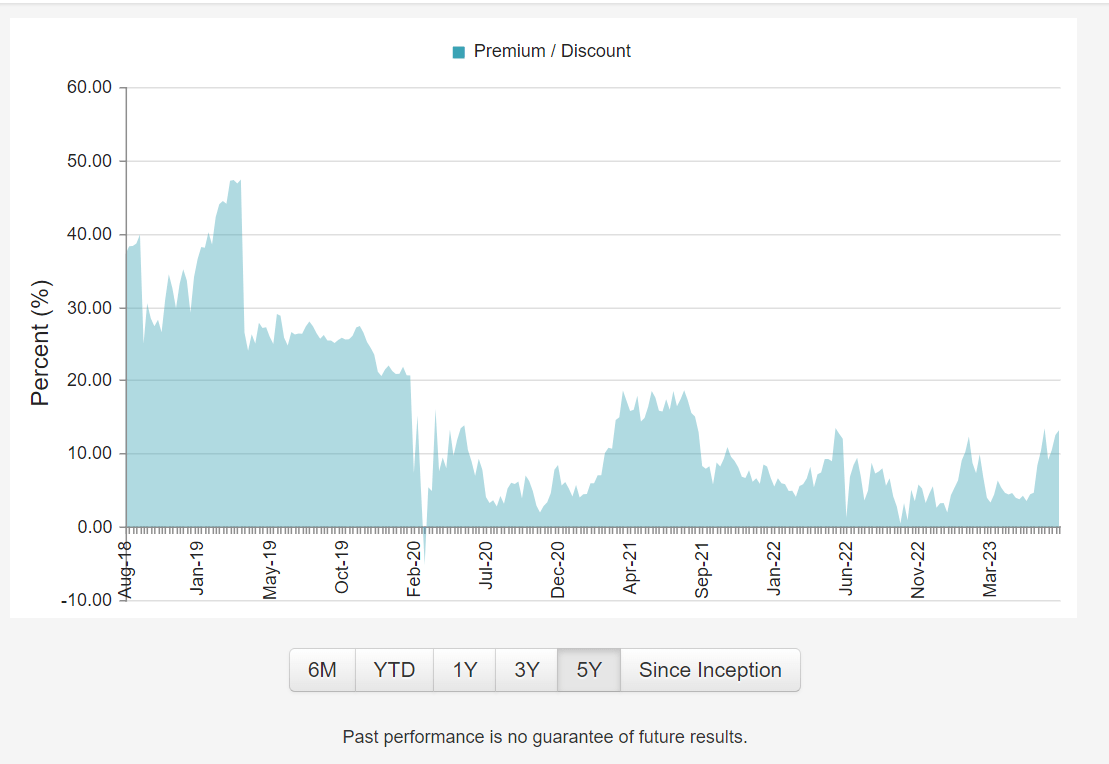

For example, the Pimco High Income Fund (PHK) have historically traded at a very wide premium to NAV for many years before the fund had to cut distributions in 2019. Ultimately, its ~40% premium to NAV collapsed to virtually nil as unitholders exited (Figure 9).

Figure 9 - PHK is another Pimco fund that had a large premium to NAV go away as distributions were cut (cefconnect.com)

{kind=link}

While I am not predicting an overnight collapse in PCM's premium to NAV, it is certainly a risk worth monitoring.

Conclusion

The PCM fund is a small MBS and junk-bond focused credit fund from Pimco. Historically, the fund had delivered solid total returns, although short-term returns have been marred by a weak 2022.

My main concern with the PCM fund is its 14.3% of NAV distribution, which appears far too high compared to the fund's historical earnings power. Furthermore, the fund is trading at a steep 47.5% premium to NAV. I would personally avoid the PCM fund.

For further details see:

PCM: Small CEF Trading At Wide Premium To NAV